Automotive Gasket Market

Automotive Gasket Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708531 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

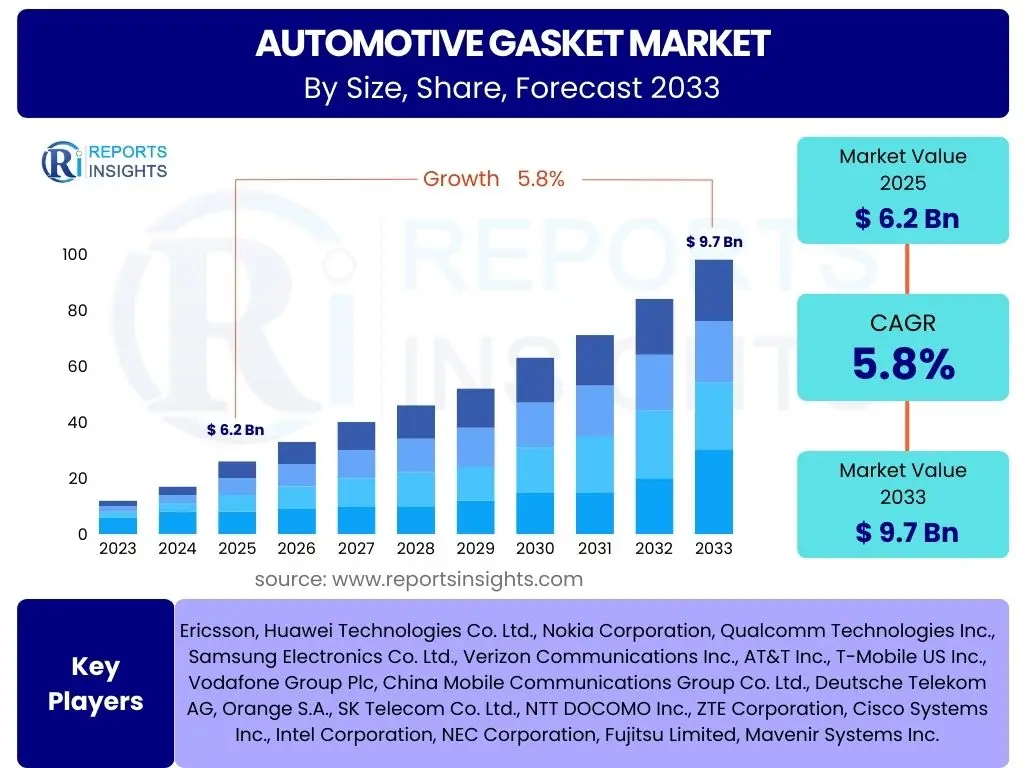

Automotive Gasket Market Size

According to Reports Insights Consulting Pvt Ltd, The Automotive Gasket Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 6.2 Billion in 2025 and is projected to reach USD 9.7 Billion by the end of the forecast period in 2033.

Key Automotive Gasket Market Trends & Insights

The automotive gasket market is currently experiencing significant shifts driven by technological advancements, evolving regulatory landscapes, and the automotive industry's pivot towards electrification. Users frequently inquire about the impact of these macro trends on gasket demand and material innovation. There is a strong interest in understanding how stricter emission standards are pushing manufacturers towards more efficient and durable sealing solutions, as well as the implications of electric vehicle (EV) proliferation on traditional gasket applications and the emergence of new sealing requirements for battery packs and power electronics.

Furthermore, inquiries often highlight the increasing adoption of advanced materials such as fluorosilicone, PTFE, and high-performance elastomers, which offer superior resistance to extreme temperatures, chemicals, and pressure, thereby extending component lifespan and enhancing vehicle reliability. The trend towards lightweighting in vehicles, aimed at improving fuel efficiency and reducing emissions, is also a key area of interest, prompting a demand for thinner, yet equally robust, gasket solutions. Additionally, the integration of smart manufacturing processes and automation in gasket production is a recurring theme, reflecting the industry's drive for efficiency and precision.

- Increasing adoption of advanced, high-performance materials for enhanced durability and thermal resistance.

- Growing demand for sealing solutions in electric vehicle (EV) battery packs and thermal management systems.

- Shift towards lightweight gasket designs to support vehicle fuel efficiency and emission reduction goals.

- Development of multi-layer steel (MLS) gaskets for improved sealing in high-pressure, high-temperature internal combustion engines.

- Integration of smart manufacturing and automation in gasket production to optimize precision and reduce waste.

AI Impact Analysis on Automotive Gasket

Common user questions regarding AI's impact on the automotive gasket sector often revolve around its potential to revolutionize manufacturing processes, enhance product design, and optimize supply chain management. Users are keen to understand how AI-driven predictive analytics can improve quality control by identifying potential defects early in the production cycle, thereby reducing waste and recall rates. The application of machine learning in material science for developing novel gasket materials with tailored properties, such as improved heat resistance or sealing capabilities, is another area of significant interest, promising to accelerate innovation cycles and meet stringent performance demands.

Furthermore, the discussion frequently extends to AI's role in optimizing the entire lifecycle of gaskets, from design to end-of-life. AI algorithms can simulate gasket performance under various operating conditions, allowing for rapid iteration and validation of designs, which reduces prototyping costs and time-to-market. In the realm of supply chain, AI can forecast demand more accurately, manage inventory efficiently, and identify potential disruptions, ensuring a more resilient and responsive supply chain for gasket manufacturers and their automotive clients. These advancements underscore AI's transformative potential in driving efficiency, innovation, and reliability within the automotive gasket market.

- AI-driven predictive maintenance enhancing the lifespan and reliability of gasket-sealed components.

- Machine learning algorithms optimizing gasket material composition for specific performance characteristics.

- Automated visual inspection systems powered by AI improving quality control and defect detection in manufacturing.

- AI in generative design for innovative gasket geometries that improve sealing efficiency and material usage.

- Enhanced supply chain resilience through AI-powered demand forecasting and inventory management for gasket components.

Key Takeaways Automotive Gasket Market Size & Forecast

The automotive gasket market is poised for steady expansion through 2033, driven by a confluence of factors including increasing global vehicle production, stringent emission regulations, and the rapid evolution of electric vehicle technology. Users frequently seek clarification on the primary growth engines and potential inhibitors. A significant takeaway is that while traditional internal combustion engine (ICE) gasket applications will continue to represent a substantial market share, the most dynamic growth will emanate from the electric vehicle segment, specifically in battery sealing, thermal management, and power electronics applications, necessitating a shift in material and design focus for manufacturers.

Another crucial insight is the intensifying focus on advanced materials and precision engineering to meet the demand for enhanced durability, efficiency, and environmental compliance. The market's resilience is further bolstered by a strong aftermarket segment, which consistently contributes to revenue streams as vehicles age and require maintenance. Geographically, Asia Pacific is expected to maintain its dominance due to high vehicle production volumes and increasing adoption of advanced automotive technologies. Stakeholders should prioritize investment in R&D for next-generation sealing solutions and explore strategic partnerships to capitalize on emerging opportunities in the evolving automotive landscape.

- Sustainable growth projected with a CAGR of 5.8%, driven by both traditional ICE and emerging EV demands.

- Electric vehicles represent a significant growth catalyst, fostering new sealing requirements and material innovations.

- Stringent environmental regulations are compelling a shift towards high-performance, durable, and lightweight gasket solutions.

- Asia Pacific is anticipated to remain the leading region, propelled by robust automotive manufacturing and market growth.

- Technological advancements in material science and manufacturing processes are critical for market competitiveness.

Automotive Gasket Market Drivers Analysis

The automotive gasket market is primarily propelled by several robust factors. A key driver is the consistent increase in global vehicle production, particularly in emerging economies, which directly translates to higher demand for gaskets in both original equipment manufacturing (OEM) and aftermarket segments. Furthermore, stringent government regulations concerning vehicle emissions and fuel efficiency worldwide are compelling automotive manufacturers to adopt advanced sealing solutions that can withstand higher temperatures and pressures, preventing leaks and improving engine performance. This regulatory pressure fosters innovation in gasket materials and designs, promoting the use of more sophisticated and durable products.

The growing adoption of electric vehicles (EVs) also represents a significant albeit evolving driver. While some traditional ICE gasket applications may diminish, EVs introduce new and critical sealing requirements for battery enclosures, thermal management systems, and power electronics, demanding specialized gaskets that offer excellent electrical insulation, thermal dissipation, and environmental sealing. Additionally, the expanding average age of vehicles on the road contributes to a steady demand in the aftermarket for replacement gaskets, ensuring continuous revenue streams for manufacturers. These combined forces create a strong foundation for sustained market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Vehicle Production | +1.5% | Asia Pacific, North America, Europe | Short to Mid-Term |

| Stringent Emission Regulations | +1.2% | Europe, North America, China | Mid to Long-Term |

| Growing Demand for Electric Vehicles (EVs) | +1.0% | Global, particularly China, Europe, USA | Mid to Long-Term |

| Advancements in Material Science | +0.8% | Global | Short to Mid-Term |

| Expanding Automotive Aftermarket | +0.7% | Global | Short to Mid-Term |

Automotive Gasket Market Restraints Analysis

Despite the positive growth trajectory, the automotive gasket market faces several notable restraints. One significant challenge is the volatile pricing of raw materials, such as rubber, silicone, and metals, which can directly impact manufacturing costs and profit margins for gasket producers. Fluctuations in these commodity prices introduce uncertainty and can necessitate frequent adjustments to product pricing, potentially affecting market competitiveness. Additionally, the increasing complexity of vehicle designs and the push for miniaturization often require highly specialized and custom-engineered gaskets, which can be more expensive to produce and may have longer lead times, thereby limiting their broad adoption.

Another major restraint is the ongoing technological shift towards electric vehicles. While EVs create new opportunities, they simultaneously reduce the demand for certain traditional ICE gaskets, such as cylinder head gaskets or exhaust manifold gaskets. This transition requires significant investment in research and development for gasket manufacturers to pivot their product portfolios and adapt to new sealing requirements, posing a challenge for companies heavily reliant on conventional applications. Furthermore, intense competition among numerous market players, including both large multinational corporations and smaller regional manufacturers, often leads to price wars and downward pressure on margins, restraining overall market value growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.9% | Global | Short to Mid-Term |

| Intense Market Competition | -0.7% | Global | Short to Mid-Term |

| Shift from ICE to EV reducing traditional gasket demand | -0.8% | Global (developed regions primarily) | Mid to Long-Term |

| High Research & Development Costs | -0.5% | Global | Short to Mid-Term |

| Supply Chain Disruptions | -0.6% | Global | Short Term |

Automotive Gasket Market Opportunities Analysis

The automotive gasket market presents numerous opportunities for growth and innovation. A prime opportunity lies in the expanding electric vehicle (EV) segment, which necessitates specialized sealing solutions for battery packs, electric motors, and advanced thermal management systems. Gaskets designed for these applications must offer superior electrical insulation, thermal conductivity or insulation, and robust sealing against fluids and contaminants, driving demand for advanced materials like high-performance silicones and fluoropolymers. Manufacturers focusing on these niche EV requirements can capture significant market share and differentiate their offerings.

Another significant avenue for growth is the continuous innovation in lightweight and eco-friendly gasket materials. With the automotive industry's relentless pursuit of reduced vehicle weight for improved fuel efficiency and lower emissions, there is a strong demand for gaskets made from composite materials, advanced polymers, or ultra-thin metal designs that offer comparable performance to traditional heavier alternatives. Furthermore, the increasing sophistication of vehicle electronics and autonomous driving systems creates opportunities for gaskets that protect sensitive components from environmental factors, vibration, and electromagnetic interference, leading to the development of integrated sealing solutions with enhanced functionalities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Electric Vehicle (EV) Sealing Applications | +1.3% | China, Europe, North America | Mid to Long-Term |

| Development of Lightweight & Eco-friendly Gasket Materials | +1.0% | Global | Short to Mid-Term |

| Aftermarket Demand for High-Performance Replacement Gaskets | +0.8% | Global | Short to Mid-Term |

| Increasing Use in Hybrid and Hydrogen Fuel Cell Vehicles | +0.7% | Europe, Japan, South Korea | Mid to Long-Term |

| Integration of Smart Gaskets with Sensing Capabilities | +0.5% | Global (R&D focus) | Long-Term |

Automotive Gasket Market Challenges Impact Analysis

The automotive gasket market encounters several formidable challenges that can impede its growth and stability. One primary challenge is the rapid pace of technological advancements in the automotive industry, which necessitates constant innovation and adaptation from gasket manufacturers. For instance, the evolving designs of internal combustion engines to meet stricter emission norms, coupled with the entirely new architecture of electric vehicles, demand continuous research and development into new materials and sealing technologies. This requires substantial investment and expertise, posing a significant hurdle for smaller or less resource-intensive companies trying to keep pace.

Another critical challenge involves maintaining supply chain resilience amidst increasing global complexities and geopolitical tensions. Disruptions, such as those caused by the recent pandemic or regional conflicts, can lead to raw material shortages, production delays, and increased logistics costs, directly impacting the availability and pricing of gaskets. Furthermore, the global trend towards vehicle lightweighting, while an opportunity, also presents a challenge by demanding thinner yet equally durable gaskets, pushing the boundaries of material science and manufacturing precision. Companies must navigate these intricate issues to sustain competitive advantage and ensure consistent product delivery.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Shifts in Automotive Industry | -0.8% | Global | Mid to Long-Term |

| Supply Chain Volatility and Geopolitical Risks | -0.7% | Global | Short to Mid-Term |

| Pressure for Cost Reduction from OEMs | -0.6% | Global | Short to Mid-Term |

| Complex Manufacturing Processes for Advanced Gaskets | -0.5% | Global | Mid-Term |

| Talent Shortage in Material Science and Engineering | -0.4% | Developed Regions | Long-Term |

Automotive Gasket Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global automotive gasket market, covering historical data from 2019 to 2023, current market estimations for 2024, and detailed forecasts up to 2033. It examines market size, growth drivers, restraints, opportunities, and challenges across various segments and key regions. The scope encompasses detailed segmentation by material type, application, vehicle type, and sales channel, offering critical insights into market dynamics and competitive landscape to support strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.2 Billion |

| Market Forecast in 2033 | USD 9.7 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Freudenberg Sealing Technologies, Dana Incorporated, ElringKlinger AG, Federal-Mogul LLC (Tenneco Inc.), NOK Corporation, Trelleborg AB, James Gaskets, The Garlock Family of Companies (Enpro Industries), Flexitallic Group, Flowserve Corporation, NICHIAS Corporation, Interface Performance Materials Inc., Victor Reinz (Dana Incorporated), Technetics Group (Enpro Industries), KLINGER Group, IGP, Cooper Standard, Parker Hannifin, SKF Group, Datwyler Holding AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The automotive gasket market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to the overall market. This segmentation is crucial for identifying key growth areas, understanding competitive landscapes, and formulating targeted business strategies. The analysis spans across material types, offering insights into the dominance of non-metallic gaskets like rubber and silicone, as well as the specialized roles of metallic and semi-metallic solutions, such as Multi-Layer Steel (MLS) gaskets, vital for high-performance applications in modern engines and exhaust systems.

Furthermore, segmenting by application elucidates the critical demand for gaskets in various automotive systems, from traditional engine components to emerging requirements in electric vehicle battery and motor sealing. Vehicle type segmentation differentiates demand patterns between passenger cars, commercial vehicles, and the rapidly expanding electric vehicle category, highlighting distinct technological needs and market trajectories. The breakdown by sales channel into OEM and aftermarket provides clarity on distribution strategies and revenue generation across new vehicle assembly and ongoing vehicle maintenance, revealing the balanced dynamics of the market.

- By Material: Non-Metallic (Rubber, Silicone, Cork, Graphite, Fiber, PTFE, Others), Metallic (Copper, Steel, Aluminum, Others), Semi-Metallic (Multi-Layer Steel (MLS), Spiral Wound, Others).

- By Application: Engine Gaskets (Cylinder Head Gasket, Exhaust Gasket, Intake Manifold Gasket, Oil Pan Gasket, Timing Cover Gasket, Valve Cover Gasket, Water Pump Gasket), Transmission Gaskets, Exhaust System Gaskets, HVAC Gaskets, Brake System Gaskets, Fuel System Gaskets, Battery & Electric Motor Gaskets (for EVs), Other Applications.

- By Vehicle Type: Passenger Cars, Commercial Vehicles (Light Commercial Vehicles, Heavy Commercial Vehicles), Electric Vehicles (BEV, PHEV, FCEV).

- By Sales Channel: OEM (Original Equipment Manufacturer), Aftermarket.

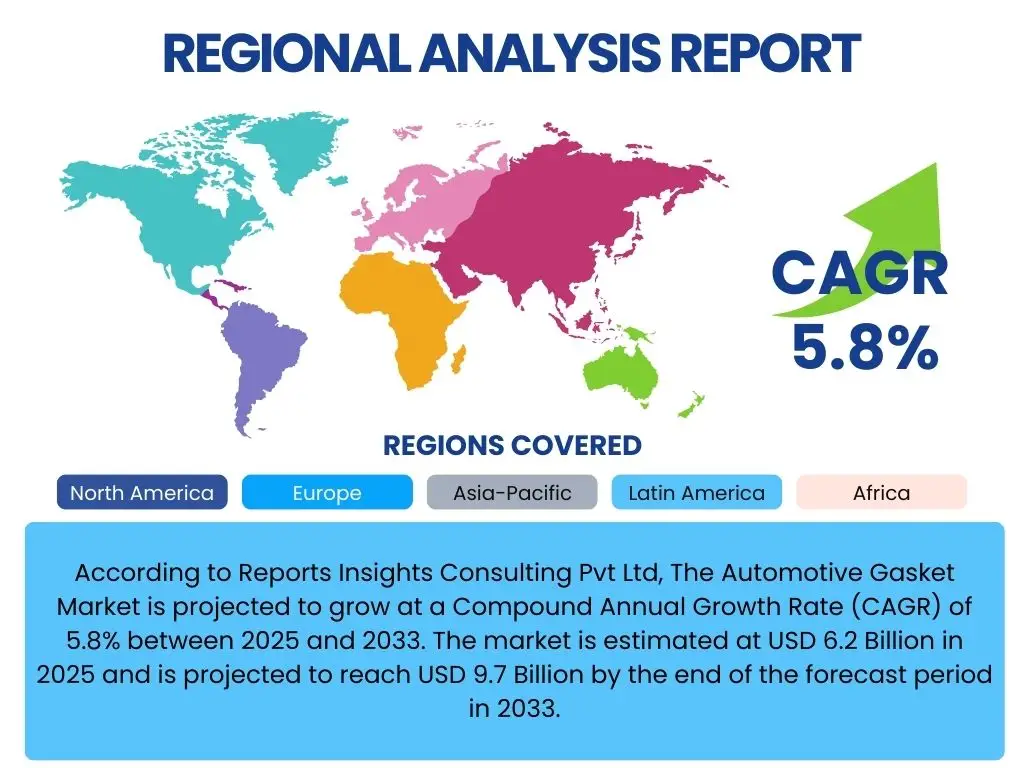

Regional Highlights

Regionally, the automotive gasket market exhibits varied dynamics influenced by local manufacturing hubs, regulatory environments, and consumer preferences. Asia Pacific (APAC) stands out as the dominant region, primarily driven by the colossal automotive production bases in China, India, Japan, and South Korea. These countries not only produce a vast number of vehicles but are also rapidly adopting advanced automotive technologies, including electric vehicles, which fuels demand for both traditional and new-age gasket solutions. The region's economic growth and increasing disposable incomes further contribute to robust vehicle sales and a flourishing aftermarket.

North America and Europe represent mature markets characterized by stringent emission standards and a strong emphasis on high-performance and durable automotive components. These regions are at the forefront of electric vehicle adoption and technological innovation, creating a significant demand for specialized gaskets in battery, fuel cell, and advanced engine applications. Latin America and the Middle East & Africa (MEA) are emerging markets, showing consistent growth influenced by expanding automotive industries, urbanization, and increasing infrastructure development, presenting long-term opportunities for market players focusing on localized production and distribution strategies.

- Asia Pacific: Largest market share driven by high vehicle production in China, India, Japan, and South Korea, coupled with rising EV adoption and economic growth.

- Europe: Strong demand for high-performance and emission-compliant gaskets due to stringent environmental regulations and significant investment in EV technology.

- North America: Mature market with steady demand from a robust automotive industry, increasing adoption of advanced materials, and a growing aftermarket.

- Latin America: Emerging market with growth potential spurred by increasing vehicle manufacturing and a developing automotive ecosystem.

- Middle East & Africa (MEA): Gradually growing market with opportunities arising from expanding vehicle fleets and infrastructure projects.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Automotive Gasket Market.- Freudenberg Sealing Technologies

- Dana Incorporated

- ElringKlinger AG

- Federal-Mogul LLC (Tenneco Inc.)

- NOK Corporation

- Trelleborg AB

- James Gaskets

- The Garlock Family of Companies (Enpro Industries)

- Flexitallic Group

- Flowserve Corporation

- NICHIAS Corporation

- Interface Performance Materials Inc.

- Victor Reinz (Dana Incorporated)

- Technetics Group (Enpro Industries)

- KLINGER Group

- IGP

- Cooper Standard

- Parker Hannifin

- SKF Group

- Datwyler Holding AG

Frequently Asked Questions

What is the projected growth rate of the Automotive Gasket Market?

The Automotive Gasket Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033.

How is the rise of Electric Vehicles (EVs) impacting the automotive gasket market?

The rise of EVs creates new demand for specialized gaskets in battery sealing, thermal management, and power electronics, while potentially reducing demand for some traditional internal combustion engine (ICE) gaskets. Manufacturers are adapting with advanced material and design innovations.

Which region is expected to dominate the Automotive Gasket Market?

Asia Pacific (APAC) is expected to maintain its dominance in the Automotive Gasket Market, driven by high vehicle production volumes and increasing adoption of advanced automotive technologies.

What are the key materials used in automotive gaskets?

Key materials include non-metallic types like rubber, silicone, cork, graphite, and PTFE; metallic types such as copper, steel, and aluminum; and semi-metallic options like Multi-Layer Steel (MLS).

What are the main drivers for the growth of the automotive gasket market?

Key drivers include increasing global vehicle production, stringent emission regulations, the growing demand for electric vehicles (EVs) requiring specialized seals, and advancements in material science for high-performance solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted