Aluminum Casting Market

Aluminum Casting Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701375 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

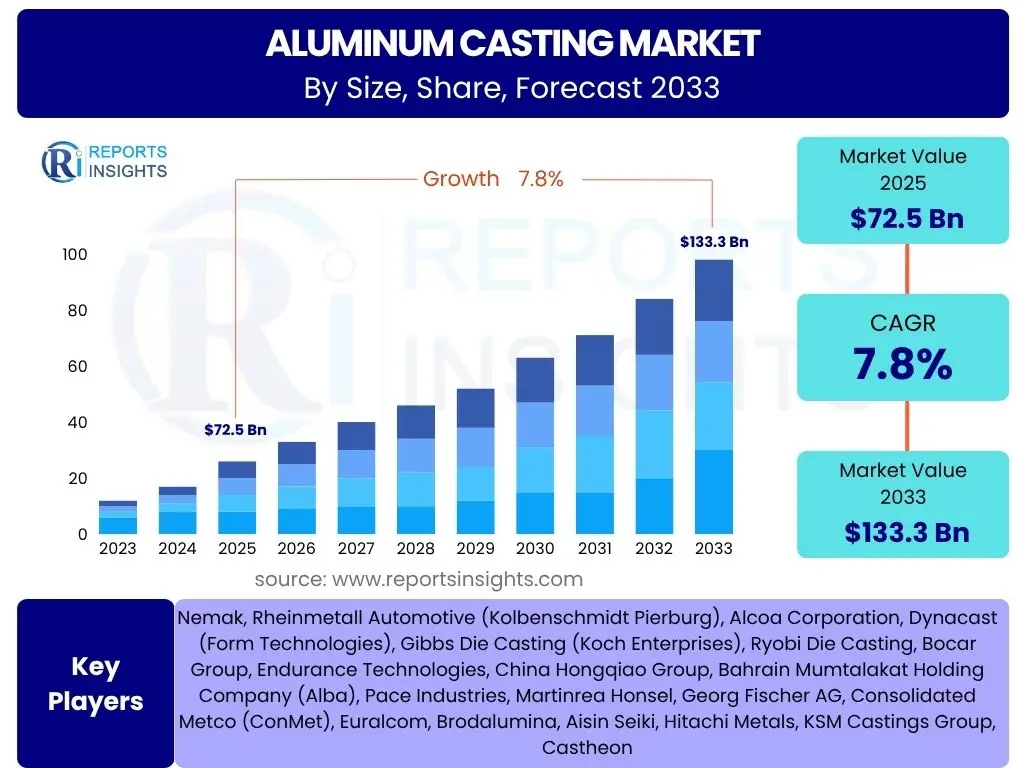

Aluminum Casting Market Size

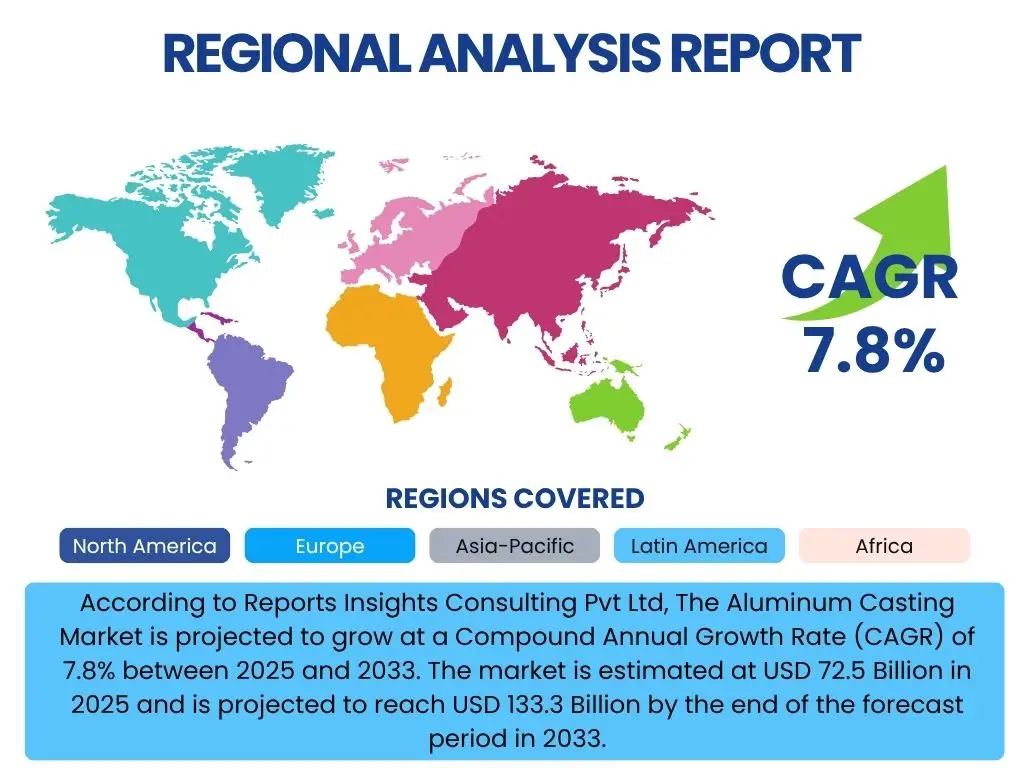

According to Reports Insights Consulting Pvt Ltd, The Aluminum Casting Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 72.5 Billion in 2025 and is projected to reach USD 133.3 Billion by the end of the forecast period in 2033.

Key Aluminum Casting Market Trends & Insights

The aluminum casting market is undergoing significant transformations driven by evolving industry demands and technological advancements. Key trends revolve around the increasing adoption of lightweight materials, particularly in the automotive and aerospace sectors, to enhance fuel efficiency and reduce emissions. Furthermore, the push towards electric vehicles (EVs) is creating new design and material requirements for battery housings, motor components, and structural parts, heavily relying on advanced aluminum casting techniques.

Technological innovations, including advancements in die-casting processes, simulation software, and robotic automation, are enabling manufacturers to produce more complex, high-precision, and defect-free components. Sustainability is another paramount trend, with a growing emphasis on using recycled aluminum and developing energy-efficient casting processes to meet stringent environmental regulations and corporate responsibility goals. This shift towards circular economy principles is influencing material sourcing and manufacturing practices across the industry.

- Lightweighting initiatives across automotive and aerospace sectors to improve fuel efficiency and reduce emissions.

- Increased demand from Electric Vehicle (EV) manufacturing for battery casings, motor housings, and structural components.

- Advancements in casting technologies such as high-pressure die casting (HPDC) and vacuum die casting for complex geometries.

- Growing adoption of automation and Industry 4.0 principles for improved process control, quality, and productivity.

- Strong emphasis on sustainable manufacturing practices, including increased use of recycled aluminum and energy-efficient processes.

AI Impact Analysis on Aluminum Casting

Artificial Intelligence (AI) is set to revolutionize the aluminum casting industry by enhancing efficiency, optimizing processes, and improving product quality. Users frequently inquire about how AI can mitigate common casting defects, streamline production cycles, and reduce material waste. The primary expectation is that AI will move the industry towards predictive manufacturing, allowing for proactive adjustments rather than reactive corrections.

AI's influence extends from the initial design phase through to post-production quality control. It enables more accurate simulation of casting processes, predicting material flow, solidification patterns, and potential defect formation with greater precision than traditional methods. This capability reduces the need for expensive physical prototypes and speeds up development cycles. Furthermore, AI-powered predictive maintenance systems can monitor equipment performance, forecasting potential failures before they occur, thereby minimizing downtime and extending machine lifespan. The integration of AI tools is anticipated to lead to significant cost reductions, improved consistency, and a more sustainable production footprint for aluminum casting operations.

- Process Optimization: AI algorithms analyze sensor data from casting machines to fine-tune parameters, leading to improved yield and energy efficiency.

- Predictive Maintenance: AI models predict equipment failures, enabling proactive maintenance, reducing downtime, and extending machinery lifespan.

- Quality Control and Defect Detection: Computer vision and machine learning identify casting defects in real-time, improving quality consistency and reducing scrap rates.

- Generative Design: AI assists in designing complex geometries and optimized part structures for lighter, stronger components.

- Supply Chain Optimization: AI enhances material procurement, inventory management, and logistics, reducing operational costs and improving responsiveness.

Key Takeaways Aluminum Casting Market Size & Forecast

The Aluminum Casting Market is poised for substantial growth, primarily driven by the escalating demand for lightweight, high-performance components across various end-use industries. A significant takeaway is the automotive sector's continuous evolution, particularly with the proliferation of Electric Vehicles (EVs), which heavily rely on aluminum castings for weight reduction and thermal management solutions. This trend underscores a pivotal shift from traditional internal combustion engine (ICE) components to new applications.

Another critical insight is the increasing emphasis on sustainable manufacturing practices and the circular economy. The market's future growth is intrinsically linked to the adoption of recycled aluminum, energy-efficient production methods, and the reduction of carbon footprints. Geographically, Asia Pacific is expected to remain the largest and fastest-growing region, fueled by rapid industrialization and expanding automotive production. The ongoing technological advancements, including advanced die-casting techniques and the integration of AI, will further bolster market expansion and redefine production capabilities, making the industry more resilient and efficient.

- Robust growth forecast driven by automotive lightweighting and Electric Vehicle (EV) adoption.

- Increasing integration of advanced casting technologies and automation for enhanced precision and efficiency.

- Significant focus on sustainability, promoting the use of recycled aluminum and eco-friendly manufacturing processes.

- Asia Pacific remains a dominant and high-growth region due to strong industrial and automotive sector expansion.

- Continuous innovation in alloy development and casting techniques to meet stringent performance and weight requirements.

Aluminum Casting Market Drivers Analysis

The Aluminum Casting Market is propelled by several robust drivers, primarily the global imperative for lightweighting across critical industries. In the automotive sector, stringent emission regulations and the increasing adoption of electric vehicles necessitate lighter components to enhance fuel efficiency, extend battery range, and improve overall performance. Aluminum castings, with their superior strength-to-weight ratio, are ideally suited for these applications, leading to higher demand for structural parts, engine blocks, and transmission housings.

Beyond automotive, the aerospace and defense industries are also significant drivers, requiring high-performance, lightweight materials for aircraft components to reduce fuel consumption and increase payload capacity. The expanding electrical and electronics sector further contributes to market growth, with aluminum castings used in heat sinks, enclosures, and various electronic housings due to their excellent thermal conductivity and EMI shielding properties. These diverse industrial applications, coupled with continuous advancements in casting technologies, collectively underpin the market's positive trajectory.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Automotive Lightweighting & EV Adoption | +2.5% | Global | Short-Mid Term (2025-2029) |

| Growth in Aerospace & Defense Industry | +1.8% | North America, Europe | Mid-Long Term (2028-2033) |

| Increasing Demand from Electrical & Electronics | +1.2% | Asia Pacific, Europe | Short-Mid Term (2025-2030) |

| Advancements in Casting Technologies | +0.9% | Global | Mid Term (2027-2032) |

Aluminum Casting Market Restraints Analysis

Despite significant growth potential, the Aluminum Casting Market faces several restraints that could impede its expansion. One major challenge is the volatility of raw material prices, particularly aluminum, which is influenced by global supply-demand dynamics, geopolitical factors, and energy costs. Fluctuating prices can significantly impact manufacturing costs and profit margins for casting companies, leading to uncertainty in market planning and investment decisions.

Another notable restraint is the increasing stringency of environmental regulations. Governments worldwide are imposing stricter rules on industrial emissions, waste management, and energy consumption, compelling foundries to invest in expensive pollution control technologies and sustainable practices. While beneficial for the environment, these compliance costs can increase operational expenses and act as a barrier to entry for new players, particularly in regions with mature regulatory frameworks. Furthermore, the high initial capital investment required for advanced casting equipment and facilities can deter new entrants and limit expansion capabilities for smaller and medium-sized enterprises.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility of Raw Material (Aluminum) Prices | -1.5% | Global | Short-Term (2025-2027) |

| Stringent Environmental Regulations | -1.0% | Europe, North America | Mid-Long Term (2028-2033) |

| High Capital Investment Requirements | -0.8% | Emerging Markets | Long-Term (2030-2033) |

| Competition from Alternative Materials (e.g., Composites, Steel) | -0.7% | Global | Mid-Term (2027-2030) |

Aluminum Casting Market Opportunities Analysis

The Aluminum Casting Market is presented with numerous opportunities for growth, particularly stemming from the rapid expansion of the Electric Vehicle (EV) sector. EVs require a substantial number of aluminum castings for battery housings, motor parts, and lightweight structural components, offering a burgeoning avenue for market expansion. As global EV production scales, so too will the demand for specialized aluminum casting solutions, driving innovation in design and manufacturing processes.

Another significant opportunity lies in the increasing emphasis on sustainable and circular economy practices. Foundries that invest in advanced recycling technologies and energy-efficient production methods can gain a competitive edge by meeting corporate sustainability goals and adhering to evolving environmental standards. Furthermore, the burgeoning industrialization and infrastructure development in emerging economies, especially across Asia Pacific and Latin America, present untapped markets for diverse aluminum casting applications in construction, machinery, and consumer goods. The continuous evolution of additive manufacturing and hybrid casting processes also offers opportunities for creating highly complex, customized components more efficiently.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Growth of Electric Vehicle (EV) Production | +2.0% | Global | Long-Term (2029-2033) |

| Increasing Focus on Recycling and Sustainable Practices | +1.5% | Europe, North America | Mid-Long Term (2028-2033) |

| Expansion in Emerging Markets & Industrialization | +1.0% | Asia Pacific, Latin America | Mid-Long Term (2027-2033) |

| Integration of Additive Manufacturing & Hybrid Casting | +0.7% | North America, Europe | Long-Term (2030-2033) |

Aluminum Casting Market Challenges Impact Analysis

The Aluminum Casting Market faces several operational and strategic challenges that require proactive management for sustained growth. A notable challenge is the persistent shortage of skilled labor, particularly technicians and engineers proficient in advanced casting processes, automation, and quality control. This deficit can lead to production bottlenecks, increased training costs, and slower adoption of new technologies, impacting overall operational efficiency and the ability to scale production effectively.

Another significant challenge is the ongoing fluctuation in energy costs, which directly impacts the energy-intensive casting processes. Rising energy prices can erode profit margins, especially for foundries heavily reliant on traditional energy sources, and necessitate significant investment in energy-efficient technologies. Furthermore, global supply chain disruptions, as witnessed in recent years, pose a challenge by affecting the timely availability of raw materials and components, leading to production delays and increased logistical costs. Ensuring consistent quality and minimizing defect rates in complex aluminum castings also remains an inherent challenge that demands continuous innovation in process control and inspection technologies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Skilled Labor Shortage | -1.2% | North America, Europe | Mid-Term (2027-2031) |

| Fluctuations in Energy Costs | -0.9% | Europe, Asia Pacific | Short-Mid Term (2025-2028) |

| Global Supply Chain Disruptions | -0.7% | Global | Short-Term (2025-2026) |

| Maintaining High Quality & Defect Reduction | -0.5% | Global | Ongoing |

Aluminum Casting Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Aluminum Casting Market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. The scope encompasses a thorough examination of market size and forecast from 2025 to 2033, covering key growth drivers, restraints, opportunities, and challenges. It also highlights the impact of emerging technologies and sustainability initiatives shaping the industry's future trajectory.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 72.5 Billion |

| Market Forecast in 2033 | USD 133.3 Billion |

| Growth Rate | 7.8% |

| Number of Pages | 255 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Nemak, Rheinmetall Automotive (Kolbenschmidt Pierburg), Alcoa Corporation, Dynacast (Form Technologies), Gibbs Die Casting (Koch Enterprises), Ryobi Die Casting, Bocar Group, Endurance Technologies, China Hongqiao Group, Bahrain Mumtalakat Holding Company (Alba), Pace Industries, Martinrea Honsel, Georg Fischer AG, Consolidated Metco (ConMet), Euralcom, Brodalumina, Aisin Seiki, Hitachi Metals, KSM Castings Group, Castheon |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Aluminum Casting Market is comprehensively segmented by process type and end-use industry to provide a granular view of its dynamics and growth prospects. This segmentation allows for a detailed understanding of how different manufacturing techniques and industry applications contribute to the overall market landscape. Analyzing these segments helps stakeholders identify key growth areas, understand technological adoption patterns, and pinpoint emerging opportunities within specific market niches.

The segmentation by process illuminates the prevalence and growth rates of various casting methods, such as high-pressure die casting, which is favored for high-volume, thin-walled components, versus sand casting, often used for larger, less intricate parts. Concurrently, the end-use industry segmentation highlights the market's reliance on sectors like automotive and aerospace, which demand lightweight and high-strength components, while also identifying emerging demand from electrical and electronics, and building and construction industries. This multi-dimensional analysis provides a robust framework for strategic decision-making and market forecasting.

- By Process:

- High Pressure Die Casting (HPDC)

- Low Pressure Die Casting (LPDC)

- Gravity Die Casting (GDC)

- Sand Casting

- Others (e.g., Investment Casting, Lost Foam Casting)

- By End-Use Industry:

- Automotive

- Passenger Vehicles

- Commercial Vehicles

- Electric Vehicles

- Aerospace & Defense

- Industrial (Machinery, Heavy Equipment)

- Electrical & Electronics

- Building & Construction

- Marine

- Others

- Automotive

Regional Highlights

- North America: This region demonstrates mature market characteristics, driven by robust automotive and aerospace sectors. The increasing focus on electric vehicle manufacturing and advanced manufacturing technologies, coupled with stringent fuel efficiency standards, propels the demand for lightweight aluminum castings. Significant investments in R&D and automation define this market.

- Europe: Characterized by stringent environmental regulations and a strong emphasis on sustainability, Europe leads in the adoption of advanced casting technologies and recycled aluminum. The region's prominent automotive industry, coupled with growth in industrial machinery and renewable energy sectors, fuels the demand for high-quality, lightweight aluminum components.

- Asia Pacific (APAC): The largest and fastest-growing market for aluminum casting, APAC's expansion is primarily driven by rapid industrialization, burgeoning automotive production (especially in China and India), and expanding electronics manufacturing. Favorable government policies, lower manufacturing costs, and increasing disposable incomes contribute to the region's dominance.

- Latin America: This region is an emerging market with significant growth potential, particularly in the automotive and industrial sectors. Investments in manufacturing capabilities and improving economic conditions are expected to drive the demand for aluminum castings, albeit at a slower pace compared to APAC.

- Middle East and Africa (MEA): The MEA region is witnessing growth spurred by infrastructure development projects, increasing automotive assembly plants, and diversification efforts away from oil-dependent economies. While smaller in market share, the long-term outlook is positive due to ongoing industrialization and urbanization.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aluminum Casting Market.- Nemak

- Rheinmetall Automotive (Kolbenschmidt Pierburg)

- Alcoa Corporation

- Dynacast (Form Technologies)

- Gibbs Die Casting (Koch Enterprises)

- Ryobi Die Casting

- Bocar Group

- Endurance Technologies

- China Hongqiao Group

- Bahrain Mumtalakat Holding Company (Alba)

- Pace Industries

- Martinrea Honsel

- Georg Fischer AG

- Consolidated Metco (ConMet)

- Euralcom

- Brodalumina

- Aisin Seiki

- Hitachi Metals

- KSM Castings Group

- Castheon

Frequently Asked Questions

What is aluminum casting and its primary advantage?

Aluminum casting is a manufacturing process where molten aluminum is poured into a mold cavity to create specific shapes or parts. Its primary advantage lies in producing lightweight components with excellent strength-to-weight ratios, high thermal conductivity, and good corrosion resistance, making it ideal for various industrial applications.

Which industries primarily utilize aluminum castings?

Aluminum castings are extensively used across several key industries, most notably the automotive sector for engine blocks, chassis components, and EV battery housings. Other major users include aerospace and defense for aircraft parts, electrical and electronics for heat sinks and enclosures, and the industrial sector for machinery components.

How do environmental regulations affect the aluminum casting market?

Environmental regulations significantly influence the aluminum casting market by driving demand for sustainable practices. This includes promoting the use of recycled aluminum, investing in energy-efficient technologies, and implementing stricter controls on emissions and waste, leading to higher operational costs but also fostering innovation in green casting processes.

What role does lightweighting play in the demand for aluminum castings?

Lightweighting is a critical driver for aluminum casting demand. Industries like automotive and aerospace seek lighter materials to improve fuel efficiency, reduce emissions, and enhance performance. Aluminum castings offer an optimal solution by reducing vehicle weight without compromising structural integrity or safety, directly contributing to these efficiency goals.

What impact will electric vehicles have on the aluminum casting market?

Electric vehicles (EVs) are expected to have a profoundly positive impact on the aluminum casting market. EVs require numerous lightweight aluminum components for battery enclosures, motor housings, and structural parts to offset battery weight and extend range, creating significant new demand avenues for advanced aluminum casting solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted