Aircraft Positioning Systems Market

Aircraft Positioning Systems Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678218 | Last Updated : July 18, 2025 |

Format : ![]()

![]()

![]()

![]()

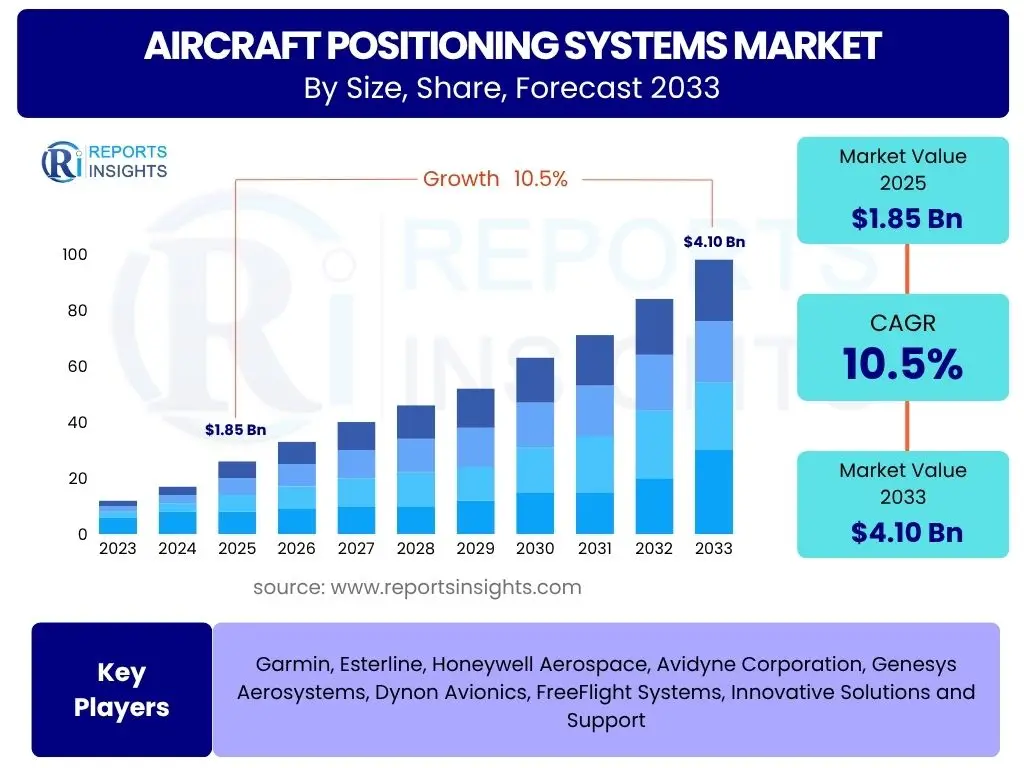

Aircraft Positioning Systems Market is projected to grow at a Compound annual growth rate (CAGR) of 10.5% between 2025 and 2033, reaching USD 1.85 Billion in 2025 and is projected to grow by USD 4.10 Billion by 2033 the end of the forecast period. This significant growth trajectory is underpinned by the increasing global demand for enhanced air traffic management, stringent aviation safety regulations, and continuous technological advancements in navigation and surveillance systems. The market's expansion is further fueled by the rising proliferation of commercial aircraft fleets and the burgeoning integration of unmanned aerial vehicles (UAVs) into diverse applications, necessitating precise and reliable positioning capabilities across all flight phases. As airspaces become more congested and operational efficiency gains paramount importance, the adoption of sophisticated aircraft positioning systems becomes indispensable for ensuring safe and streamlined air travel, driving sustained investment and innovation within this critical sector.

Key Aircraft Positioning Systems Market Trends & Insights

The Aircraft Positioning Systems Market is undergoing a transformative period, driven by a confluence of technological advancements and evolving operational demands. Key trends include the widespread adoption of satellite-based navigation systems, such as GPS, GLONASS, Galileo, and BeiDou, which offer unparalleled accuracy and global coverage, gradually reducing reliance on traditional ground-based aids. There is also a significant shift towards integrated modular avionics (IMA) architectures that consolidate various aircraft systems, including positioning, into a unified platform, enhancing efficiency, reducing weight, and simplifying maintenance. The increasing emphasis on autonomous flight capabilities, from advanced drone operations to future air taxis, is propelling the development of more robust, redundant, and secure positioning solutions. Furthermore, the integration of real-time data analytics and artificial intelligence (AI) is optimizing positioning data for predictive maintenance, route optimization, and enhanced situational awareness, ushering in an era of intelligent aviation. Finally, heightened cybersecurity concerns are leading to the development of resilient positioning systems capable of resisting jamming, spoofing, and other malicious attacks, ensuring the integrity and reliability of navigation critical for flight safety.

- Widespread adoption of satellite-based navigation systems.

- Integration of modular avionics (IMA) architectures.

- Increasing focus on autonomous flight capabilities.

- Real-time data analytics and AI integration for optimization.

- Enhanced cybersecurity measures for system resilience.

AI Impact Analysis on Aircraft Positioning Systems

Artificial Intelligence (AI) is poised to revolutionize Aircraft Positioning Systems by introducing unprecedented levels of precision, reliability, and automation. AI algorithms can process vast amounts of real-time navigation data from multiple sensors, including GPS, Inertial Navigation Systems (INS), and radar, to deliver highly accurate position estimates, even in challenging environments where traditional signals might be weak or unavailable. This capability significantly enhances situational awareness for pilots and air traffic controllers, enabling more precise flight path management and collision avoidance. Moreover, AI-driven predictive analytics can forecast potential system failures or performance degradations, allowing for proactive maintenance and minimizing downtime, thereby improving operational efficiency and safety. The integration of AI also facilitates the development of advanced decision-making tools for route optimization, fuel efficiency, and adverse weather avoidance, translating raw positioning data into actionable insights. Looking ahead, AI will be fundamental to fully autonomous aircraft, enabling them to self-navigate, adapt to dynamic conditions, and operate safely without direct human intervention, fundamentally reshaping the future of aviation.

- Enhanced precision through multi-sensor data fusion.

- Predictive maintenance for positioning system components.

- Optimized flight path planning and real-time route adjustments.

- Improved resilience against signal interference and jamming.

- Foundation for autonomous navigation and decision-making.

Key Takeaways Aircraft Positioning Systems Market Size & Forecast

- The global Aircraft Positioning Systems Market is projected to experience substantial growth, reaching a market value of USD 4.10 Billion by 2033 from USD 1.85 Billion in 2025.

- The market is anticipated to expand at a robust Compound Annual Growth Rate (CAGR) of 10.5% between 2025 and 2033, indicating strong investment and adoption.

- Growth is primarily driven by increasing global air traffic, stringent aviation safety regulations, and the continuous evolution of advanced navigation technologies.

- The market's expansion is further boosted by the rising demand for autonomous flight capabilities in both commercial and military aviation.

- Key segments include Portable GPS and Fixed GPS products, catering to diverse aircraft types and operational needs.

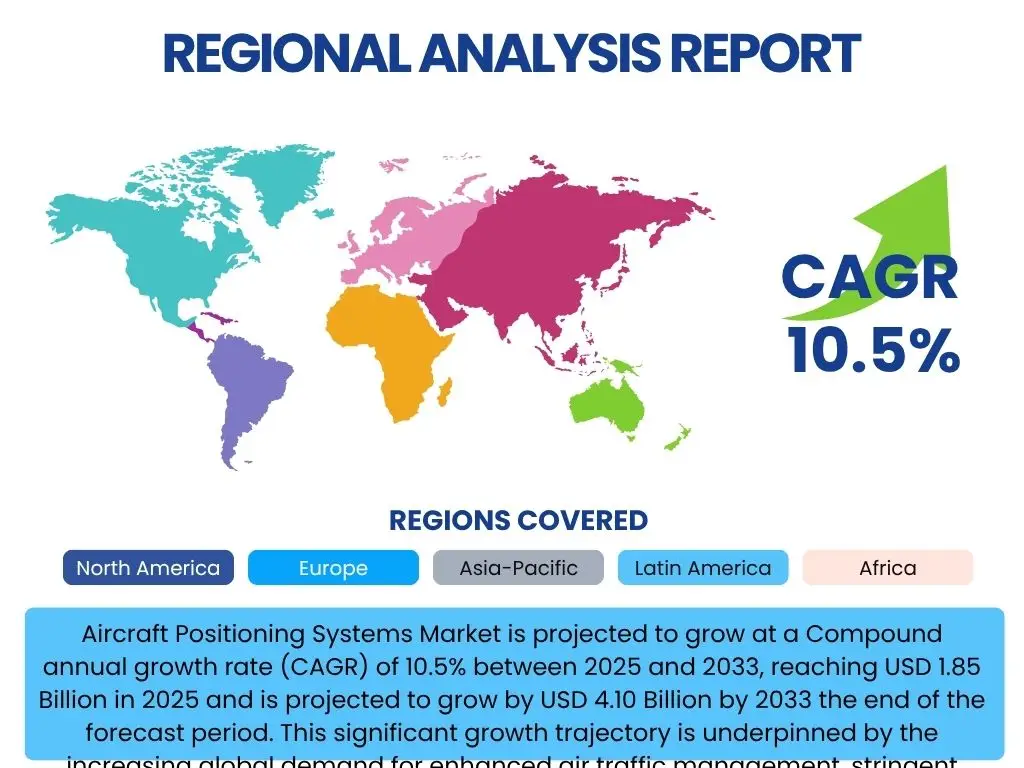

- North America and Europe are expected to remain dominant markets due to early technology adoption and significant aerospace investments, while the Asia Pacific region is poised for rapid growth driven by expanding aviation infrastructure.

- The market forecast highlights significant opportunities for innovation in areas such as AI-powered positioning, enhanced cybersecurity, and integration with Unmanned Aerial Systems (UAS).

Aircraft Positioning Systems Market Drivers Impact Analysis

The Aircraft Positioning Systems Market is propelled by several robust drivers that collectively foster its expansion and technological evolution. A primary driver is the continuous increase in global air passenger and cargo traffic, necessitating more efficient and precise air traffic management (ATM) solutions to prevent congestion and enhance safety. This surge in demand directly translates into the need for advanced positioning systems capable of supporting higher densities of aircraft movements. Furthermore, increasingly stringent aviation safety regulations imposed by international bodies like ICAO and national authorities mandate the adoption of highly accurate and reliable navigation systems, pushing airlines and aircraft manufacturers to upgrade their fleets with the latest positioning technologies. The rapid pace of technological advancements, particularly in satellite navigation, inertial reference systems, and sensor fusion, continuously introduces more capable and cost-effective solutions, further stimulating market growth. Additionally, the proliferation of unmanned aerial vehicles (UAVs) across various sectors, from commercial delivery to military surveillance, is creating new demand for specialized, high-precision positioning systems that can operate autonomously and safely in diverse environments. These combined factors create a fertile ground for sustained market growth and innovation.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Air Traffic and Fleet Expansion | +3.2% | Global, especially Asia Pacific & Middle East | Long-term (2025-2033) |

| Growing Emphasis on Aviation Safety and Regulations | +2.8% | North America, Europe, International | Medium to Long-term (2025-2030) |

| Technological Advancements in Navigation Systems | +2.5% | Global, primarily developed economies | Continuous (2025-2033) |

| Rise in Autonomous Flight and UAV Integration | +2.0% | North America, Europe, China | Medium to Long-term (2027-2033) |

| Modernization of Air Traffic Management (ATM) Infrastructure | +1.8% | Europe, North America, select developing countries | Medium-term (2026-2031) |

Aircraft Positioning Systems Market Restraints Impact Analysis

Despite robust growth drivers, the Aircraft Positioning Systems Market faces several significant restraints that could impede its full potential. One major challenge is the substantial capital expenditure required for the development, acquisition, and integration of advanced positioning systems. The high cost of R&D, coupled with the expensive certification processes and the need for frequent upgrades, can be prohibitive for smaller airlines or those operating on tight budgets, particularly in developing economies. Regulatory complexities and the slow pace of standardization across different regions also pose a restraint. Diverse national and international aviation regulations create compliance hurdles, leading to fragmented market requirements and increasing the time and cost associated with product development and deployment. Furthermore, the inherent vulnerability of satellite-based navigation systems to jamming, spoofing, and cyberattacks represents a critical security concern. These threats necessitate continuous investment in sophisticated counter-measures, adding to operational costs and potentially undermining confidence in system reliability. The long product lifecycles of aircraft also mean that the integration of new technologies can be slow, as existing fleets require costly retrofits. These factors collectively contribute to a cautious adoption pace and impact overall market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Upgrade Costs | -2.5% | Global, more pronounced in developing regions | Long-term (2025-2033) |

| Strict Regulatory and Certification Processes | -2.0% | Global, especially North America & Europe | Medium to Long-term (2025-2030) |

| Vulnerability to Signal Interference and Cyber Threats | -1.8% | Global, critical for military and commercial | Continuous (2025-2033) |

| Complexity of System Integration and Maintenance | -1.5% | Global, impacts smaller operators more | Medium-term (2026-2031) |

| Limited Availability of Skilled Workforce | -1.0% | Global, pronounced in highly technical roles | Long-term (2025-2033) |

Aircraft Positioning Systems Market Opportunities Impact Analysis

The Aircraft Positioning Systems Market is characterized by a dynamic landscape of opportunities, poised to accelerate its growth and foster innovation. A significant avenue lies in the burgeoning urban air mobility (UAM) sector, encompassing air taxis and delivery drones, which will require highly precise and reliable positioning systems for safe and efficient operations in complex urban environments. This emerging market presents a fresh demand stream distinct from traditional aviation. The continuous advancements in satellite-based augmentation systems (SBAS) and ground-based augmentation systems (GBAS) offer improved accuracy and integrity, creating opportunities for enhanced landing capabilities and all-weather operations, thus improving overall air traffic flow. Furthermore, the increasing focus on the Internet of Things (IoT) and connected aircraft initiatives enables positioning systems to integrate seamlessly with other aircraft systems and ground networks, facilitating real-time data exchange, predictive maintenance, and optimized operational insights. The modernization programs for aging military and commercial aircraft fleets worldwide also present substantial opportunities for retrofitting advanced positioning systems, driving demand for upgrades and replacement solutions. Lastly, the development of robust anti-jamming and anti-spoofing technologies to counter evolving threats ensures system resilience and opens new markets for secure navigation solutions, especially in defense and critical infrastructure applications.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Urban Air Mobility (UAM) and eVTOL Aircraft | +3.0% | North America, Europe, Asia Pacific (Tier-1 cities) | Medium to Long-term (2027-2033) |

| Advancements in Satellite-Based Augmentation Systems (SBAS/GBAS) | +2.5% | Global, especially regions with existing infrastructure | Medium-term (2025-2030) |

| Integration with IoT and Connected Aircraft Ecosystems | +2.2% | Global, driven by digital transformation initiatives | Medium to Long-term (2026-2032) |

| Fleet Modernization and Retrofit Programs | +1.8% | North America, Europe, developing economies with aging fleets | Short to Medium-term (2025-2029) |

| Development of Robust Anti-Jamming and Anti-Spoofing Solutions | +1.5% | Global, critical for defense and commercial aviation | Continuous (2025-2033) |

Aircraft Positioning Systems Market Challenges Impact Analysis

The Aircraft Positioning Systems Market encounters several critical challenges that stakeholders must address for sustained growth and innovation. One prominent challenge is the persistent threat of GNSS (Global Navigation Satellite System) signal vulnerabilities, including jamming and spoofing. These deliberate interferences can compromise the accuracy and integrity of positioning data, posing significant safety risks and necessitating substantial investment in resilient navigation technologies and backup systems. Another key challenge arises from the rapid pace of technological obsolescence. As new and more advanced positioning technologies emerge, existing systems can quickly become outdated, requiring frequent and costly upgrades or replacements for airlines and military operators to maintain competitive and regulatory compliance. Furthermore, the complexities associated with integrating diverse positioning systems, sensors, and avionics architectures into a cohesive and interoperable framework present a significant technical hurdle. Ensuring seamless communication and data exchange between various components, often from different manufacturers, demands extensive testing and standardization efforts. Geopolitical instabilities and supply chain disruptions can also impact the market by affecting the availability of critical components or imposing trade restrictions, thereby increasing costs and lead times for manufacturers. Lastly, the shortage of highly skilled professionals capable of developing, maintaining, and operating these sophisticated systems poses a workforce challenge, hindering innovation and efficient deployment. Addressing these multifaceted challenges is crucial for unlocking the full potential of the Aircraft Positioning Systems Market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| GNSS Signal Vulnerabilities (Jamming, Spoofing) | -2.8% | Global, particularly in contested airspaces | Continuous (2025-2033) |

| Rapid Technological Obsolescence | -2.3% | Global, impacts long-term fleet planning | Medium to Long-term (2025-2030) |

| Integration Complexities with Legacy Systems | -1.7% | Global, impacts established airlines and militaries | Medium-term (2026-2031) |

| Geopolitical Instabilities and Supply Chain Disruptions | -1.5% | Global, particularly critical component sourcing | Short to Medium-term (2025-2028) |

| Data Integrity and Security Concerns | -1.2% | Global, critical for safety and operational reliability | Continuous (2025-2033) |

Aircraft Positioning Systems Market - Updated Report Scope

The updated report scope for the Aircraft Positioning Systems Market provides a comprehensive and in-depth analysis of market dynamics, growth drivers, restraints, opportunities, and challenges influencing the industry's trajectory from 2025 to 2033. It offers crucial insights into market sizing, segmentation by various criteria, and detailed regional breakdowns, enabling stakeholders to make informed strategic decisions. The report also profiles key industry players, offering a competitive landscape analysis and highlighting their product portfolios, strategies, and market presence. This detailed examination aims to provide a holistic view of the market, addressing the evolving needs of aircraft manufacturers, airlines, defense organizations, and technology providers.

| Report Attributes | Report Details |

|---|---|

| Report Name | Aircraft Positioning Systems Market |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 4.10 Billion |

| Growth Rate | CAGR of 2025 to 2033 10.5% |

| Number of Pages | 280 |

| Key Companies Covered | Garmin, Esterline, Honeywell Aerospace, Avidyne Corporation, Genesys Aerosystems, Dynon Avionics, FreeFlight Systems, Innovative Solutions and Support |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

:Market Product Type Segmentation:-

- Portable GPS

- Fixed GPS

Market Application Segmentation:-

- Military Aircrafts

- Civil Aircrafts

Regional Highlights

The global Aircraft Positioning Systems Market exhibits distinct regional dynamics, with certain geographies leading in adoption and technological innovation due to significant aerospace investments, stringent regulatory frameworks, and expanding aviation sectors. Understanding these regional nuances is crucial for strategic market entry and expansion.- North America: This region is anticipated to maintain a dominant position in the Aircraft Positioning Systems Market, driven by the presence of major aerospace and defense manufacturers, early adoption of advanced aviation technologies, and substantial government investments in military modernization. The robust commercial aviation sector and pioneering work in Urban Air Mobility (UAM) also contribute significantly to its market share.

- Europe: Europe stands as another key market, characterized by stringent aviation safety regulations, significant R&D activities in avionics, and the presence of leading aircraft manufacturers. The region's focus on modernizing its air traffic management systems (e.g., SESAR initiative) and integrating next-generation navigation capabilities ensures sustained demand for advanced positioning solutions.

- Asia Pacific (APAC): The APAC region is projected to witness the highest growth rate during the forecast period. This rapid expansion is primarily attributed to the burgeoning commercial aviation sector driven by increasing passenger traffic, massive investments in new airport infrastructure, and a growing number of aircraft orders across countries like China, India, and Southeast Asian nations. The region's rising defense budgets also contribute to the demand for advanced military aircraft positioning systems.

- Latin America, Middle East, and Africa (MEA): These regions are expected to experience moderate but steady growth. Latin America's growth is linked to fleet modernization efforts and increasing regional air connectivity. The Middle East benefits from significant investments in aviation infrastructure and the expansion of major airlines, while Africa's market is gradually evolving with improvements in its aviation safety standards and air traffic management.

Top Key Players:

The market research report covers the analysis of key stake holders of the Aircraft Positioning Systems Market. Some of the leading players profiled in the report include -:- Garmin

- Esterline

- Honeywell Aerospace

- Avidyne Corporation

- Genesys Aerosystems

- Dynon Avionics

- FreeFlight Systems

- Innovative Solutions and Support

Frequently Asked Questions:

What is an Aircraft Positioning System?

Response: An Aircraft Positioning System is an onboard navigational technology that determines the precise geographical location, altitude, and velocity of an aircraft. These systems utilize various technologies, including Global Navigation Satellite Systems (GNSS) like GPS, GLONASS, Galileo, or BeiDou, and Inertial Navigation Systems (INS). They are crucial for flight planning, air traffic control, collision avoidance, and ensuring overall aviation safety and efficiency by providing real-time positional data to pilots and ground operations.

How does AI impact Aircraft Positioning Systems?

Response: Artificial Intelligence significantly enhances Aircraft Positioning Systems by enabling more accurate data fusion from multiple sensors, predictive maintenance capabilities, and advanced decision-making for route optimization. AI algorithms can process vast and complex datasets to provide more reliable position estimates, even in environments with signal degradation. This facilitates improved situational awareness, automation in flight operations, and is foundational for the development of fully autonomous aircraft, transforming how aircraft navigate and interact within airspaces.

What are the primary drivers of the Aircraft Positioning Systems Market growth?

Response: The primary drivers include the continuous increase in global air traffic and expanding commercial aircraft fleets, which necessitate more efficient air traffic management. Stricter aviation safety regulations imposed by international and national authorities also drive demand for highly accurate navigation systems. Furthermore, ongoing technological advancements in satellite navigation and sensor technologies, alongside the burgeoning integration of Unmanned Aerial Vehicles (UAVs) across various sectors, are significantly contributing to market expansion.

What challenges does the Aircraft Positioning Systems Market face?

Response: Key challenges in the Aircraft Positioning Systems Market include the inherent vulnerability of GNSS signals to jamming and spoofing, which poses significant security and safety risks. The rapid pace of technological obsolescence demands frequent and costly system upgrades. Additionally, the complexity of integrating diverse positioning systems with existing aircraft avionics, geopolitical instabilities affecting supply chains, and the shortage of skilled technical personnel further constrain market growth and widespread adoption.

Which regions are leading in the adoption of Aircraft Positioning Systems?

Response: North America and Europe are currently leading in the adoption of Aircraft Positioning Systems due to their advanced aerospace industries, significant investments in defense, stringent aviation safety standards, and proactive efforts in modernizing air traffic management infrastructure. The Asia Pacific region is expected to demonstrate the highest growth in adoption, driven by its rapidly expanding commercial aviation sector, increasing passenger volumes, and substantial investments in new airport and aircraft development.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted