Anisotropic Conductive Adhesive Market

Anisotropic Conductive Adhesive Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709037 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Anisotropic Conductive Adhesive Market Size

The Anisotropic Conductive Adhesive (ACA) Market is experiencing robust growth, driven by the increasing demand for miniaturized and high-performance electronic components across various industries. These specialized adhesives are crucial for fine-pitch interconnections, offering electrical conductivity in one direction while maintaining electrical insulation in the transverse plane, thereby enabling compact and reliable packaging solutions. The market’s expansion is closely linked to technological advancements in consumer electronics, automotive systems, and advanced displays, where density and reliability are paramount.

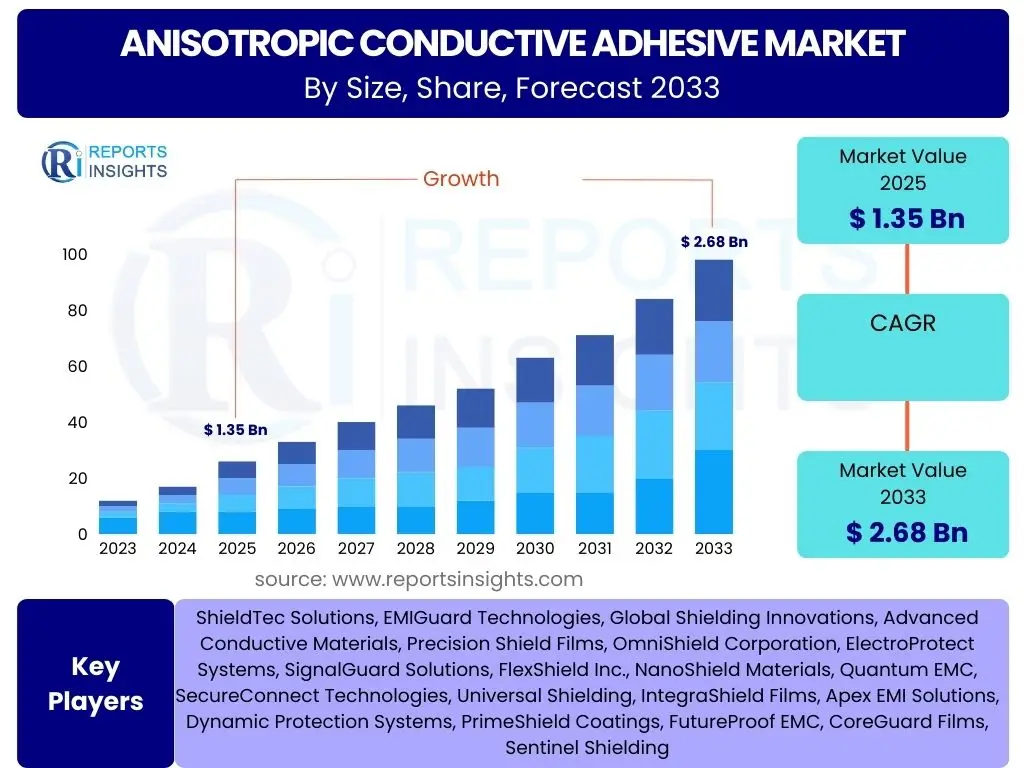

According to Reports Insights Consulting Pvt Ltd, The Anisotropic Conductive Adhesive Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 1.35 billion in 2025 and is projected to reach USD 2.68 billion by the end of the forecast period in 2033. This growth trajectory underscores the critical role ACAs play in the evolving landscape of electronic manufacturing, as industries increasingly adopt advanced bonding techniques for enhanced performance and reduced form factors.

Key Anisotropic Conductive Adhesive Market Trends & Insights

User inquiries frequently focus on the primary forces shaping the Anisotropic Conductive Adhesive market, seeking to understand how technological shifts and industrial demands are influencing its development. Common questions revolve around the adoption of ACAs in emerging applications, the impact of miniaturization trends, and the ongoing innovations in material science that enhance performance. Insights suggest a significant pivot towards flexible electronics and advanced packaging, driving the need for more versatile and high-reliability adhesive solutions, alongside a growing emphasis on sustainable manufacturing practices and materials.

- Miniaturization of Electronic Devices: The relentless drive towards smaller, thinner, and lighter electronic products necessitates fine-pitch interconnection solutions, directly boosting ACA demand for display drivers, camera modules, and wearables.

- Advancements in Flexible and Wearable Electronics: The emergence of flexible displays, bendable circuits, and wearable health monitors requires robust and flexible bonding, positioning ACAs as a critical enabler for these innovative products.

- Increasing Adoption in Automotive Electronics: The proliferation of advanced driver-assistance systems (ADAS), infotainment systems, and electric vehicle components demands high-reliability, vibration-resistant, and thermally stable interconnections provided by ACAs.

- Growth of 5G Technology and IoT Devices: The deployment of 5G networks and the expansion of the Internet of Things (IoT) ecosystem generate increased demand for high-frequency and high-speed electronic components, requiring ACAs for reliable signal integrity and compact packaging.

- Development of Advanced Packaging Technologies: Techniques like Chip-on-Glass (CoG), Chip-on-Flex (CoF), and System-in-Package (SiP) extensively utilize ACAs for secure and efficient electrical and mechanical connections.

AI Impact Analysis on Anisotropic Conductive Adhesive

User queries regarding the impact of Artificial Intelligence (AI) on the Anisotropic Conductive Adhesive market often explore how AI can optimize material development, enhance manufacturing processes, and improve product quality and reliability. There is significant interest in AI's potential to accelerate the design and discovery of novel ACA formulations with enhanced properties, as well as its application in predictive analytics for quality control. Expectations center on AI's ability to drive greater efficiency, reduce development cycles, and enable more precise customization of ACA solutions to meet specific application requirements.

AI's influence is also anticipated in streamlining the entire supply chain, from raw material sourcing to final product delivery, by optimizing inventory management and predicting demand fluctuations. This predictive capability can help manufacturers reduce waste and improve overall operational agility. Furthermore, AI-powered vision systems are expected to enhance automated inspection processes in ACA application, ensuring higher precision and reducing defects in complex electronic assemblies, thereby contributing to higher yield rates and lower production costs.

- Accelerated Material Design and Discovery: AI algorithms can analyze vast datasets of material properties, predicting optimal compositions for new ACA formulations with desired electrical, mechanical, and thermal characteristics, significantly reducing research and development timelines.

- Optimized Manufacturing Processes: AI-driven process control systems can monitor and adjust parameters during ACA production and application, such as dispensing volume, curing temperature, and pressure, leading to higher precision, consistency, and reduced waste.

- Predictive Quality Control and Defect Detection: Machine learning models can analyze real-time data from production lines to identify potential defects in ACA bonds, allowing for proactive adjustments and ensuring higher product reliability and yield rates.

- Enhanced Supply Chain Management: AI can optimize inventory levels, forecast demand more accurately, and identify potential supply chain disruptions for raw materials used in ACAs, improving operational efficiency and resilience.

- Personalized Formulation for Specific Applications: AI can facilitate the customization of ACA properties to meet the unique requirements of diverse applications, enabling faster development of specialized adhesives for niche markets.

Key Takeaways Anisotropic Conductive Adhesive Market Size & Forecast

The primary insights derived from the Anisotropic Conductive Adhesive market size and forecast consistently highlight its strong growth potential, driven by the pervasive trend of electronic device miniaturization and the increasing demand for advanced connectivity. Users are keen to understand the core factors contributing to this expansion and the long-term viability of ACA solutions. Key takeaways emphasize the crucial role ACAs play in enabling next-generation electronics across diverse sectors, underlining their indispensable nature in modern manufacturing processes and their continued evolution to meet escalating performance requirements.

The forecast underscores a significant shift towards high-performance and specialty ACAs designed for extreme conditions or specific application needs, such as high-frequency communication or harsh automotive environments. This indicates not just an increase in volume but also a qualitative improvement in the market offerings. Furthermore, the robust CAGR signals sustained investment in R&D within the ACA sector, aimed at overcoming existing limitations and exploring new application frontiers, thereby ensuring its continued relevance and expansion over the coming decade.

- Robust Growth Trajectory: The market is projected for significant expansion with a CAGR of 8.9% from 2025 to 2033, indicating sustained demand and technological advancements.

- Essential for Miniaturization: ACAs are critical enablers for the ongoing miniaturization of electronic devices, particularly in displays, semiconductors, and portable electronics.

- Diversifying Application Landscape: Beyond traditional displays, ACAs are gaining traction in high-growth areas like automotive electronics, 5G infrastructure, IoT, and medical devices.

- Technological Innovation is Key: Continuous innovation in material science, processing techniques, and formulation development is essential to address evolving industry requirements for performance and reliability.

- Strategic Market Importance: ACAs represent a strategic component in the electronics manufacturing supply chain, offering a cost-effective and efficient alternative to traditional soldering in certain applications.

Anisotropic Conductive Adhesive Market Drivers Analysis

The Anisotropic Conductive Adhesive (ACA) market is propelled by several potent forces, primarily stemming from the pervasive trends within the electronics industry. The relentless pursuit of smaller, lighter, and more powerful electronic devices mandates advanced interconnection solutions that traditional methods often cannot provide. ACAs offer a unique combination of fine-pitch capability, low-temperature processing, and lead-free compliance, making them an ideal choice for a wide array of modern electronic assemblies.

Furthermore, the rapid expansion of application areas such as high-resolution displays, sophisticated automotive electronics, and the burgeoning ecosystem of IoT devices significantly contributes to market acceleration. These sectors require robust, reliable, and space-efficient electrical connections, which ACAs are uniquely positioned to deliver. The growing emphasis on sustainable and lead-free manufacturing also indirectly boosts the adoption of ACAs as an environmentally friendlier alternative to solder-based processes.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Miniaturized Electronic Devices | +2.5% | Global, particularly Asia Pacific (China, South Korea, Japan), North America, Europe | 2025-2033 (Long-term) |

| Growth in Flexible and Wearable Electronics | +1.8% | Global, particularly Asia Pacific, North America, Europe | 2025-2033 (Long-term) |

| Expanding Application in Automotive Electronics (ADAS, Infotainment) | +1.5% | Europe, North America, Asia Pacific (China, Japan) | 2025-2033 (Mid to Long-term) |

| Technological Advancements in Display Manufacturing (e.g., OLED, Micro-LED) | +1.2% | Asia Pacific (South Korea, China, Japan) | 2025-2033 (Long-term) |

Anisotropic Conductive Adhesive Market Restraints Analysis

Despite the strong growth drivers, the Anisotropic Conductive Adhesive market faces several notable restraints that could temper its expansion. One significant challenge is the relatively higher cost of ACA materials compared to traditional soldering techniques, which can deter adoption in cost-sensitive applications or regions. This cost factor often includes not only the adhesive itself but also the specialized equipment required for precise application and curing processes, presenting a barrier to entry for smaller manufacturers.

Another key restraint is the limited repairability of ACA bonds. Once an ACA joint is formed, disassembling and rejoining components without damage can be significantly more challenging than with traditional solder, leading to higher scrap rates in rework scenarios. Furthermore, the performance of ACAs can be sensitive to environmental factors like humidity and temperature fluctuations, potentially impacting long-term reliability in harsh operating conditions. Competition from alternative bonding technologies, especially advanced soldering pastes and other conductive materials, also poses a continuous challenge to market penetration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Cost Compared to Traditional Soldering | -1.0% | Global, particularly emerging economies | 2025-2033 (Long-term) |

| Limited Repairability and Rework Challenges | -0.8% | Global | 2025-2033 (Long-term) |

| Performance Sensitivity to Environmental Factors (e.g., Humidity, Temperature) | -0.6% | Global, particularly high-reliability applications | 2025-2033 (Mid-term) |

| Competition from Alternative Interconnection Technologies | -0.5% | Global | 2025-2033 (Long-term) |

Anisotropic Conductive Adhesive Market Opportunities Analysis

The Anisotropic Conductive Adhesive market is poised to capitalize on several significant opportunities, driven by ongoing technological advancements and evolving industry requirements. The proliferation of 5G technology and the expansion of the Internet of Things (IoT) ecosystem represent substantial avenues for growth, as these applications demand high-density, high-frequency, and reliable interconnections in compact form factors. ACAs are ideally suited for these requirements, enabling the integration of complex modules into smaller devices without compromising performance.

Furthermore, the continuous innovation in advanced display technologies, such as micro-LEDs and flexible OLEDs, presents a fertile ground for ACA adoption. These displays require extremely fine-pitch bonding and excellent optical performance, areas where ACAs are rapidly improving. The increasing complexity and sophistication of medical devices, particularly in diagnostics and wearables, also open new niches for high-reliability and biocompatible ACA solutions. Finally, the growing demand for sustainable and lead-free electronic manufacturing processes aligns well with the inherent advantages of many ACA formulations, positioning them as a preferred choice for environmentally conscious industries.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of 5G Technology and IoT Devices | +1.5% | Global, particularly North America, Europe, Asia Pacific | 2025-2033 (Mid to Long-term) |

| Advancements in Micro-LED and Flexible Display Technologies | +1.3% | Asia Pacific (South Korea, China, Japan), North America | 2025-2033 (Mid to Long-term) |

| Increasing Use in Advanced Medical Devices and Wearables | +1.0% | North America, Europe, Asia Pacific | 2025-2033 (Long-term) |

| Development of Sustainable and Lead-Free Electronic Manufacturing | +0.8% | Europe, North America, Japan | 2025-2033 (Long-term) |

Anisotropic Conductive Adhesive Market Challenges Impact Analysis

The Anisotropic Conductive Adhesive market, while promising, must navigate several significant challenges that could hinder its full potential. One primary concern revolves around the long-term reliability and stability of ACA bonds, particularly under harsh environmental conditions such as extreme temperatures, high humidity, or mechanical stress. Ensuring consistent performance over the lifetime of a device, especially in critical applications like automotive or aerospace, requires continuous material innovation and rigorous testing protocols.

Another major challenge is the inherent complexity in optimizing the material properties of ACAs to meet diverse application requirements. Balancing electrical conductivity, mechanical strength, adhesion, and thermal performance while maintaining ease of processing can be a delicate act. Furthermore, scaling up the production of high-performance ACAs while maintaining quality and cost-effectiveness remains an ongoing hurdle. The need for specialized equipment and precise manufacturing controls also presents a barrier, especially for smaller players in the electronics assembly industry, impacting broader adoption.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring Long-Term Reliability Under Harsh Conditions | -0.9% | Global, particularly automotive, industrial, and military applications | 2025-2033 (Long-term) |

| Complexity in Material Formulation and Optimization | -0.7% | Global (R&D focused) | 2025-2033 (Long-term) |

| High Capital Investment for Specialized Manufacturing Equipment | -0.6% | Global (for new market entrants) | 2025-2033 (Mid-term) |

| Adherence to Evolving Environmental Regulations and Standards | -0.4% | Europe, North America, Japan | 2025-2033 (Long-term) |

Anisotropic Conductive Adhesive Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Anisotropic Conductive Adhesive (ACA) market, offering a detailed assessment of its current landscape, historical performance, and future growth projections. The scope includes a thorough examination of market size, trends, drivers, restraints, opportunities, and challenges influencing market dynamics globally. It further delves into the impact of emerging technologies like AI and 5G on the ACA sector, providing a holistic view for stakeholders.

The report meticulously segments the market by various critical parameters, including filler material type, adhesive type, application, and end-use industry, alongside a robust regional analysis. It aims to equip industry participants, investors, and policymakers with actionable insights to make informed strategic decisions. Furthermore, the report profiles key market players, offering competitive intelligence and a deeper understanding of the market's competitive intensity and strategic alliances.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.35 billion |

| Market Forecast in 2033 | USD 2.68 billion |

| Growth Rate | 8.9% CAGR |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Hitachi Chemical Co., Ltd. (now Showa Denko Materials), 3M Company, Henkel AG & Co. KGaA, Delo Industrie Klebstoffe GmbH & Co. KGaA, Kyocera Corporation, LG Chem, Lord Corporation (now Parker Hannifin), Shin-Etsu Chemical Co., Ltd., SEKISUI CHEMICAL CO., LTD., Dymax Corporation, Namics Corporation, Sunray Scientific, Creative Materials, Inc., Epoxy Technology, Inc., Panacol-Elring GmbH, Fujipoly, Dexerials Corporation, The Dow Chemical Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Anisotropic Conductive Adhesive (ACA) market is intricately segmented to provide a detailed understanding of its diverse components and their respective contributions to the overall market. This segmentation allows for a granular analysis of various product types, material compositions, and specific application areas, highlighting the nuances and growth drivers within each category. Understanding these segments is crucial for identifying key market niches, assessing competitive landscapes, and formulating targeted business strategies.

The market's segmentation by filler material, for instance, reveals how different conductive particles impact performance and cost, catering to distinct technological requirements. Similarly, segmenting by adhesive type (film vs. paste) showcases the preferred form factors for different manufacturing processes and assembly challenges. Application and end-use industry breakdowns further clarify where ACA technology is most impactful and where future growth opportunities lie, from high-volume consumer electronics to specialized medical or automotive applications, demonstrating the broad utility and adaptability of ACAs across modern industries.

- By Filler Material:

- Nickel (Ni)

- Gold (Au)

- Silver (Ag)

- Carbon

- Others (e.g., polymer beads with metallic coating)

- By Adhesive Type:

- Film Type (Anisotropic Conductive Film - ACF)

- Paste Type (Anisotropic Conductive Paste - ACP)

- By Application:

- Display (LCD, OLED, Micro-LED modules, driver IC bonding)

- IC Packaging (Flip Chip interconnection, COF/COG bonding)

- Automotive Electronics (ADAS sensors, infotainment systems, control units)

- Consumer Electronics (Smartphones, Tablets, Laptops, Wearables, Cameras)

- Medical Devices (Flexible circuits, sensors, diagnostic equipment)

- Others (Industrial automation, aerospace & defense, telecommunications infrastructure)

- By End-use Industry:

- Consumer Electronics

- Automotive

- Medical

- Industrial

- Telecommunications

- Others (e.g., Defence & Aerospace, IoT infrastructure)

Regional Highlights

The Anisotropic Conductive Adhesive (ACA) market exhibits distinct regional dynamics, influenced by local industrial growth, technological adoption rates, and manufacturing capabilities. Asia Pacific stands as the dominant region, primarily due to its robust electronics manufacturing base, encompassing major players in consumer electronics, display production, and semiconductor fabrication. Countries like China, South Korea, Japan, and Taiwan are at the forefront of driving demand for ACAs, fueled by high production volumes and continuous innovation in these sectors.

North America and Europe also represent significant markets, characterized by strong R&D activities, early adoption of advanced technologies, and a growing demand from the automotive, medical, and aerospace industries. These regions prioritize high-reliability and high-performance ACAs, often for more specialized and critical applications. Latin America, the Middle East, and Africa are emerging markets, showing gradual growth as their industrial and technological infrastructure develops, offering future potential for ACA market expansion.

- Asia Pacific: Dominant market share due to the presence of major electronics manufacturing hubs (China, South Korea, Japan, Taiwan), high production volumes of consumer electronics, displays, and semiconductors, and rapid adoption of advanced packaging technologies. Strong government support for electronics innovation further propels regional growth.

- North America: Significant market driven by robust R&D in advanced electronics, strong presence of automotive and medical device industries, and demand for high-performance and specialized ACA solutions. Focus on IoT, 5G, and high-reliability applications contributes to market value.

- Europe: Key market with substantial growth in automotive electronics (particularly ADAS and EV components), industrial automation, and high-end consumer electronics. Stringent environmental regulations also drive the adoption of lead-free ACA solutions.

- Latin America: Emerging market with increasing electronics manufacturing activities, particularly in Brazil and Mexico. Growing demand for consumer electronics and automotive components contributes to steady ACA market expansion.

- Middle East and Africa (MEA): Nascent market with potential driven by investments in telecommunications infrastructure, smart city projects, and gradual development of local electronics assembly.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Anisotropic Conductive Adhesive Market. These companies are at the forefront of material science innovation, developing advanced adhesive solutions that meet the demanding requirements of modern electronics manufacturing. Their strategic focus includes research and development of novel filler materials, polymer matrices, and processing techniques to enhance product performance, reliability, and cost-effectiveness. These key players continuously invest in improving properties such as conductivity, adhesion strength, thermal stability, and low-temperature curability to address evolving industry needs.

The competitive landscape is characterized by both global chemical giants and specialized adhesive manufacturers, each striving to gain market share through technological differentiation, strategic partnerships, and expanding global distribution networks. Key initiatives include developing ACAs for specific applications like flexible displays, 5G components, and advanced automotive sensors, as well as optimizing their production processes for scalability and sustainability. Understanding the strategies and product portfolios of these leading companies is crucial for comprehending the overall market dynamics and future growth trajectories within the Anisotropic Conductive Adhesive sector.

- Hitachi Chemical Co., Ltd. (now Showa Denko Materials)

- 3M Company

- Henkel AG & Co. KGaA

- Delo Industrie Klebstoffe GmbH & Co. KGaA

- Kyocera Corporation

- LG Chem

- Lord Corporation (now Parker Hannifin)

- Shin-Etsu Chemical Co., Ltd.

- SEKISUI CHEMICAL CO., LTD.

- Dymax Corporation

- Namics Corporation

- Sunray Scientific

- Creative Materials, Inc.

- Epoxy Technology, Inc.

- Panacol-Elring GmbH

- Fujipoly

- Dexerials Corporation

- The Dow Chemical Company

- Heraeus Holding GmbH

- M.G. Chemicals

Frequently Asked Questions

What is an Anisotropic Conductive Adhesive (ACA)?

An Anisotropic Conductive Adhesive (ACA) is a specialized adhesive material that provides electrical conductivity in one direction (typically Z-axis) while remaining electrically insulating in the other two directions (X-Y plane). It contains fine conductive particles dispersed in an adhesive matrix, which form electrical connections only when compressed between two contact points, making it ideal for fine-pitch interconnections in electronics.

How do ACAs differ from traditional soldering?

ACAs differ from soldering primarily in their mechanism and properties. Soldering creates a continuous metallic bond for electrical and mechanical connection, requiring high temperatures and often lead. ACAs provide selective electrical conductivity through compressed conductive particles at lower temperatures, are typically lead-free, and offer finer pitch capabilities and better flexibility, but generally have higher electrical resistance than solder.

What are the primary applications of Anisotropic Conductive Adhesives?

The primary applications of ACAs include bonding display driver ICs to LCD/OLED panels (Chip-on-Glass/Film), flip-chip interconnections in IC packaging, connecting flexible printed circuits (FPCs) to rigid PCBs, and various applications in compact electronic modules for consumer electronics, automotive systems, and medical devices where fine-pitch and low-temperature bonding are critical.

What are the key advantages of using ACAs in electronics manufacturing?

Key advantages of ACAs include fine-pitch capability, enabling miniaturization; low-temperature processing, protecting heat-sensitive components; lead-free compliance, aligning with environmental regulations; excellent adhesion for mechanical strength; and the ability to bond different material substrates, enhancing design flexibility. They simplify processes by combining bonding and interconnection into one step.

What is the future outlook for the Anisotropic Conductive Adhesive market?

The future outlook for the ACA market is highly positive, driven by continued growth in electronic device miniaturization, the expansion of flexible and wearable electronics, increasing adoption in automotive electronics (e.g., ADAS, EVs), and the proliferation of 5G and IoT devices. Ongoing R&D in material science will enhance ACA performance and expand their application range, supporting a robust CAGR through 2033.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted