Automotive Cyber Security Market

Automotive Cyber Security Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702853 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

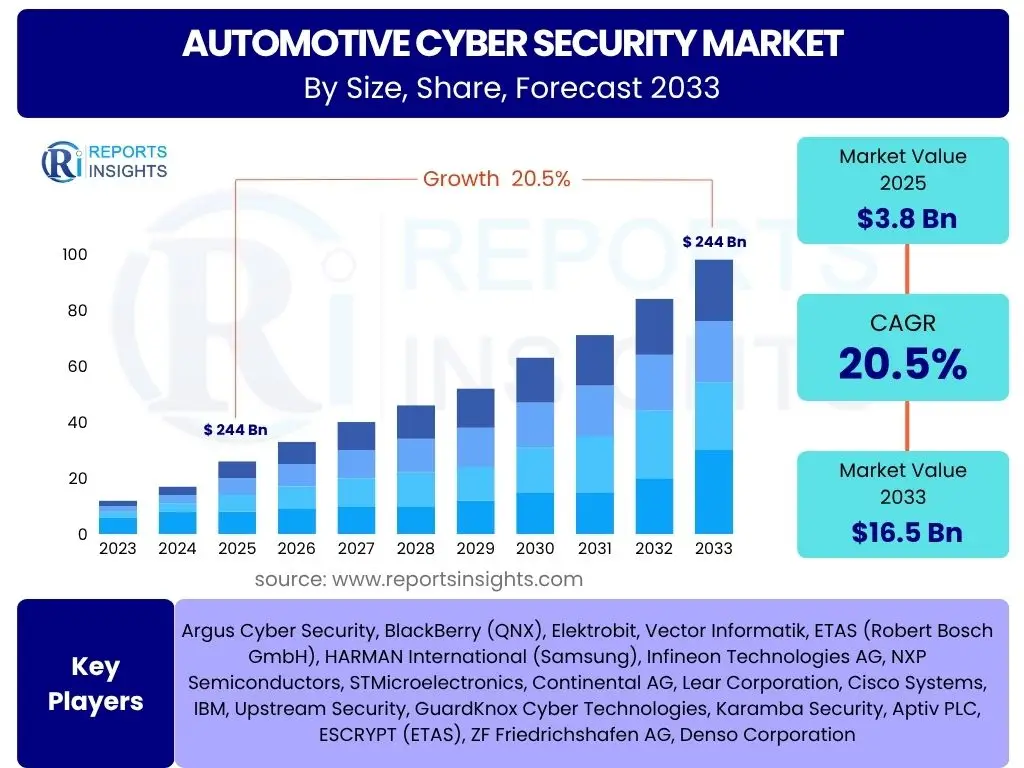

Automotive Cyber Security Market Size

According to Reports Insights Consulting Pvt Ltd, The Automotive Cyber Security Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 20.5% between 2025 and 2033. The market is estimated at USD 3.8 Billion in 2025 and is projected to reach USD 16.5 Billion by the end of the forecast period in 2033.

Key Automotive Cyber Security Market Trends & Insights

The Automotive Cyber Security market is experiencing rapid evolution driven by the increasing connectivity and complexity of modern vehicles. Key trends indicate a significant shift towards software-defined vehicles, requiring robust cybersecurity measures integrated throughout the vehicle's lifecycle. Users are increasingly concerned about data privacy, vehicle integrity against remote attacks, and the secure implementation of advanced features like over-the-air (OTA) updates and autonomous driving. This necessitates proactive threat intelligence, real-time intrusion detection, and continuous vulnerability management to protect against an ever-evolving threat landscape.

Another prominent insight is the growing emphasis on regulatory compliance, with global standards like UN R155 and ISO/SAE 21434 mandating comprehensive cybersecurity management systems for vehicle manufacturers and suppliers. This regulatory pressure is compelling the industry to adopt a security-by-design approach, moving cybersecurity from an afterthought to a foundational element of vehicle development. The convergence of IT and OT security practices is also becoming critical, addressing vulnerabilities that span traditional IT networks within the vehicle to operational technologies controlling core vehicle functions. Furthermore, the expansion of the connected car ecosystem, including V2X communication, introduces new attack surfaces that require innovative, multi-layered security solutions.

- Increasing adoption of software-defined vehicles and vehicle-to-everything (V2X) communication.

- Rising sophistication of cyber threats targeting vehicle systems and data.

- Growing emphasis on regulatory compliance with standards like UN R155 and ISO/SAE 21434.

- Integration of advanced security features for Over-the-Air (OTA) updates.

- Shift towards holistic, end-to-end security architectures across the automotive supply chain.

AI Impact Analysis on Automotive Cyber Security

User inquiries about AI's impact on automotive cybersecurity frequently revolve around its potential to enhance threat detection and response capabilities, as well as the inherent risks associated with AI being exploited for malicious purposes. There is a strong expectation that AI will significantly improve the efficiency of identifying complex attack patterns and anomalies that traditional rule-based systems might miss. Users are keen to understand how AI can provide predictive analytics for emerging threats, automate security operations, and adapt defenses in real-time against dynamic cyberattacks, ultimately bolstering the resilience of connected and autonomous vehicles.

Conversely, concerns persist regarding the vulnerability of AI models themselves to adversarial attacks, where subtle manipulations can lead to misclassifications or bypassed defenses. Users also question the ethical implications and potential for bias in AI-driven security systems, as well as the complexity of validating and certifying AI-powered cybersecurity solutions for safety-critical automotive applications. The balance between leveraging AI's analytical power for defense and mitigating its potential as a tool for sophisticated attacks remains a central theme, highlighting the need for robust AI governance, explainability, and continuous testing within the automotive cybersecurity domain.

- Enhanced real-time threat detection and anomaly identification through machine learning algorithms.

- Predictive analytics for anticipating and mitigating emerging cyber threats.

- Automation of security operations and incident response, reducing human intervention.

- Potential for AI-powered adversarial attacks, requiring robust AI defense mechanisms.

- Development of adaptive security systems that learn and evolve with the threat landscape.

Key Takeaways Automotive Cyber Security Market Size & Forecast

Common user questions about the Automotive Cyber Security market size and forecast reveal a strong interest in understanding the primary growth drivers, the longevity of market expansion, and the critical factors that will shape its future. Users are looking for assurances regarding the market's resilience against evolving threats and economic fluctuations, as well as insights into which technological advancements will most significantly contribute to its projected growth. There is a clear demand for understanding the long-term viability and investment potential within this rapidly expanding sector, emphasizing the necessity of proactive security measures as vehicles become more connected and autonomous.

The core insights indicate that the market is poised for sustained, significant growth, primarily fueled by stringent regulatory mandates, the proliferation of connected and electric vehicles, and the increasing sophistication of cyber threats. While challenges such as high implementation costs and the scarcity of skilled professionals persist, the overarching trend points towards an indispensable need for robust automotive cybersecurity solutions. The forecast suggests that continuous innovation in areas like AI-driven security, secure over-the-air updates, and supply chain integrity will be paramount for securing future mobility and realizing the full potential of smart vehicles.

- The market is projected for substantial growth, driven by increasing vehicle connectivity and autonomy.

- Regulatory compliance (e.g., UN R155) acts as a significant catalyst for market expansion.

- Continuous evolution of cyber threats necessitates dynamic and adaptive security solutions.

- Investment in secure software development and hardware-level security is critical.

- The demand for end-to-end cybersecurity solutions across the vehicle lifecycle will intensify.

Automotive Cyber Security Market Drivers Analysis

The Automotive Cyber Security market is significantly propelled by several concurrent factors that collectively create a compelling demand for robust security solutions. The proliferation of connected vehicles, equipped with extensive Internet of Things (IoT) capabilities, dramatically expands the attack surface, necessitating advanced cybersecurity measures to protect vehicle systems and user data. This increasing connectivity, coupled with the rising adoption of electric and autonomous vehicles, introduces complex software stacks and communication protocols, each requiring stringent security protocols to ensure operational integrity and safety. The inherent vulnerability of these sophisticated systems to remote attacks and data breaches underscores the urgent need for comprehensive automotive cybersecurity frameworks.

Furthermore, stringent regulatory frameworks and global standards play a pivotal role in driving market growth. Regulations such as UN R155 and ISO/SAE 21434 mandate that vehicle manufacturers and their suppliers implement a comprehensive cybersecurity management system across the entire vehicle lifecycle, from design to post-production. These regulations impose legal obligations for cybersecurity assurance, pushing industry players to invest heavily in security technologies and practices. Additionally, the growing awareness among consumers regarding vehicle data privacy and safety concerns is exerting market pressure, compelling manufacturers to integrate advanced cybersecurity features as a key differentiator, thereby fueling market expansion.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Vehicle Connectivity and IoT Integration | +3.0% | Global | Long-term (2025-2033) |

| Stringent Cybersecurity Regulations (e.g., UN R155, ISO/SAE 21434) | +2.5% | Europe, North America, Asia Pacific | Mid-term (2025-2029) |

| Rising Sophistication and Frequency of Cyberattacks | +2.0% | Global | Ongoing (2025-2033) |

| Growth in Electric and Autonomous Vehicle Production | +1.8% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Increasing Consumer Awareness and Demand for Secure Vehicles | +1.5% | Global | Mid-term (2025-2029) |

Automotive Cyber Security Market Restraints Analysis

Despite the robust growth trajectory, the Automotive Cyber Security market faces several significant restraints that could impede its full potential. One primary challenge is the high cost associated with implementing comprehensive cybersecurity solutions across the entire automotive value chain. Developing and integrating advanced security hardware, software, and services, coupled with the need for continuous monitoring and updates, represents a substantial financial burden for manufacturers and suppliers, particularly for smaller entities. This cost factor can lead to slower adoption rates, especially in price-sensitive markets or for legacy vehicle platforms that require extensive retrofitting.

Another major restraint is the pervasive shortage of skilled cybersecurity professionals with specialized automotive expertise. The unique blend of automotive engineering knowledge, embedded systems security, and traditional IT cybersecurity skills is rare, creating a talent gap that hinders the effective development, deployment, and management of robust security solutions. This shortage can lead to delayed implementation, reliance on external consultants, and an increased risk of vulnerabilities due to inadequate in-house capabilities. Furthermore, the lack of universal standardization across different vehicle architectures and communication protocols complicates the development of interoperable security solutions, creating fragmentation and hindering broader market adoption.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Implementation and Maintenance Costs | -1.2% | Global | Mid-term (2025-2029) |

| Shortage of Skilled Cybersecurity Professionals | -1.0% | Global | Long-term (2025-2033) |

| Lack of Industry-Wide Standardization and Interoperability | -0.8% | Global | Mid-term (2025-2029) |

| Complexity of Integrating Security into Legacy Systems | -0.7% | Developing Regions | Short-term (2025-2027) |

Automotive Cyber Security Market Opportunities Analysis

The Automotive Cyber Security market presents numerous lucrative opportunities driven by evolving technological landscapes and increasing industry focus on holistic security. The rapid advancement of V2X (Vehicle-to-Everything) communication, including V2V (Vehicle-to-Vehicle) and V2I (Vehicle-to-Infrastructure), creates a substantial demand for specialized security solutions that can protect these new communication channels from eavesdropping, spoofing, and data manipulation. Companies developing innovative cryptographic protocols, secure authentication mechanisms, and intrusion prevention systems for V2X environments are well-positioned to capitalize on this expanding segment. This includes securing smart city infrastructure interactions and enhancing traffic management systems.

Another significant opportunity lies in the burgeoning field of AI and Machine Learning applications within cybersecurity. AI can be leveraged for proactive threat intelligence, anomaly detection, and automated incident response, providing a crucial advantage in combating sophisticated, polymorphic attacks that traditional signature-based methods might miss. The development of post-quantum cryptography also presents a long-term opportunity, as quantum computing threatens to break current cryptographic standards, necessitating the development of future-proof security algorithms for automotive systems. Furthermore, the growing trend of offering automotive cybersecurity as a managed service allows OEMs and suppliers to outsource complex security operations, creating new revenue streams for specialized cybersecurity firms.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of V2X Security Solutions | +2.5% | Global | Mid-term (2025-2029) |

| Leveraging AI/ML for Advanced Threat Detection and Prevention | +2.0% | Global | Long-term (2025-2033) |

| Expansion of Managed Security Services for Automotive OEMs | +1.8% | North America, Europe | Mid-term (2025-2029) |

| Implementation of Post-Quantum Cryptography | +1.5% | Global (Research & Development Focus) | Long-term (2030-2033) |

| Growth in Automotive Security Consulting and Auditing Services | +1.2% | Global | Ongoing (2025-2033) |

Automotive Cyber Security Market Challenges Impact Analysis

The Automotive Cyber Security market is continually challenged by the dynamic and rapidly evolving nature of the threat landscape. Cybercriminals and state-sponsored actors are constantly developing more sophisticated attack vectors, including zero-day exploits, supply chain attacks, and ransomware, which target the complex interconnected systems within modern vehicles. Keeping pace with these evolving threats requires continuous investment in research and development, frequent software updates, and advanced threat intelligence, posing a significant operational and financial challenge for the industry. The sheer volume and diversity of potential attack surfaces, from infotainment systems to critical powertrain components, further complicate comprehensive security efforts.

Another critical challenge is the inherent vulnerability of the automotive supply chain. A vehicle's components, software, and services are sourced from a vast network of suppliers, each presenting potential entry points for attackers. Ensuring end-to-end security requires rigorous cybersecurity assessments and compliance across all tiers of the supply chain, a complex undertaking that demands robust governance and contractual agreements. Furthermore, managing the long lifecycle of vehicles, often extending beyond a decade, poses a significant challenge for delivering continuous security updates and patching vulnerabilities post-sale, especially for vehicles not equipped with robust over-the-air (OTA) update capabilities. This makes securing existing fleets a continuous and resource-intensive endeavor.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapidly Evolving and Sophisticated Threat Landscape | -1.5% | Global | Ongoing (2025-2033) |

| Securing the Complex Automotive Supply Chain | -1.0% | Global | Long-term (2025-2033) |

| Ensuring Post-Sales Security Updates and Vulnerability Management | -0.9% | Global | Mid-term (2025-2029) |

| Maintaining Security Across Diverse Vehicle Platforms and Architectures | -0.8% | Global | Ongoing (2025-2033) |

Automotive Cyber Security Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Automotive Cyber Security market, covering critical aspects such as market size, historical data, and future forecasts. It delves into key market trends, significant drivers, prevailing restraints, emerging opportunities, and inherent challenges that shape the industry landscape. The report offers a detailed segmentation analysis, breaking down the market by various categories, along with a thorough regional assessment to highlight geographical market dynamics. Additionally, it includes profiles of leading companies, offering insights into the competitive environment and strategic initiatives of key players in the global automotive cybersecurity domain.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.8 Billion |

| Market Forecast in 2033 | USD 16.5 Billion |

| Growth Rate | 20.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Argus Cyber Security, BlackBerry (QNX), Elektrobit, Vector Informatik, ETAS (Robert Bosch GmbH), HARMAN International (Samsung), Infineon Technologies AG, NXP Semiconductors, STMicroelectronics, Continental AG, Lear Corporation, Cisco Systems, IBM, Upstream Security, GuardKnox Cyber Technologies, Karamba Security, Aptiv PLC, ESCRYPT (ETAS), ZF Friedrichshafen AG, Denso Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Cyber Security market is segmented to provide a granular understanding of its diverse components and growth avenues. This segmentation allows for precise analysis of market dynamics across various dimensions, including the type of security implemented, specific vehicle applications, vehicle types, connectivity methods, underlying components, and deployment models. Each segment represents distinct technological requirements, threat vectors, and market demands, influencing investment and development strategies within the industry. Understanding these sub-markets is crucial for identifying niche opportunities and developing targeted cybersecurity solutions that address the specific vulnerabilities inherent in different automotive systems.

This detailed segmentation not only highlights the areas of significant growth but also enables stakeholders to pinpoint regions and applications where cybersecurity investments are most critical. For instance, the demand for endpoint security is paramount for protecting individual electronic control units (ECUs), while network security is vital for safeguarding in-vehicle communication buses. Similarly, the unique security needs of autonomous vehicles differ significantly from those of conventional connected cars, necessitating specialized solutions. The component and deployment type segments offer insights into the preferred delivery mechanisms for cybersecurity, whether through integrated hardware, sophisticated software, or comprehensive managed services, and whether these are on-premise or cloud-based solutions.

- By Security Type:

- Endpoint Security

- Network Security

- Cloud Security

- Application Security

- Wireless Security

- By Application:

- ADAS & Safety Systems

- Infotainment Systems

- Telematics

- Powertrain Systems

- Body Electronics

- Others

- By Vehicle Type:

- Passenger Cars

- Commercial Vehicles

- By Connectivity:

- Vehicle-to-Everything (V2X)

- In-vehicle Network (CAN, Ethernet, LIN, FlexRay)

- External Cloud

- By Component:

- Software (Intrusion Detection/Prevention, Data Encryption, Secure Boot)

- Hardware (Secure Hardware Extensions, HSMs, Secure Elements)

- Services (Consulting, Integration, Maintenance, Managed Security Services)

- By Deployment Type:

- On-Premise

- Cloud-Based

Regional Highlights

- North America: This region is a leading market for automotive cybersecurity, driven by early adoption of connected and autonomous vehicle technologies, stringent regulatory frameworks, and the significant presence of key automotive OEMs and technology providers. The U.S. and Canada are at the forefront of implementing advanced cybersecurity measures, with a strong focus on research and development in secure vehicle architectures and V2X communication. The robust regulatory landscape and high consumer awareness regarding data privacy and vehicle safety also contribute to sustained market growth.

- Europe: Europe represents a crucial market segment, primarily due to the proactive regulatory environment, notably the UN R155 regulation, which mandates cybersecurity management systems for vehicle type approval. Countries like Germany, France, and the UK are investing heavily in cybersecurity solutions to comply with these regulations and to protect their advanced automotive manufacturing base. The region's strong emphasis on data protection and consumer privacy also fuels the demand for robust cybersecurity solutions integrated throughout the vehicle lifecycle.

- Asia Pacific (APAC): The APAC region is poised for significant growth in automotive cybersecurity, propelled by the rapid expansion of automotive production, particularly in China, Japan, and South Korea, and the increasing penetration of electric vehicles and smart mobility solutions. While regulatory frameworks are still evolving in some parts, the region's burgeoning middle class and growing demand for connected features are driving the adoption of cybersecurity solutions. Investment in domestic capabilities and strategic partnerships with global cybersecurity firms are also contributing to market expansion.

- Latin America: This region is an emerging market for automotive cybersecurity, characterized by increasing vehicle sales and growing connectivity in new car models. While cybersecurity awareness and regulatory frameworks are still developing compared to more mature markets, the need for basic security measures to protect against common cyber threats is growing. Countries like Brazil and Mexico are seeing initial investments in cybersecurity infrastructure as part of broader automotive industry modernization efforts.

- Middle East and Africa (MEA): The MEA region is experiencing gradual growth in the automotive cybersecurity market, primarily driven by government initiatives to develop smart cities and invest in transportation infrastructure. The increasing adoption of connected vehicles and the nascent development of autonomous driving projects in certain Gulf Cooperation Council (GCC) countries are creating a demand for cybersecurity solutions. However, challenges related to regulatory enforcement and technological maturity may influence the pace of adoption.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Cyber Security Market.- Argus Cyber Security

- BlackBerry (QNX)

- Elektrobit

- Vector Informatik

- ETAS (Robert Bosch GmbH)

- HARMAN International (Samsung)

- Infineon Technologies AG

- NXP Semiconductors

- STMicroelectronics

- Continental AG

- Lear Corporation

- Cisco Systems

- IBM

- Upstream Security

- GuardKnox Cyber Technologies

- Karamba Security

- Aptiv PLC

- ESCRYPT (ETAS)

- ZF Friedrichshafen AG

- Denso Corporation

Frequently Asked Questions

Analyze common user questions about the Automotive Cyber Security market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is automotive cybersecurity?

Automotive cybersecurity refers to the practices and technologies designed to protect vehicle electronic systems, communication networks, software, and data from malicious attacks, unauthorized access, manipulation, or damage. It encompasses securing everything from in-vehicle systems to external connections like cloud services and V2X communication.

Why is automotive cybersecurity important?

It is crucial for ensuring vehicle safety, functionality, and data privacy. Cyberattacks can lead to vehicle control compromises, theft of personal data, financial losses, and even threats to human lives. With increasing vehicle connectivity and autonomy, robust cybersecurity is indispensable to prevent catastrophic failures and maintain consumer trust.

What are the primary threats to automotive cybersecurity?

Key threats include remote vehicle hijacking, data theft from infotainment and telematics systems, ransomware attacks, exploitation of software vulnerabilities (e.g., via OTA updates), supply chain attacks injecting malicious code, and denial-of-service attacks targeting critical vehicle functions or external services.

How do regulations impact the automotive cybersecurity market?

Regulations like UN R155 and ISO/SAE 21434 mandate comprehensive cybersecurity management systems for vehicle manufacturers and suppliers. These regulations drive significant investment in security solutions, promote security-by-design principles, and accelerate the adoption of standardized cybersecurity practices across the industry, fundamentally shaping market demand and innovation.

How is AI transforming automotive cybersecurity?

AI enhances automotive cybersecurity by enabling real-time anomaly detection, predicting potential threats, and automating responses to cyberattacks. Machine learning algorithms can analyze vast amounts of data to identify sophisticated attack patterns, improve intrusion detection systems, and adapt defenses dynamically, offering a proactive approach against evolving cyber threats.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted