Aircraft Heat Exchanger Market

Aircraft Heat Exchanger Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_703333 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Aircraft Heat Exchanger Market Size

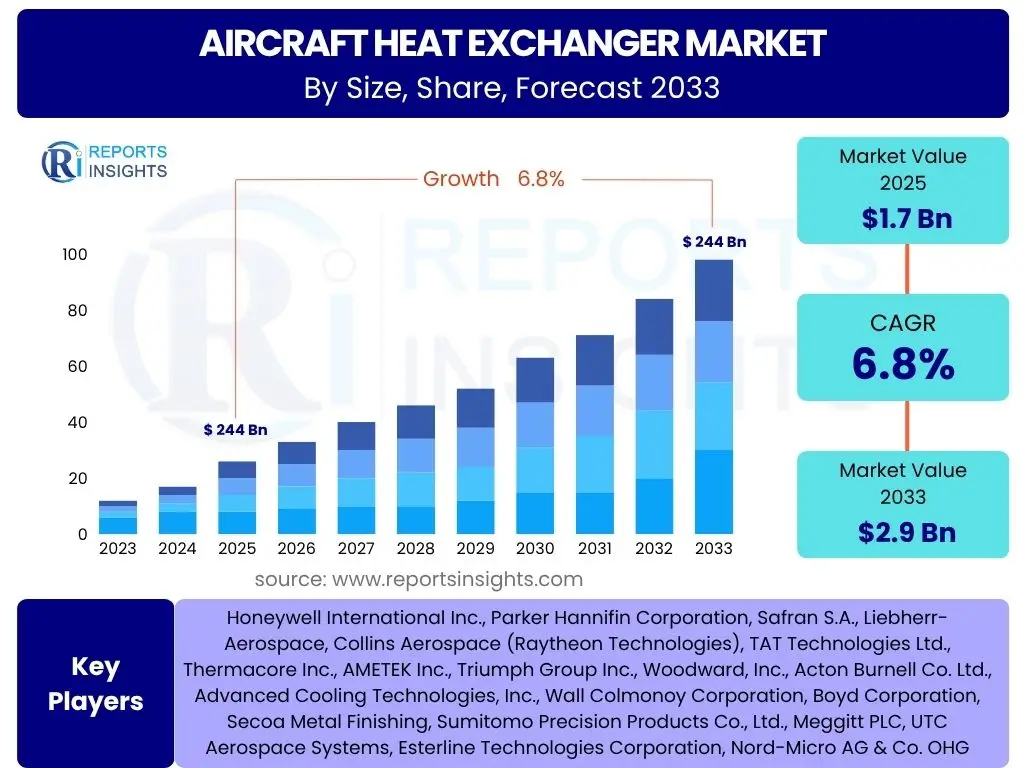

According to Reports Insights Consulting Pvt Ltd, The Aircraft Heat Exchanger Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 1.7 Billion in 2025 and is projected to reach USD 2.9 Billion by the end of the forecast period in 2033.

Key Aircraft Heat Exchanger Market Trends & Insights

User inquiries frequently highlight the evolving demands on aircraft thermal management systems, driven by advancements in propulsion, avionics, and overall aircraft design. Key areas of interest revolve around the adoption of lightweight materials, the integration of additive manufacturing techniques, and the increasing need for highly efficient heat exchangers to manage the thermal loads of more electric aircraft (MEA). There is a significant focus on solutions that reduce weight, improve fuel efficiency, and enhance the reliability of thermal components, which are critical for both commercial and military aviation sectors.

Another prominent trend observed in market research is the shift towards more integrated thermal management systems rather than standalone components. This holistic approach is essential for accommodating the complex thermal requirements of next-generation aircraft, including supersonic jets and urban air mobility vehicles. Users are also keen to understand how sustainability initiatives are influencing the design and material selection for heat exchangers, pushing for solutions that contribute to lower emissions and reduced environmental impact throughout the product lifecycle.

Furthermore, the drive for enhanced performance in extreme conditions, particularly in military and high-altitude applications, is spurring innovation in heat exchanger technology. This includes developments in micro-channel designs, phase-change materials, and advanced fin geometries to maximize heat transfer efficiency within constrained spaces. The aerospace industry's continuous pursuit of operational excellence and safety mandates constant evolution in thermal management, making these trends central to market growth and technological development.

- Lightweighting initiatives through advanced materials and additive manufacturing.

- Increased demand for thermal management in More Electric Aircraft (MEA) and hybrid-electric propulsion systems.

- Development of highly efficient, compact heat exchanger designs (e.g., micro-channel).

- Integration of smart sensors and diagnostic capabilities for predictive maintenance.

- Emphasis on sustainable manufacturing processes and recyclable materials.

AI Impact Analysis on Aircraft Heat Exchanger

Common user questions regarding AI's impact on aircraft heat exchangers primarily center on its role in design optimization, predictive maintenance, and operational efficiency. Users are particularly interested in how artificial intelligence algorithms can accelerate the design cycle by exploring a vast parameter space for optimal heat exchanger geometries, material combinations, and fluid dynamics, far beyond traditional simulation methods. This capability promises to yield designs that are lighter, more efficient, and cost-effective, directly addressing critical industry demands.

Furthermore, there is significant curiosity about AI's application in real-time monitoring and anomaly detection for in-service heat exchangers. By analyzing operational data from sensors, AI can predict potential failures, optimize maintenance schedules, and even suggest real-time adjustments to thermal management systems to enhance performance and longevity. This shift from reactive to proactive maintenance can drastically reduce downtime, improve safety, and lower operational costs for airlines and military operators.

Beyond design and maintenance, AI is also anticipated to play a crucial role in the manufacturing process of heat exchangers, enabling intelligent automation, quality control, and supply chain optimization. The ability of AI to process and derive insights from complex datasets will allow manufacturers to identify bottlenecks, reduce waste, and improve production consistency. Overall, users view AI as a transformative technology that will drive significant efficiency gains and innovation across the entire lifecycle of aircraft heat exchangers.

- AI-driven generative design for optimized heat exchanger geometries and performance.

- Predictive maintenance algorithms for early detection of heat exchanger degradation and failures.

- Real-time thermal management system optimization using machine learning.

- Enhanced material selection and process control through AI in manufacturing.

- Data analytics for improving operational efficiency and reducing fuel consumption linked to thermal systems.

Key Takeaways Aircraft Heat Exchanger Market Size & Forecast

The aircraft heat exchanger market is poised for steady expansion through 2033, primarily fueled by the robust growth in global air traffic, increasing aircraft deliveries, and the relentless pursuit of fuel efficiency and reduced emissions in the aviation industry. The forecast underscores a sustained demand for advanced thermal management solutions as new aircraft designs incorporate more electric systems and require optimized heat dissipation capabilities. This growth trajectory is reflective of continuous technological advancements aimed at enhancing performance, durability, and weight reduction of heat exchanger components.

A significant takeaway is the pivotal role of research and development in driving market dynamics. Innovations in materials science, such as the adoption of lightweight composites and advanced alloys, along with sophisticated manufacturing techniques like additive manufacturing, are enabling the creation of more compact and efficient heat exchangers. These technological leaps are crucial for meeting the stringent performance requirements of next-generation aircraft, including those focused on hybrid-electric propulsion and urban air mobility platforms.

Furthermore, the aftermarket segment, driven by maintenance, repair, and overhaul (MRO) activities, will continue to contribute substantially to market revenue. The long operational lifespans of aircraft necessitate regular inspection, repair, and replacement of heat exchanger components, ensuring a stable demand stream irrespective of new aircraft production cycles. This dual growth from OEM and aftermarket segments positions the aircraft heat exchanger market for consistent and resilient expansion over the forecast period.

- Consistent growth projected through 2033, driven by increasing air travel and fleet modernization.

- Technological advancements in materials and manufacturing are critical for market expansion.

- Emergence of More Electric Aircraft (MEA) and hybrid propulsion systems creates new demand.

- Significant contributions from both Original Equipment Manufacturer (OEM) and aftermarket segments.

- Emphasis on efficiency, weight reduction, and reliability remains a core focus.

Aircraft Heat Exchanger Market Drivers Analysis

The increasing global demand for new commercial and military aircraft is a primary driver for the aircraft heat exchanger market. As airlines expand their fleets to accommodate rising passenger traffic and defense budgets allocate more funds towards modernizing military aviation, the need for advanced thermal management systems intensifies. Each new aircraft requires multiple heat exchangers for various critical functions, from engine oil cooling to cabin air conditioning, directly translating into higher market demand.

Technological advancements in aircraft design, particularly the shift towards More Electric Aircraft (MEA) and hybrid-electric propulsion, are fundamentally reshaping the thermal management landscape. These new architectures introduce higher electrical power loads, requiring more sophisticated and efficient heat dissipation solutions to manage the heat generated by avionics, power electronics, and high-power motors. This evolution necessitates the development of heat exchangers capable of handling greater thermal loads within strict weight and space constraints.

Moreover, the stringent regulatory environment concerning fuel efficiency and emissions reduction compels aircraft manufacturers to adopt highly optimized components. Efficient heat exchangers contribute significantly to overall aircraft performance by minimizing energy loss and improving system efficiency, thereby directly impacting fuel consumption and reducing the environmental footprint. This regulatory pressure acts as a continuous impetus for innovation and adoption of advanced heat exchanger technologies across the aerospace industry.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Commercial Aircraft Deliveries | +1.5% | Asia Pacific, North America, Europe | 2025-2033 |

| Rising Defense Spending & Military Aircraft Modernization | +1.2% | North America, Europe, Middle East | 2025-2033 |

| Development of More Electric Aircraft (MEA) & Hybrid Propulsion | +1.0% | North America, Europe | 2027-2033 |

| Growing Demand for Fuel-Efficient & Low-Emission Aircraft | +0.8% | Global | 2025-2033 |

| Expansion of Urban Air Mobility (UAM) and eVTOL Projects | +0.5% | North America, Europe, Asia Pacific | 2028-2033 |

Aircraft Heat Exchanger Market Restraints Analysis

The aircraft heat exchanger market faces significant restraints, primarily stemming from the high research and development costs associated with designing and qualifying new thermal management solutions for aerospace applications. The stringent performance requirements, extreme operating conditions, and the need for lightweight yet robust materials demand substantial investment in R&D. This elevated cost can prolong product development cycles and limit the rapid adoption of innovative technologies, particularly for smaller market players or niche applications.

Furthermore, the aerospace industry is characterized by an exceptionally rigorous regulatory and certification process. Aircraft heat exchangers, being critical components, must adhere to numerous national and international aviation standards for safety, reliability, and environmental compliance. Obtaining the necessary certifications from bodies like the FAA or EASA is a time-consuming and expensive endeavor, often involving extensive testing and documentation. This regulatory burden acts as a barrier to market entry and can slow down the introduction of new products, impacting overall market growth.

Additionally, the volatility in raw material prices, particularly for specialized alloys and composites used in heat exchanger manufacturing, poses a significant challenge. Fluctuations in the cost of aluminum, titanium, and other high-performance materials directly impact production costs, which can then affect the final price of the components. Supply chain disruptions, often exacerbated by geopolitical tensions or global events, can further complicate material procurement, leading to production delays and increased operational expenses for manufacturers in this market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Research & Development Costs | -0.9% | Global | 2025-2033 |

| Stringent Regulatory & Certification Processes | -0.8% | Global | 2025-2033 |

| Volatility in Raw Material Prices & Supply Chain Disruptions | -0.7% | Global | 2025-2030 |

| Complexity of Integrating New Thermal Systems | -0.6% | Global | 2025-2033 |

Aircraft Heat Exchanger Market Opportunities Analysis

The burgeoning market for More Electric Aircraft (MEA) and emerging hybrid-electric and all-electric propulsion systems presents a significant growth opportunity for aircraft heat exchanger manufacturers. These next-generation aircraft architectures necessitate substantially more robust and efficient thermal management solutions to dissipate heat generated by increased electrical components, power electronics, and high-power motors. Developing specialized heat exchangers optimized for these novel power systems will be crucial for the successful implementation and adoption of electric aviation, opening up entirely new revenue streams for innovators in this field.

Another substantial opportunity lies in the expanding urban air mobility (UAM) and advanced air mobility (AAM) sectors, encompassing electric Vertical Take-Off and Landing (eVTOL) vehicles and drones. While still in their nascent stages, these segments are projected to experience rapid growth, requiring compact, lightweight, and highly efficient heat exchangers for their propulsion systems, batteries, and avionics. Companies that can quickly adapt their core competencies to meet the unique size, weight, and power (SWaP) constraints of these emerging aircraft types will gain a significant competitive advantage.

Furthermore, the ongoing emphasis on sustainable aviation fuels (SAF) and hydrogen propulsion, alongside the continued focus on reducing carbon emissions, creates a persistent demand for high-efficiency components. Heat exchangers that can contribute to overall system efficiency, thereby lowering fuel consumption and emissions, will remain highly sought after. Innovations in design and materials that enhance heat transfer while reducing component weight will align with industry sustainability goals, providing long-term growth prospects for the market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of More Electric Aircraft (MEA) and Hybrid-Electric Propulsion | +1.1% | North America, Europe, Asia Pacific | 2027-2033 |

| Emergence of Urban Air Mobility (UAM) and eVTOL Aircraft | +1.0% | North America, Europe, Asia Pacific | 2028-2033 |

| Increased Adoption of Additive Manufacturing for Complex Geometries | +0.9% | Global | 2026-2033 |

| Focus on Lightweight & Compact Designs for Space-Constrained Applications | +0.8% | Global | 2025-2033 |

| Integration of Smart & Adaptive Thermal Management Systems | +0.7% | Global | 2027-2033 |

Aircraft Heat Exchanger Market Challenges Impact Analysis

One of the primary challenges for the aircraft heat exchanger market is the continuous pressure to achieve higher thermal efficiency within ever-decreasing size, weight, and power (SWaP) envelopes. As aircraft become more sophisticated and integrate more complex systems, the available space and weight for thermal management components become highly constrained. Designing heat exchangers that can dissipate significant amounts of heat while being incredibly compact and lightweight requires cutting-edge materials and manufacturing processes, often pushing the boundaries of current engineering capabilities.

Another significant challenge is ensuring the reliability and durability of heat exchangers under extreme operating conditions. Aircraft thermal systems are exposed to wide temperature fluctuations, high pressures, vibrations, and corrosive environments. Components must be engineered to withstand these harsh conditions for extended periods without degradation in performance or structural integrity. This necessitates rigorous testing and validation, adding to development costs and timelines, and posing a substantial barrier to rapid innovation and deployment.

Furthermore, integrating new heat exchanger technologies seamlessly into existing or novel aircraft architectures presents considerable complexity. Thermal management systems are intrinsically linked with various other aircraft systems, including propulsion, environmental control, and avionics. Ensuring compatibility, optimizing performance across multiple interfaces, and validating system-level interactions require extensive collaboration between component manufacturers and aircraft integrators. This intricate integration process can lead to design iterations and delays, impacting market timelines and adoption rates for advanced heat exchanger solutions.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving High Efficiency within Size, Weight, and Power (SWaP) Constraints | -0.9% | Global | 2025-2033 |

| Ensuring Durability & Reliability in Extreme Operating Environments | -0.8% | Global | 2025-2033 |

| Complex Integration with New Aircraft Architectures (e.g., Electric Propulsion) | -0.7% | Global | 2025-2033 |

| High Manufacturing Precision & Quality Control Demands | -0.6% | Global | 2025-2033 |

Aircraft Heat Exchanger Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Aircraft Heat Exchanger Market, examining historical data, current market dynamics, and future projections. It offers a detailed breakdown by type, application, aircraft type, end-use, and material, alongside a thorough regional analysis. The report highlights key market trends, drivers, restraints, opportunities, and challenges, providing strategic insights for stakeholders. It also includes an impact analysis of artificial intelligence on the market and profiles of leading companies, offering a holistic view of the industry landscape from 2019 to 2033.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.7 Billion |

| Market Forecast in 2033 | USD 2.9 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Honeywell International Inc., Parker Hannifin Corporation, Safran S.A., Liebherr-Aerospace, Collins Aerospace (Raytheon Technologies), TAT Technologies Ltd., Thermacore Inc., AMETEK Inc., Triumph Group Inc., Woodward, Inc., Acton Burnell Co. Ltd., Advanced Cooling Technologies, Inc., Wall Colmonoy Corporation, Boyd Corporation, Secoa Metal Finishing, Sumitomo Precision Products Co., Ltd., Meggitt PLC, UTC Aerospace Systems, Esterline Technologies Corporation, Nord-Micro AG & Co. OHG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The aircraft heat exchanger market is meticulously segmented to provide a granular understanding of its diverse applications and technological nuances. This comprehensive breakdown allows for a detailed analysis of demand patterns across various aircraft types, operational functions, and material compositions. Understanding these segments is crucial for identifying specific growth pockets and tailoring product development to meet specialized industry requirements, from high-performance military applications to lightweight commercial aircraft systems.

- By Type: Plate-Fin, Shell and Tube, Micro-channel, Recuperators, Regenerators, Others.

- By Application: Engine, Air Conditioning, Oil Cooling, Fuel Cooling, Electronic Cooling, Environmental Control Systems (ECS), Auxiliary Power Units (APU), Others.

- By Aircraft Type: Commercial Aircraft, Military Aircraft, Business Jets, Helicopters, General Aviation, UAVs/Drones, Advanced Air Mobility (AAM) / Urban Air Mobility (UAM).

- By End-Use: OEM (Original Equipment Manufacturer), Aftermarket (MRO - Maintenance, Repair, and Overhaul).

- By Material: Aluminum Alloys, Titanium Alloys, Stainless Steel, Composites, Others.

Regional Highlights

- North America: Dominates the market due to the presence of major aircraft manufacturers, significant defense spending, and robust research and development activities in advanced aerospace technologies. The region leads in the adoption of More Electric Aircraft (MEA) concepts and has a strong focus on military modernization programs.

- Europe: A key market driven by established aerospace players, a strong emphasis on environmental regulations, and investments in next-generation aircraft projects, including urban air mobility. Collaborative European defense initiatives also contribute to market growth.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate, fueled by rapid expansion of commercial airline fleets, increasing passenger traffic, and growing defense budgets in countries like China, India, and Japan. The region is a burgeoning hub for both aircraft manufacturing and MRO activities.

- Latin America: Demonstrates steady growth, primarily influenced by fleet modernization efforts and increasing air travel within the region, leading to demand for efficient and reliable aircraft components.

- Middle East and Africa (MEA): Growing investments in aviation infrastructure, expansion of national carriers, and geopolitical factors driving defense spending contribute to the demand for aircraft heat exchangers in this region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aircraft Heat Exchanger Market.- Honeywell International Inc.

- Parker Hannifin Corporation

- Safran S.A.

- Liebherr-Aerospace

- Collins Aerospace (Raytheon Technologies)

- TAT Technologies Ltd.

- Thermacore Inc.

- AMETEK Inc.

- Triumph Group Inc.

- Woodward, Inc.

- Acton Burnell Co. Ltd.

- Advanced Cooling Technologies, Inc.

- Wall Colmonoy Corporation

- Boyd Corporation

- Secoa Metal Finishing

- Sumitomo Precision Products Co., Ltd.

- Meggitt PLC

- UTC Aerospace Systems

- Esterline Technologies Corporation

- Nord-Micro AG & Co. OHG

Frequently Asked Questions

What is an Aircraft Heat Exchanger?

An aircraft heat exchanger is a device designed to transfer thermal energy between two or more fluids or between a fluid and a solid surface, typically without allowing them to mix. These components are essential for maintaining optimal operating temperatures for various aircraft systems, including engines, hydraulics, avionics, and environmental control systems, ensuring safety, efficiency, and performance.

How do heat exchangers contribute to aircraft efficiency?

Heat exchangers significantly enhance aircraft efficiency by optimizing thermal management. By efficiently cooling critical systems, they prevent overheating, reduce energy consumption from cooling, and improve component lifespan and reliability. This directly contributes to better fuel economy, reduced maintenance costs, and overall improved operational performance for the aircraft.

What materials are commonly used in Aircraft Heat Exchangers?

Commonly used materials for aircraft heat exchangers include aluminum alloys, titanium alloys, and stainless steel, chosen for their high thermal conductivity, strength-to-weight ratio, and corrosion resistance. Advanced materials like composites are also gaining traction for their lightweight properties and ability to withstand extreme conditions, further optimizing performance.

What are the key future trends in the Aircraft Heat Exchanger Market?

Key future trends include the increasing demand for lightweight and compact designs, driven by More Electric Aircraft (MEA) and urban air mobility (UAM) concepts. There is also a strong focus on additive manufacturing for complex geometries, integrated thermal management systems, and the incorporation of smart technologies for predictive maintenance and real-time optimization.

What factors drive the growth of the Aircraft Heat Exchanger Market?

Market growth is primarily driven by increasing global aircraft deliveries, both commercial and military, due to rising air travel and defense modernization. Additionally, technological advancements in aircraft design, the development of More Electric Aircraft, and stringent regulations on fuel efficiency and emissions are compelling the adoption of advanced heat exchanger solutions.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted