Aircraft Nose Landing Gear Market

Aircraft Nose Landing Gear Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702283 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Aircraft Nose Landing Gear Market Size

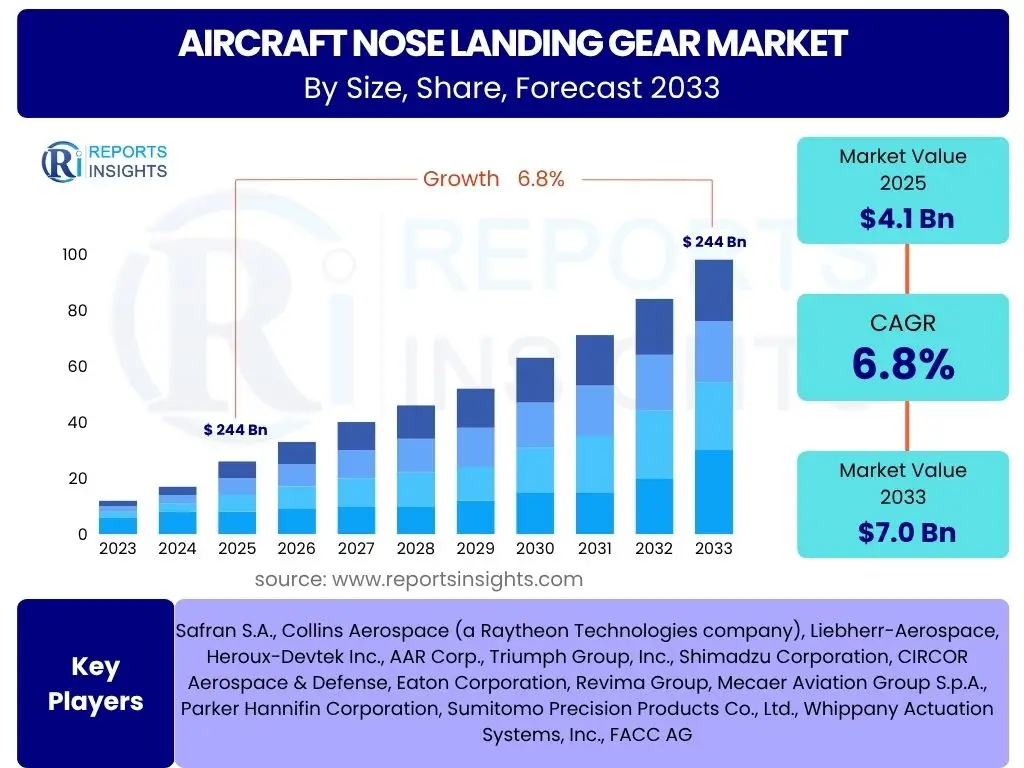

According to Reports Insights Consulting Pvt Ltd, The Aircraft Nose Landing Gear Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 4.1 Billion in 2025 and is projected to reach USD 7.0 Billion by the end of the forecast period in 2033.

Key Aircraft Nose Landing Gear Market Trends & Insights

Users frequently inquire about the evolving technological landscape, material advancements, and operational shifts impacting the Aircraft Nose Landing Gear market. They seek to understand how the industry is adapting to demands for increased efficiency, reduced weight, and enhanced safety. Specific areas of interest include the adoption of predictive maintenance technologies, the integration of smart systems, and the impact of sustainable aviation initiatives on landing gear design and manufacturing.

Current insights reveal a strong emphasis on innovation driven by the need for more robust, yet lighter, components, and systems that can perform complex self-diagnostics. The drive towards electrification in aircraft is also influencing landing gear development, with a focus on electric braking and e-taxi systems. Furthermore, manufacturers are exploring advanced manufacturing techniques, such as additive manufacturing, to create intricate designs, optimize material usage, and accelerate production cycles, thereby contributing to overall market dynamics and competitive advantage.

- Adoption of lightweight and high-strength materials such as advanced composites and titanium alloys.

- Integration of smart landing gear systems with advanced sensors for real-time monitoring and predictive maintenance.

- Development of electric braking and e-taxi systems to reduce ground operations emissions and fuel consumption.

- Increasing use of additive manufacturing (3D printing) for complex component geometries and rapid prototyping.

- Emphasis on digital twin technology for design optimization, testing, and in-service performance monitoring.

- Focus on modular designs for easier maintenance, repair, and overhaul (MRO).

AI Impact Analysis on Aircraft Nose Landing Gear

Common user questions regarding AI's impact on Aircraft Nose Landing Gear center on its potential to revolutionize design, manufacturing, and maintenance processes. Users are keen to understand how artificial intelligence can improve system reliability, extend component lifespan, and reduce operational costs. Specific inquiries often relate to AI-driven predictive analytics for maintenance scheduling, intelligent automation in production, and AI-assisted design optimization for enhanced performance.

AI is set to significantly transform the lifecycle of aircraft nose landing gear by enabling more proactive and precise interventions. In design, generative AI can explore numerous design iterations to optimize weight, strength, and aerodynamic properties, leading to more efficient and safer components. For manufacturing, AI-powered robotics and quality control systems can ensure higher precision and reduce defects. Post-delivery, AI algorithms analyze sensor data from landing gear to predict potential failures before they occur, allowing for condition-based maintenance rather than time-based, thereby minimizing downtime and maximizing asset utilization.

- AI-powered predictive maintenance enhances diagnostic accuracy and optimizes maintenance schedules, reducing unscheduled downtime.

- Generative design and simulation tools, leveraging AI, optimize landing gear structures for weight reduction and performance.

- AI-driven automation in manufacturing processes improves precision, efficiency, and quality control during production.

- Machine learning algorithms analyze sensor data from landing gear for real-time health monitoring and anomaly detection.

- AI applications streamline supply chain and inventory management for landing gear components, improving logistics.

Key Takeaways Aircraft Nose Landing Gear Market Size & Forecast

Users frequently seek a concise understanding of the market's trajectory, principal growth drivers, and the underlying factors influencing its expansion. They are interested in identifying the primary segments contributing to market growth and the technological shifts that are most impactful. Questions often revolve around what makes the nose landing gear market a critical component of aerospace industry growth and where the most significant investment opportunities lie.

The Aircraft Nose Landing Gear market is poised for steady growth, primarily fueled by the increasing demand for new commercial and military aircraft, coupled with the substantial need for MRO services for the existing global fleet. Technological advancements, particularly in lightweight materials, intelligent systems, and electrification, are key enablers of this growth, enhancing operational efficiency and safety. The market's resilience is also supported by the long operational lifespans of aircraft and the critical safety function of landing gear, necessitating continuous upgrades and maintenance throughout an aircraft's service life.

- Market growth is consistently driven by global air traffic expansion and new aircraft deliveries.

- Technological advancements in materials and smart systems are critical for future market development.

- The aftermarket segment, particularly MRO, contributes significantly to overall market revenue.

- Increased defense spending and military aircraft procurement also play a substantial role in market expansion.

- Sustainability initiatives are influencing design and manufacturing towards more environmentally friendly solutions.

Aircraft Nose Landing Gear Market Drivers Analysis

The Aircraft Nose Landing Gear market is significantly propelled by several macro and micro-economic factors. A primary driver is the consistent increase in global air passenger traffic, which necessitates the expansion and modernization of commercial aircraft fleets. This directly translates into higher demand for new aircraft, and consequently, new landing gear systems as original equipment.

Furthermore, the ongoing trend of airlines and cargo operators investing in new generation, fuel-efficient aircraft drives innovation and procurement in the landing gear sector. These modern aircraft require advanced landing gear systems that are lighter, more robust, and integrate sophisticated technologies to enhance performance and reduce operational costs. Simultaneously, the aging global aircraft fleet requires substantial maintenance, repair, and overhaul (MRO) services, creating a robust aftermarket demand for replacement components and upgrades, thereby sustaining market activity even during periods of slower new aircraft production.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increase in global air passenger traffic & freight volume | +1.8% | Global, particularly APAC & North America | Medium to Long Term (2025-2033) |

| Growing demand for new generation, fuel-efficient aircraft | +1.5% | North America, Europe, Asia Pacific | Medium Term (2025-2030) |

| Rise in defense spending and military aircraft procurement | +1.2% | North America, Europe, Middle East | Medium to Long Term (2025-2033) |

| Aging commercial aircraft fleet requiring MRO and upgrades | +1.0% | Global, especially mature markets | Long Term (2025-2033) |

| Technological advancements in landing gear systems (e.g., lightweighting) | +0.8% | Global | Short to Medium Term (2025-2028) |

Aircraft Nose Landing Gear Market Restraints Analysis

Despite robust growth drivers, the Aircraft Nose Landing Gear market faces certain restraints that could temper its expansion. One significant impediment is the exceptionally high cost associated with research and development (R&D) for new landing gear technologies. Developing advanced materials, integrated smart systems, and electric components requires substantial investment, often spanning several years, which can be a barrier for smaller players and impacts the overall profitability and pace of innovation for larger firms.

Furthermore, the aviation industry is subject to extremely stringent certification and regulatory standards, particularly concerning safety. These rigorous compliance requirements, imposed by bodies such as the FAA and EASA, lead to lengthy and costly approval processes for any new design or modification, extending time-to-market and increasing development expenses. Additionally, the complex global supply chains for specialized materials and components, coupled with potential geopolitical instabilities or trade disputes, can lead to disruptions and price volatility, directly impacting manufacturing costs and delivery timelines for landing gear systems.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High research and development (R&D) costs | -0.9% | Global | Long Term (2025-2033) |

| Stringent aviation certification and regulatory standards | -0.8% | Global | Long Term (2025-2033) |

| Supply chain disruptions and material price volatility | -0.7% | Global | Short to Medium Term (2025-2028) |

| Economic downturns impacting air travel demand and aircraft orders | -0.6% | Global | Short Term (2025-2027) |

| Environmental noise and pollution concerns leading to operational restrictions | -0.4% | Europe, North America | Medium Term (2025-2030) |

Aircraft Nose Landing Gear Market Opportunities Analysis

The Aircraft Nose Landing Gear market presents several promising opportunities for growth and innovation. The emergence of Urban Air Mobility (UAM) and Electrical Vertical Take-off and Landing (eVTOL) aircraft represents a significant new market segment. As these novel aircraft move from conceptualization to commercialization, they will require specialized, lightweight, and highly reliable landing gear systems, opening new avenues for manufacturers and technological development.

Another substantial opportunity lies in the increasing demand for aftermarket services and MRO outsourcing. Airlines and operators are increasingly opting to outsource their maintenance activities to specialized MRO providers, driving demand for spare parts, repairs, and component upgrades for existing fleets. Furthermore, the industry's sustained focus on sustainable aviation initiatives, including the development of eco-friendly hydraulic fluids, quieter landing gear designs, and energy-efficient braking systems, creates a robust demand for new, environmentally conscious product offerings, aligning with global sustainability goals and expanding market potential.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Urban Air Mobility (UAM) and eVTOL aircraft | +1.3% | North America, Europe, Asia Pacific | Medium to Long Term (2028-2033) |

| Increasing demand for aftermarket services and MRO outsourcing | +1.1% | Global | Long Term (2025-2033) |

| Development of advanced materials and manufacturing processes | +0.9% | Global | Short to Medium Term (2025-2030) |

| Focus on sustainable aviation initiatives and green technologies | +0.8% | Europe, North America | Medium to Long Term (2025-2033) |

| Integration of intelligent systems for enhanced safety and efficiency | +0.7% | Global | Short to Medium Term (2025-2029) |

Aircraft Nose Landing Gear Market Challenges Impact Analysis

The Aircraft Nose Landing Gear market faces significant challenges that can impede its development and operational efficiency. One primary challenge is the inherent complexity of integrating new and advanced technologies, such as smart sensors, AI-driven diagnostics, and electric actuators, into existing aircraft designs. This integration requires extensive testing, redesigns, and re-certification, leading to protracted development cycles and substantial cost implications for manufacturers.

Another critical challenge is the persistent shortage of a skilled workforce in both aerospace manufacturing and MRO sectors. The highly specialized nature of landing gear design, production, and maintenance demands highly trained engineers and technicians. A lack of adequate talent can lead to production bottlenecks, delays in service delivery, and increased operational costs. Furthermore, as landing gear systems become increasingly interconnected and intelligent, they become susceptible to cybersecurity risks, requiring robust protection measures to prevent unauthorized access or manipulation, which represents a continuous and evolving challenge for the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complexity of integrating new technologies into existing aircraft designs | -0.7% | Global | Long Term (2025-2033) |

| Skilled workforce shortage in aerospace manufacturing and MRO | -0.6% | Global | Long Term (2025-2033) |

| Cybersecurity risks for integrated smart systems | -0.5% | Global | Medium Term (2025-2030) |

| Balancing performance requirements with cost efficiency | -0.4% | Global | Long Term (2025-2033) |

| Long product development and certification cycles | -0.3% | Global | Long Term (2025-2033) |

Aircraft Nose Landing Gear Market - Updated Report Scope

This report provides a comprehensive analysis of the global Aircraft Nose Landing Gear market, encompassing historical data from 2019 to 2023 and offering detailed forecasts from 2025 to 2033. It examines market size, growth drivers, restraints, opportunities, and challenges, along with the impact of emerging technologies like AI. The scope includes in-depth segmentation by aircraft type, end-use, system type, material, and sales channel, providing a granular view of market dynamics across key regions and highlighting the competitive landscape with profiles of leading market participants.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 4.1 Billion |

| Market Forecast in 2033 | USD 7.0 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Safran S.A., Collins Aerospace (a Raytheon Technologies company), Liebherr-Aerospace, Heroux-Devtek Inc., AAR Corp., Triumph Group, Inc., Shimadzu Corporation, CIRCOR Aerospace & Defense, Eaton Corporation, Revima Group, Mecaer Aviation Group S.p.A., Parker Hannifin Corporation, Sumitomo Precision Products Co., Ltd., Whippany Actuation Systems, Inc., FACC AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Aircraft Nose Landing Gear market is meticulously segmented to provide a comprehensive understanding of its diverse components and drivers. This segmentation allows for a detailed analysis of specific market niches, identifying unique growth patterns and influencing factors across different applications and technologies. The primary classifications delineate the market based on the type of aircraft, the end-use sector, the specific system components, and the materials utilized in their construction.

Each segment offers distinct characteristics and growth trajectories. For instance, the commercial aircraft segment is driven by fleet expansion and replacement cycles, while the military segment is influenced by defense budgets and strategic procurements. Similarly, the OEM market reflects new aircraft production, whereas the aftermarket thrives on maintenance, repair, and overhaul demands for existing fleets. Understanding these interdependencies and individual segment dynamics is crucial for strategic planning and investment within the Aircraft Nose Landing Gear industry.

- By Aircraft Type:

- Commercial Aircraft (Narrow-body, Wide-body, Regional Jets)

- Military Aircraft (Fighters, Transports, Helicopters)

- Business Jets

- Regional Aircraft

- Helicopters

- Urban Air Mobility (UAM) / eVTOL

- By End-Use:

- Original Equipment Manufacturer (OEM)

- Aftermarket (MRO, Spares)

- By System Type:

- Retraction System

- Steering System

- Braking System

- Shock Absorption System

- Monitoring & Control System

- By Material:

- Aluminum Alloys

- Steel Alloys

- Titanium Alloys

- Composites

- By Sales Channel:

- Direct Sales

- Distribution Channels

Regional Highlights

- North America: This region dominates the Aircraft Nose Landing Gear market due to the presence of major aircraft manufacturers, significant defense spending, and a large existing commercial fleet requiring continuous MRO services. The United States, in particular, is a hub for aerospace innovation and production, contributing substantially to market demand and technological advancements.

- Europe: A mature market characterized by robust aerospace manufacturing capabilities, particularly in countries like France, Germany, and the UK. Europe benefits from strong R&D investments in advanced materials and smart systems, driven by initiatives like Clean Sky, which foster sustainable aviation technologies. The region’s aftermarket sector is also highly developed.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate, fueled by increasing air passenger traffic, rapid expansion of commercial fleets, and growing defense budgets in countries like China, India, and Japan. The region is witnessing significant investment in new airport infrastructure and domestic aircraft manufacturing capabilities, creating substantial demand for nose landing gear components.

- Latin America: This region presents emerging opportunities, driven by increasing air travel and fleet modernization efforts by regional airlines. While smaller in market size compared to North America or Europe, consistent investments in aviation infrastructure and a growing middle class contribute to steady demand for new aircraft and associated landing gear.

- Middle East and Africa (MEA): Characterized by significant investments in new aircraft by rapidly expanding airlines and a focus on building MRO capabilities, particularly in the Middle East. Strategic geographical location and growing tourism are also contributing to fleet expansion, thereby generating demand for nose landing gear. Defense spending in various countries further supports market growth in the region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aircraft Nose Landing Gear Market.- Safran S.A.

- Collins Aerospace (a Raytheon Technologies company)

- Liebherr-Aerospace

- Heroux-Devtek Inc.

- AAR Corp.

- Triumph Group, Inc.

- Shimadzu Corporation

- CIRCOR Aerospace & Defense

- Eaton Corporation

- Revima Group

- Mecaer Aviation Group S.p.A.

- Parker Hannifin Corporation

- Sumitomo Precision Products Co., Ltd.

- Whippany Actuation Systems, Inc.

- FACC AG

Frequently Asked Questions

Analyze common user questions about the Aircraft Nose Landing Gear market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate for the Aircraft Nose Landing Gear market?

The Aircraft Nose Landing Gear market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated USD 7.0 Billion by the end of the forecast period.

What are the primary drivers of the Aircraft Nose Landing Gear market?

Key drivers include the increase in global air passenger traffic, growing demand for new generation fuel-efficient aircraft, rising defense spending, and the substantial MRO needs of aging commercial aircraft fleets.

How is AI impacting the Aircraft Nose Landing Gear industry?

AI is transforming the industry through applications in predictive maintenance, generative design for weight optimization, automated manufacturing processes, and real-time health monitoring via advanced sensor data analysis.

Which regions are most significant for the Aircraft Nose Landing Gear market?

North America and Europe are established markets with strong manufacturing and MRO bases, while Asia Pacific is expected to demonstrate the highest growth due to fleet expansion and increased air travel.

What are the key technological trends in Aircraft Nose Landing Gear?

Significant trends include the adoption of lightweight and high-strength materials, integration of smart systems for monitoring, development of electric braking and e-taxi systems, and the increasing use of additive manufacturing.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted