Aerospace Part Market

Aerospace Part Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710244 | Last Updated : January 02, 2026 |

Format : ![]()

![]()

![]()

![]()

Aerospace Part Market Size

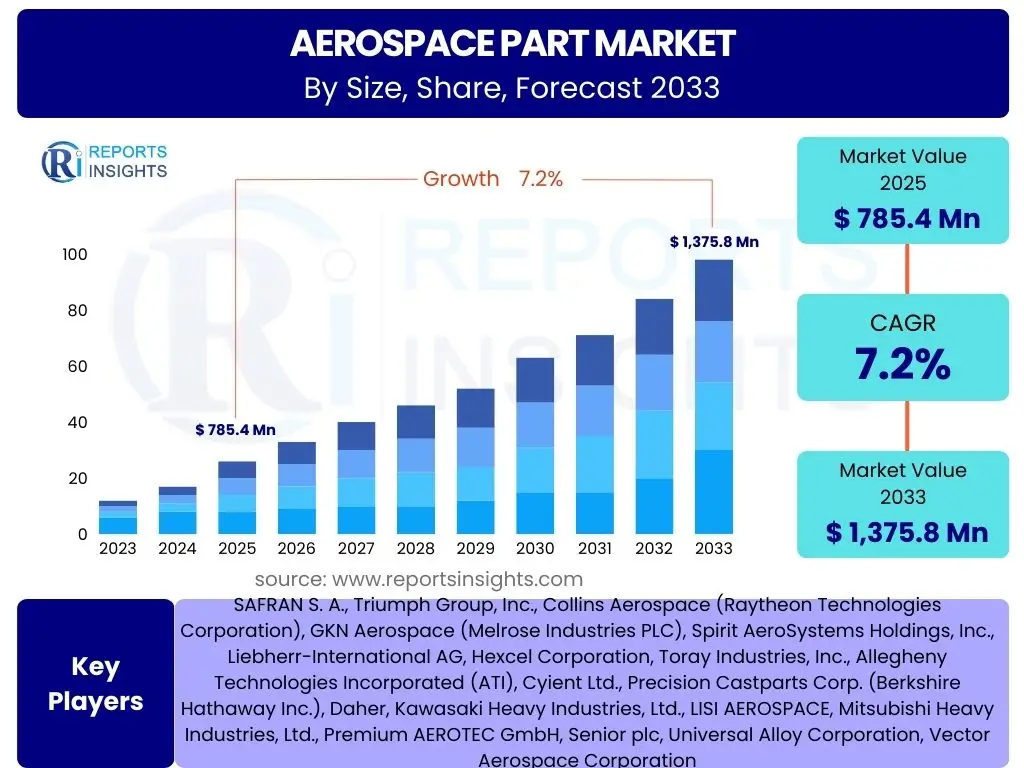

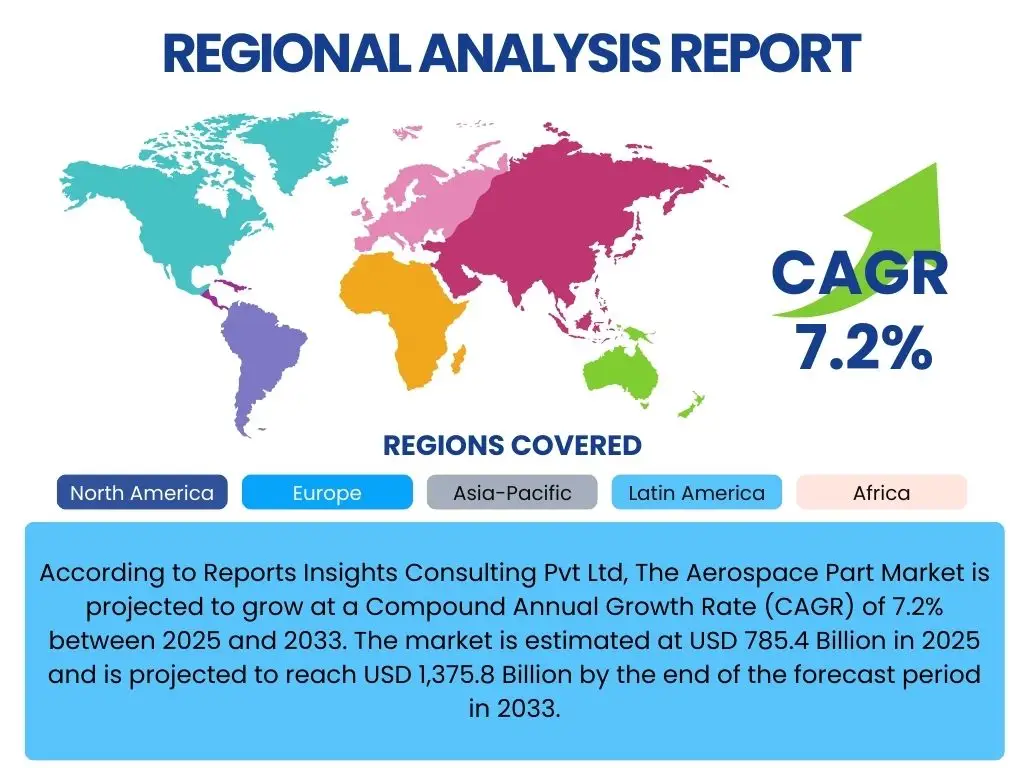

According to Reports Insights Consulting Pvt Ltd, The Aerospace Part Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.2% between 2025 and 2033. The market is estimated at USD 785.4 Billion in 2025 and is projected to reach USD 1,375.8 Billion by the end of the forecast period in 2033.

Key Aerospace Part Market Trends & Insights

The Aerospace Part market is witnessing transformative shifts driven by technological advancements, evolving global demand, and a heightened focus on sustainability. User queries frequently revolve around the adoption of advanced manufacturing techniques, the integration of smart technologies, and the impact of environmental regulations on part design and production. Key trends indicate a robust demand for lightweight, durable, and high-performance components, propelled by an increasing global air passenger traffic, expanding defense budgets, and the sustained growth of maintenance, repair, and overhaul (MRO) activities.

Manufacturers are increasingly investing in research and development to innovate materials and production processes, seeking to reduce operational costs, enhance fuel efficiency, and minimize environmental footprint. The market is also experiencing a surge in demand for specialized parts catering to next-generation aircraft, including electric and hybrid-electric propulsion systems, and advanced air mobility (AAM) platforms. Furthermore, supply chain resilience and localization strategies are becoming critical, addressing past vulnerabilities and ensuring consistent material and component availability in a complex global geopolitical landscape.

- Additive manufacturing (3D printing) adoption for complex geometries and on-demand production.

- Increasing demand for lightweight and high-performance composite materials.

- Digitalization across the product lifecycle, from design to MRO, leveraging digital twins and predictive analytics.

- Growing emphasis on sustainable materials and eco-friendly manufacturing processes.

- Electrification of aircraft and the development of parts for electric propulsion systems.

- Enhanced focus on supply chain resilience and regional manufacturing hubs.

AI Impact Analysis on Aerospace Part

The integration of Artificial Intelligence (AI) into the Aerospace Part sector is a prominent subject of user inquiry, reflecting significant expectations for improved efficiency, quality, and innovation. Users are keen to understand how AI can optimize design processes, enhance predictive maintenance capabilities, streamline manufacturing operations, and bolster supply chain management. AI's ability to analyze vast datasets is proving instrumental in identifying complex patterns for material science, aerodynamic optimization, and component longevity, thereby reducing development cycles and improving product performance.

AI-driven solutions are also transforming quality control by enabling automated defect detection and inspection, ensuring higher precision and consistency in aerospace parts. In the realm of MRO, AI algorithms predict component failures, allowing for proactive maintenance and minimizing unscheduled downtime, which is critical for airline operations. Furthermore, generative design, powered by AI, allows engineers to explore thousands of design permutations for optimal weight, strength, and functionality, pushing the boundaries of traditional design methodologies and fostering the creation of highly efficient, customized parts.

- AI-powered generative design optimizes part geometries for weight and performance.

- Predictive maintenance analytics enhance part reliability and reduce unscheduled downtime.

- Automated visual inspection and quality control systems improve manufacturing accuracy.

- Supply chain optimization through AI for demand forecasting and inventory management.

- Robotics and AI integration in advanced manufacturing for improved precision and speed.

Key Takeaways Aerospace Part Market Size & Forecast

Analysis of common user questions regarding the Aerospace Part market size and forecast reveals a strong interest in understanding the primary growth drivers, the longevity of the market expansion, and the regional dynamics contributing to its trajectory. The market is underpinned by a robust increase in global air travel, significant investments in defense and space programs, and the continuous innovation in aircraft technology. The consistent growth projected over the next decade underscores the resilient nature of the aerospace industry, even in the face of cyclical economic pressures.

A significant takeaway is the pivotal role of technological advancements, particularly in lightweight materials, advanced manufacturing, and digitalization, in shaping future market demand and supply. The forecast indicates that while commercial aviation will remain a dominant segment, the burgeoning space sector and the emergence of urban air mobility (UAM) platforms will introduce new avenues for specialized part manufacturing. Moreover, understanding the interplay between geopolitical stability, supply chain efficiency, and regulatory frameworks is crucial for stakeholders to capitalize on the growth opportunities and mitigate potential risks within this dynamic market.

- The market exhibits substantial long-term growth driven by commercial aviation, defense, and space.

- Technological innovation, especially in materials and manufacturing, is critical for competitive advantage.

- Asia Pacific and North America are poised to remain leading regions, with significant MRO and manufacturing activities.

- Sustainability and fuel efficiency are increasingly influencing part design and material selection.

- Investments in research and development for next-generation aircraft components are paramount for market players.

Aerospace Part Market Drivers Analysis

The Aerospace Part market's expansion is fundamentally propelled by several interconnected factors that create sustained demand across the aviation and defense sectors. A primary driver is the consistent increase in global air passenger traffic, which necessitates the expansion of aircraft fleets and, consequently, boosts the demand for new aircraft parts and ongoing maintenance components. Additionally, substantial defense spending by major global powers, aimed at modernizing existing fleets and developing advanced military aircraft, ensures a steady influx of orders for specialized aerospace parts. Technological advancements, particularly in material science and manufacturing processes, enable the production of lighter, stronger, and more fuel-efficient parts, driving replacement cycles and innovation.

Furthermore, the robust growth of the Maintenance, Repair, and Overhaul (MRO) sector significantly contributes to market expansion. As aircraft fleets age and operational hours accumulate, the need for regular inspections, repairs, and component replacements escalates. This creates a perpetual demand for spare parts, ranging from engine components to structural elements and avionics. The emergence of new aircraft programs, including next-generation commercial jets and futuristic urban air mobility vehicles, also provides a long-term growth trajectory for part manufacturers, as these platforms require entirely new sets of components designed with cutting-edge technologies and performance specifications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Air Passenger Traffic | +2.5% | Global, particularly APAC, North America | Long-term (2025-2033) |

| Rising Defense Budgets and Aircraft Modernization | +1.8% | North America, Europe, Asia Pacific (China, India) | Mid to Long-term (2025-2033) |

| Growth in Maintenance, Repair, and Overhaul (MRO) Activities | +1.5% | Global, especially established aviation markets | Continuous |

| Technological Advancements in Materials and Manufacturing | +1.4% | Global, R&D-intensive regions | Mid to Long-term (2025-2033) |

| New Aircraft Program Developments | +1.0% | North America, Europe, China | Long-term (Post-2027) |

Aerospace Part Market Restraints Analysis

Despite significant growth prospects, the Aerospace Part market faces several formidable restraints that can impede its full potential. One major challenge is the inherent cyclical nature of the aerospace industry, which is highly susceptible to global economic downturns, geopolitical tensions, and unforeseen events such as pandemics. These factors can lead to reduced air travel, deferred aircraft orders, and decreased MRO activities, directly impacting the demand for aerospace parts. Furthermore, the aerospace supply chain is notoriously complex and globalized, making it vulnerable to disruptions stemming from trade disputes, natural disasters, and logistical bottlenecks, which can cause significant delays and cost escalations.

Another significant restraint is the extremely high cost associated with research, development, and certification of new aerospace parts. Adherence to stringent regulatory standards and safety protocols requires extensive testing, validation, and documentation, demanding substantial capital investment and prolonged lead times. This not only increases the financial burden on manufacturers but also creates a high barrier to entry for new players. Additionally, the increasing focus on environmental regulations and sustainability, while driving innovation, can also impose significant costs on manufacturers to transition to greener materials and production methods, potentially slowing down growth in the short to medium term due to compliance expenses and retooling requirements.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Economic Volatility and Geopolitical Instability | -1.2% | Global | Short to Mid-term (2025-2027) |

| High R&D and Certification Costs | -0.9% | Global, particularly developed economies | Continuous |

| Complex and Fragile Supply Chains | -0.8% | Global | Short to Mid-term (2025-2028) |

| Stringent Regulatory Compliance and Environmental Mandates | -0.7% | Europe, North America | Mid-term (2026-2030) |

| Technological Obsolescence for Legacy Systems | -0.5% | Global | Long-term (2029-2033) |

Aerospace Part Market Opportunities Analysis

The Aerospace Part market is replete with significant opportunities stemming from evolving technological landscapes and emerging market demands. The burgeoning adoption of additive manufacturing, or 3D printing, presents a transformative opportunity, enabling the production of complex, lightweight parts with reduced lead times and material waste. This technology facilitates rapid prototyping, customization, and on-demand production, which is particularly beneficial for specialized and low-volume components. Furthermore, the global push towards sustainable aviation is opening doors for manufacturers specializing in eco-friendly materials, such as advanced composites and bio-based plastics, and for those developing parts optimized for electric and hydrogen propulsion systems, addressing the industry's carbon footprint reduction goals.

Digitalization and the integration of Industry 4.0 technologies throughout the aerospace supply chain also represent a substantial opportunity. This includes the implementation of digital twins for enhanced design and maintenance, predictive analytics for operational efficiency, and advanced robotics for automated manufacturing. Such innovations can dramatically improve productivity, reduce errors, and optimize asset utilization. Moreover, the rapid expansion of the space industry, driven by commercial space ventures, satellite constellations, and lunar/Martian missions, is creating new, high-growth niches for specialized, extreme-environment aerospace parts. Emerging markets, especially in Asia Pacific, continue to witness substantial growth in air travel and defense spending, providing fertile ground for market penetration and expansion for part manufacturers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption of Additive Manufacturing (3D Printing) | +1.8% | Global | Mid to Long-term (2026-2033) |

| Development of Sustainable Aviation Materials and Technologies | +1.5% | Europe, North America | Long-term (2027-2033) |

| Growth in Commercial Space and Urban Air Mobility (UAM) Sectors | +1.3% | North America, Europe, China | Mid to Long-term (2026-2033) |

| Digital Transformation and Industry 4.0 Integration in Manufacturing | +1.1% | Global | Continuous |

| Market Expansion in Emerging Economies (e.g., APAC) | +0.9% | Asia Pacific, Latin America, Middle East & Africa | Long-term (2025-2033) |

Aerospace Part Market Challenges Impact Analysis

The Aerospace Part market, while experiencing significant growth, is not immune to considerable challenges that can hinder progress and profitability. One pervasive challenge is the persistent shortage of skilled labor, including engineers, machinists, and technicians, which impacts manufacturing capacity, innovation, and the ability to scale production. This shortage is exacerbated by an aging workforce and a relatively low influx of new talent, particularly in specialized areas like advanced composites and additive manufacturing. Addressing this requires significant investment in training and education programs, which can be a long-term endeavor.

Another critical challenge is cybersecurity, as the increasing digitalization of aerospace manufacturing and supply chains creates vulnerabilities to cyberattacks. Data breaches, intellectual property theft, and disruption of operational technology systems pose substantial risks to manufacturers, potentially leading to financial losses, reputational damage, and compromised safety. Furthermore, the volatility in raw material prices, such as aluminum, titanium, and carbon fiber, can significantly impact production costs and profit margins for aerospace part manufacturers. Geopolitical tensions and trade protectionism can also disrupt the global supply chain, causing delays and increasing the cost of essential materials and components, necessitating robust risk management and diversification strategies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Skilled Labor Shortage | -1.0% | North America, Europe | Long-term (2025-2033) |

| Cybersecurity Threats to Digitalized Supply Chains | -0.8% | Global | Continuous |

| Raw Material Price Volatility | -0.7% | Global | Short to Mid-term (2025-2028) |

| Complex and Evolving Regulatory Compliance | -0.6% | Global | Continuous |

| Supply Chain Resilience and Geopolitical Risks | -0.5% | Global | Short to Mid-term (2025-2027) |

Aerospace Part Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Aerospace Part market, covering key growth drivers, challenges, opportunities, and emerging trends from 2019 to 2033. It offers a detailed segmentation analysis based on product type, aircraft type, application, and material, providing granular insights into various market segments. The report includes a robust regional analysis, highlighting market dynamics across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa, complemented by a competitive landscape assessment of key industry players. This updated scope ensures a thorough understanding of the current market state and future projections, assisting stakeholders in strategic decision-making and investment planning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 785.4 Billion |

| Market Forecast in 2033 | USD 1,375.8 Billion |

| Growth Rate | 7.2% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | SAFRAN S. A., Triumph Group, Inc., Collins Aerospace (Raytheon Technologies Corporation), GKN Aerospace (Melrose Industries PLC), Spirit AeroSystems Holdings, Inc., Liebherr-International AG, Hexcel Corporation, Toray Industries, Inc., Allegheny Technologies Incorporated (ATI), Cyient Ltd., Precision Castparts Corp. (Berkshire Hathaway Inc.), Daher, Kawasaki Heavy Industries, Ltd., LISI AEROSPACE, Mitsubishi Heavy Industries, Ltd., Premium AEROTEC GmbH, Senior plc, Universal Alloy Corporation, Vector Aerospace Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Aerospace Part market is comprehensively segmented to provide a detailed understanding of its diverse components and dynamics. This segmentation allows for precise analysis of various product categories, types of aircraft served, end-user applications, and the materials utilized in manufacturing. Such a granular breakdown is essential for identifying specific growth pockets, understanding technological shifts within sub-sectors, and formulating targeted business strategies. The analysis highlights how different segments contribute to the overall market growth, influenced by factors such as aircraft production rates, technological advancements, and MRO demands.

Understanding these segments provides clarity on where investments are being directed and which areas are experiencing the most rapid innovation. For instance, the OEM segment is driven by new aircraft deliveries, while the aftermarket is sustained by the existing fleet's operational needs. Similarly, the shift towards lightweight composite materials impacts the material segment, reflecting the industry's focus on fuel efficiency and performance. Each segment's unique characteristics and growth trajectories offer invaluable insights for stakeholders looking to navigate this complex and dynamic market landscape effectively.

- By Product Type: This segment categorizes parts into aerostructure, engine, interiors, and system & equipment components, reflecting the diverse functional areas within an aircraft.

- By Aircraft Type: This segment differentiates parts based on the type of aircraft they are designed for, including commercial, military, business jets, rotorcraft, UAVs, and spacecraft, each with unique requirements.

- By Application: This segment distinguishes between parts supplied to Original Equipment Manufacturers (OEMs) for new aircraft production and those supplied to the aftermarket for Maintenance, Repair, and Overhaul (MRO).

- By Material: This segment examines the various materials used in part manufacturing, such as metals (aluminum, titanium, steel, nickel alloys), composites (carbon fiber, glass fiber), plastics, and ceramics, driven by performance and weight considerations.

Regional Highlights

- North America: Dominates the market due to robust defense spending, a large installed base of commercial aircraft, and significant R&D investments in advanced aerospace technologies. The presence of major OEMs and Tier 1 suppliers further solidifies its leading position.

- Europe: A strong market driven by key aerospace manufacturers, active participation in military aircraft programs, and a growing focus on sustainable aviation. Countries like France, Germany, and the UK are major contributors to both OEM and MRO segments.

- Asia Pacific (APAC): Expected to exhibit the highest growth rate, fueled by increasing air passenger traffic, expanding commercial aircraft fleets, rising defense expenditures, and growing manufacturing capabilities, particularly in China and India.

- Latin America: A growing market with increasing demand for new aircraft and MRO services, primarily driven by fleet modernization and expanding regional air connectivity, albeit from a smaller base.

- Middle East & Africa (MEA): Shows promising growth propelled by significant investments in new aircraft by prominent airlines and strategic initiatives to establish regional MRO hubs, enhancing its position in the global aerospace value chain.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aerospace Part Market.- SAFRAN S. A.

- Triumph Group, Inc.

- Collins Aerospace (Raytheon Technologies Corporation)

- GKN Aerospace (Melrose Industries PLC)

- Spirit AeroSystems Holdings, Inc.

- Liebherr-International AG

- Hexcel Corporation

- Toray Industries, Inc.

- Allegheny Technologies Incorporated (ATI)

- Cyient Ltd.

- Precision Castparts Corp. (Berkshire Hathaway Inc.)

- Daher

- Kawasaki Heavy Industries, Ltd.

- LISI AEROSPACE

- Mitsubishi Heavy Industries, Ltd.

- Premium AEROTEC GmbH

- Senior plc

- Universal Alloy Corporation

- Vector Aerospace Corporation

- Aernnova Aerospace S.A.

Frequently Asked Questions

What factors are driving the growth of the Aerospace Part market?

The Aerospace Part market is primarily driven by increasing global air passenger traffic, growing defense budgets for aircraft modernization, sustained expansion of Maintenance, Repair, and Overhaul (MRO) activities, and continuous technological advancements in materials and manufacturing processes.

How is additive manufacturing impacting the production of aerospace parts?

Additive manufacturing, or 3D printing, is significantly impacting aerospace part production by enabling the creation of complex, lightweight geometries, reducing material waste, facilitating rapid prototyping, and allowing for on-demand manufacturing of specialized components, thereby enhancing efficiency and design flexibility.

Which regions are key contributors to the Aerospace Part market?

North America and Europe are major contributors due to established aerospace industries and significant defense spending. The Asia Pacific region is expected to show the highest growth, driven by increasing air travel demand and expanding manufacturing capabilities, particularly in China and India.

What are the major challenges faced by manufacturers in the Aerospace Part market?

Key challenges include a persistent skilled labor shortage, the high costs and stringent regulations associated with R&D and certification, vulnerability of complex global supply chains to disruptions, and the imperative to manage raw material price volatility effectively.

What role does AI play in the Aerospace Part industry?

AI plays a transformative role by optimizing part design through generative AI, enhancing predictive maintenance with advanced analytics, improving manufacturing quality control via automated inspection, and streamlining supply chain management through intelligent forecasting and logistics optimization.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted