Aluminum Alloy Extrusion Profile Market

Aluminum Alloy Extrusion Profile Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703800 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

Aluminum Alloy Extrusion Profile Market Size

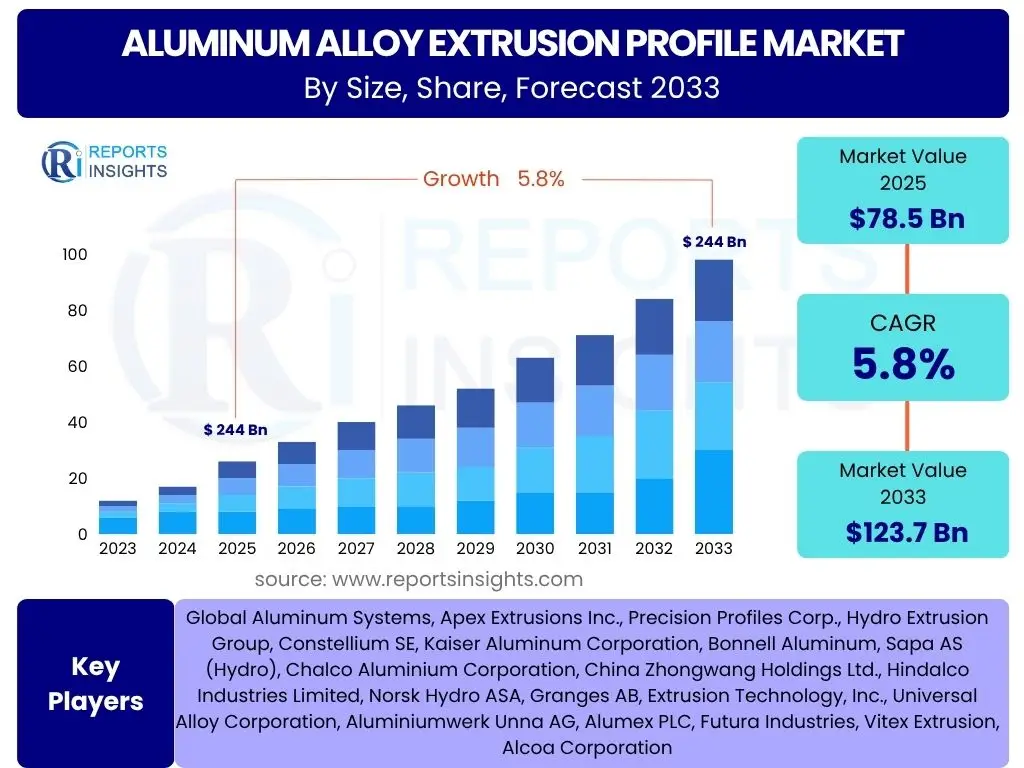

According to Reports Insights Consulting Pvt Ltd, The Aluminum Alloy Extrusion Profile Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 78.5 billion in 2025 and is projected to reach USD 123.7 billion by the end of the forecast period in 2033.

Key Aluminum Alloy Extrusion Profile Market Trends & Insights

The aluminum alloy extrusion profile market is undergoing significant transformation driven by evolving industrial demands and technological advancements. Market queries frequently center on the adoption of sustainable practices, the impact of lightweighting in automotive and aerospace sectors, and the increasing integration of smart manufacturing processes. Users are keenly interested in how these trends are shaping material innovation, product design, and overall market dynamics, particularly concerning energy efficiency and performance optimization. The ongoing shift towards renewable energy infrastructure and electric vehicles further underscores the market's dynamic landscape, demanding new specifications for strength-to-weight ratios and design flexibility.

Another area of intense interest revolves around the customization and specialized applications of aluminum extrusions. As industries such as construction, electronics, and medical devices require increasingly precise and complex profiles, the market is seeing a surge in demand for bespoke solutions. This trend is supported by advancements in extrusion technologies, including advanced die design and precision tooling, enabling manufacturers to produce intricate shapes with tight tolerances. Furthermore, the push for circular economy principles is fostering greater adoption of recycled aluminum, influencing sourcing strategies and manufacturing processes across the supply chain.

- Growing demand for lightweight materials in automotive and aerospace.

- Increasing adoption in renewable energy infrastructure (solar panel frames, wind turbine components).

- Technological advancements in extrusion processes for complex profiles.

- Emphasis on sustainable production and use of recycled aluminum.

- Expansion of applications in building and construction for green buildings.

AI Impact Analysis on Aluminum Alloy Extrusion Profile

Common user questions regarding AI's impact on the aluminum alloy extrusion profile sector reveal a keen interest in enhanced operational efficiency, predictive maintenance, and quality control. Stakeholders are exploring how artificial intelligence can optimize extrusion parameters, reduce material waste, and improve product consistency, thereby addressing critical manufacturing challenges. There is also significant curiosity about AI's role in accelerating new product development, particularly in simulating complex profile designs and predicting material performance under various conditions, which can drastically cut down R&D cycles and costs.

Moreover, the integration of AI is expected to revolutionize supply chain management within the industry. User inquiries frequently highlight the potential for AI to optimize inventory levels, forecast demand more accurately, and streamline logistics, leading to more resilient and responsive supply chains. Beyond operational aspects, AI also holds promise for advanced data analytics, offering insights into market trends, customer preferences, and competitive intelligence, enabling businesses to make more informed strategic decisions and identify new growth opportunities in a rapidly evolving market landscape.

- Optimization of extrusion processes through machine learning algorithms.

- Predictive maintenance for machinery, reducing downtime and operational costs.

- Enhanced quality control and defect detection using AI-powered vision systems.

- Accelerated design and prototyping through AI-driven simulation.

- Improved supply chain efficiency and demand forecasting.

Key Takeaways Aluminum Alloy Extrusion Profile Market Size & Forecast

The analysis of common user questions about the aluminum alloy extrusion profile market size and forecast highlights several critical insights. Users are primarily concerned with the consistent growth trajectory driven by broad industrial applications, emphasizing its indispensable role in modern infrastructure and technological advancements. The forecast indicates robust expansion, largely attributable to increasing urbanization, the global push for sustainable solutions, and the ongoing shift towards lightweight materials in key end-use sectors. These trends collectively underscore the market's resilience and its potential for sustained long-term value creation.

Furthermore, inquiries often delve into the specific regional contributions to market growth, with particular attention paid to emerging economies in Asia Pacific and the evolving regulatory landscapes in North America and Europe. The competitive dynamics, including the emergence of new technologies and production methodologies, also frequently surface in user questions, indicating a strong interest in understanding how market players are adapting to these changes. The overall sentiment suggests a market characterized by continuous innovation and adaptation to meet diverse and stringent industrial requirements.

- Market poised for substantial growth driven by diverse industrial applications.

- Significant opportunities in sustainable construction and electric vehicle manufacturing.

- Technological innovation is key to maintaining competitive edge.

- Asia Pacific remains a dominant and high-growth region.

- Focus on recycling and green manufacturing processes is increasing.

Aluminum Alloy Extrusion Profile Market Drivers Analysis

The increasing demand for lightweight and high-strength materials across various industries stands as a primary driver for the aluminum alloy extrusion profile market. Industries such as automotive, aerospace, and transportation are continually seeking solutions to reduce vehicle weight, improve fuel efficiency, and enhance structural integrity. Aluminum extrusions offer an exceptional strength-to-weight ratio, making them an ideal choice for these applications. The shift towards electric vehicles (EVs) further amplifies this demand, as lightweight components are crucial for extending battery range and improving overall performance, positioning aluminum extrusions as a fundamental material in the EV revolution.

Moreover, the booming construction sector, particularly in emerging economies and the global focus on green building initiatives, significantly propels market growth. Aluminum extrusions are extensively used in windows, doors, curtain walls, facades, and structural components due to their durability, corrosion resistance, aesthetic versatility, and recyclability. The emphasis on sustainable and energy-efficient building practices encourages the adoption of aluminum profiles, as they contribute to LEED certifications and other environmental standards. Urbanization and infrastructure development projects worldwide continue to create a robust demand base for these versatile profiles.

Additionally, the renewable energy sector, encompassing solar and wind power installations, presents a substantial growth impetus. Aluminum extrusions are integral to solar panel frames, mounting structures, and components for wind turbines due to their excellent weather resistance and structural stability. The global commitment to reducing carbon emissions and transitioning to clean energy sources ensures a sustained demand for aluminum profiles in this expanding sector. Furthermore, the electrical and electronics industries, along with consumer goods, leverage aluminum extrusions for their thermal management properties, design flexibility, and sleek aesthetics, solidifying their market position across diverse applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Automotive & EV Sector Demand | +1.5% | North America, Europe, Asia Pacific | 2025-2033 |

| Rapid Urbanization & Construction Growth | +1.2% | Asia Pacific, Middle East & Africa | 2025-2033 |

| Expansion of Renewable Energy Sector | +1.0% | Europe, Asia Pacific, North America | 2025-2033 |

| Emphasis on Lightweighting and Fuel Efficiency | +0.8% | Global | 2025-2033 |

| Technological Advancements in Extrusion | +0.6% | Global | 2025-2033 |

Aluminum Alloy Extrusion Profile Market Restraints Analysis

One significant restraint impacting the aluminum alloy extrusion profile market is the volatility in raw material prices, particularly aluminum ingots. The global aluminum market is subject to fluctuations driven by supply-demand dynamics, geopolitical tensions, energy costs, and trade policies. This price instability directly affects the production costs for manufacturers of extrusion profiles, making it challenging to maintain stable profit margins and predict long-term pricing strategies. Such unpredictability can deter new investments and complicate procurement processes for downstream industries, thereby slowing market expansion in certain segments.

Another notable restraint is the high initial capital investment required for establishing and upgrading extrusion facilities. The sophisticated machinery, specialized tooling, and advanced technological infrastructure necessary for producing high-quality and complex aluminum profiles represent a substantial upfront cost. This barrier to entry limits the participation of new players and can restrict the expansion capacity of existing small and medium-sized enterprises. Furthermore, the need for continuous investment in research and development to keep pace with evolving material science and process innovations adds to the financial burden, potentially slowing down overall market growth.

Intense competition from substitute materials, such as steel, plastics, and composites, also poses a significant challenge to the aluminum alloy extrusion market. While aluminum offers distinct advantages in specific applications, other materials may provide comparable performance at lower costs or possess unique properties that are preferred for certain end-uses. For instance, in some structural applications, steel might be chosen for its higher tensile strength, while advanced composites are increasingly favored in aerospace for their even lighter weight. Manufacturers must continuously innovate and emphasize the unique benefits of aluminum, such as recyclability and design versatility, to maintain their competitive edge against these alternative materials and prevent market share erosion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatility in Raw Material Prices | -1.1% | Global | Short-to-Medium Term |

| High Initial Capital Investment | -0.8% | Global, particularly Emerging Economies | Long Term |

| Competition from Substitute Materials | -0.7% | Global | 2025-2033 |

| Stringent Environmental Regulations | -0.5% | Europe, North America | 2025-2033 |

| Skilled Labor Shortage | -0.4% | Developed Economies | Medium Term |

Aluminum Alloy Extrusion Profile Market Opportunities Analysis

The escalating global focus on sustainability and circular economy principles presents a significant opportunity for the aluminum alloy extrusion profile market. Aluminum is highly recyclable without losing its intrinsic properties, making it a preferred material for environmentally conscious industries. The increasing adoption of recycled aluminum (secondary aluminum) in extrusion processes not only reduces the carbon footprint associated with primary aluminum production but also offers cost advantages. Manufacturers can leverage this attribute to appeal to green building initiatives, sustainable automotive design, and eco-friendly consumer products, positioning themselves as leaders in responsible manufacturing and meeting growing consumer and regulatory demands for sustainable materials.

Technological advancements in extrusion processes and alloys are continuously opening new avenues for market expansion. Innovations in die design, such as porthole and multi-hole dies, enable the production of more complex, intricate, and precise profiles with thinner walls and tighter tolerances. This capability allows aluminum extrusions to penetrate new high-value applications in sectors like aerospace, medical devices, and high-performance electronics, where precision and specific material properties are critical. Furthermore, the development of new aluminum alloys with enhanced strength, corrosion resistance, or thermal conductivity characteristics broadens the scope of applications and improves product performance, addressing previously unmet industrial needs.

The expansion into emerging markets, particularly in Asia Pacific, Latin America, and parts of Africa, represents another substantial opportunity. Rapid urbanization, industrialization, and infrastructure development in these regions are driving massive construction activities and increasing demand across various end-use sectors, including automotive, transportation, and consumer goods. As these economies grow, the demand for high-performance and lightweight materials like aluminum extrusions is expected to surge. Establishing local production capabilities, developing robust distribution networks, and tailoring product offerings to meet regional specificities can enable market players to capitalize on these burgeoning opportunities and secure long-term growth.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increased Focus on Sustainable & Recyclable Materials | +1.3% | Global | Long Term |

| Advancements in Extrusion Technology & Alloys | +1.0% | Global | 2025-2033 |

| Expansion into Emerging Markets & Industrialization | +0.9% | Asia Pacific, Latin America, MEA | 2025-2033 |

| Growth in Niche Applications (Aerospace, Medical) | +0.7% | North America, Europe | Long Term |

| Smart City Development & Infrastructure Upgrades | +0.6% | Global | 2025-2033 |

Aluminum Alloy Extrusion Profile Market Challenges Impact Analysis

One of the persistent challenges in the aluminum alloy extrusion profile market is managing the high and fluctuating energy costs associated with the extrusion process. Aluminum production, including primary smelting and subsequent extrusion, is energy-intensive. Variations in electricity and natural gas prices directly impact operational expenses, putting pressure on manufacturers' profit margins, especially in regions with volatile energy markets. This challenge necessitates continuous investment in energy-efficient technologies and process optimization to maintain cost competitiveness, potentially diverting capital from other growth initiatives.

The industry also faces a significant challenge in the form of intense global competition and overcapacity in certain regions. The proliferation of extrusion facilities, particularly in Asia, has led to a highly competitive landscape where pricing pressures and market share battles are common. This competitive intensity can erode profit margins, especially for manufacturers without strong differentiation or specialized product portfolios. Companies must continuously innovate, optimize production processes, and focus on value-added services or niche markets to stand out in a crowded market and avoid commoditization.

Maintaining consistent product quality and adhering to stringent industry standards across diverse applications presents another complex challenge. Aluminum extrusions are used in critical sectors like automotive and aerospace where safety and performance are paramount, requiring precise dimensional tolerances, surface finishes, and mechanical properties. Achieving and sustaining these high-quality standards across various alloys and complex profiles demands advanced manufacturing processes, rigorous quality control systems, and a highly skilled workforce. Any deviation can lead to product recalls, reputational damage, and financial losses, making quality assurance a continuous and demanding endeavor for market participants.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High & Volatile Energy Costs | -0.9% | Global | Short-to-Medium Term |

| Intense Competition & Overcapacity | -0.8% | Asia Pacific, Europe | Long Term |

| Adherence to Stringent Quality Standards | -0.7% | Global | Ongoing |

| Supply Chain Disruptions | -0.6% | Global | Short-to-Medium Term |

| Innovation & R&D Investment Burden | -0.5% | Global | Long Term |

Aluminum Alloy Extrusion Profile Market - Updated Report Scope

This report offers a comprehensive analysis of the global aluminum alloy extrusion profile market, providing insights into its current size, historical trends, and future growth projections. It delineates key market segments, regional dynamics, competitive landscape, and the impact of significant drivers, restraints, opportunities, and challenges. The study aims to equip stakeholders with actionable intelligence to navigate market complexities and identify strategic growth avenues over the forecast period.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 78.5 billion |

| Market Forecast in 2033 | USD 123.7 billion |

| Growth Rate | 5.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Aluminum Systems, Apex Extrusions Inc., Precision Profiles Corp., Hydro Extrusion Group, Constellium SE, Kaiser Aluminum Corporation, Bonnell Aluminum, Sapa AS (Hydro), Chalco Aluminium Corporation, China Zhongwang Holdings Ltd., Hindalco Industries Limited, Norsk Hydro ASA, Granges AB, Extrusion Technology, Inc., Universal Alloy Corporation, Aluminiumwerk Unna AG, Alumex PLC, Futura Industries, Vitex Extrusion, Alcoa Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The aluminum alloy extrusion profile market is comprehensively segmented to provide granular insights into its diverse applications and material compositions. This segmentation highlights the specific characteristics and end-use requirements that drive demand across various industries. Understanding these distinct segments is crucial for identifying targeted growth strategies and product development opportunities, as each segment responds to unique market forces and technological imperatives.

The market is primarily analyzed by alloy type, end-use industry, and form, reflecting the multifaceted nature of aluminum extrusions. Alloy types, such as 6000 series (magnesium-silicon alloy), are particularly dominant due to their excellent balance of strength, formability, weldability, and corrosion resistance, making them ideal for architectural and structural applications. The diverse end-use industries ranging from construction to aerospace underscore the material's versatility, while the classification by form (solid, hollow, semi-hollow, complex) illustrates the manufacturing capabilities and design flexibility inherent in the extrusion process, catering to increasingly complex geometric requirements.

- By Alloy Type:

- 1000 Series (Pure Aluminum): Known for excellent corrosion resistance and electrical conductivity.

- 2000 Series (Copper Alloy): High strength, used in aerospace.

- 3000 Series (Manganese Alloy): Moderate strength, good workability, corrosion resistance.

- 5000 Series (Magnesium Alloy): Excellent corrosion resistance, good weldability, marine applications.

- 6000 Series (Magnesium-Silicon Alloy): Most common, good strength, formability, weldability; widely used in construction, automotive.

- 7000 Series (Zinc Alloy): Highest strength, used in high-stress applications.

- By End-Use Industry:

- Building & Construction: Windows, doors, facades, structural components.

- Automotive & Transportation: Chassis, body structures, battery enclosures for EVs.

- Industrial & Engineering: Machinery parts, heat sinks, fluid power components.

- Electrical & Electronics: Conduits, heat dissipaters, electronic enclosures.

- Consumer Goods: Furniture, appliances, sporting equipment.

- Machinery & Equipment: Industrial frames, conveyor systems.

- Solar & Renewable Energy: Solar panel frames, wind turbine parts.

- Aerospace & Defense: Aircraft structural components, missile parts.

- By Form:

- Solid: Uniform cross-section, often used for structural applications.

- Hollow: Enclosed void, used for lightweight structures, conduits.

- Semi-Hollow: Partially enclosed void, combines benefits of solid and hollow.

- Complex: Intricate designs, often multi-void or highly customized profiles.

Regional Highlights

- Asia Pacific: This region dominates the global aluminum alloy extrusion profile market, driven by rapid urbanization, significant infrastructure development, and booming construction activities, particularly in China and India. The expansive automotive industry, coupled with increasing investments in renewable energy and electronics manufacturing, further fuels demand. Governments' focus on smart cities and sustainable development initiatives also contributes to the market's robust growth in this region.

- Europe: Characterized by stringent environmental regulations and a strong emphasis on sustainability, Europe is a mature yet growing market. The region's automotive sector, especially the push for electric vehicles, drives demand for lightweight aluminum extrusions. Additionally, the well-established construction industry and the adoption of advanced manufacturing technologies contribute significantly to market expansion, with Germany, France, and the UK leading the way.

- North America: The market in North America is propelled by innovation in the automotive and aerospace sectors, focusing on lightweighting and fuel efficiency. Investment in commercial and residential construction, along with growing applications in industrial machinery and electrical components, supports steady growth. The region's technological advancements and demand for high-performance materials continue to be key drivers.

- Latin America: This region presents emerging opportunities, with Brazil and Mexico at the forefront of growth due to expanding construction activities and industrial development. Investments in infrastructure and manufacturing sectors are gradually increasing the adoption of aluminum extrusion profiles, though market maturity is still lower compared to developed regions.

- Middle East & Africa (MEA): The MEA region is experiencing substantial growth, primarily fueled by massive construction projects, particularly in the GCC countries (e.g., UAE, Saudi Arabia) as part of economic diversification efforts. Renewable energy projects and industrial expansion also contribute to the increasing demand for aluminum extrusions in this dynamic market.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aluminum Alloy Extrusion Profile Market.- Global Aluminum Systems

- Apex Extrusions Inc.

- Precision Profiles Corp.

- Hydro Extrusion Group

- Constellium SE

- Kaiser Aluminum Corporation

- Bonnell Aluminum

- Sapa AS (Hydro)

- Chalco Aluminium Corporation

- China Zhongwang Holdings Ltd.

- Hindalco Industries Limited

- Norsk Hydro ASA

- Granges AB

- Extrusion Technology, Inc.

- Universal Alloy Corporation

- Aluminiumwerk Unna AG

- Alumex PLC

- Futura Industries

- Vitex Extrusion

Frequently Asked Questions

Analyze common user questions about the Aluminum Alloy Extrusion Profile market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current market size of the Aluminum Alloy Extrusion Profile market?

The Aluminum Alloy Extrusion Profile Market is estimated at USD 78.5 billion in 2025. This valuation reflects the widespread adoption of these profiles across various industries, driven by their unique properties such as lightweight, strength, and recyclability. The market's sizeis a testament to its critical role in modern industrial and architectural applications, serving sectors from construction to advanced transportation.

What are the primary growth drivers for the Aluminum Alloy Extrusion Profile market?

Key growth drivers include the increasing demand for lightweight materials in the automotive industry, particularly for electric vehicles, and the robust growth in the construction sector fueled by urbanization and green building initiatives. Furthermore, the expansion of the renewable energy sector, demanding structural components for solar panels and wind turbines, significantly contributes to market expansion. Technological advancements in extrusion processes also enable new applications.

Which end-use industries are the largest consumers of Aluminum Alloy Extrusion Profiles?

The largest consumers of Aluminum Alloy Extrusion Profiles are primarily the Building & Construction industry, where they are used extensively for windows, doors, facades, and structural elements. The Automotive & Transportation sector also represents a significant segment, with profiles used in vehicle chassis, body structures, and battery enclosures. Other key industries include industrial and engineering applications, electrical and electronics, and the rapidly growing solar and renewable energy sector.

How do sustainability trends impact the Aluminum Alloy Extrusion Profile market?

Sustainability trends profoundly impact the market by driving demand for recycled aluminum and promoting energy-efficient manufacturing processes. Aluminum's high recyclability positions extrusion profiles as a preferred material for environmentally conscious projects and products. This emphasis on circular economy principles not only reduces the carbon footprint but also presents cost advantages and enhances the market's appeal to eco-friendly consumers and regulations.

What are the key challenges facing the Aluminum Alloy Extrusion Profile market?

The market faces several challenges, including the volatility of raw material prices and high, fluctuating energy costs, which directly impact production expenses and profit margins. Intense global competition and potential overcapacity in certain regions also exert pricing pressures. Additionally, the industry must continuously invest in innovation and adhere to stringent quality standards to meet the evolving demands of critical end-use applications, posing an ongoing challenge for manufacturers.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted