Aircraft Insurance Market

Aircraft Insurance Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709467 | Last Updated : December 09, 2025 |

Format : ![]()

![]()

![]()

![]()

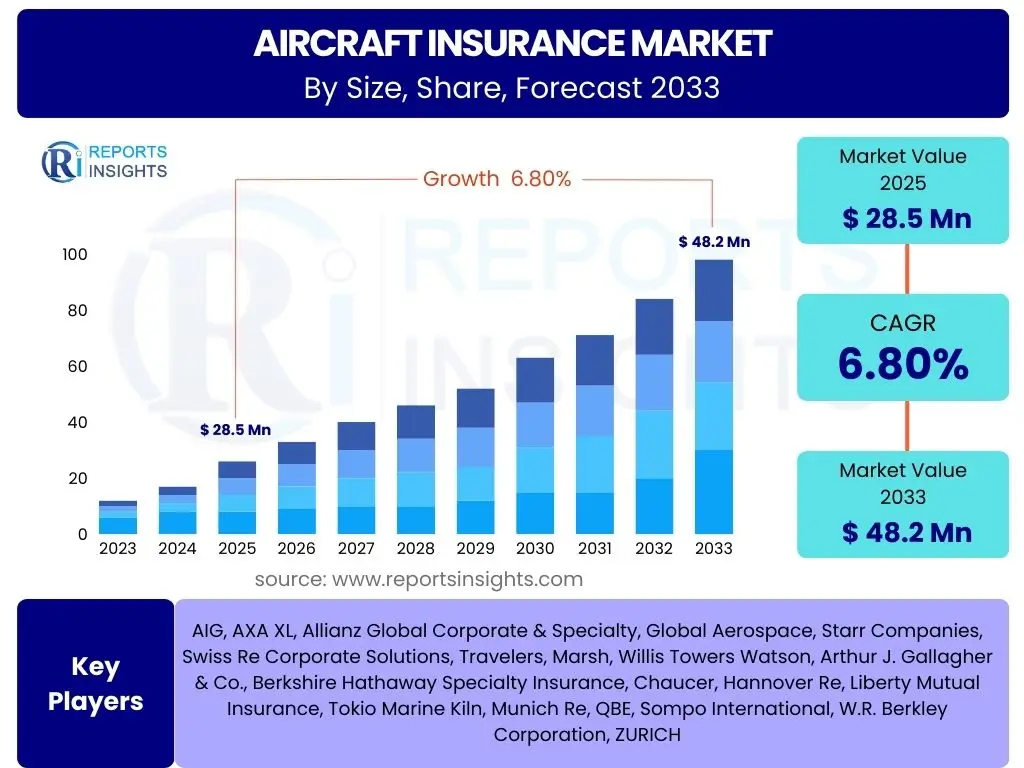

Aircraft Insurance Market Size

According to Reports Insights Consulting Pvt Ltd, The Aircraft Insurance Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 28.5 Billion in 2025 and is projected to reach USD 48.2 Billion by the end of the forecast period in 2033.

Key Aircraft Insurance Market Trends & Insights

The aircraft insurance market is experiencing significant evolution, driven by technological advancements, changing risk landscapes, and a global increase in air traffic. User inquiries frequently highlight the shift towards more sophisticated risk assessment models, the impact of digitalization on policy administration, and the increasing demand for specialized coverage for emerging aviation sectors like Urban Air Mobility (UAM) and unmanned aircraft systems (UAS). Concerns also revolve around the integration of cyber risks into traditional policies and the industry's response to environmental sustainability pressures.

Furthermore, there is a strong focus on how data analytics and artificial intelligence are revolutionizing underwriting processes, claims management, and pricing strategies, leading to more tailored and efficient insurance solutions. Stakeholders are keen to understand how insurers are adapting to the complexities of new aircraft technologies, including electric and hybrid propulsion systems, and the evolving regulatory frameworks that govern these innovations. The market is also keenly observing the expansion of aviation infrastructure in developing economies and its implications for insurance demand and product development.

- Digital transformation in policy administration and claims processing.

- Increasing adoption of advanced data analytics for precise risk assessment.

- Emergence of specialized insurance products for Urban Air Mobility (UAM) and Advanced Air Mobility (AAM).

- Growing integration of cyber risk coverage into standard aviation insurance policies.

- Emphasis on sustainable aviation practices influencing insurance premiums and coverage.

- Expansion of aviation infrastructure and fleet sizes in emerging economies.

AI Impact Analysis on Aircraft Insurance

User questions regarding the impact of Artificial Intelligence (AI) on aircraft insurance predominantly focus on its potential to enhance efficiency, accuracy, and personalized risk assessment. There is significant interest in how AI can streamline claims processing through automation, improve fraud detection capabilities, and facilitate predictive maintenance insights by analyzing vast datasets from aircraft operations. Common inquiries also touch upon the ethical implications of AI in decision-making, the necessity for robust data governance, and the potential for job displacement within the underwriting and claims departments.

The integration of AI is expected to revolutionize various facets of aircraft insurance, from initial policy issuance to post-incident analysis. It promises more dynamic pricing models based on real-time operational data, allowing for more granular risk segmentation and customized policy offerings. While concerns exist about the transparency of AI algorithms and the need for human oversight, the general expectation is that AI will enable insurers to manage complex risks more effectively, reduce operational costs, and offer more competitive and tailored insurance solutions to a rapidly evolving aviation sector.

- Enhanced risk assessment and underwriting through advanced data analysis.

- Automated and expedited claims processing reducing settlement times.

- Improved fraud detection capabilities leveraging pattern recognition.

- Predictive maintenance insights leading to reduced incident rates and claims.

- Development of dynamic pricing models based on real-time operational data.

- Increased operational efficiency and cost reduction for insurers.

Key Takeaways Aircraft Insurance Market Size & Forecast

Analysis of common user questions regarding the Aircraft Insurance market size and forecast reveals a strong emphasis on understanding the primary growth drivers, the resilience of the market against external shocks, and the key regions poised for significant expansion. Stakeholders are particularly interested in how the market is adapting to technological disruptions and evolving regulatory landscapes. There is a clear demand for insights into the long-term sustainability of growth given geopolitical uncertainties and the increasing focus on environmental factors.

The market is characterized by steady growth, primarily fueled by the increasing global demand for air travel, the expansion of commercial and general aviation fleets, and the advent of new aviation technologies requiring specialized coverage. The forecast indicates that while established markets like North America and Europe will continue to be significant, the Asia Pacific region is expected to demonstrate robust growth due to rapid infrastructure development and increasing aircraft procurement. Insurers capable of innovating their product offerings and leveraging advanced analytics will be best positioned to capitalize on these trends.

- Consistent growth trajectory driven by expanding global air travel and fleet modernization.

- Technological innovation, including UAM and UAS, serves as a significant growth catalyst.

- Asia Pacific region identified as a key growth hub due to aviation infrastructure development.

- Risk management and specialized coverage for evolving threats remain critical.

- Digital transformation and AI adoption are essential for competitive advantage.

Aircraft Insurance Market Drivers Analysis

The Aircraft Insurance market is propelled by a confluence of factors, prominently including the sustained increase in global air passenger and cargo traffic. This growth necessitates the expansion and modernization of aircraft fleets, directly translating to higher demand for comprehensive insurance coverage. Furthermore, continuous technological advancements in aircraft design and manufacturing, leading to more sophisticated and valuable assets, require advanced and specialized insurance products to cover enhanced risks and complexities.

Additionally, the rigorous and continuously evolving regulatory frameworks imposed by aviation authorities worldwide mandate comprehensive insurance for aircraft operations, ensuring safety and financial protection against liabilities. The growing demand for general aviation and business jets, alongside the burgeoning maintenance, repair, and overhaul (MRO) sector, further stimulates the market. These factors collectively create a robust environment for sustained market expansion, pushing insurers to innovate and adapt their offerings.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global increase in air travel and cargo demand | +1.8% | Global, particularly APAC and North America | Long-term |

| Expansion and modernization of commercial and general aviation fleets | +1.5% | Global | Mid- to Long-term |

| Technological advancements in aircraft design and manufacturing | +1.2% | North America, Europe, China | Mid-term |

| Stringent and evolving aviation regulatory frameworks | +1.0% | Global | Ongoing |

| Growth in the Maintenance, Repair, and Overhaul (MRO) sector | +0.8% | Global | Mid- to Long-term |

Aircraft Insurance Market Restraints Analysis

Despite robust growth drivers, the Aircraft Insurance market faces several notable restraints that can impede its expansion. One significant factor is the high capital intensity and operational costs associated with aviation, which can limit fleet expansion for some operators, thereby dampening insurance demand. Moreover, the stringent and ever-evolving regulatory landscape, while a driver for mandatory insurance, can also be a restraint due to the complex compliance burden it places on both operators and insurers, requiring substantial resources and expertise.

Geopolitical instability and regional conflicts represent a continuous threat, leading to elevated war risk premiums and potential exclusions, which can increase the overall cost of insurance or limit coverage in affected areas. Economic downturns globally or regionally can significantly reduce air travel and cargo volumes, directly impacting airline profitability and their ability to invest in new aircraft or maintain existing fleets, consequently affecting insurance market revenues. Furthermore, the inherent volatility of insurance premiums, driven by market capacity and claims experience, can create uncertainty for aviation businesses planning their operational budgets.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High capital requirements and operational costs for aviation operators | -0.9% | Global | Mid- to Long-term |

| Stringent and complex regulatory compliance burden | -0.7% | Global | Ongoing |

| Geopolitical instability and regional conflicts | -0.8% | Specific regions (e.g., Middle East, Eastern Europe) | Short- to Mid-term |

| Economic downturns affecting air travel demand | -1.1% | Global, varies by region | Short- to Mid-term |

| Premium volatility due to high-value claims and market capacity fluctuations | -0.6% | Global | Short- to Mid-term |

Aircraft Insurance Market Opportunities Analysis

The Aircraft Insurance market is ripe with opportunities stemming from the rapid advancements and diversification within the aviation sector. A significant area of growth lies in the emerging Urban Air Mobility (UAM) and Advanced Air Mobility (AAM) markets, encompassing air taxis, delivery drones, and other innovative aerial vehicles. These new segments present novel risk profiles, driving demand for entirely new and specialized insurance products that cater to their unique operational complexities, regulatory environments, and liability structures.

The increasing adoption of Unmanned Aircraft Systems (UAS) across various industries—from logistics and agriculture to surveillance and infrastructure inspection—also creates a substantial opportunity for insurers to develop tailored drone insurance policies. Furthermore, the expansion of aviation infrastructure in developing economies, particularly in the Asia Pacific and Latin American regions, signifies an untapped market for insurance services as new airlines emerge and existing fleets grow. The integration of cyber insurance policies specifically designed to address the growing cyber threats to interconnected aircraft systems and ground operations represents another critical growth avenue, as does leveraging data analytics for more refined risk assessment and personalized insurance offerings.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of Urban Air Mobility (UAM) and Advanced Air Mobility (AAM) | +1.5% | North America, Europe, Asia Pacific | Mid- to Long-term |

| Increasing adoption of Unmanned Aircraft Systems (UAS) across industries | +1.3% | Global | Mid- to Long-term |

| Expansion into developing aviation markets (e.g., APAC, Latin America) | +1.2% | Asia Pacific, Latin America, Africa | Long-term |

| Integration of cyber insurance policies for aviation systems | +1.0% | Global | Mid-term |

| Leveraging data analytics for tailored and personalized insurance policies | +0.9% | Global | Ongoing |

Aircraft Insurance Market Challenges Impact Analysis

The Aircraft Insurance market faces a complex array of challenges that necessitate innovative responses from industry stakeholders. A primary concern is the escalating risk of climate change and natural disasters, which can lead to increased frequency and severity of weather-related incidents, impacting aircraft and airport infrastructure, and consequently, claims. This necessitates a re-evaluation of risk models and policy terms to adequately address these evolving environmental threats.

Furthermore, the rapid pace of technological innovation, particularly with new aircraft types and autonomous systems, creates an evolving regulatory landscape that insurers must constantly adapt to. This includes challenges in accurately assessing new and untested risks. The persistent global shortage of skilled aviation personnel, including pilots, maintenance technicians, and air traffic controllers, can contribute to operational errors and accidents, thereby increasing insurable risks. Additionally, global supply chain disruptions can delay aircraft repairs and increase costs, impacting claims duration and magnitude. Finally, ensuring robust data security and privacy in an increasingly interconnected aviation ecosystem is a critical challenge, as cyber-attacks can compromise operational integrity and lead to significant financial and reputational damages for all parties involved.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Climate change risks and increased frequency of natural disasters | -1.0% | Global, particularly coastal and high-risk zones | Long-term |

| Evolving regulatory landscape for new aviation technologies | -0.8% | Global | Ongoing |

| Pilot and skilled personnel shortages in the aviation sector | -0.7% | Global, particularly North America, Europe | Mid- to Long-term |

| Global supply chain disruptions impacting aircraft repair and maintenance | -0.9% | Global | Short- to Mid-term |

| Ensuring data security and privacy in interconnected aviation systems | -0.6% | Global | Ongoing |

Aircraft Insurance Market - Updated Report Scope

This report offers a comprehensive analysis of the Aircraft Insurance market, covering key market dynamics, segmentation, regional insights, and the competitive landscape. It provides an in-depth assessment of market size, growth trends, and future projections, incorporating the impact of technological advancements and evolving regulatory environments. The scope extends to analyzing drivers, restraints, opportunities, and challenges that shape the market, providing stakeholders with critical intelligence for strategic decision-making and market positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 28.5 Billion |

| Market Forecast in 2033 | USD 48.2 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | AIG, AXA XL, Allianz Global Corporate & Specialty, Global Aerospace, Starr Companies, Swiss Re Corporate Solutions, Travelers, Marsh, Willis Towers Watson, Arthur J. Gallagher & Co., Berkshire Hathaway Specialty Insurance, Chaucer, Hannover Re, Liberty Mutual Insurance, Tokio Marine Kiln, Munich Re, QBE, Sompo International, W.R. Berkley Corporation, ZURICH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Aircraft Insurance market is comprehensively segmented to provide granular insights into its various components, allowing for a detailed understanding of market dynamics and growth opportunities across different categories. This segmentation is crucial for stakeholders to identify specific market niches, understand demand patterns, and tailor their product and service offerings to meet diverse client needs within the aviation industry. The market is primarily analyzed based on the type of insurance coverage offered, the application segment it serves, and the end-users requiring these specialized policies, each with distinct risk profiles and requirements.

This multi-dimensional segmentation facilitates a robust analysis of market penetration and future growth potential for each category. For instance, the Hull Insurance segment caters to physical damage to aircraft, while Liability Insurance covers third-party damages and injuries. The rise of new applications like Unmanned Aircraft Systems (UAS) necessitates distinct coverage types compared to traditional commercial aviation. Similarly, the varying operational scales and risk exposures of different end-users, from major airlines to private jet operators and MRO providers, dictate unique insurance demands and market responses, shaping the competitive landscape within each segment.

- By Type: Hull Insurance, Liability Insurance, Passenger Liability Insurance, War Risk Insurance, Others.

- By Application: Commercial Aviation, General Aviation, Private Aviation, Unmanned Aircraft Systems (UAS).

- By End-User: Airlines, Airport Operators, Aircraft Manufacturers, Maintenance, Repair, and Overhaul (MRO) Providers, Corporate Jet Operators, Others.

Regional Highlights

- North America: This region holds a significant share of the aircraft insurance market, characterized by a mature aviation industry, a large fleet of commercial and general aviation aircraft, and a strong presence of key market players. High adoption rates of advanced technologies and stringent regulatory frameworks contribute to sustained demand.

- Europe: A well-established market with a robust regulatory environment and a high concentration of major airlines and aerospace manufacturers. The region exhibits strong demand for comprehensive insurance solutions, with an increasing focus on sustainability and compliance with evolving EU regulations.

- Asia Pacific (APAC): Expected to be the fastest-growing region, driven by rapid economic growth, increasing air passenger traffic, significant investments in new airport infrastructure, and the expansion of commercial and general aviation fleets, particularly in China and India.

- Latin America: This region is experiencing steady growth in its aviation sector, leading to increased demand for aircraft insurance. Market expansion is supported by growing tourism and business travel, albeit with challenges related to economic volatility and infrastructure development.

- Middle East and Africa (MEA): Characterized by significant investments in airline expansion, particularly in the Middle East, fueled by strategic geographical positioning for international travel. Africa's aviation sector is also growing, though at a slower pace, presenting long-term opportunities as infrastructure improves.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aircraft Insurance Market.- AIG

- AXA XL

- Allianz Global Corporate & Specialty

- Global Aerospace

- Starr Companies

- Swiss Re Corporate Solutions

- Travelers

- Marsh

- Willis Towers Watson

- Arthur J. Gallagher & Co.

- Berkshire Hathaway Specialty Insurance

- Chaucer

- Hannover Re

- Liberty Mutual Insurance

- Tokio Marine Kiln

- Munich Re

- QBE

- Sompo International

- W.R. Berkley Corporation

- ZURICH

Frequently Asked Questions

What types of aircraft insurance are available?

Aircraft insurance generally includes hull insurance, which covers physical damage to the aircraft, and liability insurance, which protects against claims from third-party injury or property damage. Additional coverages like passenger liability and war risk are also common.

Who needs aircraft insurance?

Anyone who owns, operates, or charters an aircraft, including commercial airlines, private plane owners, general aviation operators, corporate jet fleets, and drone operators, typically requires aircraft insurance to comply with regulations and protect against financial risks.

How are aircraft insurance premiums calculated?

Premiums are determined by various factors, including the type and value of the aircraft, its intended use (commercial, private), the pilot's experience and qualifications, operating regions, claims history, and specific coverage limits and deductibles selected.

What is the impact of new aviation technologies like drones and UAM on the insurance market?

New technologies like drones and Urban Air Mobility (UAM) are creating demand for specialized insurance products to cover novel risks such as autonomous flight liability, cyber threats, and unique operational environments, driving innovation in policy design and risk assessment.

What are the primary challenges facing the aircraft insurance market?

Key challenges include evolving climate change risks, adapting to new aviation regulations, managing global supply chain disruptions affecting repairs, the increasing complexity of cyber threats, and addressing pilot and skilled personnel shortages.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted