Automotive ADA Market

Automotive ADA Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705822 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

Automotive ADA Market Size

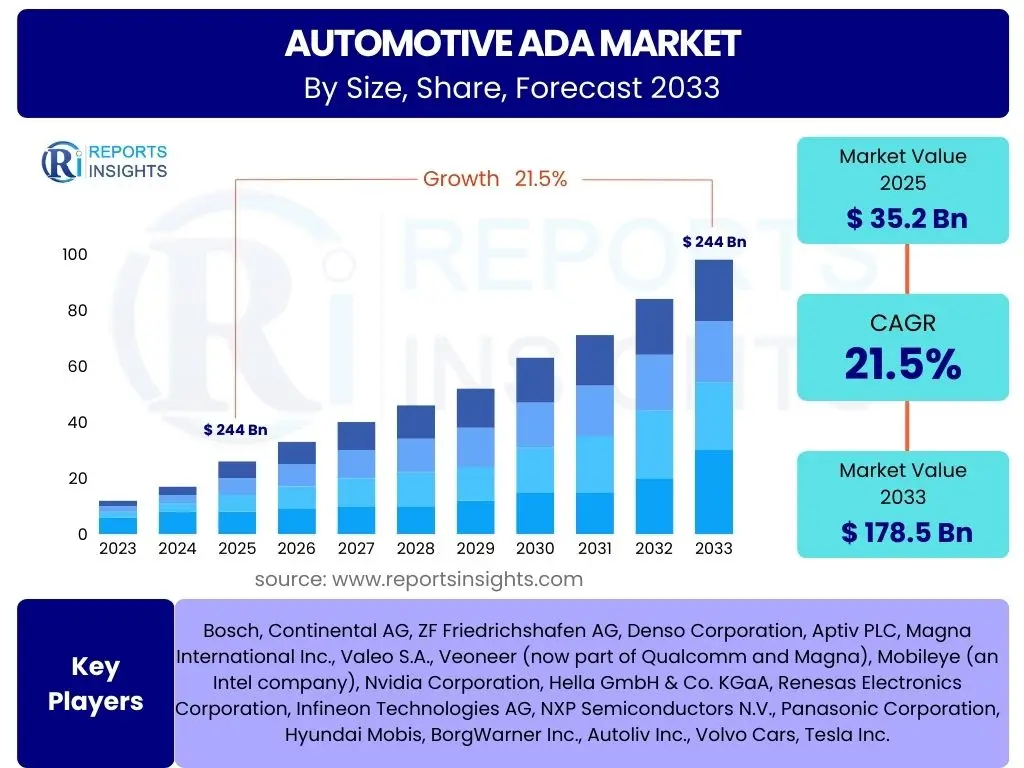

According to Reports Insights Consulting Pvt Ltd, The Automotive ADA Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.5% between 2025 and 2033. The market is estimated at USD 35.2 Billion in 2025 and is projected to reach USD 178.5 Billion by the end of the forecast period in 2033.

Key Automotive ADA Market Trends & Insights

The Automotive Advanced Driver Assistance Systems (ADA) market is witnessing rapid evolution driven by technological convergence, regulatory pressures, and shifting consumer expectations. Common user inquiries often revolve around the most significant technological advancements, the influence of electrification, and the role of connectivity in shaping future ADA landscapes. Users are keen to understand how sensor fusion, artificial intelligence, and software-defined architectures are fundamentally transforming vehicle capabilities and safety standards.

A prominent trend is the increasing integration of sophisticated sensor technologies, including high-resolution cameras, advanced radar, and LiDAR systems, which are becoming more compact and cost-effective. This proliferation enables more accurate environmental perception and robust decision-making for ADA functionalities. Furthermore, the push towards higher levels of autonomous driving, particularly Level 2+ and Level 3, is compelling manufacturers to invest heavily in redundant systems and fail-safe mechanisms, thereby expanding the market for complex ADA suites.

Another critical insight is the symbiotic relationship between ADA development and vehicle electrification. Electric vehicles (EVs) often serve as ideal platforms for integrating advanced electronics and software, fostering innovation in battery management systems that can also power sophisticated ADA components. The rise of software-defined vehicles (SDVs) is also a transformative trend, allowing for over-the-air (OTA) updates for ADA features, enabling continuous improvement and personalization, which resonates strongly with modern consumers seeking upgradeable vehicle experiences.

- Integration of advanced sensor fusion technologies (e.g., LiDAR, radar, camera).

- Rapid progression towards higher levels of autonomous driving (Level 2+ and Level 3).

- Increasing adoption of software-defined vehicle architectures and OTA updates.

- Convergence of ADA systems with vehicle electrification trends.

- Growing demand for personalized and upgradeable safety and convenience features.

AI Impact Analysis on Automotive ADA

User questions frequently address the transformative impact of artificial intelligence (AI) on Automotive Advanced Driver Assistance Systems (ADA), particularly regarding its role in enhancing system intelligence, reliability, and predictive capabilities. There is a strong interest in understanding how AI algorithms contribute to more accurate environmental perception, improved decision-making in complex scenarios, and the overall progression towards fully autonomous vehicles. Users also express concerns about the ethical implications of AI-driven decisions and the robustness of AI systems in diverse driving conditions.

AI's influence is pervasive, enabling sophisticated data processing from multiple sensors to create a comprehensive and dynamic understanding of the vehicle's surroundings. Machine learning algorithms are crucial for pattern recognition, object classification, and predicting the behavior of other road users, which are foundational for functions like adaptive cruise control, lane keeping assist, and automatic emergency braking. This cognitive leap allows ADA systems to react more intelligently and preemptively than traditional rule-based systems, significantly improving safety and driving comfort.

Moreover, AI is pivotal in facilitating the development of self-learning ADA systems that can continuously improve performance through real-world data collection and analysis. This capability extends beyond basic functions to advanced features such as predictive maintenance for ADA components, optimized route planning incorporating real-time traffic and weather, and personalized driver assistance based on individual driving styles. The continuous evolution of AI models promises to unlock new levels of autonomy and functionality, addressing user expectations for safer, smarter, and more intuitive vehicles, while also necessitating robust validation and ethical frameworks.

- Enhanced perception and environmental understanding through AI-powered sensor fusion.

- Improved decision-making and predictive capabilities for ADAS functions.

- Facilitation of self-learning and adaptive ADAS systems through machine learning.

- Development of advanced features like predictive maintenance and optimized driving.

- Addressing ethical considerations and ensuring robust AI performance in diverse scenarios.

Key Takeaways Automotive ADA Market Size & Forecast

Common inquiries about the Automotive ADA market size and forecast center on understanding the primary growth drivers, the long-term outlook for market expansion, and the most significant opportunities for stakeholders. Users seek concise summaries of what truly propels this market forward and what strategic implications these trends hold for investment and development. The essence of these questions is to distill complex market dynamics into actionable insights, highlighting the critical factors influencing the trajectory of Automotive ADA adoption and technological advancement.

A key takeaway is the robust and sustained growth projected for the Automotive ADA market, driven predominantly by escalating global safety regulations and increasing consumer demand for advanced safety and convenience features. Governments worldwide are introducing stricter mandates for the inclusion of specific ADA functionalities, such as Automatic Emergency Braking (AEB) and Lane Keeping Assist (LKA), which serves as a significant market accelerator. This regulatory push, combined with a growing awareness among consumers about the life-saving potential of these technologies, ensures a consistent baseline for market expansion.

Furthermore, the continuous technological advancements, particularly in sensor technology, AI, and connectivity, are not only enhancing the capabilities of existing ADA systems but also enabling the development of new, more sophisticated functions. This innovation cycle is critical for market penetration and value addition. The long-term forecast indicates that the market will continue its upward trajectory, bolstered by the transition towards semi-autonomous and fully autonomous vehicles, which inherently rely on highly integrated and advanced ADA platforms, presenting substantial revenue opportunities for industry participants across the value chain.

- Significant market growth driven by global safety regulations and consumer demand.

- Technological innovation in sensors, AI, and connectivity fueling new ADA functionalities.

- Strong revenue opportunities for component suppliers, software developers, and OEMs.

- Continued evolution towards higher levels of autonomous driving as a primary growth vector.

- Asia Pacific and North America poised for substantial market expansion.

Automotive ADA Market Drivers Analysis

The Automotive ADA market is primarily driven by a confluence of stringent safety regulations, increasing consumer awareness regarding vehicle safety, and rapid technological advancements in sensor and computing capabilities. Governments globally are implementing mandates for the integration of specific ADAS features, propelling original equipment manufacturers (OEMs) to adopt and standardize these systems across vehicle segments. This regulatory landscape creates a foundational demand that continually expands the market size.

Moreover, rising disposable incomes in emerging economies, coupled with a preference for technologically advanced and safer vehicles, contribute significantly to market expansion. The integration of advanced features such as adaptive cruise control, lane departure warning, and blind-spot detection not only enhances safety but also improves driving comfort, leading to higher consumer acceptance and willingness to invest in vehicles equipped with these systems. The ongoing development of artificial intelligence and machine learning algorithms further refines ADA system performance, making them more reliable and attractive to end-users.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Safety Regulations & Mandates | +5.5% | Europe, North America, Asia Pacific (China, Japan) | Short to Mid-term (2025-2029) |

| Growing Consumer Demand for Safety & Convenience | +4.8% | North America, Europe, Asia Pacific | Mid to Long-term (2026-2033) |

| Technological Advancements in Sensors & AI | +6.2% | Global | Short to Long-term (2025-2033) |

| Rise in Premium & Luxury Vehicle Sales | +2.5% | Europe, North America, China | Mid-term (2027-2031) |

| Focus on Reducing Road Accidents & Fatalities | +2.5% | Global | Short to Long-term (2025-2033) |

Automotive ADA Market Restraints Analysis

Despite the robust growth trajectory, the Automotive ADA market faces several significant restraints that could impede its full potential. A primary challenge is the high cost associated with the integration of sophisticated ADA hardware and software components. Advanced sensor suites, high-performance electronic control units (ECUs), and complex algorithms significantly increase the overall manufacturing cost of vehicles, particularly for entry-level and mid-range segments, which can limit widespread adoption.

Another critical restraint involves the complexity and reliability concerns surrounding these advanced systems. Integrating multiple sensors and software platforms from various suppliers can lead to interoperability issues and increased potential for system malfunctions. Consumer apprehension regarding the reliability of autonomous features, coupled with the need for extensive testing and validation, poses a significant hurdle. Furthermore, cybersecurity vulnerabilities present a growing concern, as interconnected ADA systems become potential targets for malicious attacks, which could compromise vehicle safety and passenger data.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of ADA System Integration | -3.5% | Global, particularly developing markets | Short to Mid-term (2025-2029) |

| Complexity & Reliability Concerns of Systems | -2.8% | Global | Short to Mid-term (2025-2028) |

| Cybersecurity Risks & Data Privacy Concerns | -2.0% | Global | Mid to Long-term (2027-2033) |

| Lack of Standardized Testing & Regulations | -1.5% | Emerging Markets | Mid-term (2026-2030) |

| Limited Infrastructure Support for Advanced Features | -1.0% | Developing Regions | Long-term (2029-2033) |

Automotive ADA Market Opportunities Analysis

The Automotive ADA market presents substantial opportunities driven by evolving technological landscapes and emerging market needs. A significant opportunity lies in the continuous advancement of software-defined vehicles (SDVs), which enable over-the-air (OTA) updates for ADA functionalities. This capability allows manufacturers to deploy new features, improve existing ones, and fix bugs post-sale, generating new revenue streams through subscriptions and feature-on-demand models, and enhancing customer lifetime value.

Furthermore, the expansion into developing markets offers immense untapped potential. As these regions experience economic growth and increasing vehicle penetration, there will be a parallel rise in demand for basic to advanced safety features. Localized solutions and cost-effective ADA systems tailored to specific market needs and infrastructure conditions could unlock significant market share. The integration of Vehicle-to-Everything (V2X) communication technologies also presents a transformative opportunity, allowing vehicles to communicate with each other, infrastructure, and pedestrians, thereby enhancing the capabilities and effectiveness of ADA systems beyond what on-board sensors can achieve.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Software-Defined Vehicles & OTA Updates | +4.0% | Global, particularly developed markets | Mid to Long-term (2027-2033) |

| Integration with Vehicle-to-Everything (V2X) Communication | +3.5% | North America, Europe, Asia Pacific | Long-term (2029-2033) |

| Emergence of New Business Models (e.g., Feature-on-Demand) | +3.0% | Global | Mid-term (2026-2031) |

| Untapped Potential in Developing Markets | +2.5% | Asia Pacific (India, Southeast Asia), Latin America, MEA | Long-term (2028-2033) |

| Development of Cost-Effective Sensor Solutions | +2.0% | Global | Short to Mid-term (2025-2029) |

Automotive ADA Market Challenges Impact Analysis

The Automotive ADA market encounters various challenges that demand innovative solutions and collaborative efforts across the industry. One significant challenge is the ongoing need for regulatory harmonization across different regions and countries. Varying safety standards, testing protocols, and certification requirements can create complexities for global manufacturers seeking to deploy ADA systems uniformly, leading to increased development costs and slower market entry in certain jurisdictions.

Furthermore, consumer perception and trust remain critical hurdles. Despite the proven benefits of ADA, public apprehension about autonomous technologies, concerns over system reliability, and questions regarding liability in the event of an accident can deter adoption. Building trust through transparent communication, rigorous testing, and education about system limitations is paramount. Additionally, the rapid pace of technological change necessitates continuous investment in research and development, posing a financial challenge for smaller players and requiring established companies to constantly innovate to remain competitive, especially with the increasing demand for specialized talent in AI and software engineering.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Regulatory Harmonization Across Regions | -2.2% | Global | Mid-term (2026-2030) |

| Consumer Trust & Acceptance of Autonomous Features | -1.8% | Global | Short to Long-term (2025-2033) |

| High R&D Investment & Short Product Lifecycles | -1.5% | Global | Short to Mid-term (2025-2029) |

| Talent Shortage in AI & Software Engineering | -1.0% | North America, Europe, Asia Pacific | Mid to Long-term (2027-2033) |

| Ensuring Cybersecurity & Data Privacy | -0.8% | Global | Short to Long-term (2025-2033) |

Automotive ADA Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the Automotive Advanced Driver Assistance Systems (ADA) market, providing detailed insights into its current size, historical trends, and future growth projections. It covers key market dynamics including drivers, restraints, opportunities, and challenges, along with a thorough segmentation analysis by component, level of autonomy, vehicle type, application, and regional outlook. The report also profiles leading industry players, offering a holistic view of the competitive landscape and strategic developments shaping the market from 2025 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 35.2 Billion |

| Market Forecast in 2033 | USD 178.5 Billion |

| Growth Rate | 21.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Bosch, Continental AG, ZF Friedrichshafen AG, Denso Corporation, Aptiv PLC, Magna International Inc., Valeo S.A., Veoneer (now part of Qualcomm and Magna), Mobileye (an Intel company), Nvidia Corporation, Hella GmbH & Co. KGaA, Renesas Electronics Corporation, Infineon Technologies AG, NXP Semiconductors N.V., Panasonic Corporation, Hyundai Mobis, BorgWarner Inc., Autoliv Inc., Volvo Cars, Tesla Inc. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Automotive ADA market is broadly segmented across several key dimensions to provide a granular understanding of its diverse landscape and growth dynamics. These segmentations by component, level of autonomy, vehicle type, and application enable a precise analysis of technological adoption, market penetration, and revenue generation across various product categories and end-use sectors. Each segment represents a distinct area of innovation and consumer demand, contributing uniquely to the overall market trajectory.

The component segmentation highlights the critical hardware and software elements powering ADA systems, including various types of sensors (radar, camera, LiDAR, ultrasonic), Electronic Control Units (ECUs), processors, and the underlying software and algorithms. The level of autonomy segmentation categorizes systems from basic driver assistance (Level 1) to more advanced partial and conditional automation (Level 2, Level 2+, Level 3), reflecting the progressive evolution of autonomous driving capabilities. Vehicle type segmentation differentiates demand between Passenger Vehicles (PVs) and Commercial Vehicles (CVs), including the growing influence of Electric Vehicles (EVs).

Application segmentation, the most detailed, covers a wide array of specific ADA functions such as Adaptive Cruise Control (ACC), Automatic Emergency Braking (AEB), Lane Keeping Assist (LKA), Blind Spot Detection (BSD), and Parking Assist Systems (PAS, among others. Each application addresses specific safety or convenience needs, with varying levels of market maturity and adoption rates. Furthermore, the market is analyzed by sales channel, distinguishing between OEM installations and aftermarket solutions, providing insights into the distribution and integration strategies within the automotive ecosystem.

- By Component: Radar Sensors, Camera Sensors, LiDAR Sensors, Ultrasonic Sensors, Electronic Control Units (ECUs), Processors, Software & Algorithms, Others.

- By Level of Autonomy: Level 1 (Driver Assistance), Level 2 (Partial Automation), Level 2+ (Advanced Partial Automation), Level 3 (Conditional Automation).

- By Vehicle Type: Passenger Vehicles (PVs), Commercial Vehicles (CVs), Electric Vehicles (EVs).

- By Application: Adaptive Cruise Control (ACC), Automatic Emergency Braking (AEB), Lane Keeping Assist (LKA), Blind Spot Detection (BSD), Parking Assist Systems (PAS), Traffic Jam Assist (TJA), Forward Collision Warning (FCW), Driver Monitoring Systems (DMS), Road Sign Recognition (RSR), Night Vision System (NVS), Adaptive Front Lighting System (AFS), Tire Pressure Monitoring System (TPMS), Other Applications.

- By Sales Channel: OEM, Aftermarket.

Regional Highlights

- North America: This region is a leading market for Automotive ADA due to stringent safety regulations, a high rate of technological adoption, and the presence of major automotive OEMs and technology companies. The U.S. and Canada are early adopters of advanced safety features, driven by consumer demand for premium vehicles and robust regulatory frameworks promoting accident reduction.

- Europe: Europe exhibits strong growth, fueled by Euro NCAP safety ratings, which incentivize the integration of advanced ADA features in new vehicles. Countries like Germany, France, and the UK are at the forefront of ADA innovation and deployment, with a strong emphasis on urban driving assistance and pedestrian safety systems.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market, primarily due to the rapid expansion of the automotive industry in China, Japan, and South Korea. Increasing disposable incomes, growing safety awareness, and supportive government initiatives promoting smart cities and autonomous driving technologies are significant drivers. India and Southeast Asian countries are emerging as key markets for mass-market ADA adoption.

- Latin America: This region is an emerging market for Automotive ADA, with growth driven by increasing vehicle production and evolving safety standards, particularly in Brazil and Mexico. While starting from a lower base, the market is expected to witness steady growth as basic ADA features become more common.

- Middle East and Africa (MEA): The MEA region is experiencing gradual adoption, influenced by increasing luxury vehicle sales and developing road infrastructure. Countries in the GCC region are investing in smart city initiatives that could accelerate the demand for advanced ADA and autonomous driving technologies in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive ADA Market.- Bosch

- Continental AG

- ZF Friedrichshafen AG

- Denso Corporation

- Aptiv PLC

- Magna International Inc.

- Valeo S.A.

- Veoneer (now part of Qualcomm and Magna)

- Mobileye (an Intel company)

- Nvidia Corporation

- Hella GmbH & Co. KGaA

- Renesas Electronics Corporation

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Panasonic Corporation

- Hyundai Mobis

- BorgWarner Inc.

- Autoliv Inc.

- Volvo Cars

- Tesla Inc.

Frequently Asked Questions

What is the projected growth rate of the Automotive ADA Market?

The Automotive ADA Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.5% between 2025 and 2033, indicating robust expansion driven by safety regulations and technological advancements.

What are the primary factors driving the Automotive ADA Market?

The market is primarily driven by increasing global safety regulations and mandates, growing consumer demand for advanced safety and convenience features, and continuous technological advancements in sensor and AI capabilities.

How is AI impacting Advanced Driver Assistance Systems?

AI significantly enhances ADA by improving sensor fusion for better environmental perception, enabling smarter decision-making, and facilitating self-learning systems. It is crucial for advanced autonomous functions and predictive analytics.

Which regions are key contributors to the Automotive ADA Market?

North America and Europe are major contributors, while Asia Pacific, especially China, Japan, and South Korea, is projected to be the fastest-growing region due to rapid automotive industry expansion and supportive government policies.

What are the key challenges faced by the Automotive ADA Market?

Key challenges include the high cost of integrating ADA systems, ensuring regulatory harmonization across diverse regions, building widespread consumer trust, and addressing cybersecurity risks and data privacy concerns.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted