Automotive Coating Adhesive and Sealant Market

Automotive Coating Adhesive and Sealant Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708777 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

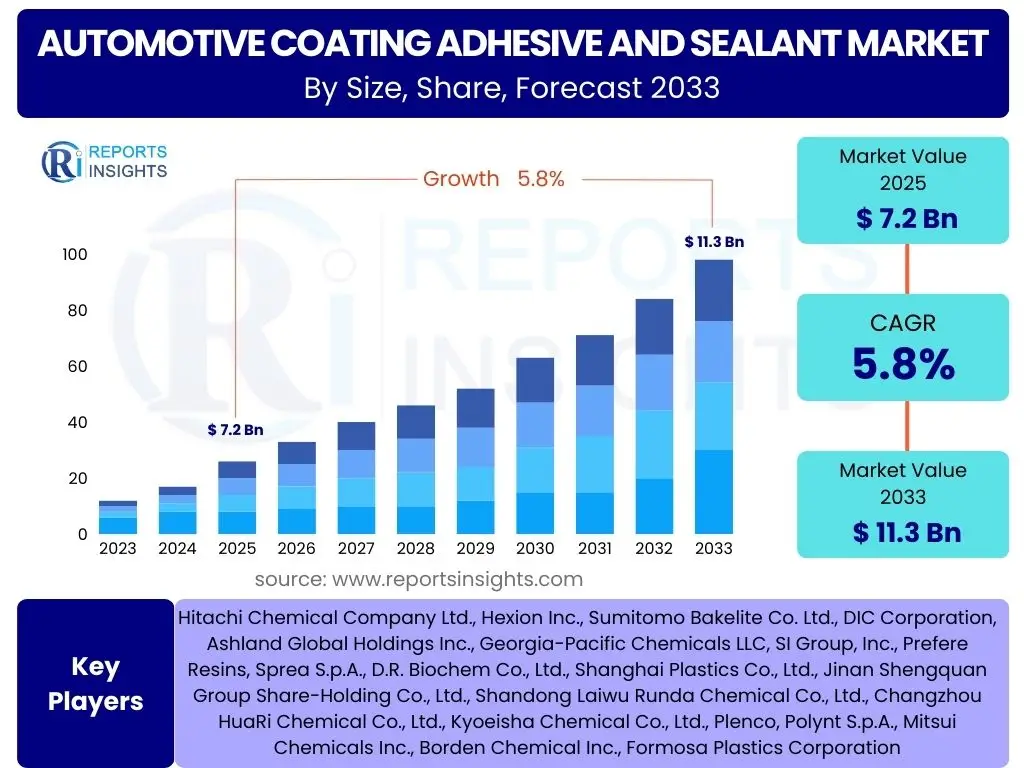

Automotive Coating Adhesive and Sealant Market Size

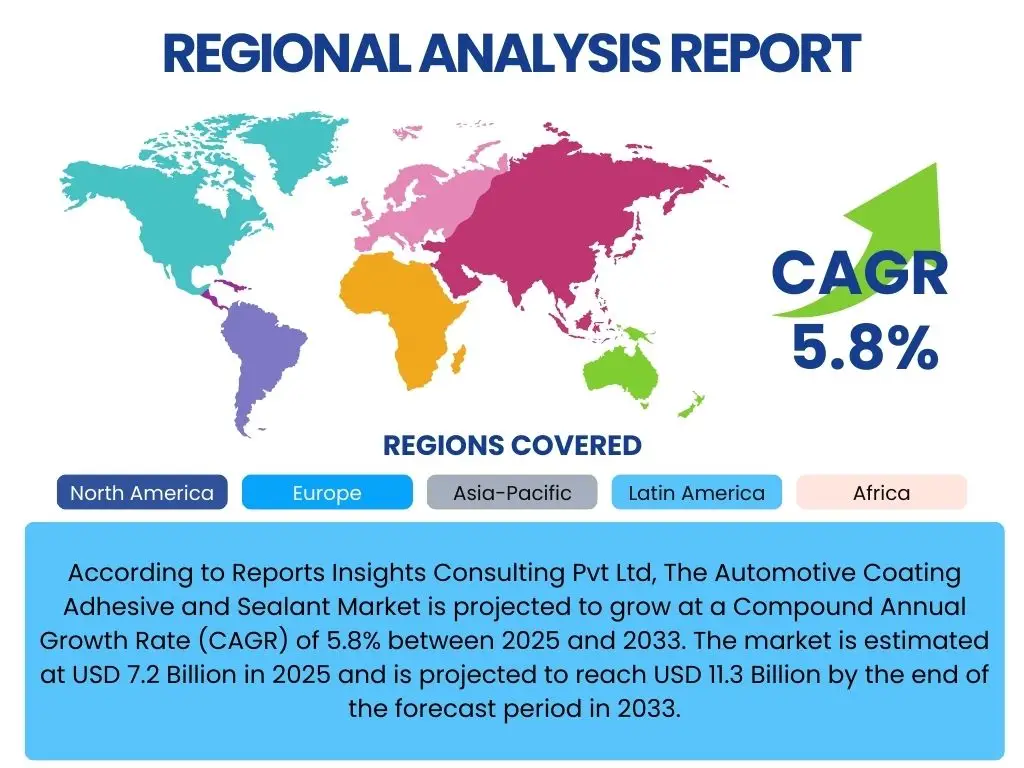

According to Reports Insights Consulting Pvt Ltd, The Automotive Coating Adhesive and Sealant Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 7.2 Billion in 2025 and is projected to reach USD 11.3 Billion by the end of the forecast period in 2033.

Key Automotive Coating Adhesive and Sealant Market Trends & Insights

Common user inquiries regarding market trends often center on the driving forces behind industry evolution, particularly concerning sustainability, technological advancements, and shifts in vehicle production. The market is experiencing significant transformation, propelled by the increasing global demand for lightweight and fuel-efficient vehicles. This demand directly influences the adoption of advanced adhesive and sealant technologies that reduce vehicle weight while maintaining structural integrity and enhancing safety features. The transition towards electric vehicles (EVs) is a critical trend, introducing new requirements for thermal management, battery structural bonding, and noise, vibration, and harshness (NVH) reduction, all of which rely heavily on specialized adhesives and sealants.

Another prominent trend is the growing emphasis on sustainable and eco-friendly solutions. Manufacturers are actively researching and developing bio-based, low-VOC (Volatile Organic Compound), and solvent-free adhesive and sealant formulations to comply with stringent environmental regulations and meet consumer demand for greener products. This push towards sustainability extends to the entire product lifecycle, from raw material sourcing to end-of-life considerations. Furthermore, the integration of automation and robotics in automotive manufacturing processes necessitates adhesives and sealants that offer rapid curing times and precise application capabilities, enhancing production efficiency and quality control.

- Increased adoption of lightweight materials, such as composites and advanced steels, necessitating high-performance structural adhesives.

- Rising demand for electric vehicles (EVs) driving innovation in battery bonding, thermal management, and electrical sealing solutions.

- Development of sustainable, bio-based, and low-VOC adhesive and sealant formulations due to stringent environmental regulations.

- Integration of advanced manufacturing technologies, including automation and robotics, requiring faster curing and more precise application.

- Growing focus on noise, vibration, and harshness (NVH) reduction in vehicles, enhancing passenger comfort and driving experience.

- Expansion of smart manufacturing and Industry 4.0 principles in automotive production lines.

AI Impact Analysis on Automotive Coating Adhesive and Sealant

User questions frequently address how artificial intelligence (AI) can revolutionize various aspects of the automotive coating, adhesive, and sealant industry, from optimizing product development to enhancing manufacturing efficiency and predictive maintenance. AI's influence is primarily observed in its capacity to accelerate material innovation by analyzing vast datasets of chemical compositions and their performance characteristics. This enables researchers to predict optimal formulations for specific applications, reducing the time and cost associated with traditional trial-and-error methods. AI-driven simulations can model how new materials will behave under diverse environmental conditions, thereby ensuring product reliability and durability before physical prototyping.

In manufacturing, AI plays a crucial role in process optimization and quality control. Machine learning algorithms can monitor production lines in real-time, detecting anomalies in application processes, curing conditions, or material consistency that might lead to defects. This proactive identification of issues minimizes waste, improves product quality, and enhances overall operational efficiency. Furthermore, AI can optimize supply chain logistics for raw materials, predicting demand fluctuations and potential disruptions, which is critical for an industry reliant on a stable supply of specialized chemicals. Predictive maintenance capabilities, powered by AI, can also extend the lifespan of manufacturing equipment, reducing downtime and maintenance costs.

- Accelerated material discovery and formulation optimization through AI-driven data analysis and predictive modeling.

- Enhanced quality control in manufacturing processes via real-time monitoring and anomaly detection using machine learning.

- Optimization of supply chain management for raw materials, improving inventory forecasting and logistics.

- Development of smart application systems using AI for precise and efficient adhesive and sealant dispensing.

- Predictive maintenance for manufacturing equipment, reducing downtime and operational costs.

- Personalization of adhesive and sealant solutions based on specific vehicle design and performance requirements.

Key Takeaways Automotive Coating Adhesive and Sealant Market Size & Forecast

Analyzing common user questions about market forecasts and key takeaways reveals a strong interest in identifying the primary growth catalysts, the most promising application segments, and the strategic implications for industry stakeholders. A significant takeaway is the robust growth trajectory projected for the market, driven by the expanding global automotive production, particularly in emerging economies, and the increasing sophistication of vehicle designs. The shift towards electric and autonomous vehicles represents a substantial growth area, as these vehicles require specialized bonding and sealing solutions for their advanced components, including batteries, sensors, and structural elements.

Another crucial insight is the intensifying focus on product innovation to meet evolving performance standards and environmental regulations. This includes the development of multi-functional adhesives and sealants that offer superior bonding strength, corrosion protection, sound dampening, and thermal management properties. The market is also characterized by a strong emphasis on sustainability, with manufacturers investing heavily in developing eco-friendly formulations that minimize environmental impact. For businesses, strategic partnerships and investments in research and development will be paramount to capitalize on emerging opportunities and maintain a competitive edge in this dynamic market.

- The market is poised for significant expansion, fueled by global automotive production increases and evolving vehicle technologies.

- Electric vehicle (EV) manufacturing is a critical growth segment, driving demand for specialized adhesives and sealants for battery packs and power electronics.

- Innovation in lightweighting and multi-functional materials will be essential for meeting future automotive design and performance requirements.

- Sustainability and environmental compliance remain key drivers for the development of bio-based and low-VOC formulations.

- Asia Pacific is expected to remain a dominant region, with significant growth also anticipated in North America and Europe due to technological advancements.

- Strategic collaborations and continuous investment in R&D are vital for companies to maintain competitiveness and capitalize on market opportunities.

Automotive Coating Adhesive and Sealant Market Drivers Analysis

The automotive coating, adhesive, and sealant market is propelled by a confluence of factors, primarily the escalating global demand for vehicles and the continuous evolution of automotive manufacturing processes. The increasing production volumes, particularly in developing economies, directly translate to a higher consumption of these materials for various vehicle components. Beyond sheer volume, the industry's shift towards advanced manufacturing techniques, such as modular assembly and lightweight construction, necessitates high-performance bonding and sealing solutions that offer superior strength, durability, and resistance to environmental factors.

A significant driver is the stringent regulatory landscape regarding vehicle safety, fuel efficiency, and environmental emissions. Adhesives and sealants play a critical role in achieving these objectives by enabling lightweighting through the use of advanced materials (e.g., composites, aluminum) and improving structural integrity, which contributes to enhanced crashworthiness. Furthermore, the rising adoption of electric and hybrid vehicles is creating new demand for specialized adhesives and sealants for battery assembly, thermal management, and vibration dampening, tailored to the unique requirements of electric powertrains. The continuous pursuit of enhanced passenger comfort and aesthetics also drives the demand for materials that reduce noise, vibration, and harshness (NVH) and provide superior finish quality.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing global automotive production and sales | +1.5% | Asia Pacific, North America, Europe | Short to Medium-term (2025-2029) |

| Rising demand for lightweight and fuel-efficient vehicles | +1.2% | Global | Medium to Long-term (2025-2033) |

| Growth in Electric Vehicle (EV) adoption and manufacturing | +1.8% | Europe, Asia Pacific (China), North America | Medium to Long-term (2025-2033) |

| Stringent environmental and safety regulations | +0.9% | Europe, North America, Japan | Short to Long-term (2025-2033) |

| Advancements in adhesive and sealant technologies | +0.8% | Global | Medium to Long-term (2025-2033) |

Automotive Coating Adhesive and Sealant Market Restraints Analysis

Despite robust growth drivers, the automotive coating, adhesive, and sealant market faces several significant restraints that could temper its expansion. One primary challenge is the volatility of raw material prices, particularly for petrochemical-derived polymers and specialty chemicals. Fluctuations in crude oil prices and supply chain disruptions can directly impact the cost of production, leading to increased pricing pressure on manufacturers and potentially affecting profit margins across the value chain. This unpredictability makes long-term planning and stable pricing strategies difficult for industry participants.

Another substantial restraint is the increasing scrutiny and regulation surrounding environmental impact, particularly concerning Volatile Organic Compounds (VOCs) emitted by certain adhesives and sealants. Stricter environmental policies in regions like Europe and North America necessitate significant investments in research and development to formulate low-VOC or VOC-free alternatives, which can be costly and time-consuming. Additionally, the relatively long product development cycles for new, high-performance materials, coupled with the rigorous testing and validation required by the automotive industry, can slow down market penetration for innovative solutions. Competition from traditional mechanical fastening methods in certain applications also presents a continued restraint, requiring adhesives and sealants to consistently demonstrate superior performance benefits.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in raw material prices | -0.7% | Global | Short to Medium-term (2025-2030) |

| Stringent environmental regulations on VOC emissions | -0.6% | Europe, North America, Japan | Medium to Long-term (2025-2033) |

| Long product development and validation cycles | -0.4% | Global | Long-term (2027-2033) |

| Competition from alternative joining technologies | -0.3% | Global | Medium-term (2026-2031) |

| Technical challenges in bonding dissimilar materials | -0.2% | Global | Short to Medium-term (2025-2030) |

Automotive Coating Adhesive and Sealant Market Opportunities Analysis

The automotive coating, adhesive, and sealant market is replete with substantial opportunities for growth and innovation, driven by evolving industry needs and technological advancements. One key area of opportunity lies in the continuous development and commercialization of sustainable and bio-based adhesive and sealant solutions. As environmental concerns intensify and regulatory frameworks become stricter, manufacturers who can offer high-performance, eco-friendly alternatives will gain a significant competitive advantage and address a growing market demand from environmentally conscious consumers and original equipment manufacturers (OEMs).

The rapid expansion of the electric vehicle (EV) market presents a multifaceted opportunity. EVs require specialized adhesives for battery module bonding, structural integration, thermal management, and electrical insulation, all demanding unique performance characteristics not typically found in conventional automotive applications. Furthermore, the trend towards autonomous vehicles and advanced driver-assistance systems (ADAS) creates opportunities for novel sealing solutions for sensitive electronic components and sensors, ensuring their protection from environmental factors. Customization and application-specific formulations, particularly for lightweight materials like composites and advanced alloys, also represent a lucrative niche, allowing manufacturers to offer tailored solutions that meet precise performance specifications for critical vehicle components.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of sustainable and bio-based solutions | +1.1% | Europe, North America, Asia Pacific | Medium to Long-term (2026-2033) |

| Expansion in Electric Vehicle (EV) battery and component bonding | +1.6% | Global | Short to Long-term (2025-2033) |

| Increased demand for structural adhesives in lightweighting applications | +1.0% | Global | Medium to Long-term (2025-2033) |

| New applications in autonomous vehicles and ADAS sensor protection | +0.8% | North America, Europe, Asia Pacific (Japan, Korea) | Long-term (2028-2033) |

| Growth in aftermarket and repair applications | +0.5% | Emerging economies, Global | Short to Medium-term (2025-2029) |

Automotive Coating Adhesive and Sealant Market Challenges Impact Analysis

The automotive coating, adhesive, and sealant market encounters several inherent challenges that demand strategic responses from industry players. One significant challenge is meeting the increasingly stringent performance requirements for materials used in modern vehicles. Adhesives and sealants must withstand extreme temperatures, vibrations, chemical exposure, and diverse environmental conditions over the vehicle's lifespan, all while contributing to lightweighting and structural integrity. This necessitates continuous investment in advanced material science and rigorous testing protocols, which can be both time-consuming and capital-intensive.

Another major challenge is navigating the complexities of a global supply chain, which is susceptible to geopolitical events, trade disputes, and natural disasters. Ensuring a consistent supply of specialized raw materials, managing logistics across multiple regions, and mitigating the risks associated with single-source suppliers require robust supply chain management strategies. Furthermore, the rapid pace of technological evolution in the automotive sector, particularly with the advent of new materials (e.g., carbon fiber composites, advanced high-strength steels) and manufacturing processes, mandates that adhesive and sealant manufacturers continuously innovate to provide compatible and effective solutions. The need for a skilled workforce capable of developing, manufacturing, and applying these highly specialized materials also poses a challenge in some regions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Meeting stringent performance and durability requirements | -0.8% | Global | Long-term (2025-2033) |

| Managing complex global supply chain disruptions | -0.7% | Global | Short to Medium-term (2025-2029) |

| Rapid technological evolution in automotive materials and processes | -0.6% | Global | Medium to Long-term (2026-2033) |

| High R&D costs for innovative and compliant formulations | -0.5% | Global | Long-term (2025-2033) |

| Lack of skilled workforce for specialized applications | -0.3% | Europe, North America | Short to Medium-term (2025-2030) |

Automotive Coating Adhesive and Sealant Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global automotive coating, adhesive, and sealant market, offering valuable insights into its current status, growth drivers, restraints, opportunities, and future outlook. The report covers detailed market sizing, segmentation analysis by type, application, vehicle type, and raw material, alongside regional breakdowns to provide a holistic view of the market dynamics. It also includes an extensive competitive landscape analysis, profiling key industry players and their strategic initiatives, enabling stakeholders to make informed business decisions. The scope encompasses a thorough examination of emerging trends, technological advancements, and the impact of regulatory frameworks on market evolution.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 7.2 Billion |

| Market Forecast in 2033 | USD 11.3 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Chemical Solutions Inc., Advanced Polymer Technologies, Industrial Sealants Corp., Specialty Adhesives & Coatings Ltd., Innovative Materials Group, Polymer Science & Technology LLC, Integrated Adhesives Systems, High-Performance Coatings Co., Sustainable Bondings Inc., Automotive Sealant Innovations, Dynamic Adhesives Global, ChemBond Solutions, FlexiCoat Systems, Precision Sealants International, EcoBond Technologies. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The automotive coating, adhesive, and sealant market is extensively segmented to provide a detailed understanding of its diverse components and their respective growth trajectories. This segmentation allows for precise analysis of market dynamics, identifying key areas of demand and technological innovation across various product types, applications, vehicle categories, and raw material compositions. Understanding these segments is crucial for stakeholders to tailor their product offerings, marketing strategies, and investment decisions to specific market needs and opportunities.

Product type segmentation differentiates between various adhesive chemistries, such as epoxy, polyurethane, and acrylic, each possessing unique properties suited for specific bonding requirements, and sealants like silicone and butyl, which offer distinct sealing capabilities. Application-based segmentation highlights critical areas within vehicle manufacturing, including body-in-white, paint shop, and assembly, where these materials perform essential functions. Further, the market is segmented by vehicle type to reflect the varying demands from passenger cars, commercial vehicles, and the rapidly expanding electric vehicle sector, each having unique material specifications. Lastly, raw material segmentation distinguishes between synthetic and emerging bio-based formulations, underscoring the industry's shift towards sustainability.

- By Product Type: Adhesives (Epoxy, Polyurethane, Acrylic, Silicone, Cyanoacrylate, SMP, Others), Sealants (Polyurethane, Silicone, Polysulfide, Butyl, Acrylic, Others)

- By Application: Body-in-White (BIW), Paint Shop, Assembly (Interior, Exterior, Engine & Drivetrain), Underbody Coatings, Engine Components, Drivetrain, Chassis, Glazing, Body Panel Bonding, Interior Trim, Electrical & Electronics, HVAC

- By Vehicle Type: Passenger Vehicles, Commercial Vehicles (Light Commercial Vehicles, Heavy Commercial Vehicles), Electric Vehicles (Battery Electric Vehicles, Hybrid Electric Vehicles, Plug-in Hybrid Electric Vehicles)

- By Raw Material: Synthetic (Epoxy, Polyurethane, Acrylic, Silicone, Others), Bio-based

Regional Highlights

- North America: This region is characterized by robust automotive R&D, a strong focus on advanced materials for lightweighting, and increasing adoption of electric vehicles. Stringent safety and environmental regulations drive the demand for high-performance, low-VOC products. The presence of major automotive OEMs and a well-developed aftermarket contributes significantly to market growth.

- Europe: A pioneer in environmental sustainability, Europe leads in the development and adoption of eco-friendly and bio-based adhesive and sealant solutions. Strict emissions standards and a strong push for electric vehicle manufacturing, particularly in Germany, France, and the UK, are key market drivers. Innovation in structural adhesives for advanced vehicle architectures is also prominent.

- Asia Pacific (APAC): The largest and fastest-growing market, APAC is driven by high-volume automotive production, especially in China, India, Japan, and South Korea. Rapid urbanization, increasing disposable incomes, and the expansion of manufacturing facilities fuel demand. The region is also a hub for EV production and offers significant opportunities for both traditional and advanced applications.

- Latin America: This region presents moderate growth opportunities, primarily influenced by fluctuating economic conditions and automotive production volumes in countries like Brazil and Mexico. The market here is focused on cost-effective solutions and meeting local demand for passenger and commercial vehicles, with increasing interest in electrification.

- Middle East and Africa (MEA): Growth in MEA is primarily driven by expanding infrastructure projects, increasing vehicle sales, and developing automotive manufacturing capabilities in certain countries. The market for coatings, adhesives, and sealants is linked to new vehicle sales and the maintenance of existing fleets, with a gradual shift towards more advanced materials.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Coating Adhesive and Sealant Market.- Global Chemical Solutions Inc.

- Advanced Polymer Technologies

- Industrial Sealants Corp.

- Specialty Adhesives & Coatings Ltd.

- Innovative Materials Group

- Polymer Science & Technology LLC

- Integrated Adhesives Systems

- High-Performance Coatings Co.

- Sustainable Bondings Inc.

- Automotive Sealant Innovations

- Dynamic Adhesives Global

- ChemBond Solutions

- FlexiCoat Systems

- Precision Sealants International

- EcoBond Technologies

- Universal Adhesives & Sealants

- Synergy Chemical Industries

- Material Science Innovators

- Future Coatings & Bonds

- Apex Sealing Solutions

Frequently Asked Questions

Analyze common user questions about the Automotive Coating Adhesive and Sealant market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are automotive coating adhesives and sealants used for?

Automotive coating adhesives and sealants are essential for various applications including structural bonding of vehicle components, sealing joints against water, dust, and noise, reducing vibration, enhancing corrosion protection, and improving vehicle aesthetics and aerodynamics. They are crucial for body-in-white, paint shop processes, and final assembly.

What are the primary types of adhesives and sealants used in the automotive industry?

The primary types include epoxy, polyurethane, acrylic, and silicone adhesives, each offering different performance characteristics like strength, flexibility, and temperature resistance. Common sealants comprise polyurethane, silicone, and butyl, known for their sealing and protective properties.

How is the electric vehicle (EV) trend impacting this market?

The EV trend is significantly impacting the market by driving demand for specialized adhesives and sealants for battery pack assembly, thermal management, structural bonding of lightweight materials, and protection of sensitive electronic components, requiring enhanced performance characteristics.

What are the key drivers for the growth of the automotive coating adhesive and sealant market?

Key drivers include increasing global automotive production, the growing demand for lightweight and fuel-efficient vehicles, the rapid expansion of the electric vehicle market, and stringent environmental and safety regulations promoting advanced material use.

What are the main challenges faced by manufacturers in this market?

Manufacturers face challenges such as volatile raw material prices, stringent environmental regulations on VOC emissions, long product development and validation cycles for new formulations, and the need to meet increasingly high performance and durability requirements in modern vehicle designs.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted