Automotive Cloud Service Market

Automotive Cloud Service Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709860 | Last Updated : December 22, 2025 |

Format : ![]()

![]()

![]()

![]()

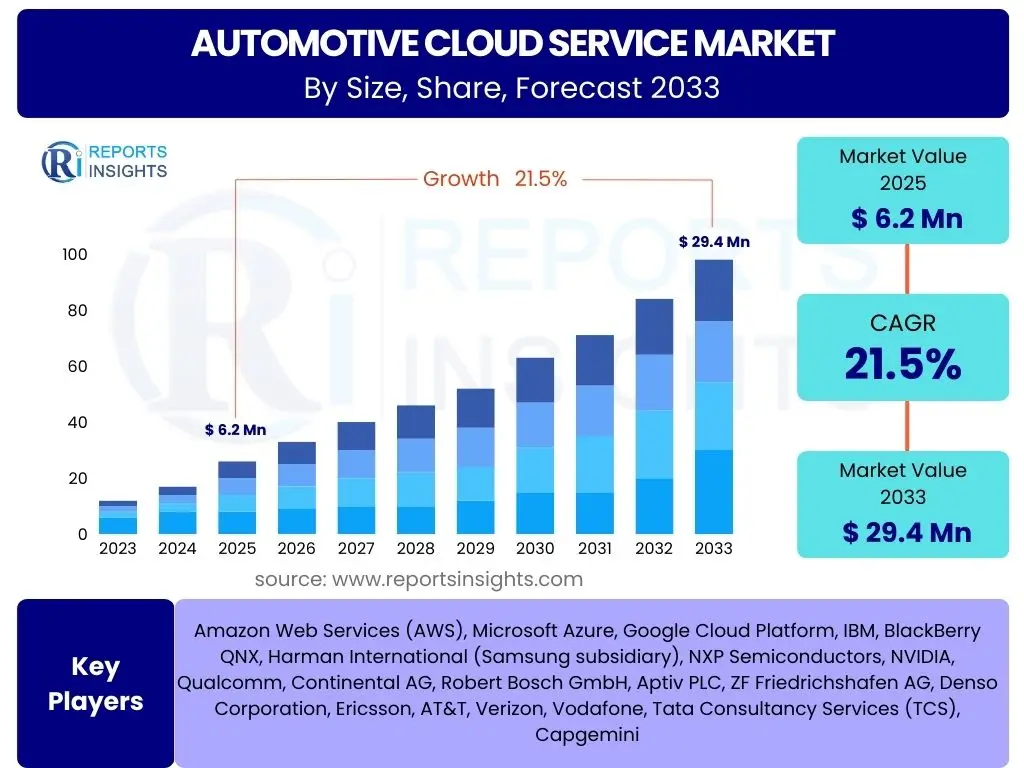

Automotive Cloud Service Market Size

According to Reports Insights Consulting Pvt Ltd, The Automotive Cloud Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.5% between 2025 and 2033. The market is estimated at USD 6.2 billion in 2025 and is projected to reach USD 29.4 billion by the end of the forecast period in 2033. This substantial growth is driven by the increasing integration of digital technologies within vehicles, the rise of connected car ecosystems, and the escalating demand for advanced in-car services and real-time data processing capabilities. The automotive industry's shift towards software-defined vehicles and autonomous driving further amplifies the need for robust, scalable, and secure cloud infrastructure, positioning cloud services as a foundational component for future mobility solutions.

The market expansion is also significantly influenced by advancements in 5G technology, which provides the low latency and high bandwidth essential for seamless cloud-based automotive applications. Furthermore, the growing adoption of electric vehicles (EVs) and the emphasis on sustainable mobility solutions necessitate sophisticated cloud platforms for battery management, charging infrastructure optimization, and over-the-air (OTA) updates. These factors collectively contribute to the robust financial projections, underscoring the critical role of cloud services in revolutionizing the automotive sector's operational efficiency, consumer experience, and innovation landscape.

Key Automotive Cloud Service Market Trends & Insights

Common user inquiries about the Automotive Cloud Service market frequently revolve around the transformative shifts impacting vehicle technology and operational paradigms. Users are keenly interested in how connectivity is evolving, the implications of software-defined vehicles, and the increasing reliance on remote service delivery. There is a strong emphasis on understanding the technologies that enable more intelligent, safer, and more personalized driving experiences, as well as the underlying infrastructure required to support these innovations. Furthermore, questions often arise regarding the security measures employed to protect sensitive vehicle and user data in cloud environments, reflecting a general concern for privacy and system integrity in an increasingly connected world.

Another significant area of user interest pertains to the practical applications of automotive cloud services, such as real-time navigation, predictive maintenance, and advanced infotainment. The potential for new business models, including subscription-based features and data monetization strategies, is also a frequent topic. Users seek clarity on how cloud services contribute to fleet management efficiency, the development of autonomous capabilities, and the overall future direction of automotive innovation. These inquiries highlight a collective desire to grasp both the technological advancements and the economic implications of cloud integration within the automotive sector.

- Connected Car Ecosystem Expansion: Proliferation of vehicles equipped with internet connectivity for enhanced navigation, infotainment, and emergency services.

- Software-Defined Vehicles (SDVs): Transition towards vehicles where functionalities are primarily controlled and updated through software, heavily reliant on cloud infrastructure.

- Over-the-Air (OTA) Updates: Increasing adoption of cloud-enabled updates for vehicle software, improving performance, adding new features, and enhancing security without physical dealer visits.

- Enhanced Cybersecurity Solutions: Growing focus on robust cloud-based security measures to protect vehicles from cyber threats and ensure data privacy.

- Data Monetization and Analytics: Leveraging vast amounts of vehicle data collected in the cloud for predictive maintenance, personalized services, and new revenue streams.

- Electrification and Charging Infrastructure Management: Cloud services optimizing EV battery management, route planning for charging, and smart grid integration.

- Advanced Telematics and Infotainment: Evolution of in-car systems offering richer content, real-time traffic, and personalized experiences powered by cloud computing.

- Vehicle-to-Everything (V2X) Communication Development: Cloud supporting the infrastructure for vehicles to communicate with other vehicles, infrastructure, and pedestrians, enhancing safety and traffic flow.

AI Impact Analysis on Automotive Cloud Service

User questions regarding the impact of Artificial Intelligence (AI) on the Automotive Cloud Service market frequently explore how AI enhances vehicle intelligence, optimizes operational efficiencies, and creates new value propositions. There is considerable interest in AI's role in processing the massive volumes of data generated by connected cars, enabling capabilities such as predictive maintenance, personalized user experiences, and advanced driver-assistance systems. Concerns often surface about the computational demands of AI algorithms and how cloud infrastructure can provide the necessary scalability and processing power to support these intelligent applications, especially for real-time decision-making in autonomous driving scenarios. Users also inquire about the ethical implications and regulatory challenges associated with AI's increasing autonomy in vehicles.

Furthermore, common inquiries highlight expectations for AI to revolutionize the entire automotive value chain, from manufacturing and supply chain optimization to customer service and post-sale vehicle management. Users are curious about how AI, when integrated with cloud services, can facilitate the development of more sophisticated autonomous features, improve traffic management in smart cities, and enable more accurate diagnostics. The potential for AI to drive innovation in areas like natural language processing for in-car assistants and advanced computer vision for perception systems is also a key area of interest, reflecting a broader anticipation of more intuitive and intelligent vehicles that are deeply interconnected through cloud-based AI solutions.

- Enhanced Data Processing and Analytics: AI algorithms leveraging cloud platforms to analyze vast quantities of vehicle data, identifying patterns for improved performance, safety, and user experience.

- Predictive Maintenance: AI in the cloud analyzing sensor data to predict component failures, enabling proactive servicing and reducing vehicle downtime.

- Autonomous Driving Capabilities: Cloud-based AI supporting the training, validation, and real-time decision-making processes for autonomous vehicles, processing data from sensors, cameras, and lidar.

- Personalized User Experience: AI utilizing cloud data to offer tailored infotainment, climate control, and driving preferences based on individual user behavior and preferences.

- Optimized Fleet Management: AI algorithms in the cloud improving route optimization, fuel efficiency, and asset utilization for commercial fleets.

- Natural Language Processing (NLP) for In-Car Assistants: AI-powered virtual assistants relying on cloud services for complex queries, voice commands, and seamless integration with external services.

- Edge AI Integration: Combining cloud AI with edge computing within vehicles to enable faster, localized decision-making while offloading heavy processing to the cloud.

- Cybersecurity Enhancement: AI systems in the cloud detecting and responding to cyber threats in real-time by analyzing network traffic and behavioral anomalies across connected vehicles.

Key Takeaways Automotive Cloud Service Market Size & Forecast

Common user questions regarding key takeaways from the Automotive Cloud Service market size and forecast often focus on understanding the primary growth drivers, the longevity of the market expansion, and the most impactful technological shifts. Users want to know what segments are experiencing the most rapid growth, which regions are leading adoption, and the overall strategic implications for automotive manufacturers and technology providers. There is a strong desire for actionable insights that highlight where investment and innovation are concentrated, indicating the future direction of the industry and potential for competitive advantage. The scalability and flexibility offered by cloud solutions are consistently recognized as fundamental enablers for the automotive sector's digital transformation.

Moreover, inquiries frequently touch upon the critical factors sustaining the projected growth, such as the increasing sophistication of connected features, the imperative for robust cybersecurity, and the move towards subscription-based service models. Users are interested in how the market’s trajectory is shaped by evolving consumer expectations for seamless digital integration and the industry's push towards software-defined vehicles and autonomous capabilities. The long-term forecast demonstrates that cloud services are not merely a supplemental technology but a core infrastructure powering the next generation of mobility, making their understanding essential for stakeholders across the automotive ecosystem.

- Robust Growth Trajectory: The Automotive Cloud Service market is projected for significant expansion with a CAGR of 21.5% from 2025 to 2033, underscoring its pivotal role in future mobility.

- Digital Transformation Catalyst: Cloud services are foundational for the automotive industry's digital shift, enabling connected cars, autonomous driving, and software-defined vehicles.

- Connected Car Ecosystem is Key: The proliferation of connected vehicles demanding real-time data, advanced navigation, and infotainment drives substantial market growth.

- Value Beyond Connectivity: Cloud enables critical applications such as predictive maintenance, remote diagnostics, and over-the-air (OTA) updates, enhancing vehicle lifecycle management.

- Strategic Investment Area: Both automotive OEMs and technology providers are heavily investing in cloud infrastructure and services to stay competitive and innovate.

- Data is the New Fuel: The ability to collect, process, and analyze vast amounts of vehicle data in the cloud is creating new opportunities for personalized services and monetization.

- Security and Scalability are Paramount: As the market grows, ensuring robust cybersecurity and scalable cloud infrastructure will remain critical challenges and differentiators.

Automotive Cloud Service Market Drivers Analysis

The Automotive Cloud Service Market is propelled by a confluence of technological advancements and evolving consumer demands. The escalating adoption of connected car technologies stands as a primary driver, as modern vehicles increasingly require constant connectivity for navigation, infotainment, and communication with external networks. This surge in connectivity generates immense volumes of data, which necessitate scalable cloud infrastructure for efficient storage, processing, and analysis. Furthermore, the automotive industry's pivot towards software-defined vehicles, where functionalities are increasingly managed and updated via software, inherently relies on robust cloud platforms for continuous deployment and remote configuration, minimizing the need for physical vehicle servicing.

Another significant driver is the global push towards autonomous driving and advanced driver-assistance systems (ADAS). These sophisticated systems demand low-latency, high-bandwidth communication and complex data processing capabilities that only cloud services can reliably provide, especially for real-time mapping, sensor fusion, and decision-making algorithms. Additionally, the growing consumer expectation for personalized in-car experiences, subscription-based services, and seamless integration with smart devices further fuels the demand for cloud-enabled solutions. Regulatory mandates for vehicle safety, emissions monitoring, and data privacy also indirectly contribute to market growth by requiring advanced data management and compliance features inherent in cloud offerings.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption of Connected Car Technologies | +4.0% | Global, particularly North America, Europe, China | Short to Medium Term (2025-2029) |

| Growth in Autonomous Driving and ADAS Development | +3.5% | North America, Europe, Japan, South Korea | Medium to Long Term (2027-2033) |

| Demand for Over-the-Air (OTA) Updates | +3.0% | Global | Short to Medium Term (2025-2030) |

| Shift towards Software-Defined Vehicles (SDVs) | +3.0% | Global, particularly developed markets | Medium to Long Term (2026-2033) |

| Rising Consumer Expectation for In-Car Digital Services | +2.5% | Global | Short to Medium Term (2025-2029) |

| Data Monetization and Analytics Opportunities | +2.0% | Global | Medium to Long Term (2027-2033) |

| Fleet Management Optimization Needs | +1.5% | Global | Short to Medium Term (2025-2030) |

Automotive Cloud Service Market Restraints Analysis

Despite the significant growth potential, the Automotive Cloud Service Market faces several notable restraints. A paramount concern is data security and privacy. With sensitive vehicle and personal data being transmitted and stored in the cloud, cybersecurity breaches pose severe risks, potentially leading to financial losses, reputational damage, and erosion of consumer trust. The complexity of regulatory frameworks, particularly across different regions and countries concerning data residency and privacy (e.g., GDPR, CCPA), creates significant compliance challenges for market participants. Ensuring adherence to these diverse regulations adds layers of cost and complexity to cloud service deployment and management.

Another key restraint is the high initial investment and operational costs associated with migrating existing automotive systems to cloud infrastructure, or developing new cloud-native solutions. This can be a deterrent for smaller players or those with legacy systems. Furthermore, the need for robust and reliable network connectivity, particularly in remote or underserved areas, can limit the effectiveness and adoption of cloud-dependent automotive services. Latency issues, especially for safety-critical autonomous driving applications that require real-time decision-making, present a technical hurdle that demands advanced edge computing integration and ultra-low-latency networks to overcome, adding to the overall cost and complexity of the cloud ecosystem.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Security and Privacy Concerns | -2.8% | Global, especially EU, North America | Short to Long Term (2025-2033) |

| High Implementation and Operational Costs | -2.2% | Global | Short to Medium Term (2025-2030) |

| Lack of Standardization and Interoperability | -1.8% | Global | Medium Term (2026-2031) |

| Regulatory Complexities and Compliance | -1.5% | EU, China, North America | Short to Long Term (2025-2033) |

| Network Connectivity and Latency Issues | -1.2% | Emerging Markets, Rural Areas | Short to Medium Term (2025-2030) |

Automotive Cloud Service Market Opportunities Analysis

The Automotive Cloud Service Market is ripe with numerous opportunities for growth and innovation. The proliferation of electric vehicles (EVs) presents a significant avenue, as cloud services are crucial for optimizing battery performance, managing charging infrastructure, and enabling smart grid integration. As the world moves towards sustainable transportation, the demand for sophisticated cloud solutions to support the EV ecosystem will only intensify. Furthermore, the emergence of Vehicle-to-Everything (V2X) communication technologies offers a substantial opportunity, where cloud platforms can facilitate real-time data exchange between vehicles, infrastructure, and smart devices, enhancing safety, traffic flow, and overall smart city initiatives.

Another compelling opportunity lies in the development of new subscription-based business models. With cloud integration, automotive manufacturers can offer a range of on-demand features and services, from advanced driver assistance functionalities to personalized infotainment packages, creating recurring revenue streams and enhancing customer loyalty. The untapped potential in emerging markets, particularly in Asia Pacific and Latin America, also presents a substantial opportunity for market expansion, as these regions witness increasing vehicle sales and a growing demand for advanced digital features. Moreover, advancements in edge computing, which complements cloud services by processing data closer to the source, will unlock new possibilities for real-time, low-latency applications, particularly for autonomous driving and other safety-critical functions, thereby expanding the overall scope and utility of automotive cloud services.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Electric Vehicle (EV) Ecosystem | +3.5% | Global, particularly Europe, China, North America | Medium to Long Term (2027-2033) |

| Development of V2X Communication Technology | +3.0% | North America, Europe, Asia Pacific | Medium to Long Term (2028-2033) |

| Expansion of Subscription-Based Services and Features | +2.5% | Global | Short to Medium Term (2025-2030) |

| Leveraging Edge Computing for Real-time Applications | +2.0% | Global | Medium to Long Term (2027-2033) |

| Untapped Potential in Emerging Markets | +1.8% | Asia Pacific, Latin America, Middle East & Africa | Short to Medium Term (2025-2030) |

Automotive Cloud Service Market Challenges Impact Analysis

The Automotive Cloud Service Market faces distinct challenges that require strategic navigation to sustain growth and ensure robust operations. One significant challenge is interoperability and integration complexity. The automotive ecosystem involves a multitude of stakeholders, including OEMs, Tier 1 suppliers, software developers, and cloud providers, each with proprietary systems and protocols. Ensuring seamless data exchange and functional integration across these diverse platforms is a complex task that can hinder widespread adoption and efficient service delivery. Moreover, the sheer volume and velocity of data generated by connected and autonomous vehicles present a substantial management challenge. Storing, processing, and analyzing petabytes of data in a cost-effective and timely manner requires sophisticated cloud architectures and advanced data management strategies.

Another critical challenge is the acute shortage of skilled professionals in both cloud computing and automotive domains. The unique blend of expertise required to develop, deploy, and maintain advanced automotive cloud services is in high demand, leading to recruitment difficulties and increased operational costs. Furthermore, ensuring quality of service (QoS) and reliability, particularly for mission-critical applications like ADAS and autonomous driving, is paramount. Any downtime or performance degradation in cloud services can have severe safety implications, necessitating stringent service level agreements (SLAs) and resilient infrastructure. Addressing these multifaceted challenges is essential for market participants to unlock the full potential of automotive cloud services and maintain a competitive edge.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Interoperability and Integration Complexity | -2.5% | Global | Short to Long Term (2025-2033) |

| Managing Massive Volumes of Vehicle Data | -2.0% | Global | Medium to Long Term (2027-2033) |

| Shortage of Skilled Cloud & Automotive Professionals | -1.7% | Global | Short to Medium Term (2025-2030) |

| Ensuring Quality of Service (QoS) and Reliability | -1.5% | Global | Short to Long Term (2025-2033) |

| Compliance with Evolving International Regulations | -1.0% | EU, China, North America | Short to Long Term (2025-2033) |

Automotive Cloud Service Market - Updated Report Scope

This comprehensive market report delves into the intricate dynamics of the Automotive Cloud Service Market, providing an in-depth analysis of its current state, historical performance, and future growth trajectories. The scope encompasses detailed segmentation by service type, deployment model, application, vehicle type, and end-user, offering granular insights into each sub-segment's contribution and potential. Furthermore, the report provides a thorough examination of market drivers, restraints, opportunities, and challenges, coupled with a robust AI impact analysis, to present a holistic view of the market ecosystem. It also highlights regional disparities and the competitive landscape, profiling key industry players to offer strategic intelligence for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.2 Billion |

| Market Forecast in 2033 | USD 29.4 Billion |

| Growth Rate | 21.5% |

| Number of Pages | 265 |

| Key Trends | |

| Segments Covered | |

| Key Companies Covered | Amazon Web Services (AWS), Microsoft Azure, Google Cloud Platform, IBM, BlackBerry QNX, Harman International (Samsung subsidiary), NXP Semiconductors, NVIDIA, Qualcomm, Continental AG, Robert Bosch GmbH, Aptiv PLC, ZF Friedrichshafen AG, Denso Corporation, Ericsson, AT&T, Verizon, Vodafone, Tata Consultancy Services (TCS), Capgemini |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Cloud Service market is intricately segmented across various dimensions to provide a granular understanding of its diverse components and growth drivers. These segmentations allow for a detailed analysis of specific market niches, enabling stakeholders to identify high-potential areas and tailor their strategies accordingly. By breaking down the market based on service types, deployment models, specific applications, vehicle types, and the ultimate end-users, this analysis illuminates the various facets of demand and supply within the evolving automotive cloud ecosystem.

Each segment reflects distinct needs and technological requirements, contributing uniquely to the overall market landscape. For instance, the differentiation between public, private, and hybrid cloud models highlights varying preferences for scalability, security, and cost-efficiency among automotive players. Similarly, the diverse range of applications, from infotainment to autonomous driving, underscores the broad utility and transformative potential of cloud services across all aspects of modern vehicle operation and passenger experience. Understanding these segmentations is crucial for navigating the complexities of the automotive cloud service market and capitalizing on its inherent opportunities.

- By Service Type: This segment includes Infrastructure as a Service (IaaS), Platform as a Service (PaaS), and Software as a Service (SaaS). IaaS provides fundamental computing resources, PaaS offers a platform for developing applications, and SaaS delivers ready-to-use software applications over the internet.

- By Deployment Model: This covers Public Cloud, Private Cloud, and Hybrid Cloud. Public cloud offers services over the internet to multiple customers, private cloud is dedicated to a single organization, and hybrid cloud combines elements of both.

- By Application: Key applications include Infotainment & Telematics, Advanced Driver-Assistance Systems (ADAS), Autonomous Driving, Predictive Maintenance, Fleet Management, Vehicle-to-Everything (V2X) Communication, and Over-the-Air (OTA) Updates. These represent the diverse functionalities enabled by cloud services in vehicles.

- By Vehicle Type: This segment differentiates between Passenger Vehicles, Commercial Vehicles, and Electric Vehicles. Each vehicle type has unique requirements and adoption rates for cloud services.

- By End User: End users include Automotive OEMs (Original Equipment Manufacturers), Tier 1 Suppliers, Fleet Operators, and Mobility Service Providers. These entities leverage automotive cloud services for various operational and strategic purposes.

Regional Highlights

- North America: This region is a leading market for automotive cloud services, characterized by rapid technological adoption, significant investments in connected car technologies, and the presence of major cloud service providers and automotive innovators. The strong focus on autonomous driving R&D and advanced telematics contributes significantly to market growth.

- Europe: Europe showcases robust growth driven by stringent regulatory frameworks for vehicle safety and emissions, a strong emphasis on data privacy (e.g., GDPR), and the proactive development of V2X communication standards. The region's luxury vehicle segment and high demand for premium in-car experiences also fuel cloud service adoption.

- Asia Pacific (APAC): APAC is anticipated to be the fastest-growing market, propelled by increasing vehicle production, a surging demand for connected cars in countries like China, India, and Japan, and government initiatives promoting smart cities and electric vehicle infrastructure. The region also benefits from a vast consumer base keen on adopting new automotive technologies.

- Latin America: This region presents a growing market opportunity, primarily driven by urbanization, increasing adoption of vehicle tracking and fleet management solutions, and evolving digital infrastructure. Economic development and rising disposable incomes are gradually accelerating the demand for connected vehicle services.

- Middle East & Africa (MEA): The MEA region is an emerging market with potential driven by investments in smart city projects, diversification of economies away from oil, and a growing consumer interest in advanced automotive technologies. The demand for fleet management and telematics services in logistics and transportation sectors is also a significant contributor.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Cloud Service Market.- Amazon Web Services (AWS)

- Microsoft Azure

- Google Cloud Platform

- IBM

- BlackBerry QNX

- Harman International (Samsung subsidiary)

- NXP Semiconductors

- NVIDIA

- Qualcomm

- Continental AG

- Robert Bosch GmbH

- Aptiv PLC

- ZF Friedrichshafen AG

- Denso Corporation

- Ericsson

- AT&T

- Verizon

- Vodafone

- Tata Consultancy Services (TCS)

- Capgemini

Frequently Asked Questions

What is the projected growth rate for the Automotive Cloud Service Market?

The Automotive Cloud Service Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.5% between 2025 and 2033, reaching an estimated USD 29.4 billion by 2033 from USD 6.2 billion in 2025.

What are the primary drivers for the Automotive Cloud Service Market?

Key drivers include the increasing adoption of connected car technologies, the growth in autonomous driving development, demand for Over-the-Air (OTA) updates, and the shift towards software-defined vehicles, all requiring robust cloud infrastructure.

How does AI impact the Automotive Cloud Service sector?

AI significantly enhances the automotive cloud by enabling advanced data processing for predictive maintenance, supporting autonomous driving capabilities, personalizing user experiences, and improving cybersecurity measures through intelligent analytics.

What are the main challenges faced by the Automotive Cloud Service Market?

Major challenges include ensuring data security and privacy, managing massive volumes of vehicle data, overcoming interoperability and integration complexities, and addressing the shortage of skilled cloud and automotive professionals.

Which applications are most significantly impacted by automotive cloud services?

Applications most impacted include infotainment & telematics, Advanced Driver-Assistance Systems (ADAS), autonomous driving, predictive maintenance, fleet management, Vehicle-to-Everything (V2X) communication, and Over-the-Air (OTA) updates.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted