Automotive Casting Market

Automotive Casting Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702439 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

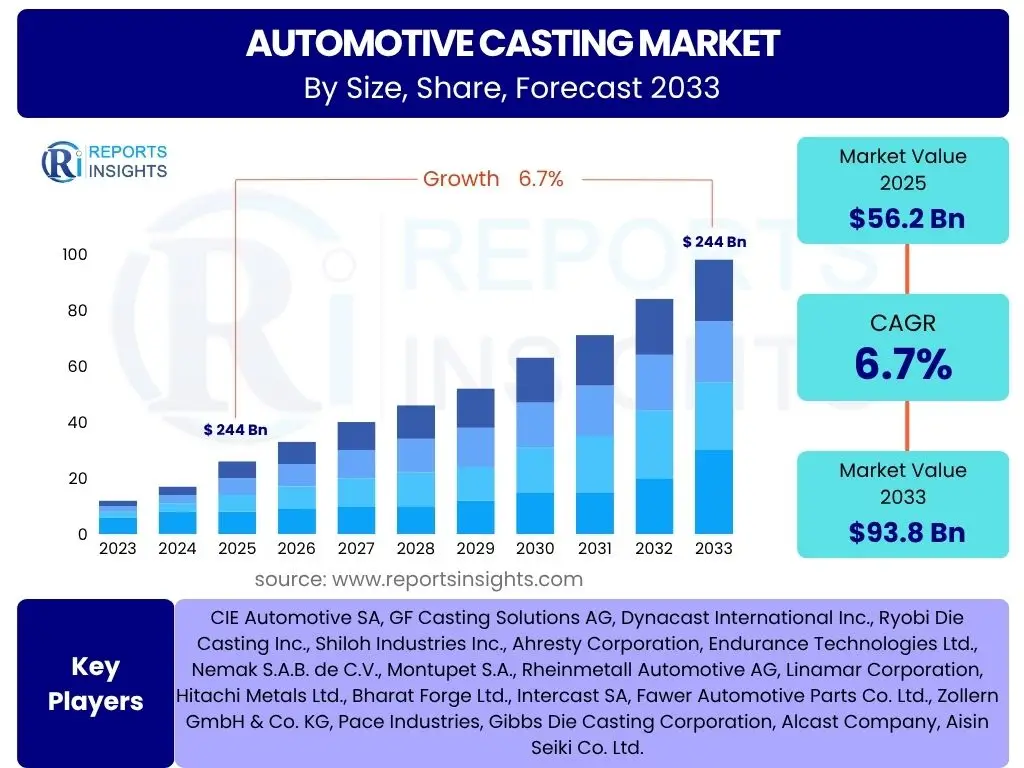

Automotive Casting Market Size

According to Reports Insights Consulting Pvt Ltd, The Automotive Casting Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 56.2 Billion in 2025 and is projected to reach USD 93.8 Billion by the end of the forecast period in 2033.

Key Automotive Casting Market Trends & Insights

User queries regarding the Automotive Casting market frequently revolve around the evolution of manufacturing processes, material innovations, and the overarching influence of electrification on traditional automotive components. There is significant interest in how the industry is adapting to demands for lighter, more efficient, and sustainable parts. Key themes include the shift towards advanced alloys, the integration of smart manufacturing techniques, and the critical role of casting in developing next-generation vehicle architectures.

The market is witnessing a profound transformation driven by stringent emission regulations and the rapid adoption of electric vehicles. This necessitates continuous innovation in casting technologies to produce high-performance, lightweight components that contribute to fuel efficiency and extended battery range. Furthermore, supply chain resilience and localized production are emerging as significant areas of focus for market participants.

- Lightweighting initiatives continue to dominate product development, focusing on aluminum and magnesium alloys.

- Increased demand for cast components in Electric Vehicles (EVs), including motor housings, battery casings, and structural parts.

- Adoption of advanced manufacturing processes such as vacuum die casting and high-pressure die casting for complex geometries.

- Integration of sustainable practices and recycled materials in the casting process to reduce environmental impact.

- Digitalization and Industry 4.0 principles, including sensor integration and data analytics, are optimizing production efficiency.

AI Impact Analysis on Automotive Casting

Common user questions concerning Artificial Intelligence's impact on Automotive Casting highlight expectations for enhanced operational efficiency, improved product quality, and cost reductions. Users are keen to understand how AI can be leveraged in design optimization, predictive maintenance of machinery, and intelligent quality control systems. There is also a level of inquiry into the potential for AI to streamline supply chain management and accelerate research and development cycles within the casting industry.

AI technologies are poised to revolutionize various stages of the automotive casting value chain, from initial design and simulation to post-production quality assurance. By processing vast datasets, AI algorithms can identify optimal parameters for casting processes, predict equipment failures before they occur, and detect microscopic defects in cast components, leading to superior product outcomes and minimized waste. This intelligent automation can significantly reduce human error and improve throughput.

- Enhanced design and simulation capabilities through AI-driven generative design and topology optimization.

- Predictive maintenance for casting machinery, reducing downtime and extending equipment lifespan.

- Automated quality inspection systems utilizing computer vision and machine learning for defect detection.

- Optimization of casting parameters (temperature, pressure, cycle time) for improved yield and material efficiency.

- Supply chain optimization and demand forecasting through AI-powered analytics.

Key Takeaways Automotive Casting Market Size & Forecast

User inquiries about key takeaways from the Automotive Casting market size and forecast reveal a focus on understanding the primary drivers of growth, the long-term viability of traditional components versus new EV-specific parts, and the overall stability of the market. There's a strong interest in identifying the most influential factors shaping investment decisions and strategic planning within the sector. The shift towards electrification and sustainable manufacturing practices is consistently a central theme.

The automotive casting market is undergoing a significant transformation, driven by the imperative for lightweighting and the accelerating transition to electric vehicles. While traditional powertrain components will see gradual shifts, the demand for specialized castings for EV platforms, such as battery housings and motor enclosures, is projected to surge. This dual evolution underscores the need for casting companies to adapt their processes and material expertise to remain competitive and capitalize on emerging opportunities.

- The market is poised for steady growth, primarily fueled by the global shift towards electric and hybrid vehicles.

- Lightweight materials, particularly aluminum and magnesium, will experience increased adoption for their contribution to vehicle efficiency.

- Technological advancements in casting processes are crucial for meeting the complex demands of modern automotive designs.

- Sustainability and circular economy principles are becoming integral to casting operations, influencing material selection and production methods.

- Emerging economies present significant growth avenues due to rising vehicle production and increasing consumer disposable income.

Automotive Casting Market Drivers Analysis

The Automotive Casting market is propelled by a confluence of factors stemming from evolving automotive industry demands and global economic trends. The most prominent driver is the relentless pursuit of lightweight vehicle components, essential for improving fuel efficiency in internal combustion engine (ICE) vehicles and extending the range of electric vehicles (EVs). This demand directly translates into increased adoption of advanced casting materials and processes capable of producing lighter yet robust parts.

Another significant driver is the global increase in automotive production, particularly in emerging markets, coupled with the escalating demand for electric and hybrid vehicles. As manufacturers commit more resources to EV development, the need for specialized cast parts for battery casings, motor housings, and structural components becomes paramount. Additionally, stringent emission regulations worldwide are compelling manufacturers to reduce vehicle weight and improve engine efficiency, further boosting the demand for high-performance cast solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Lightweight Vehicles | +1.8% | Global, particularly North America, Europe, Asia Pacific | Short to Long Term (2025-2033) |

| Rising Production of Electric Vehicles (EVs) | +2.1% | Global, particularly China, Europe, North America | Short to Long Term (2025-2033) |

| Strict Environmental and Emission Regulations | +1.5% | Europe, North America, Asia Pacific (e.g., China, India) | Medium to Long Term (2027-2033) |

| Technological Advancements in Casting Processes | +1.3% | Global | Short to Medium Term (2025-2030) |

| Growth in Automotive Production in Emerging Economies | +1.0% | Asia Pacific (e.g., India, Southeast Asia), Latin America | Medium to Long Term (2028-2033) |

Automotive Casting Market Restraints Analysis

Despite robust growth prospects, the Automotive Casting market faces several significant restraints that could impede its expansion. One primary concern is the volatility of raw material prices, particularly for aluminum, iron, and magnesium. Fluctuations in these prices can directly impact production costs, squeezing profit margins for casting manufacturers and potentially leading to price increases for automotive OEMs, thereby affecting overall vehicle affordability.

Another key restraint involves the substantial capital investment required for modern casting facilities and advanced machinery. The high upfront costs associated with setting up or upgrading casting plants, coupled with the need for continuous research and development to stay competitive, can be a barrier to entry for new players and a challenge for existing ones, especially smaller and medium-sized enterprises. Furthermore, stringent environmental regulations regarding emissions and waste disposal impose additional costs and operational complexities on casting foundries.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -1.2% | Global | Short to Medium Term (2025-2030) |

| High Initial Investment and Operating Costs | -0.8% | Global | Long Term (2025-2033) |

| Stringent Environmental Regulations | -0.7% | Europe, North America, Asia Pacific | Medium to Long Term (2027-2033) |

| Competition from Alternative Manufacturing Processes | -0.6% | Global | Medium to Long Term (2028-2033) |

| Skilled Labor Shortage | -0.5% | North America, Europe, parts of Asia Pacific | Short to Long Term (2025-2033) |

Automotive Casting Market Opportunities Analysis

The Automotive Casting market is ripe with opportunities driven by technological advancements and shifting industry paradigms. A significant opportunity lies in the burgeoning electric vehicle (EV) segment, which demands new and specialized cast components such as battery housings, motor casings, and complex structural parts that optimize weight and integrate multiple functions. This shift allows casting manufacturers to innovate with new alloys and designs tailored for EV performance and safety requirements.

Another promising area is the continuous development of advanced materials, including high-strength aluminum alloys, magnesium alloys, and composite materials that offer superior strength-to-weight ratios. The integration of digitalization and Industry 4.0 technologies, such as IoT sensors, AI, and advanced analytics, presents an opportunity to optimize casting processes, enhance quality control, and achieve greater operational efficiency. Furthermore, the increasing focus on circular economy principles creates opportunities for developing advanced recycling techniques and utilizing secondary raw materials, aligning with global sustainability goals.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion in Electric Vehicle (EV) Component Production | +1.9% | Global, particularly China, Europe, North America | Short to Long Term (2025-2033) |

| Development of New and Advanced Light Alloys | +1.4% | Global | Medium to Long Term (2027-2033) |

| Adoption of Smart Manufacturing and Industry 4.0 Technologies | +1.2% | Global, particularly developed economies | Short to Medium Term (2025-2030) |

| Focus on Sustainable and Recycled Materials | +0.9% | Europe, North America | Medium to Long Term (2028-2033) |

| Customization and Prototyping for Niche Applications | +0.8% | Global | Short to Medium Term (2025-2030) |

Automotive Casting Market Challenges Impact Analysis

The Automotive Casting market contends with several notable challenges that demand strategic responses from industry players. A persistent challenge is the need to manage the high energy consumption inherent in casting processes, which directly impacts operational costs and carbon footprint. Fluctuating energy prices and the global push for decarbonization necessitate significant investment in energy-efficient technologies and renewable energy sources, adding complexity to manufacturing operations.

Another critical challenge is the intense competition from alternative manufacturing processes, such as stamping, forging, and additive manufacturing (3D printing). While casting offers unique advantages for complex geometries and material properties, these alternative methods are continuously evolving, putting pressure on casting manufacturers to innovate and demonstrate superior cost-effectiveness and performance. Furthermore, maintaining stringent quality control for increasingly intricate and lightweight cast components remains a significant technical hurdle, requiring advanced inspection technologies and skilled personnel.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Energy Cost Fluctuations and High Energy Consumption | -1.1% | Global | Short to Long Term (2025-2033) |

| Maintaining High Quality for Complex, Lightweight Parts | -0.9% | Global | Short to Long Term (2025-2033) |

| Waste Management and Environmental Compliance | -0.8% | Global, particularly developed regions | Medium to Long Term (2027-2033) |

| Adapting to Rapid Technological Shifts | -0.7% | Global | Short to Medium Term (2025-2030) |

| Global Supply Chain Disruptions | -0.6% | Global | Short to Medium Term (2025-2028) |

Automotive Casting Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global Automotive Casting market, providing an in-depth analysis of market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. It offers strategic insights for stakeholders to navigate the evolving landscape shaped by technological advancements, regulatory changes, and the accelerating transition towards vehicle electrification.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 56.2 Billion |

| Market Forecast in 2033 | USD 93.8 Billion |

| Growth Rate | 6.7% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | CIE Automotive SA, GF Casting Solutions AG, Dynacast International Inc., Ryobi Die Casting Inc., Shiloh Industries Inc., Ahresty Corporation, Endurance Technologies Ltd., Nemak S.A.B. de C.V., Montupet S.A., Rheinmetall Automotive AG, Linamar Corporation, Hitachi Metals Ltd., Bharat Forge Ltd., Intercast SA, Fawer Automotive Parts Co. Ltd., Zollern GmbH & Co. KG, Pace Industries, Gibbs Die Casting Corporation, Alcast Company, Aisin Seiki Co. Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive Casting market is extensively segmented to provide a granular view of its diverse landscape, reflecting the varied materials, manufacturing processes, application areas, and vehicle types that constitute this critical industry. This segmentation allows for a precise understanding of market dynamics within each niche, identifying areas of high growth, emerging demand, and competitive intensity. Analyzing these segments helps stakeholders tailor strategies to specific market needs and technological advancements.

- By Material:

- Aluminum: Dominates due to lightweighting trends and versatility for various components.

- Iron: Traditionally used for engine blocks and heavy-duty parts, seeing continued use in specific applications.

- Magnesium: Gaining traction for ultra-lightweight components, particularly in high-performance and EV applications.

- Zinc: Utilized for smaller, intricate components requiring high precision.

- Other Alloys: Includes various specialized alloys for specific performance requirements.

- By Process:

- Die Casting:

- High-Pressure Die Casting (HPDC): Widely used for complex, thin-walled components at high volumes.

- Low-Pressure Die Casting (LPDC): Preferred for larger, structural components with controlled solidification.

- Gravity Die Casting (GDC): Suitable for relatively simpler parts with good mechanical properties.

- Sand Casting: Traditional method for larger, more intricate parts, or low-volume production.

- Investment Casting: Used for high-precision, complex geometries with excellent surface finish.

- Others: Includes processes like squeeze casting and continuous casting.

- Die Casting:

- By Application:

- Engine Components: Cylinder Blocks, Cylinder Heads, Crankshafts, Pistons, Manifolds.

- Transmission Components: Gearboxes, Housings, Clutch Housings.

- Body Components: Chassis Parts, Structural Components, Shock Towers, Door Frames.

- Braking Components: Calipers, Drums, Brackets.

- Steering Components: Steering Housings, Brackets.

- Others: Various smaller components and sub-assemblies.

- By Vehicle Type:

- Passenger Vehicles: Sedans, SUVs, Hatchbacks, Luxury Cars.

- Commercial Vehicles: Light Commercial Vehicles (LCVs), Medium & Heavy Commercial Vehicles (M&HCVs).

- Electric Vehicles: Battery Electric Vehicles (BEVs), Plug-in Hybrid Electric Vehicles (PHEVs), Hybrid Electric Vehicles (HEVs).

- By End-Use:

- Original Equipment Manufacturer (OEM): Direct supply to vehicle manufacturers for new vehicle assembly.

- Aftermarket: Supply of replacement parts and components for vehicle maintenance and repair.

Regional Highlights

- Asia Pacific (APAC): The APAC region stands as the dominant market for automotive casting, primarily driven by the colossal automotive manufacturing bases in China, India, Japan, and South Korea. Rapid urbanization, increasing disposable incomes, and the burgeoning electric vehicle ecosystem in these countries are fueling demand. China, in particular, leads in both vehicle production and EV adoption, making it a critical hub for casting activities and innovation. The region benefits from a robust supply chain and significant investments in advanced manufacturing technologies.

- Europe: Europe represents a mature yet highly innovative market, characterized by stringent emission norms and a strong emphasis on premium and electric vehicles. Countries like Germany, France, and Italy are at the forefront of automotive design and engineering, necessitating advanced casting solutions for lightweighting and performance. The region's focus on sustainability also drives the adoption of eco-friendly casting processes and recycled materials. Investment in next-generation manufacturing facilities is common to meet the evolving demands of its sophisticated automotive industry.

- North America: North America is a significant market, influenced by robust demand for SUVs and light trucks, and a growing shift towards electric vehicles. The region is characterized by substantial investments from major automotive OEMs and a focus on advanced manufacturing techniques, including high-pressure die casting. Efforts to reshore manufacturing and strengthen regional supply chains are also contributing to the market's dynamics. Research and development into new materials and processes, particularly for improving fuel efficiency and EV range, are key drivers.

- Latin America: The Latin American market for automotive casting is experiencing steady growth, largely propelled by increasing automotive production in Brazil, Mexico, and Argentina. Economic development, a rising middle class, and expanding vehicle fleets contribute to the demand for both OEM and aftermarket casting components. While the region faces economic fluctuations, long-term growth is anticipated due to expanding manufacturing capabilities and regional trade agreements supporting automotive exports.

- Middle East and Africa (MEA): The MEA region is an emerging market for automotive casting, with growth influenced by expanding automotive assembly plants and infrastructure development. Countries like South Africa, Turkey, and some GCC nations are investing in their automotive sectors. While smaller in scale compared to other regions, the market shows potential for growth, particularly in aftermarket demand and as regional manufacturing capabilities mature and expand to meet local and export requirements.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Casting Market.- CIE Automotive SA

- GF Casting Solutions AG

- Dynacast International Inc.

- Ryobi Die Casting Inc.

- Shiloh Industries Inc.

- Ahresty Corporation

- Endurance Technologies Ltd.

- Nemak S.A.B. de C.V.

- Montupet S.A.

- Rheinmetall Automotive AG

- Linamar Corporation

- Hitachi Metals Ltd.

- Bharat Forge Ltd.

- Intercast SA

- Fawer Automotive Parts Co. Ltd.

- Zollern GmbH & Co. KG

- Pace Industries

- Gibbs Die Casting Corporation

- Alcast Company

- Aisin Seiki Co. Ltd.

Frequently Asked Questions

Analyze common user questions about the Automotive Casting market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is automotive casting?

Automotive casting is a manufacturing process that involves pouring molten metal into a mold to create components for vehicles. These components are critical for various systems, including engines, transmissions, chassis, and body structures, and are designed to meet stringent specifications for strength, weight, and durability.

How is the rise of electric vehicles impacting the automotive casting market?

The rise of electric vehicles (EVs) significantly impacts the market by shifting demand from traditional powertrain components to new parts like battery housings, motor casings, and lightweight structural components. This drives innovation in casting processes and the use of materials like aluminum and magnesium to reduce vehicle weight and extend battery range.

What are the primary materials used in automotive casting?

The primary materials used in automotive casting include aluminum alloys, iron (gray iron, ductile iron), magnesium alloys, and zinc alloys. Aluminum and magnesium are increasingly preferred for lightweighting initiatives, while iron remains vital for high-strength, durable components.

What are the key trends shaping the automotive casting industry?

Key trends include the relentless pursuit of lightweighting, accelerated adoption of electric vehicle component production, integration of smart manufacturing technologies (Industry 4.0), emphasis on sustainable and circular economy practices, and the development of advanced casting processes for complex geometries.

What challenges does the automotive casting market face?

The market faces challenges such as volatile raw material and energy prices, high initial investment costs for advanced facilities, stringent environmental regulations, intense competition from alternative manufacturing methods like forging and stamping, and the ongoing need for skilled labor.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted