Aluminum Alloy Wheel Market

Aluminum Alloy Wheel Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700129 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

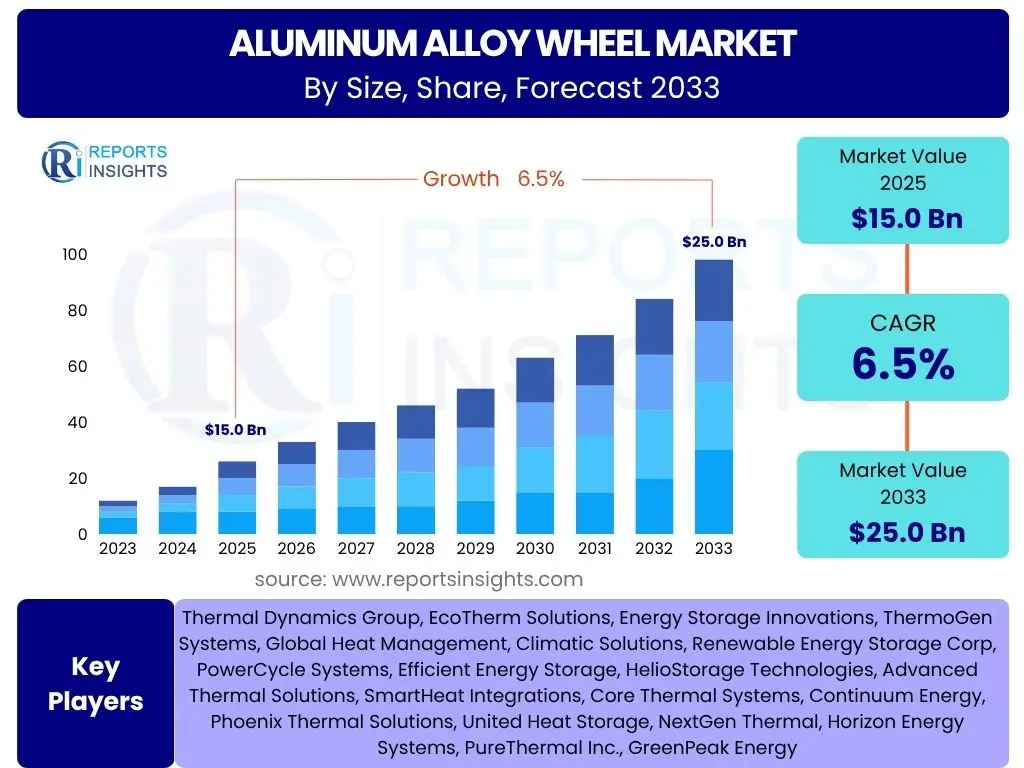

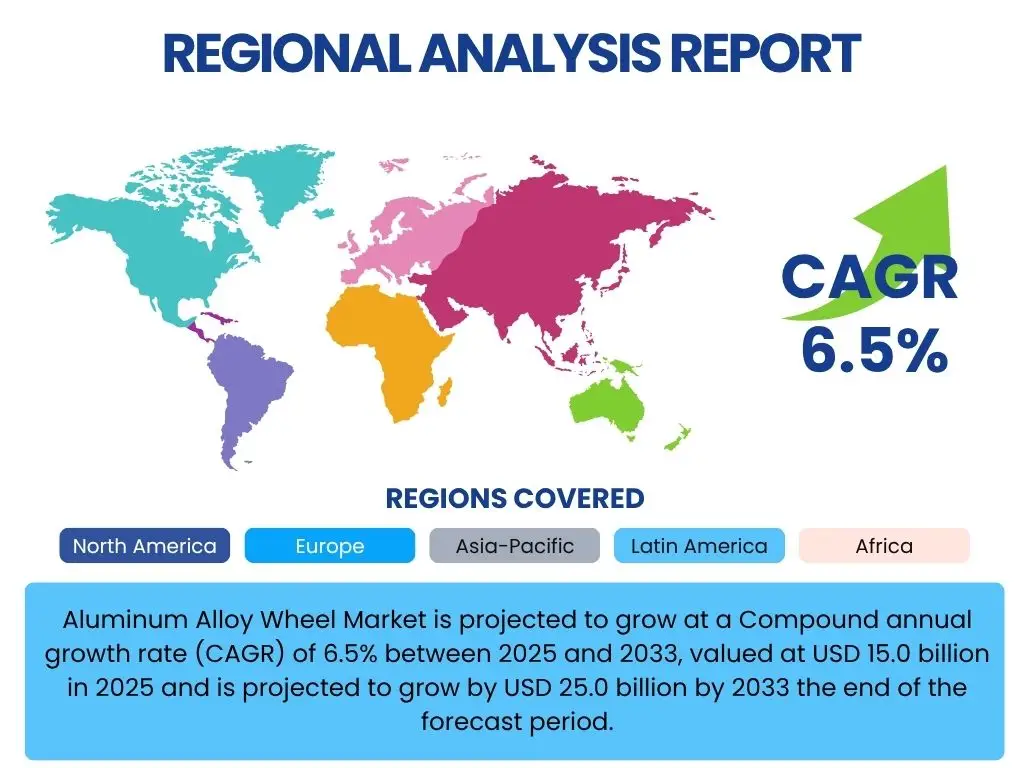

Aluminum Alloy Wheel Market is projected to grow at a Compound annual growth rate (CAGR) of 6.5% between 2025 and 2033, current valued at USD 15.0 billion in 2025 and is projected to grow by USD 25.0 billion by 2033 the end of the forecast period.

Key Aluminum Alloy Wheel Market Trends & Insights

The global aluminum alloy wheel market is witnessing a transformative phase driven by evolving automotive industry demands, a growing emphasis on vehicle performance, and consumer aesthetic preferences. Key trends include the widespread adoption of lightweight materials to enhance fuel efficiency and reduce emissions, a surging demand from the electric vehicle segment, and advancements in manufacturing processes such as flow forming and advanced casting techniques. Furthermore, increasing customization options and the premiumization of vehicle components are significantly influencing market dynamics, leading to higher average selling prices and expanded product portfolios. The aftermarket segment also continues to play a crucial role, driven by consumer desire for vehicle personalization and performance upgrades.

- Increased adoption of lightweight aluminum alloys for improved fuel efficiency and reduced emissions.

- Surge in demand from the rapidly expanding electric vehicle (EV) market.

- Advancements in manufacturing technologies like flow forming and advanced casting.

- Growing consumer preference for aesthetically appealing and customizable wheel designs.

- Premiumization trend in automotive components driving demand for high-end alloy wheels.

- Expansion of the aftermarket segment fueled by vehicle personalization and upgrades.

- Focus on sustainable manufacturing practices and recyclable materials.

- Integration of smart wheel technologies for enhanced driving experience and safety.

AI Impact Analysis on Aluminum Alloy Wheel

Artificial Intelligence (AI) is poised to revolutionize the aluminum alloy wheel market across its entire value chain, from design and manufacturing to supply chain management and aftermarket services. AI-driven generative design tools can rapidly create optimized wheel structures that are lighter yet stronger, reducing material usage and improving performance. In manufacturing, AI enables predictive maintenance for machinery, enhances quality control through automated inspection, and optimizes production processes for greater efficiency and reduced waste. Furthermore, AI algorithms can refine supply chain logistics, predict market demand fluctuations, and personalize marketing efforts, ultimately leading to more agile operations and a more responsive market. This technological integration promises significant cost reductions, improved product quality, and accelerated innovation within the industry.

- AI-driven generative design for optimized wheel geometry, strength, and weight.

- Enhanced manufacturing efficiency through AI-powered predictive maintenance and process automation.

- Improved quality control and defect detection using AI-vision systems during production.

- Optimized supply chain management and logistics with AI-driven forecasting and route planning.

- Personalized design recommendations and customer experiences leveraging AI analytics.

- Reduced material waste and energy consumption through AI-optimized manufacturing parameters.

Key Takeaways Aluminum Alloy Wheel Market Size & Forecast

- The global aluminum alloy wheel market is projected for substantial growth between 2025 and 2033.

- Market value is estimated at USD 15.0 billion in 2025, reaching USD 25.0 billion by 2033.

- A robust Compound Annual Growth Rate (CAGR) of 6.5% is anticipated over the forecast period.

- Growth is primarily driven by increasing automotive production, especially electric vehicles, and rising consumer demand for lightweight and aesthetically appealing components.

- Asia Pacific is expected to maintain its dominance due to high vehicle manufacturing volumes and expanding economic landscapes.

- Technological advancements in alloy compositions and manufacturing processes are key enablers of market expansion.

Aluminum Alloy Wheel Market Drivers Analysis

The aluminum alloy wheel market is propelled by a confluence of macroeconomic factors, technological advancements, and evolving consumer preferences. A significant driver is the relentless pursuit of fuel efficiency and reduced emissions in the automotive industry, where lightweight aluminum wheels play a critical role in decreasing vehicle mass. The global expansion of automotive production, particularly in emerging economies and the surging demand for electric vehicles, further amplifies market growth. Consumers' increasing emphasis on vehicle aesthetics, performance enhancement, and personalization also fuels the demand for premium and custom alloy wheels, pushing manufacturers to innovate designs and expand their product offerings. These factors collectively create a robust growth environment for the aluminum alloy wheel sector, necessitating continuous innovation in materials and manufacturing to meet evolving industry standards and consumer expectations.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Automotive Production and Sales | +2.0% | Asia Pacific, North America, Europe | Short- to Mid-term |

| Growing Preference for Lightweight and Fuel-Efficient Vehicles | +1.5% | Global, particularly Europe, North America, China | Mid- to Long-term |

| Rising Demand for Aesthetic Appeal and Vehicle Customization | +1.0% | North America, Europe, Developed Asia Pacific | Short- to Mid-term |

| Rapid Growth of the Electric Vehicle (EV) Market | +1.2% | China, Europe, North America | Mid- to Long-term |

| Technological Advancements in Alloy Manufacturing | +0.8% | Global, with focus on innovation hubs | Long-term |

| Expansion of the Aftermarket Segment | +0.5% | North America, Europe, Asia Pacific | Short- to Mid-term |

Aluminum Alloy Wheel Market Restraints Analysis

Despite robust growth prospects, the aluminum alloy wheel market faces several significant restraints that could impede its expansion. One primary challenge is the higher manufacturing cost of aluminum alloy wheels compared to conventional steel wheels, which can deter cost-sensitive consumers and vehicle manufacturers, particularly in budget segments. Volatility in the prices of raw materials, primarily aluminum and associated alloying elements, can directly impact production costs and profit margins. Furthermore, the market is subject to increasingly stringent regulatory standards concerning vehicle safety, durability, and performance, necessitating significant investments in research and development to comply, thereby adding to the overall cost structure. These factors, alongside potential economic downturns affecting overall automotive sales, pose substantial challenges for sustained market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Cost Compared to Steel Wheels | -1.5% | Emerging Markets, Budget Vehicle Segments Globally | Mid-term |

| Volatility in Raw Material Prices (Aluminum) | -1.0% | Global | Short- to Mid-term |

| Stringent Regulatory Standards for Safety and Performance | -0.8% | Europe, North America, Japan | Long-term |

| Economic Slowdowns Affecting Automotive Sales | -1.2% | Global | Short-term |

Aluminum Alloy Wheel Market Opportunities Analysis

The aluminum alloy wheel market presents significant opportunities for growth driven by evolving automotive trends and technological advancements. One key area of expansion lies in the increasing adoption of aluminum wheels in commercial vehicles, including heavy-duty trucks and buses, where the benefits of weight reduction translate into substantial fuel savings and increased payload capacity. Emerging economies, particularly in Southeast Asia, Africa, and parts of Latin America, represent largely untapped markets with rapidly growing automotive industries and rising disposable incomes. Furthermore, continuous innovation in metallurgy and manufacturing processes, such as the development of advanced high-strength aluminum alloys, promises further weight reduction and performance improvements, opening new avenues for product differentiation. The integration of smart technologies, such as sensors for tire pressure monitoring and wheel health, also presents a novel opportunity to add value and enhance the overall driving experience.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Adoption in Commercial Vehicles and Heavy-Duty Trucks | +1.0% | North America, Europe, China | Mid- to Long-term |

| Untapped Potential in Emerging Economies | +1.5% | Southeast Asia, Africa, Latin America, Eastern Europe | Mid- to Long-term |

| Development of Advanced Alloys for Further Weight Reduction | +0.7% | Global, R&D focused regions | Long-term |

| Integration with Smart Technologies and Sensor-Equipped Wheels | +0.5% | Developed Markets | Long-term |

| Increasing Demand for Customization and Premium Wheels in Aftermarket | +0.8% | North America, Europe, Japan | Short- to Mid-term |

Aluminum Alloy Wheel Market Challenges Impact Analysis

The aluminum alloy wheel market faces several critical challenges that demand strategic responses from manufacturers. Environmental concerns surrounding the energy-intensive production of primary aluminum and the need for efficient recycling processes pose a significant sustainability challenge, impacting brand image and potentially leading to higher regulatory costs. Global supply chain disruptions, stemming from geopolitical tensions, natural disasters, or pandemics, can severely affect raw material availability and logistics, leading to production delays and increased costs. Furthermore, intense competition among existing players and the entry of new manufacturers, particularly from Asian markets, can lead to aggressive pricing strategies, eroding profit margins across the industry. Maintaining high standards of durability and repairability, especially with increasingly complex designs and larger wheel sizes, also presents an engineering and service challenge that impacts consumer satisfaction and long-term market viability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Environmental Concerns Related to Aluminum Production and Recycling | -0.8% | Global, particularly Europe and North America | Long-term |

| Supply Chain Disruptions and Volatility | -1.0% | Global | Short- to Mid-term |

| Intense Competition Leading to Price Pressure | -1.2% | Global, especially Asian markets | Mid-term |

| Maintaining Durability and Repairability with Complex Designs | -0.5% | Global | Mid- to Long-term |

Aluminum Alloy Wheel Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global aluminum alloy wheel market, offering critical insights into its current status, historical performance, and future growth trajectories. The scope encompasses detailed market sizing, meticulous forecasting, and a thorough examination of key trends, drivers, restraints, opportunities, and challenges shaping the industry. Furthermore, the report delves into a granular segmentation analysis across various parameters, offering regional breakdowns and profiles of key market participants, empowering stakeholders with actionable intelligence for strategic decision-making and competitive positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.0 billion |

| Market Forecast in 2033 | USD 25.0 billion |

| Growth Rate | 6.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Maxion Wheels, Enkei Corporation, Borbet GmbH, Ronal Group, Superior Industries International, CITIC Dicastal Co. Ltd., Lizhong Wheel Group, Topy Industries Limited, BBS GmbH, OZ S.p.A., American Racing, Konig Wheels, Advanti Racing, Wheel Pros, Weds Co. Ltd., Rays Co. Ltd., Fuchsfelge, Alcoa Wheels, Uniwheels, Mandrus Wheels |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

:The global aluminum alloy wheel market is comprehensively segmented to provide a granular view of its diverse dynamics and opportunities. This segmentation considers critical differentiating factors such as vehicle type, wheel size, the manufacturing process employed, and the primary sales channel. Understanding these segments is crucial for identifying specific market niches, tailoring product strategies, and forecasting demand patterns accurately across the industry landscape. Each segment represents distinct consumer needs, technological requirements, and competitive environments, driving varied growth trajectories and investment opportunities.

- By Vehicle Type: This segment analyzes the market based on the types of vehicles utilizing aluminum alloy wheels.

- Passenger Cars: Covers a broad range from compact cars to luxury sedans and SUVs.

- Commercial Vehicles: Includes light commercial vehicles, heavy-duty trucks, and buses.

- Two-Wheelers: Focuses on motorcycles and scooters adopting alloy wheels.

- By Wheel Size: This segmentation categorizes the market based on the diameter of the wheels, impacting performance, aesthetics, and vehicle compatibility.

- Up to 18-inch: Typically found in smaller vehicles or base models.

- 19-21-inch: Common in mid-range to premium sedans and SUVs.

- Above 21-inch: Predominantly for high-performance, luxury, and large SUV segments.

- By Manufacturing Process: This segment examines the market based on the production techniques used for alloy wheels, each offering distinct advantages in terms of cost, strength, and design flexibility.

- Casting: Includes gravity casting, low-pressure casting, and counter-pressure casting, known for cost-effectiveness and design versatility.

- Forging: Produces highly dense and strong wheels, ideal for performance and luxury vehicles.

- Flow Forming: A hybrid process combining casting and forging, offering improved strength-to-weight ratio.

- By Sales Channel: This segmentation differentiates between the primary sales avenues for aluminum alloy wheels, reflecting varied distribution strategies and customer bases.

- OEM (Original Equipment Manufacturer): Wheels supplied directly to vehicle manufacturers for new vehicle assembly.

- Passenger Cars OEM

- Commercial Vehicles OEM

- Aftermarket: Wheels sold separately for replacement, customization, or performance upgrades.

- Passenger Cars Aftermarket

- Commercial Vehicles Aftermarket

- OEM (Original Equipment Manufacturer): Wheels supplied directly to vehicle manufacturers for new vehicle assembly.

Regional Highlights

The global aluminum alloy wheel market exhibits significant regional disparities in terms of production, consumption, and growth drivers, reflecting varied automotive landscapes, economic conditions, and consumer preferences. Asia Pacific stands out as the largest and fastest-growing market, primarily fueled by robust automotive production volumes, particularly in China, India, and Japan, coupled with rising disposable incomes and increasing vehicle ownership. North America and Europe represent mature markets characterized by a strong demand for premium, high-performance, and custom alloy wheels, driven by a preference for larger vehicles and a thriving aftermarket segment. Latin America and the Middle East & Africa are emerging markets, showing gradual growth driven by urbanization, expanding infrastructure, and increasing foreign investments in the automotive sector.

- North America: Characterized by a strong demand for larger diameter wheels for SUVs and pickup trucks, a robust aftermarket segment driven by customization, and an increasing adoption of alloy wheels in luxury and performance vehicles. The region also benefits from advancements in manufacturing technologies and a focus on fuel efficiency.

- Europe: Leads in the adoption of lightweight alloy wheels driven by stringent emission regulations and a strong preference for premium and aesthetically refined vehicle components. The region is a hub for high-performance and luxury car manufacturers, further boosting demand for sophisticated alloy wheel designs and advanced manufacturing processes.

- Asia Pacific (APAC): Dominates the global market in terms of production and consumption, primarily due to the massive automotive manufacturing base in China, India, Japan, and South Korea. Rapid economic growth, rising disposable incomes, and increasing vehicle sales in developing countries within this region are key factors contributing to its leading position and highest growth rate. The region is also at the forefront of electric vehicle production, which significantly drives alloy wheel demand.

- Latin America: Exhibits steady growth, propelled by expanding automotive production capacities, increasing urbanization, and a growing middle class. While demand may be more sensitive to economic fluctuations, the preference for vehicle upgrades and new car sales contribute positively to the market.

- Middle East and Africa (MEA): Represents an emerging market with gradual growth. Factors such as increasing infrastructure development, a growing automotive aftermarket, and rising vehicle ownership in key countries contribute to the demand for aluminum alloy wheels, albeit at a slower pace compared to other regions.

Top Key Players:

The market research report covers the analysis of key stake holders of the Aluminum Alloy Wheel Market. Some of the leading players profiled in the report include -:- Maxion Wheels

- Enkei Corporation

- Borbet GmbH

- Ronal Group

- Superior Industries International

- CITIC Dicastal Co. Ltd.

- Lizhong Wheel Group

- Topy Industries Limited

- BBS GmbH

- OZ S.p.A.

- American Racing

- Konig Wheels

- Advanti Racing

- Wheel Pros

- Weds Co. Ltd.

- Rays Co. Ltd.

- Fuchsfelge

- Alcoa Wheels

- Uniwheels

- Mandrus Wheels

Frequently Asked Questions:

What is the current market size of the Aluminum Alloy Wheel Market?

The global Aluminum Alloy Wheel Market was valued at approximately USD 15.0 billion in 2025. This valuation reflects the widespread adoption of alloy wheels across various vehicle types due to their aesthetic appeal, performance benefits, and lightweight properties contributing to fuel efficiency. The market size is projected to expand significantly over the forecast period.What are the primary drivers for the growth of aluminum alloy wheels?

Key drivers include the automotive industry's increasing focus on lightweight components to enhance fuel efficiency and reduce emissions, a surging demand for electric vehicles (EVs) which benefit from lighter wheels for extended range, and growing consumer preferences for vehicle customization and aesthetic upgrades. Additionally, advancements in manufacturing technologies contribute to the market's expansion.How is the electric vehicle (EV) trend impacting the aluminum alloy wheel market?

The electric vehicle (EV) trend is significantly boosting the aluminum alloy wheel market. EVs heavily rely on lightweight components to maximize battery range and optimize performance. Aluminum alloy wheels, being lighter than traditional steel wheels, directly contribute to reducing the overall vehicle weight, thereby extending driving range and improving energy efficiency for electric vehicles. This makes them a preferred choice for EV manufacturers globally.Which region holds the largest share in the Aluminum Alloy Wheel Market?

Asia Pacific holds the largest market share in the Aluminum Alloy Wheel Market. This dominance is primarily attributed to the region's robust automotive production base, particularly in countries like China, India, and Japan, coupled with rapid economic growth and increasing vehicle sales volumes. The expanding middle class and rising disposable incomes further fuel the demand for aluminum alloy wheels in this region.What manufacturing processes are commonly used for aluminum alloy wheels?

Common manufacturing processes for aluminum alloy wheels include casting, forging, and flow forming. Casting methods like gravity casting and low-pressure casting are popular for their cost-effectiveness and design flexibility. Forging produces denser and stronger wheels, ideal for high-performance applications. Flow forming is a hybrid process combining casting with a rotary forging technique, offering an excellent balance of strength, weight reduction, and cost efficiency.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted