Annuity Insurance Market

Annuity Insurance Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701009 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

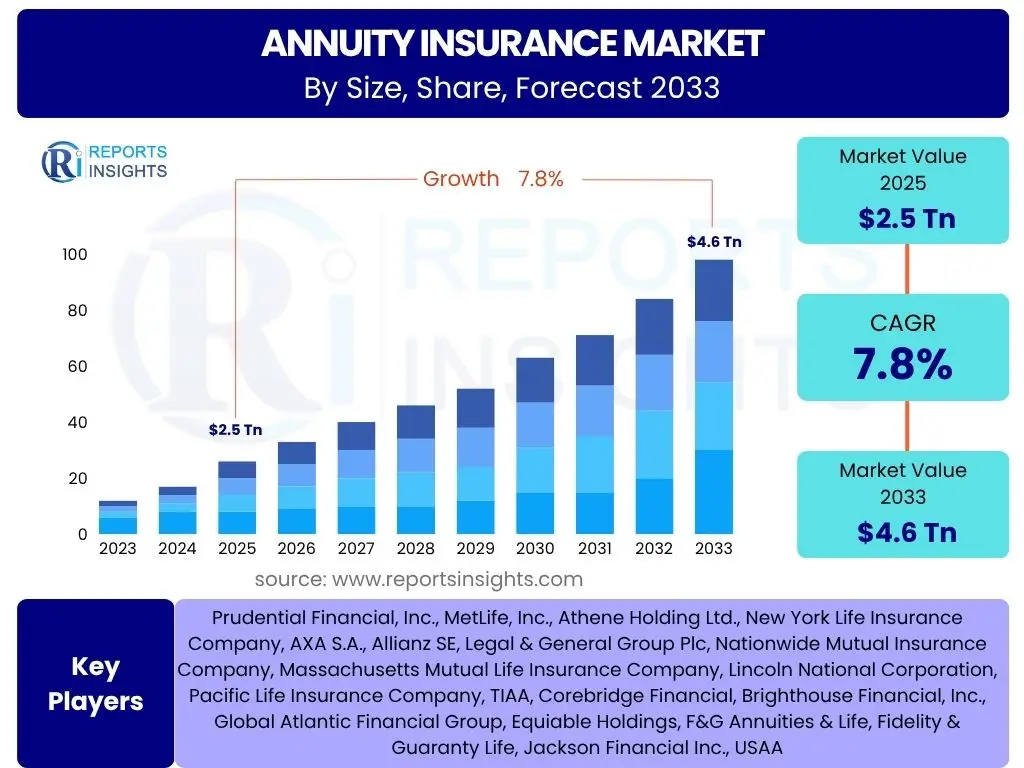

Annuity Insurance Market Size

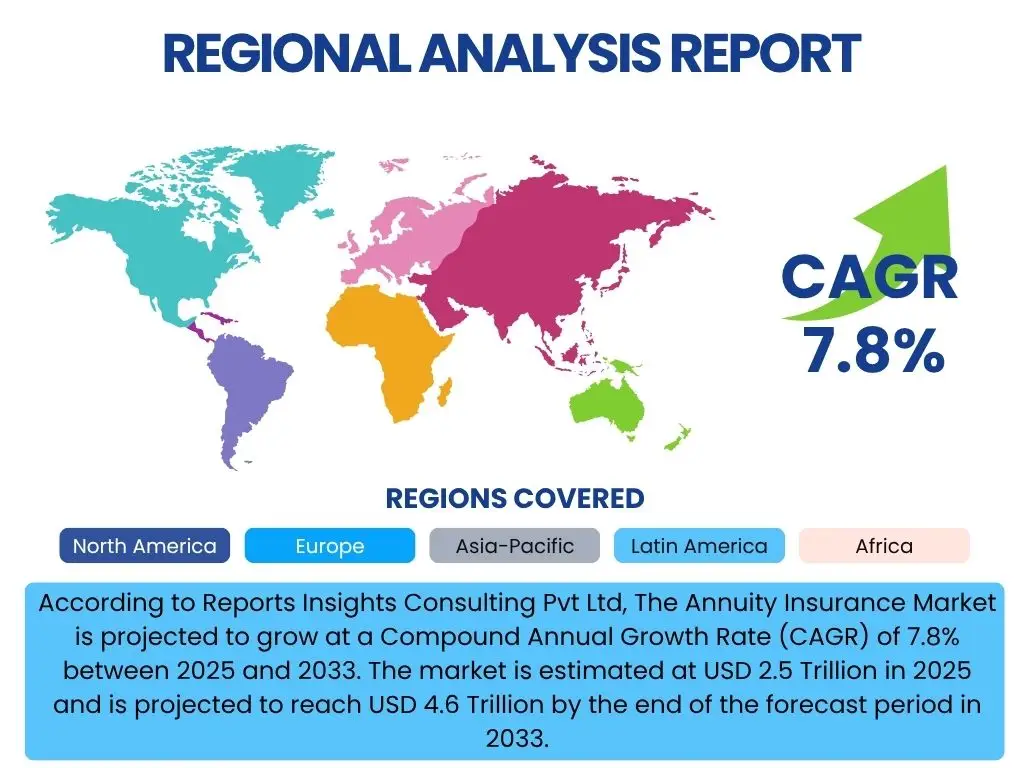

According to Reports Insights Consulting Pvt Ltd, The Annuity Insurance Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 2.5 Trillion in 2025 and is projected to reach USD 4.6 Trillion by the end of the forecast period in 2033.

Key Annuity Insurance Market Trends & Insights

The Annuity Insurance market is witnessing significant shifts driven by evolving demographic landscapes, technological advancements, and changing consumer expectations. Common user inquiries often focus on how longevity risk is being addressed, the impact of digital platforms on distribution, and the increasing demand for personalized retirement solutions. Furthermore, there is growing interest in annuities that offer protection against market volatility while providing guaranteed income streams, reflecting a desire for financial security amidst economic uncertainties. The integration of environmental, social, and governance (ESG) factors into investment strategies for annuity portfolios is also emerging as a notable trend, aligning with broader responsible investing principles.

Another prominent area of interest concerns the adaptability of annuity products to diverse retirement needs, moving beyond traditional structures to offer more flexibility and customization. This includes products designed for phased retirement, those with long-term care riders, and options catering to different risk appetites. The expansion of financial literacy initiatives regarding annuities is also critical, as consumers seek clearer understanding of complex product features and their role in comprehensive financial planning. The market is striving to demystify annuities, making them more accessible and transparent to a wider demographic.

Additionally, the regulatory landscape continues to shape market trends, with ongoing discussions around consumer protection, disclosure requirements, and capital adequacy for insurers. Insurers are also exploring new distribution channels beyond traditional agents, including direct-to-consumer digital platforms and partnerships with financial advisors, to broaden their reach and enhance customer engagement. This multi-channel approach is crucial for capturing the attention of younger generations who are beginning to plan for retirement.

- Increased demand for guaranteed lifetime income solutions amidst market volatility.

- Growing adoption of digital platforms for annuity sales, servicing, and personalized advice.

- Development of hybrid annuity products combining guaranteed income with growth potential.

- Emphasis on customization and flexibility in annuity design to meet diverse retirement needs.

- Integration of ESG principles into annuity investment strategies.

AI Impact Analysis on Annuity Insurance

The integration of Artificial Intelligence (AI) into the annuity insurance sector is a topic of considerable user interest, particularly concerning its potential to transform operational efficiency, risk management, and customer engagement. Users frequently inquire about how AI can streamline complex underwriting processes, personalize product offerings, and enhance the overall client experience. There is a general expectation that AI will lead to more accurate risk assessments and pricing, ultimately benefiting both insurers through reduced losses and consumers through more tailored and competitive products.

AI's influence extends to predictive analytics, enabling insurers to forecast market trends, consumer behavior, and actuarial risks with greater precision. This capability is crucial for managing long-term liabilities associated with annuity products and ensuring solvency. Concerns often revolve around data privacy, the ethical implications of AI-driven decision-making, and the need for robust cybersecurity measures to protect sensitive client information. Users also seek clarity on how AI will impact job roles within the industry and the skill sets required for the future workforce.

Furthermore, AI is expected to revolutionize customer service through intelligent chatbots, virtual assistants, and automated claims processing, providing faster and more efficient interactions. This shift aims to improve customer satisfaction by offering instantaneous support and resolving queries without human intervention for routine tasks. The ultimate goal is to leverage AI to create a more dynamic, responsive, and secure annuity ecosystem that can adapt to future market demands and consumer preferences.

- Enhanced underwriting and risk assessment through advanced data analytics.

- Personalized product recommendations and customized client portfolios.

- Automated customer service via chatbots and virtual assistants for improved efficiency.

- Improved fraud detection and prevention capabilities.

- Streamlined claims processing and operational efficiencies.

Key Takeaways Annuity Insurance Market Size & Forecast

Common inquiries regarding the Annuity Insurance market size and forecast often center on the primary drivers of growth, the long-term viability of guaranteed income products, and the influence of macroeconomic factors. The market is poised for sustained expansion, primarily driven by the demographic imperative of an aging global population seeking reliable retirement income solutions. The forecast indicates a robust Compound Annual Growth Rate, underscoring the increasing recognition of annuities as essential components of comprehensive financial planning, particularly for individuals concerned about outliving their savings.

A significant takeaway is the resilience and adaptability of the annuity sector. Despite historical challenges such as periods of low interest rates, the industry has demonstrated an ability to innovate and introduce products that cater to diverse investor needs and risk tolerances. The projected growth reflects ongoing product diversification, the adoption of digital distribution channels, and efforts to simplify complex offerings to improve consumer understanding and accessibility. This forward momentum is expected to continue as awareness of longevity risk intensifies globally.

Moreover, the forecast highlights the critical role of favorable regulatory environments and increasing financial literacy in accelerating market adoption. Insurers are strategically investing in technology and talent to capitalize on these trends, aiming to optimize their operational frameworks and enhance their competitive positioning. The overall outlook suggests a dynamic market environment characterized by continuous innovation and a steady increase in demand for predictable retirement income streams.

- The Annuity Insurance market is projected for significant growth, driven by an aging global population and increasing longevity risk awareness.

- Technological advancements and digital transformation are key enablers for market expansion and improved customer engagement.

- Product innovation, including hybrid and customized annuities, is addressing diverse retirement income needs and risk appetites.

- The market exhibits resilience and adaptability, continuously evolving to meet changing macroeconomic conditions and consumer demands.

- Growing financial literacy and supportive regulatory frameworks are fostering greater adoption and trust in annuity products.

Annuity Insurance Market Drivers Analysis

The Annuity Insurance market is propelled by a confluence of demographic and economic factors, creating a strong demand for guaranteed retirement income solutions. The global aging population is a primary driver, as more individuals enter retirement age and seek reliable income streams to cover living expenses for an extended period. This demographic shift intensifies the need for products that mitigate longevity risk, ensuring that individuals do not outlive their savings.

Furthermore, the shift from defined benefit pension plans to defined contribution plans places greater responsibility on individuals for their retirement savings, spurring demand for products that can replicate the certainty of a pension. Rising awareness about the importance of financial planning and the risks associated with market volatility also encourages individuals to seek the security offered by annuities. Economic environments with stable or rising interest rates can also enhance the attractiveness of certain annuity products, as they may offer more competitive returns.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Aging Global Population & Longevity Risk | +1.5% | Global, particularly Developed Economies (North America, Europe, East Asia) | Long-term (2025-2033) |

| Shift from Defined Benefit to Defined Contribution Plans | +0.8% | North America, Europe, Australia | Medium-term (2025-2029) |

| Increasing Demand for Guaranteed Income Solutions | +1.2% | Global | Long-term (2025-2033) |

| Rising Interest Rate Environment | +0.7% | Global, especially US & EU markets | Short to Medium-term (2025-2027) |

| Growing Awareness of Retirement Planning & Financial Literacy | +0.6% | Emerging Economies (APAC, Latin America), Developed Markets | Medium-term (2026-2030) |

Annuity Insurance Market Restraints Analysis

Despite significant growth drivers, the Annuity Insurance market faces several restraints that can impede its expansion and adoption. One major historical challenge has been periods of persistently low interest rates, which can diminish the attractiveness of annuities by reducing the payout rates insurers can offer. While interest rates have recently seen an upward trend, the sensitivity of annuity products to rate fluctuations remains a key consideration for consumers and providers alike.

The inherent complexity of many annuity products also acts as a restraint. Consumers often find it challenging to understand the various features, riders, surrender charges, and tax implications, leading to hesitation and a preference for simpler investment vehicles. This complexity can erode consumer trust and make the sales process more arduous. Regulatory scrutiny and evolving compliance requirements also impose significant operational and financial burdens on insurers, potentially limiting product innovation or increasing costs for consumers.

Furthermore, economic uncertainties, such as inflation or recessionary fears, can make consumers wary of committing large sums to long-term products. Inflation, in particular, poses a risk to fixed annuity payouts, as the purchasing power of future income streams can erode over time, which may deter potential buyers who prioritize inflation-protected growth. The perception of illiquidity, where funds are tied up for extended periods, also remains a concern for some investors.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of Product Structures & Lack of Consumer Understanding | -0.9% | Global | Long-term (2025-2033) |

| Historical Low Interest Rate Environment (impact on perception) | -0.6% | Global | Medium-term (2025-2028) |

| Regulatory Scrutiny & Compliance Burden | -0.5% | North America, Europe | Medium-term (2025-2029) |

| Perception of Illiquidity & Surrender Charges | -0.4% | Global | Long-term (2025-2033) |

| Concerns over Inflation and Erosion of Purchasing Power | -0.7% | Global | Short to Medium-term (2025-2027) |

Annuity Insurance Market Opportunities Analysis

The Annuity Insurance market is ripe with opportunities for innovation and expansion, particularly driven by technological advancements and evolving consumer preferences. The digitalization of the insurance industry presents a significant avenue for growth, enabling insurers to streamline distribution, enhance customer onboarding, and offer more personalized digital experiences. Direct-to-consumer models and online platforms can significantly reduce acquisition costs and broaden market reach, attracting younger demographics who prefer digital interactions.

Customization and personalization of annuity products represent another major opportunity. As consumer needs become more segmented, there is increasing demand for flexible solutions that can be tailored to individual financial goals, risk tolerances, and life stages. This includes the development of hybrid products that combine features of traditional annuities with long-term care benefits or enhanced death benefits, appealing to a wider audience. The increasing focus on ESG (Environmental, Social, and Governance) investing also opens doors for annuity products linked to sustainable investment portfolios, attracting socially conscious investors.

Moreover, untapped markets, particularly in emerging economies with growing middle classes and developing retirement savings cultures, offer substantial growth potential. Educating these new markets about the benefits of annuities and adapting products to local economic conditions and cultural preferences can unlock significant demand. Partnerships with financial advisors and wealth management firms to integrate annuities into holistic financial plans also remain a critical growth strategy, leveraging their expertise and client networks.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Digitalization of Distribution and Sales Channels | +1.0% | Global | Medium-term (2025-2030) |

| Development of Hybrid and Customizable Annuity Products | +0.9% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Expansion into Emerging Markets & Underserved Demographics | +0.8% | Asia Pacific, Latin America, Africa | Long-term (2027-2033) |

| Integration of ESG-aligned Investment Options | +0.6% | Europe, North America | Medium-term (2026-2031) |

| Partnerships with Financial Advisors & Wealth Management Firms | +0.7% | Global | Medium to Long-term (2025-2033) |

Annuity Insurance Market Challenges Impact Analysis

The Annuity Insurance market faces several challenges that require strategic responses from insurers to maintain growth and profitability. Economic volatility, including fluctuating interest rates, inflationary pressures, and unpredictable market performance, poses significant challenges to product design and pricing. Sustained periods of low interest rates can squeeze profit margins for insurers and reduce the attractiveness of guaranteed income products, while high inflation can erode the real value of fixed payouts, making them less appealing to consumers.

The evolving regulatory landscape presents a continuous challenge, as compliance with new rules related to consumer protection, solvency, and disclosure requires substantial investment and adaptation. Insurers must navigate a complex patchwork of regulations across different jurisdictions, which can hinder product standardization and market entry. Additionally, maintaining consumer trust is paramount, particularly given past controversies or mis-selling allegations in the financial services sector; transparency and clear communication are vital to rebuilding and sustaining confidence.

Moreover, the industry grapples with technological disruption and the need for significant digital transformation. Legacy IT systems can impede innovation and efficiency, while cybersecurity threats pose risks to sensitive client data. Attracting and retaining talent with expertise in both actuarial science and advanced technology is also a growing challenge, as the demand for data scientists, AI specialists, and digital marketing experts intensifies across all sectors.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Economic Volatility & Interest Rate Fluctuations | -0.8% | Global | Short to Medium-term (2025-2028) |

| Evolving & Complex Regulatory Environment | -0.7% | North America, Europe | Medium-term (2025-2030) |

| Consumer Trust Issues & Need for Enhanced Transparency | -0.6% | Global | Long-term (2025-2033) |

| Technological Adoption & Legacy System Modernization | -0.5% | Global | Medium-term (2025-2029) |

| Cybersecurity Risks & Data Privacy Concerns | -0.4% | Global | Long-term (2025-2033) |

Annuity Insurance Market - Updated Report Scope

This market insights report provides a detailed analysis of the Annuity Insurance market, offering a comprehensive understanding of its current size, historical performance, and future growth projections from 2025 to 2033. It examines key market trends, drivers, restraints, opportunities, and challenges influencing the industry landscape. The report also includes an in-depth assessment of AI's impact on the sector, along with a detailed segmentation analysis across various product types, distribution channels, and end-users, complemented by regional highlights and profiles of leading market players. The objective is to equip stakeholders with actionable insights for strategic decision-making in the dynamic annuity insurance market.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.5 Trillion |

| Market Forecast in 2033 | USD 4.6 Trillion |

| Growth Rate | 7.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Prudential Financial, Inc., MetLife, Inc., Athene Holding Ltd., New York Life Insurance Company, AXA S.A., Allianz SE, Legal & General Group Plc, Nationwide Mutual Insurance Company, Massachusetts Mutual Life Insurance Company, Lincoln National Corporation, Pacific Life Insurance Company, TIAA, Corebridge Financial, Brighthouse Financial, Inc., Global Atlantic Financial Group, Equiable Holdings, F&G Annuities & Life, Fidelity & Guaranty Life, Jackson Financial Inc., USAA |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Annuity Insurance market is meticulously segmented to provide a granular view of its diverse landscape, enabling a deeper understanding of market dynamics and consumer preferences. This segmentation helps in identifying specific growth pockets, tailoring product offerings, and optimizing distribution strategies. The primary dimensions of segmentation include product type, distribution channel, and end-user, each revealing unique market characteristics and growth trajectories. This detailed analysis supports stakeholders in making informed decisions by highlighting the performance and potential of various market niches within the broader annuity sector.

Analyzing the market across these segments reveals shifts in consumer demand from traditional fixed annuities towards more flexible and hybrid products that offer a balance of guaranteed income and growth potential, especially in an evolving interest rate environment. The proliferation of digital distribution channels is also reshaping how annuities are sold and serviced, complementing traditional agent-based models. Furthermore, understanding the distinct needs of individual retirees versus corporate pension plans is crucial for product development and marketing efforts. This comprehensive segmentation framework ensures that all facets of the annuity market are thoroughly explored, providing a complete picture for strategic planning.

- By Product Type:

- Fixed Annuities: Provide guaranteed income and principal protection, often chosen for their predictability.

- Variable Annuities: Offer investment options tied to market performance, with potential for higher returns but also greater risk.

- Indexed Annuities: Combine features of fixed and variable annuities, linking returns to a market index without direct exposure to market losses.

- Longevity Annuities: Designed to provide income far into the future, mitigating the risk of outliving savings, typically starting payouts at an advanced age.

- Qualified Longevity Annuity Contracts (QLACs): A specific type of longevity annuity designed to meet IRS requirements, often used in retirement plans.

- Other Annuity Products: Includes innovative or specialized annuity structures not covered by the main categories.

- By Distribution Channel:

- Agency/Captive Agents: Insurers' dedicated sales forces.

- Independent Agents/Brokers: Licensed professionals representing multiple insurance companies.

- Bancassurance: Distribution through banks and financial institutions.

- Direct to Consumer (Online/Digital): Sales directly to customers via digital platforms.

- Financial Advisors/RIAs: Independent financial professionals offering comprehensive planning.

- Other Channels: Includes workplace benefits programs, associations, etc.

- By End-User:

- Individuals: Focus on personal retirement planning, wealth preservation, and income generation for single or joint lives.

- Groups/Corporate: Annuities used in employer-sponsored retirement plans, pension de-risking, or employee benefit programs.

Regional Highlights

- North America: The region, particularly the United States, represents a mature and dominant market for annuity insurance, driven by a large aging population, sophisticated financial planning infrastructure, and a robust regulatory framework. The demand for guaranteed retirement income is consistently high, with a strong focus on variable and indexed annuities providing a balance of security and growth potential. Canada also contributes significantly with its emphasis on retirement savings and pension solutions.

- Europe: Characterized by diverse regulatory environments and varying retirement cultures, Europe is a substantial market with steady growth. Countries like the UK, Germany, and France are key players, experiencing increasing demand for annuities due to demographic shifts and a move towards individual retirement planning. The market here often sees innovative products adapting to specific national pension reforms and an increasing interest in unit-linked and hybrid annuity products.

- Asia Pacific (APAC): This region is projected to be the fastest-growing market, fueled by rapidly aging populations in countries like Japan, South Korea, and China, along with a burgeoning middle class in emerging economies such as India and Southeast Asian nations. Rising disposable incomes, increasing financial literacy, and developing social security systems are driving a strong demand for long-term savings and retirement solutions, presenting immense opportunities for annuity providers.

- Latin America: While a nascent market compared to North America and Europe, Latin America is experiencing gradual growth in annuity adoption. Economic reforms, increasing awareness of retirement planning, and a growing insurance sector are contributing to this expansion. Countries like Brazil and Mexico are leading the way, though market development is often influenced by economic stability and the evolution of regulatory frameworks to support long-term insurance products.

- Middle East and Africa (MEA): This region is at an early stage of annuity market development but holds significant potential, particularly in the Gulf Cooperation Council (GCC) countries due to wealth accumulation and a growing expatriate population seeking retirement solutions. Market growth is contingent on regulatory harmonization, increased financial literacy, and the introduction of Sharia-compliant annuity products to cater to specific regional demands.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Annuity Insurance Market.- Prudential Financial, Inc.

- MetLife, Inc.

- Athene Holding Ltd.

- New York Life Insurance Company

- AXA S.A.

- Allianz SE

- Legal & General Group Plc

- Nationwide Mutual Insurance Company

- Massachusetts Mutual Life Insurance Company

- Lincoln National Corporation

- Pacific Life Insurance Company

- TIAA

- Corebridge Financial

- Brighthouse Financial, Inc.

- Global Atlantic Financial Group

- Equitable Holdings

- F&G Annuities & Life

- Fidelity & Guaranty Life

- Jackson Financial Inc.

- USAA

Frequently Asked Questions

What is an annuity and how does it work?

An annuity is a financial contract typically issued by insurance companies, designed to provide a steady stream of income, usually for retirement. It involves making payments to the insurer, either in a lump sum or over time, in exchange for regular disbursements that begin immediately or at a future date. Annuities offer various features, including principal protection, tax-deferred growth, and guaranteed income for life, helping to mitigate the risk of outliving one's savings.

Why should I consider an annuity for retirement planning?

Annuities are considered for retirement planning primarily for their ability to provide guaranteed income, addressing longevity risk and ensuring a predictable cash flow in retirement. They offer tax-deferred growth on investments, which can enhance overall returns over the long term. Additionally, some annuities offer riders for inflation protection, long-term care benefits, or death benefits, providing comprehensive financial security and peace of mind for retirees and their beneficiaries.

What are the main types of annuities available?

The primary types of annuities include Fixed Annuities, offering guaranteed interest rates and predictable payouts; Variable Annuities, whose returns are tied to underlying investment performance with potential for higher growth but also market risk; and Indexed Annuities, which link returns to a market index without direct stock market exposure, providing a balance of growth potential and principal protection. Each type serves different risk appetites and financial goals for retirement income planning.

How do interest rates impact annuity products and their payouts?

Interest rates significantly impact annuity products, especially fixed annuities. Higher prevailing interest rates generally allow insurers to offer more attractive guaranteed interest rates and higher payout percentages on fixed and immediate annuities, increasing their appeal to consumers. Conversely, prolonged periods of low interest rates can reduce the competitiveness of annuity payouts, making it more challenging for insurers to offer attractive returns while managing their liabilities. Variable and indexed annuities are less directly affected by interest rate fluctuations as their returns are tied to market performance or indices.

What is the future outlook for the Annuity Insurance market?

The future outlook for the Annuity Insurance market is positive, driven by a growing aging global population and increasing awareness of longevity risk. Technological advancements, particularly in AI and digital distribution, are expected to enhance product customization and accessibility. While challenges such as economic volatility and regulatory complexity persist, the market is poised for continued innovation in product design and distribution strategies, aiming to meet the evolving demands for secure and flexible retirement income solutions worldwide.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted