Anti Corrosive Pigment Market

Anti Corrosive Pigment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702966 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

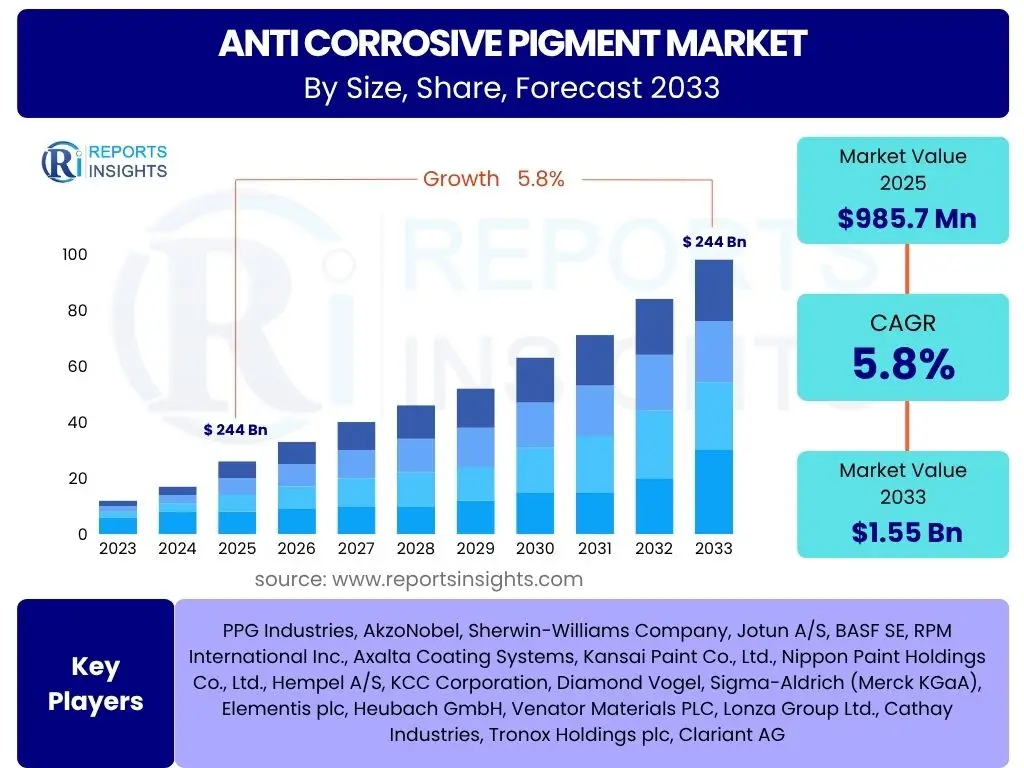

Anti Corrosive Pigment Market Size

According to Reports Insights Consulting Pvt Ltd, The Anti Corrosive Pigment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 985.7 Million in 2025 and is projected to reach USD 1.55 Billion by the end of the forecast period in 2033.

Key Anti Corrosive Pigment Market Trends & Insights

The Anti Corrosive Pigment market is undergoing a significant transformation driven by a confluence of evolving environmental regulations, advancements in material science, and increasing demand for sustainable and high-performance solutions. Key user inquiries often revolve around the shift from traditional, toxic pigments like chromates to eco-friendly alternatives, the integration of smart technologies in coatings, and the impact of nanotechnology on corrosion protection efficacy. These trends reflect a broader industry push towards innovation that balances superior protective capabilities with environmental responsibility and operational efficiency.

Moreover, end-use industries such as automotive, marine, and construction are continuously seeking more durable and long-lasting anti-corrosion solutions to reduce maintenance costs and extend asset lifespans. This demand is fostering research and development into novel pigment formulations that offer enhanced barrier properties, active inhibition mechanisms, and self-healing functionalities. The emphasis is also on multi-functional pigments that can provide additional benefits beyond corrosion protection, such as UV resistance, anti-fouling properties, or aesthetic appeal, thereby offering comprehensive solutions for diverse applications.

- Transition towards eco-friendly and non-toxic pigment formulations, driven by stringent environmental regulations.

- Increased adoption of smart coatings incorporating anti-corrosive pigments with self-healing capabilities.

- Growing integration of nanotechnology to enhance barrier properties and extend coating lifespan.

- Emphasis on multi-functional pigments offering combined corrosion protection with other performance attributes.

- Rising demand for high-performance solutions in harsh operating environments across industries.

AI Impact Analysis on Anti Corrosive Pigment

Common user questions regarding AI's impact on the Anti Corrosive Pigment market frequently address its role in accelerating material discovery, optimizing formulation processes, and improving predictive maintenance strategies for coated assets. Users are keen to understand how artificial intelligence and machine learning algorithms can reduce the time and cost associated with developing new pigment chemistries and how these technologies can lead to more effective and durable corrosion protection solutions. The interest extends to AI's potential in analyzing vast datasets of material properties and performance under various conditions, enabling a more informed and data-driven approach to product development.

Furthermore, AI is poised to revolutionize quality control and supply chain management within the anti-corrosive pigment industry. Predictive analytics, powered by AI, can forecast potential raw material shortages, optimize inventory levels, and enhance production efficiency, thereby streamlining operations and reducing costs. In application, AI can assist in monitoring the integrity of coatings in real-time, predicting failure points, and scheduling maintenance proactively, significantly extending the lifespan of infrastructure and industrial assets. This integration of AI offers substantial opportunities for innovation and operational excellence across the entire value chain of anti-corrosive pigments.

- Accelerated discovery and development of novel anti-corrosive pigment chemistries through AI-driven material informatics.

- Optimization of pigment formulations for enhanced performance and cost-efficiency using machine learning algorithms.

- Improved predictive maintenance and lifespan estimation of coated assets via AI-powered data analytics.

- Enhanced quality control and real-time monitoring of pigment production processes.

- Optimization of supply chain logistics and inventory management for raw materials and finished products.

Key Takeaways Anti Corrosive Pigment Market Size & Forecast

Key user inquiries regarding the Anti Corrosive Pigment market size and forecast consistently highlight the market's robust growth trajectory and the underlying factors contributing to this expansion. Stakeholders are particularly interested in understanding which regions will experience the most significant growth, the primary drivers of this market expansion, and the impact of technological advancements on future market dynamics. The insights reveal a market driven by global infrastructure development, increasing industrialization, and a pervasive need for asset protection across diverse sectors, underscoring the criticality of corrosion prevention in maintaining economic stability and operational integrity.

The forecast indicates a sustained shift towards high-performance and environmentally compliant pigments, reflecting evolving regulatory landscapes and increasing corporate responsibility initiatives. Furthermore, the market's resilience is demonstrated by its continuous innovation, with research focusing on creating more efficient, durable, and sustainable solutions that address both existing and emerging challenges. The consistent demand for effective corrosion control, coupled with technological progress and a growing emphasis on green chemistry, positions the anti-corrosive pigment market for significant expansion over the next decade.

- The market exhibits a stable and significant growth rate, driven by industrial and infrastructure expansion globally.

- Strong emphasis on sustainable and eco-friendly pigment solutions is shaping future market direction.

- Asia Pacific is anticipated to be a major growth hub due to rapid industrialization and construction activities.

- Technological advancements, including smart coatings and nanotechnology, are key to enhancing product performance.

- Increasing lifespan requirements for assets across various industries are fueling demand for advanced anti-corrosive solutions.

Anti Corrosive Pigment Market Drivers Analysis

The global Anti Corrosive Pigment market is significantly propelled by the escalating demand for infrastructure development and maintenance worldwide. Rapid urbanization, industrial expansion, and the continuous need to upgrade existing infrastructure such as bridges, pipelines, and buildings necessitate robust corrosion protection solutions. Governments and private entities are investing heavily in new construction projects and the refurbishment of aging assets, creating a sustained demand for anti-corrosive pigments that ensure durability and extend the lifespan of these structures. This imperative to safeguard large-scale investments against degradation drives innovation and adoption of advanced protective coatings.

Furthermore, stringent regulatory frameworks imposing limits on volatile organic compound (VOC) emissions and the use of hazardous materials are compelling industries to shift towards eco-friendly and non-toxic anti-corrosive pigments. Environmental compliance is no longer just a preference but a mandatory requirement, particularly in developed economies. This regulatory pressure accelerates the research and development of sustainable alternatives, such as zinc-free, chromate-free, and organic-based pigments, fostering a market environment where innovation in green chemistry is rewarded. The drive for sustainability aligns with corporate social responsibility goals and consumer demand for safer products, further stimulating market growth.

The expansion of key end-use industries, including automotive, marine, and industrial coatings, also serves as a crucial market driver. The automotive sector requires advanced anti-corrosion treatments for vehicle bodies and components to enhance their longevity and aesthetic appeal. In the marine industry, constant exposure to saltwater and harsh weather conditions necessitates highly effective anti-corrosion solutions for ships, offshore platforms, and port infrastructure. Similarly, general industrial applications, encompassing machinery, equipment, and pipelines, rely on anti-corrosive pigments to prevent costly damage and downtime, ensuring operational efficiency and safety across various manufacturing and processing plants.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Infrastructure Development & Maintenance | +1.5% | Asia Pacific, North America, Europe | Medium to Long-term (2025-2033) |

| Stringent Environmental Regulations | +1.2% | Europe, North America, East Asia | Medium to Long-term (2025-2033) |

| Increasing Demand from End-Use Industries (Automotive, Marine, Industrial) | +1.3% | Global, particularly APAC and Europe | Medium-term (2025-2029) |

| Technological Advancements in Pigment Formulations | +0.8% | North America, Europe, China | Long-term (2029-2033) |

Anti Corrosive Pigment Market Restraints Analysis

The Anti Corrosive Pigment market faces significant restraints primarily due to the volatility and high costs associated with key raw materials. Pigments often rely on a variety of inorganic compounds, metals, and specialty chemicals whose prices are subject to global supply chain disruptions, geopolitical tensions, and fluctuating commodity markets. This price instability directly impacts manufacturing costs, making it challenging for producers to maintain stable profit margins and competitive pricing for their end products. Such cost pressures can lead to delayed investments in R&D and potentially hinder market expansion, particularly for manufacturers operating on tighter budgets or in price-sensitive regional markets.

Another major restraint is the increasing regulatory scrutiny and public concern regarding the environmental impact and toxicity of certain traditional anti-corrosive pigments. Historically, heavy metal-based pigments like chromates and lead-based compounds were widely used due to their superior performance. However, their known health hazards and environmental persistence have led to bans and severe restrictions in many parts of the world. This necessitates continuous reformulation and investment in new, safer alternatives, which can be costly and time-consuming. The transition away from established, effective chemistries toward novel, less proven, or more expensive green alternatives poses a significant challenge for market players, especially small and medium-sized enterprises.

Furthermore, the availability of alternative corrosion protection methods poses a competitive restraint on the anti-corrosive pigment market. Methods such as cathodic protection, galvanization, organic coatings without pigments, and specialized polymer coatings can sometimes offer competitive advantages in specific applications or cost structures. While anti-corrosive pigments are integral to many coating systems, the existence of these alternatives means that market participants must continuously innovate and demonstrate the superior efficacy, longevity, and cost-effectiveness of pigment-based solutions to maintain market share. This competitive landscape demands ongoing investment in performance enhancement and differentiation to justify the use of pigment-inclusive systems.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.8% | Global, particularly APAC (manufacturing hubs) | Medium-term (2025-2029) |

| Stringent Regulations on Hazardous Chemicals | -0.9% | Europe, North America | Long-term (2025-2033) |

| Competition from Alternative Corrosion Protection Methods | -0.5% | Global | Medium to Long-term (2025-2033) |

Anti Corrosive Pigment Market Opportunities Analysis

Significant opportunities exist in the Anti Corrosive Pigment market through the development and commercialization of eco-friendly and sustainable pigment solutions. As environmental regulations become increasingly stringent and consumer awareness about health and sustainability grows, the demand for non-toxic and low-VOC (volatile organic compound) alternatives is surging. This creates a fertile ground for innovation in areas such as phosphate-based, silicate-based, or organic pigments that offer comparable or superior corrosion protection without the associated environmental hazards of traditional heavy metal-based options. Companies investing in green chemistry and sustainable manufacturing processes can capture a growing market segment and differentiate themselves from competitors, appealing to environmentally conscious industries and end-users.

The burgeoning construction and infrastructure sectors in emerging economies, particularly in Asia Pacific and Latin America, present substantial untapped market opportunities. Countries like India, China, and Brazil are undergoing rapid urbanization and industrialization, leading to massive investments in new buildings, transportation networks, and industrial facilities. These regions often lack extensive existing infrastructure, creating a high demand for durable and cost-effective anti-corrosion solutions from the ground up. Manufacturers can tailor their product offerings to meet the specific needs and regulatory environments of these developing markets, leveraging lower production costs and expanding industrial bases to establish a strong market presence.

Lastly, the increasing focus on smart coatings and nanotechnology integration offers a significant avenue for market expansion and value addition. Smart coatings capable of self-healing, real-time corrosion detection, or multi-functional properties are gaining traction in high-value applications such as aerospace, marine, and defense. The incorporation of nanoparticles can enhance the barrier properties and overall performance of anti-corrosive coatings, allowing for thinner, more durable, and more effective protective layers. This technological frontier promises higher performance characteristics and longer asset lifespans, creating premium market segments for manufacturers capable of delivering these advanced, high-tech pigment solutions.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Eco-Friendly & Non-Toxic Pigments | +1.5% | Global, particularly Europe & North America | Long-term (2025-2033) |

| Expansion in Emerging Economies (Infrastructure & Construction) | +1.3% | Asia Pacific, Latin America, Middle East | Medium to Long-term (2025-2033) |

| Technological Innovation in Smart Coatings & Nanotechnology | +1.0% | North America, Europe, Developed Asia | Long-term (2029-2033) |

Anti Corrosive Pigment Market Challenges Impact Analysis

The Anti Corrosive Pigment market faces a persistent challenge in terms of the complex regulatory landscape and the need for continuous compliance. Different regions and countries have varying, and often evolving, regulations regarding the use and disposal of chemicals, especially those with perceived environmental or health risks. This patchwork of regulations, including REACH in Europe, TSCA in the US, and similar frameworks in Asia, necessitates significant investment in product development, testing, and registration to ensure compliance across all target markets. Meeting these diverse and stringent requirements can be time-consuming and expensive, particularly for new product introductions or market entries, creating barriers for innovation and global market access.

Another significant challenge lies in the performance gap and cost-effectiveness of eco-friendly alternatives compared to traditional, highly effective, but toxic pigments. While there is a strong push towards sustainable solutions, many non-toxic pigments currently available may not offer the same level of long-term protection, durability, or broad applicability as their chromate- or lead-based counterparts. Bridging this performance gap without significantly increasing costs is a major hurdle for R&D departments. End-users in cost-sensitive industries may be reluctant to switch to greener options if it means compromising on performance or incurring substantially higher material costs, thus slowing the market's transition to more sustainable solutions.

Furthermore, the market experiences challenges related to the intense competition and market fragmentation. The anti-corrosive pigment industry includes a diverse range of players, from large multinational chemical corporations to specialized niche manufacturers. This fragmentation leads to competitive pricing pressures, making it difficult for all players to maintain healthy profit margins. Rapid technological advancements and the continuous introduction of new products also contribute to market dynamism, requiring companies to constantly innovate and differentiate their offerings. Maintaining a competitive edge necessitates substantial ongoing investment in research and development, efficient production processes, and effective marketing strategies, which can be particularly challenging for smaller market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Regulatory Compliance & Evolving Standards | -1.0% | Global, particularly Europe & North America | Long-term (2025-2033) |

| Performance & Cost-Effectiveness of Eco-Friendly Alternatives | -0.7% | Global | Medium-term (2025-2029) |

| Intense Market Competition & Fragmentation | -0.6% | Global | Medium-term (2025-2029) |

Anti Corrosive Pigment Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Anti Corrosive Pigment market, offering strategic insights into its current size, historical performance, and future growth trajectory. The scope includes a detailed examination of market drivers, restraints, opportunities, and challenges, providing a holistic understanding of the factors influencing market dynamics. Furthermore, the report delves into the impact of artificial intelligence on the industry, highlighting emerging technological trends and their potential to reshape the market landscape.

The study meticulously segments the market by various types, applications, and end-use industries, offering granular data for strategic decision-making. It also provides a thorough regional analysis, identifying key growth pockets and market opportunities across major geographical areas. Profiles of leading market players are included to offer insights into the competitive landscape, product portfolios, and strategic initiatives. This report serves as an essential resource for stakeholders seeking to understand market trends, identify investment opportunities, and formulate effective business strategies within the anti-corrosive pigment sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 985.7 Million |

| Market Forecast in 2033 | USD 1.55 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | PPG Industries, AkzoNobel, Sherwin-Williams Company, Jotun A/S, BASF SE, RPM International Inc., Axalta Coating Systems, Kansai Paint Co., Ltd., Nippon Paint Holdings Co., Ltd., Hempel A/S, KCC Corporation, Diamond Vogel, Sigma-Aldrich (Merck KGaA), Elementis plc, Heubach GmbH, Venator Materials PLC, Lonza Group Ltd., Cathay Industries, Tronox Holdings plc, Clariant AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Anti Corrosive Pigment market is intricately segmented to provide a detailed understanding of its diverse components and their respective growth dynamics. This segmentation is crucial for stakeholders to identify specific market niches, tailor product development strategies, and optimize distribution channels. The primary segmentation is by type, which includes traditional categories like zinc-based and chromate-based pigments, alongside the rapidly expanding non-toxic alternatives such as phosphate-based, organic, silicate-based, molybdate-based, and vanadate-based pigments. This categorization highlights the industry's shift towards safer and more environmentally friendly solutions, reflecting regulatory pressures and increasing demand for sustainable products.

Further segmentation by application provides insights into how these pigments are utilized across various industries, primarily within paints & coatings, which remains the largest application segment. However, their use in adhesives & sealants, plastics, and inks is also growing, indicating diversification of their functional roles beyond traditional coating systems. Each application demands specific performance characteristics from anti-corrosive pigments, influencing product formulation and development. Understanding these application-specific requirements is vital for manufacturers to create customized solutions that effectively address the unique challenges of each end-use.

Finally, the market is segmented by end-use industry, encompassing major sectors such as automotive, marine, construction (both buildings and infrastructure), industrial machinery and pipelines, aerospace, and packaging, among others. Each of these industries presents distinct needs for corrosion protection, driven by varying operating environments, material substrates, and regulatory compliance standards. For instance, marine applications require pigments resistant to saltwater and harsh weather, while automotive applications demand excellent adhesion and aesthetic compatibility. Analyzing these end-use segments helps in identifying key demand drivers, regional consumption patterns, and opportunities for specialized product development, enabling targeted market penetration strategies.

- By Type: Zinc-based, Chromate-based, Non-toxic (Phosphate-based, Organic, Silicate-based, Molybdate-based, Vanadate-based), Others

- By Application: Paints & Coatings, Adhesives & Sealants, Plastics, Inks

- By End-Use Industry: Automotive, Marine, Construction (Buildings & Infrastructure), Industrial (Machinery, Pipelines), Aerospace, Packaging, Others

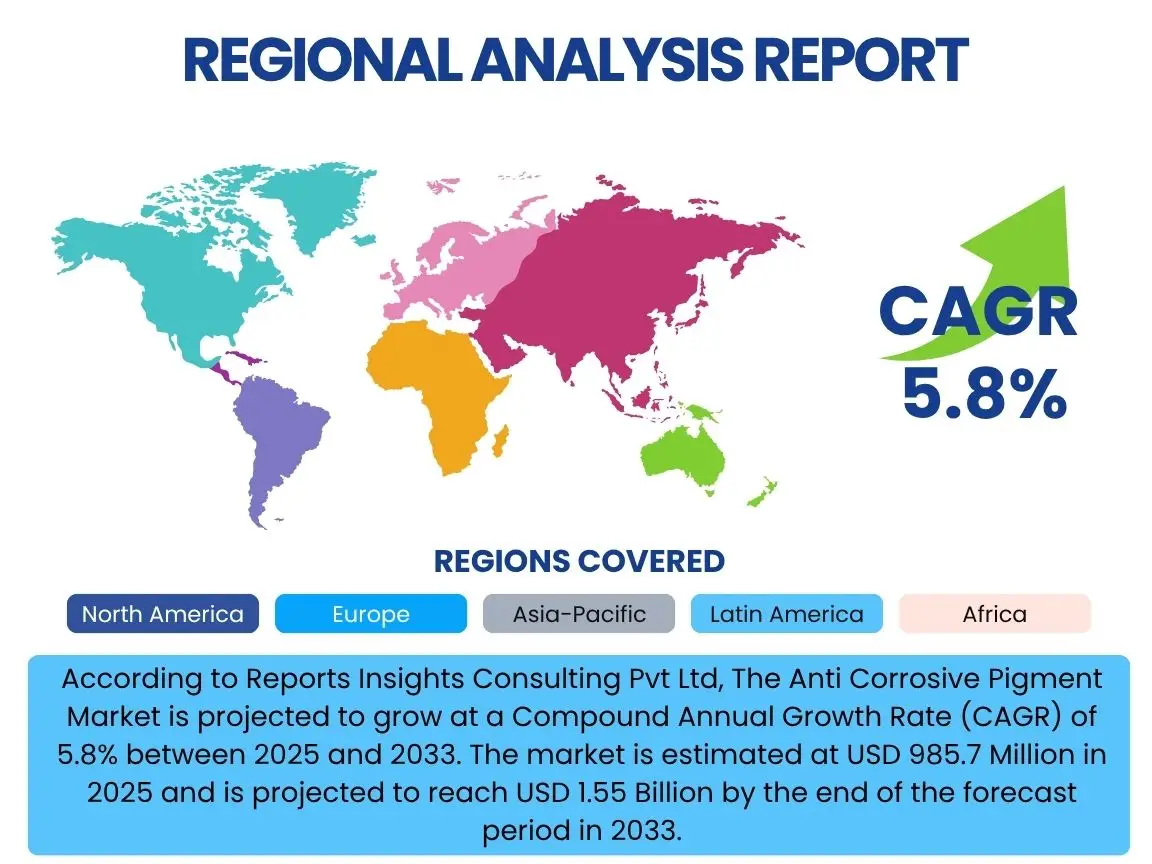

Regional Highlights

- North America: This region is characterized by stringent environmental regulations and a high demand for high-performance and innovative anti-corrosive solutions, especially in the automotive, aerospace, and general industrial sectors. Significant investments in infrastructure refurbishment and the adoption of advanced technologies like smart coatings drive market growth. The presence of key market players and a robust research and development ecosystem contribute to continuous innovation.

- Europe: Europe is a leader in adopting eco-friendly and sustainable anti-corrosive pigments due to strict environmental policies, such as REACH regulations. The region's mature automotive, marine, and industrial sectors consistently demand advanced corrosion protection, pushing manufacturers towards greener formulations. Eastern European countries also present emerging opportunities with increasing industrialization and infrastructure projects.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing region in the Anti Corrosive Pigment market, primarily driven by rapid industrialization, urbanization, and massive infrastructure development projects in countries like China, India, Japan, and South Korea. The expanding automotive, construction, and marine industries, coupled with rising manufacturing activities, fuel the demand for cost-effective and efficient anti-corrosive solutions. Increasing environmental awareness is also gradually accelerating the shift towards non-toxic alternatives.

- Latin America: This region shows steady growth, fueled by investments in infrastructure, oil and gas, and mining sectors. Countries like Brazil and Mexico are leading the demand for anti-corrosive pigments, driven by economic development and the need to protect assets in challenging environmental conditions. Regulatory frameworks are evolving, slowly encouraging the adoption of more advanced and environmentally compliant products.

- Middle East and Africa (MEA): The MEA region presents opportunities driven by the robust oil and gas sector, construction boom (particularly in the GCC countries), and increasing investments in industrial and marine infrastructure. Harsh climatic conditions in many parts of the region necessitate highly durable and effective anti-corrosive coatings, creating a consistent demand for specialized pigments. Diversification efforts away from oil economies are also spurring growth in other industrial sectors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Anti Corrosive Pigment Market.- PPG Industries

- AkzoNobel

- Sherwin-Williams Company

- Jotun A/S

- BASF SE

- RPM International Inc.

- Axalta Coating Systems

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- Hempel A/S

- KCC Corporation

- Diamond Vogel

- Sigma-Aldrich (Merck KGaA)

- Elementis plc

- Heubach GmbH

- Venator Materials PLC

- Lonza Group Ltd.

- Cathay Industries

- Tronox Holdings plc

- Clariant AG

Frequently Asked Questions

What is the current market size and projected growth rate of the Anti Corrosive Pigment market?

The Anti Corrosive Pigment market is estimated at USD 985.7 Million in 2025. It is projected to reach USD 1.55 Billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 5.8% from 2025 to 2033. This growth is primarily driven by global infrastructure development, increasing industrialization, and rising demand for enhanced asset protection across various end-use industries.

What are the primary drivers propelling the growth of the Anti Corrosive Pigment market?

The key drivers for the Anti Corrosive Pigment market include expanding infrastructure development and maintenance activities globally, increasingly stringent environmental regulations mandating the use of eco-friendly solutions, and robust demand from major end-use industries such as automotive, marine, and construction. Furthermore, continuous technological advancements in pigment formulation are enhancing performance and broadening application possibilities, contributing significantly to market expansion.

Which regions are expected to exhibit the most significant growth in the Anti Corrosive Pigment market?

Asia Pacific (APAC) is anticipated to be the fastest-growing region in the Anti Corrosive Pigment market due to rapid industrialization, extensive urbanization, and substantial infrastructure projects, particularly in countries like China and India. North America and Europe will also maintain significant market shares, driven by a strong focus on high-performance coatings, advanced research and development, and strict environmental compliance.

What are the major challenges faced by the Anti Corrosive Pigment market?

The Anti Corrosive Pigment market faces several challenges, including the volatility of raw material prices, which impacts manufacturing costs and profit margins. Stringent and evolving regulatory landscapes concerning hazardous chemicals necessitate continuous reformulation and investment in compliance. Additionally, the challenge lies in developing eco-friendly alternatives that can match the performance and cost-effectiveness of traditional pigments, alongside intense market competition and fragmentation that demand constant innovation and differentiation.

How is artificial intelligence impacting the Anti Corrosive Pigment industry?

Artificial intelligence (AI) is significantly impacting the Anti Corrosive Pigment industry by accelerating the discovery and development of novel pigment chemistries through advanced material informatics. AI also optimizes pigment formulations for enhanced performance and cost-efficiency using machine learning algorithms. Furthermore, it improves predictive maintenance and lifespan estimation of coated assets through data analytics, leading to more efficient operations and extended product durability across the value chain.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted