ATM Market

ATM Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709332 | Last Updated : December 08, 2025 |

Format : ![]()

![]()

![]()

![]()

ATM Market Size

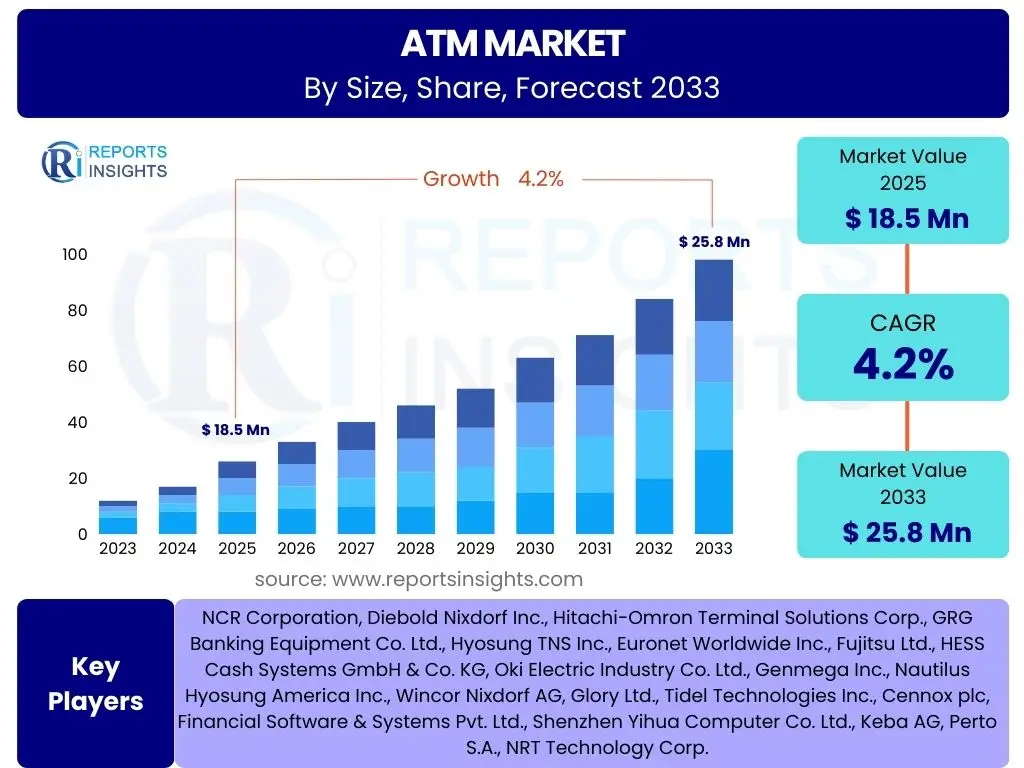

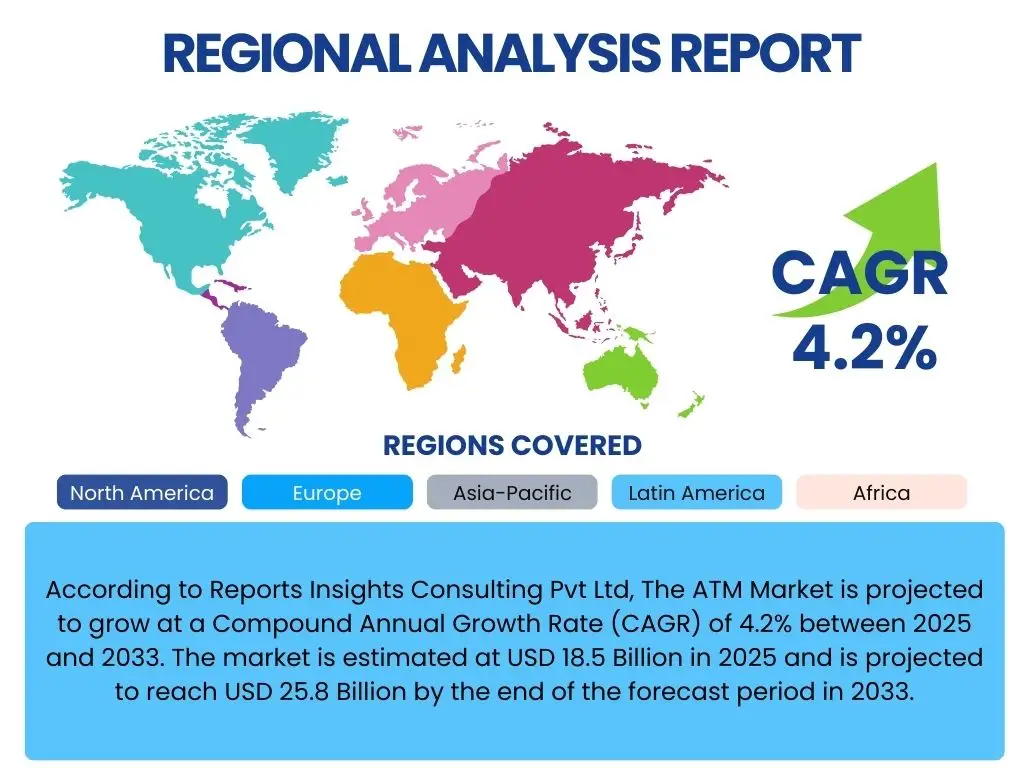

According to Reports Insights Consulting Pvt Ltd, The ATM Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.2% between 2025 and 2033. The market is estimated at USD 18.5 Billion in 2025 and is projected to reach USD 25.8 Billion by the end of the forecast period in 2033.

Key ATM Market Trends & Insights

The ATM market is undergoing a significant transformation, driven by evolving consumer expectations and technological advancements. User inquiries frequently highlight a shift from basic cash dispensing to more sophisticated, integrated self-service terminals. There is strong interest in the adoption of features such as contactless transactions, advanced security protocols, and personalization capabilities, signaling a move towards smart, digitally-enabled ATMs that complement rather than compete with online banking channels.

Furthermore, discussions often revolve around the economic viability of ATMs in an increasingly cashless society and the strategies employed by financial institutions to maintain their relevance. Insights reveal a dual approach: optimizing the existing footprint in cash-reliant regions and transforming ATMs into multifunctional service points in developed markets. This includes providing value-added services beyond cash, enhancing the customer experience, and integrating seamlessly with digital banking ecosystems, which are critical for future growth and market penetration.

- Contactless ATM functionality (NFC, QR codes) for enhanced user convenience and hygiene.

- Biometric authentication (fingerprint, facial recognition) for heightened security and card-less transactions.

- Cash recycling machines gaining traction for operational efficiency and reduced cash-in-transit costs.

- Integration with mobile banking applications for pre-staging transactions and personalized offers.

- Branch transformation strategies leveraging intelligent ATMs as self-service hubs.

- Increased deployment of white-label ATMs in non-bank locations for broader accessibility.

- Focus on predictive maintenance and remote monitoring using IoT for improved uptime and cost savings.

AI Impact Analysis on ATM

Common user questions regarding AI's impact on ATMs center on how artificial intelligence will enhance security, improve efficiency, and personalize customer interactions. There is a clear expectation that AI will move beyond basic operational improvements to deliver more intelligent, predictive, and secure self-service experiences. Users are keen to understand how AI can combat fraud, streamline maintenance, and offer tailored financial advice or services directly at the ATM terminal, making the device a more intelligent financial touchpoint.

The analysis reveals that AI is poised to revolutionize several aspects of ATM operations, from backend management to front-end customer engagement. Concerns also arise about data privacy and the ethical implications of AI deployment, indicating a need for transparent and secure AI frameworks. However, the overarching sentiment points towards AI as a critical enabler for the next generation of ATMs, transforming them into proactive, smart financial assistants capable of adapting to individual user needs and anticipating operational issues before they occur.

- Enhanced fraud detection through real-time anomaly analysis and behavioral biometrics.

- Predictive maintenance capabilities, allowing ATMs to self-diagnose and alert for service needs, minimizing downtime.

- Personalized user experiences, offering tailored services, marketing messages, and financial advice based on user history.

- Improved security through AI-powered surveillance and identification of suspicious activity around the ATM.

- Optimized cash management and forecasting, reducing operational costs and ensuring cash availability.

- Natural Language Processing (NLP) integration for voice-guided transactions and customer support at the ATM.

- Automated dispute resolution and inquiry handling, improving customer service efficiency.

Key Takeaways ATM Market Size & Forecast

User inquiries about the ATM market size and forecast consistently seek clarity on the overall trajectory and resilience of this sector amidst the rise of digital payments. A primary concern is whether the ATM market is in decline or undergoing a strategic transformation. The overarching insight is that while cash usage dynamics are shifting in some regions, the ATM market is not contracting globally; instead, it is evolving to meet new demands for convenience, security, and diversified self-service options, thereby maintaining a positive growth outlook.

Furthermore, discussions frequently touch upon the factors underpinning the forecast growth, specifically the role of emerging economies and technological innovations. The key takeaway emphasizes that financial inclusion initiatives in developing markets, coupled with the upgrade and modernization of ATM infrastructure in mature economies, are crucial growth drivers. The market's stability and projected growth underscore its continued relevance as a critical component of the financial ecosystem, adapting to serve both traditional cash needs and emerging digital integration requirements.

- The ATM market is experiencing steady, albeit moderate, growth, primarily driven by modernization efforts and expansion in developing regions.

- Technological innovation, particularly in biometrics, contactless features, and AI, is crucial for market sustainability and growth.

- Financial inclusion initiatives in emerging markets represent a significant driver for new ATM deployments.

- Despite the rise of digital payments, cash continues to play a vital role globally, sustaining demand for ATM services.

- Strategic repositioning of ATMs as multi-functional self-service terminals is key to their long-term relevance and market expansion.

ATM Market Drivers Analysis

The ATM market continues to be propelled by several robust drivers that underscore its enduring importance in the global financial landscape. A primary driver is the persistent demand for cash, especially in developing economies where digital payment infrastructure is still nascent or unevenly distributed. For vast populations, ATMs remain the most accessible and reliable channel for immediate cash withdrawals, which is essential for daily transactions and economic participation.

Furthermore, advancements in ATM technology, such as the introduction of smart ATMs, cash recycling machines, and advanced security features, are transforming the user experience and operational efficiency, thereby fueling adoption. Financial institutions are also increasingly leveraging ATMs for branch transformation strategies, deploying them as self-service hubs to offer a wider array of services beyond cash transactions, including bill payments, account inquiries, and even loan applications. This expansion of functionalities enhances convenience and reduces the operational burden on traditional branch staff.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Demand for Cash in Developing Economies | +1.1% | Asia Pacific, Latin America, MEA | Short to Mid-term (2025-2029) |

| Financial Inclusion Initiatives | +0.9% | Asia Pacific, Africa, South America | Mid to Long-term (2027-2033) |

| Technological Advancements (Smart ATMs, Biometrics, Contactless) | +0.8% | North America, Europe, Asia Pacific | Short to Long-term (2025-2033) |

| Expansion of White-Label ATMs | +0.7% | Global, particularly emerging markets | Mid-term (2026-2031) |

| Branch Transformation and Self-Service Strategy | +0.6% | North America, Europe, parts of Asia Pacific | Short to Mid-term (2025-2030) |

ATM Market Restraints Analysis

Despite the prevailing drivers, the ATM market faces several significant restraints that could temper its growth trajectory. The most prominent restraint is the accelerating global shift towards digital and cashless payment methods, particularly in developed economies. As mobile payments, online banking, and contactless cards become more ubiquitous, the frequency of cash transactions decreases, potentially reducing the necessity for traditional ATM services.

Another key restraint involves the high operational and maintenance costs associated with ATM networks. These costs include physical security, cash replenishment, software updates, and regulatory compliance, which can be substantial for financial institutions. Furthermore, the increasing sophistication of cyber threats and physical attacks on ATMs necessitates continuous investment in security measures, adding to the overall cost burden and potentially deterring expansion in certain high-risk areas. Regulatory complexities and compliance requirements across different regions also pose a challenge, increasing the administrative overhead for ATM operators.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Adoption of Digital Payment Methods | -1.2% | North America, Europe, parts of Asia Pacific | Short to Long-term (2025-2033) |

| High Operational and Maintenance Costs | -0.9% | Global | Short to Long-term (2025-2033) |

| Increasing Cybersecurity Threats and Physical Attacks | -0.8% | Global | Short to Long-term (2025-2033) |

| Declining Cash Usage in Developed Economies | -0.7% | North America, Western Europe | Mid to Long-term (2027-2033) |

| Regulatory Complexities and Compliance Burden | -0.5% | Global, especially highly regulated markets | Short to Mid-term (2025-2029) |

ATM Market Opportunities Analysis

Despite the challenges, significant opportunities exist within the ATM market, particularly in leveraging advanced technologies and expanding service offerings. One major opportunity lies in the deployment of next-generation ATMs that integrate features like video tellers, cryptocurrency access, and advanced biometric security. These intelligent terminals can serve as mini-branches, offering a comprehensive suite of financial services and addressing a wider range of customer needs, thereby attracting new users and retaining existing ones.

Furthermore, the growth of white-label ATMs and ATM-as-a-Service models presents a substantial opportunity for non-bank entities and smaller financial institutions to expand their reach without significant capital expenditure. These models can enhance accessibility in underserved areas and provide tailored services. The ongoing need for financial inclusion in developing markets also offers a fertile ground for expansion, as ATMs continue to be a primary gateway to financial services for unbanked and underbanked populations, driving new deployments and modernization initiatives.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Deployment of Next-Generation & Smart ATMs | +1.3% | Global, particularly North America, Europe, Asia Pacific | Short to Long-term (2025-2033) |

| Expansion of White-Label ATMs and ATM-as-a-Service | +1.1% | Emerging markets, rural areas globally | Mid to Long-term (2027-2033) |

| Integration with Digital Banking & Mobile Platforms | +0.9% | Global | Short to Mid-term (2025-2030) |

| Offering Value-Added Services (e.g., Bill Pay, Cryptocurrency) | +0.8% | Global, especially tech-savvy regions | Mid-term (2026-2031) |

| Market Penetration in Underserved Rural & Remote Areas | +0.7% | Asia Pacific, Africa, Latin America | Mid to Long-term (2027-2033) |

ATM Market Challenges Impact Analysis

The ATM market is confronted with a range of operational and strategic challenges that demand innovative solutions for sustained growth. A significant challenge stems from the rapidly evolving consumer preferences, with an increasing shift towards digital channels and a decreased reliance on physical cash for transactions. This requires ATM operators to continuously adapt their services and technologies to remain relevant and appealing to a tech-savvy demographic that expects seamless, integrated financial experiences.

Another substantial challenge is the intense competitive landscape, not only from other ATM manufacturers and service providers but also from a burgeoning fintech sector offering alternative, often more convenient, digital payment and banking solutions. This competition necessitates ongoing innovation and differentiation. Furthermore, ensuring robust cybersecurity measures against sophisticated attacks, maintaining data privacy, and navigating complex regulatory environments across diverse geographies add layers of complexity and cost to ATM operations, impacting profitability and hindering rapid deployment strategies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Evolving Consumer Preferences and Digital Adoption | -1.0% | Global, particularly developed markets | Short to Long-term (2025-2033) |

| Intensified Competition from Fintech and Digital Payment Providers | -0.9% | Global | Short to Long-term (2025-2033) |

| Maintaining Cybersecurity and Data Privacy Standards | -0.8% | Global | Short to Long-term (2025-2033) |

| High Initial Investment and Upgrade Costs for Modern ATMs | -0.7% | Global | Short to Mid-term (2025-2030) |

| Navigating Diverse and Complex Regulatory Frameworks | -0.6% | Global, especially multi-national operators | Short to Mid-term (2025-2029) |

ATM Market - Updated Report Scope

This comprehensive market report delves into the intricate dynamics of the ATM market, providing an exhaustive analysis of its current state and future growth trajectories. The scope encompasses detailed segmentation by type, deployment, solution, technology, and application, alongside a thorough examination of regional market performance and competitive landscape. The report aims to offer strategic insights into the driving forces, inherent restraints, emerging opportunities, and critical challenges shaping the market from 2025 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 18.5 Billion |

| Market Forecast in 2033 | USD 25.8 Billion |

| Growth Rate | 4.2% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | NCR Corporation, Diebold Nixdorf Inc., Hitachi-Omron Terminal Solutions Corp., GRG Banking Equipment Co. Ltd., Hyosung TNS Inc., Euronet Worldwide Inc., Fujitsu Ltd., HESS Cash Systems GmbH & Co. KG, Oki Electric Industry Co. Ltd., Genmega Inc., Nautilus Hyosung America Inc., Wincor Nixdorf AG, Glory Ltd., Tidel Technologies Inc., Cennox plc, Financial Software & Systems Pvt. Ltd., Shenzhen Yihua Computer Co. Ltd., Keba AG, Perto S.A., NRT Technology Corp. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The ATM market is extensively segmented to provide a granular view of its diverse components and their respective contributions to overall market growth. These segments highlight distinct areas of innovation, deployment strategies, and service offerings that cater to a wide array of consumer and institutional needs. Understanding these segmentations is critical for stakeholders to identify niche markets, optimize product development, and tailor their go-to-market strategies effectively across different regions and customer demographics.

The detailed breakdown allows for a comprehensive assessment of how various types of ATMs, deployment locations, technological integrations, and application functionalities influence market share and growth prospects. For instance, the distinction between conventional and smart ATMs underscores the ongoing shift towards advanced, multi-functional terminals, while the varied deployment options reflect strategies to maximize accessibility. Similarly, the segmentation by solution and application illustrates the breadth of services offered and the underlying technological infrastructure supporting these capabilities.

- By Type: Includes Conventional/Traditional ATM, Smart ATM, Cash Recycler ATM, White Label ATM, Brown Label ATM, Green Label ATM, Pink Label ATM, Yellow Label ATM.

- By Deployment: Encompasses On-site ATM, Off-site ATM, Worksite ATM, and Mobile ATM.

- By Solution: Covers Managed Services, ATM Software, ATM Hardware, and ATM Security.

- By Technology: Features Biometric ATM, Contactless ATM, Card-less ATM, and Voice-Guided ATM.

- By Application: Addresses Cash Withdrawals, Cash Deposits, Balance Inquiry, Fund Transfers, Bill Payments, Mini Statements, Mobile Top-ups, and Card-less Transactions.

Regional Highlights

- North America: A mature market characterized by the modernization of existing ATM infrastructure, significant adoption of advanced technologies like contactless and biometric features, and a strategic shift towards branch transformation where ATMs act as self-service hubs. Despite declining cash usage, the demand for sophisticated, multi-functional ATMs persists.

- Europe: Demonstrates a diverse landscape with varying rates of cashless adoption. Western European countries focus on advanced security, cash recycling, and integration with digital banking, while Eastern European nations still see steady demand for cash access, driving new deployments and upgrades.

- Asia Pacific (APAC): The fastest-growing region, driven by robust economic development, rapid urbanization, and extensive financial inclusion initiatives. Countries like India, China, and Southeast Asian nations are witnessing substantial new ATM installations, particularly in rural and semi-urban areas, alongside the adoption of smart and white-label ATMs.

- Latin America: Characterized by a significant unbanked population and a strong reliance on cash. This region presents substantial opportunities for new ATM deployments, especially white-label models, and a growing emphasis on enhancing security features to combat fraud.

- Middle East and Africa (MEA): A region experiencing steady growth in ATM infrastructure, spurred by government efforts to promote financial inclusion and the expansion of banking services. Investment in secure, robust ATM solutions is a priority, particularly in areas with limited traditional banking access.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the ATM Market.- NCR Corporation

- Diebold Nixdorf Inc.

- Hitachi-Omron Terminal Solutions Corp.

- GRG Banking Equipment Co. Ltd.

- Hyosung TNS Inc.

- Euronet Worldwide Inc.

- Fujitsu Ltd.

- HESS Cash Systems GmbH & Co. KG

- Oki Electric Industry Co. Ltd.

- Genmega Inc.

- Nautilus Hyosung America Inc.

- Wincor Nixdorf AG

- Glory Ltd.

- Tidel Technologies Inc.

- Cennox plc

- Financial Software & Systems Pvt. Ltd.

- Shenzhen Yihua Computer Co. Ltd.

- Keba AG

- Perto S.A.

- NRT Technology Corp.

Frequently Asked Questions

What is the current estimated size of the ATM market?

The ATM market is estimated at USD 18.5 Billion in 2025, reflecting its continued relevance and strategic evolution in the global financial ecosystem.

How fast is the ATM market projected to grow?

The ATM market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.2% between 2025 and 2033, driven by modernization and expansion in emerging economies.

What are the key technological trends shaping the ATM market?

Key technological trends include the integration of contactless and card-less transaction capabilities, advanced biometric authentication, AI-driven predictive maintenance, and the adoption of cash recycling solutions for improved efficiency and security.

How does AI impact the future of ATMs?

AI significantly impacts ATMs by enhancing fraud detection, enabling predictive maintenance, personalizing user experiences, and improving security through intelligent surveillance, transforming ATMs into smarter, more efficient financial touchpoints.

Which regions are driving the growth of the ATM market?

The Asia Pacific region is a primary driver of ATM market growth due to financial inclusion initiatives and rapid urbanization, while North America and Europe focus on modernizing existing infrastructure with advanced features.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted