Aerospace and Defense Actuator Market

Aerospace and Defense Actuator Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701249 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

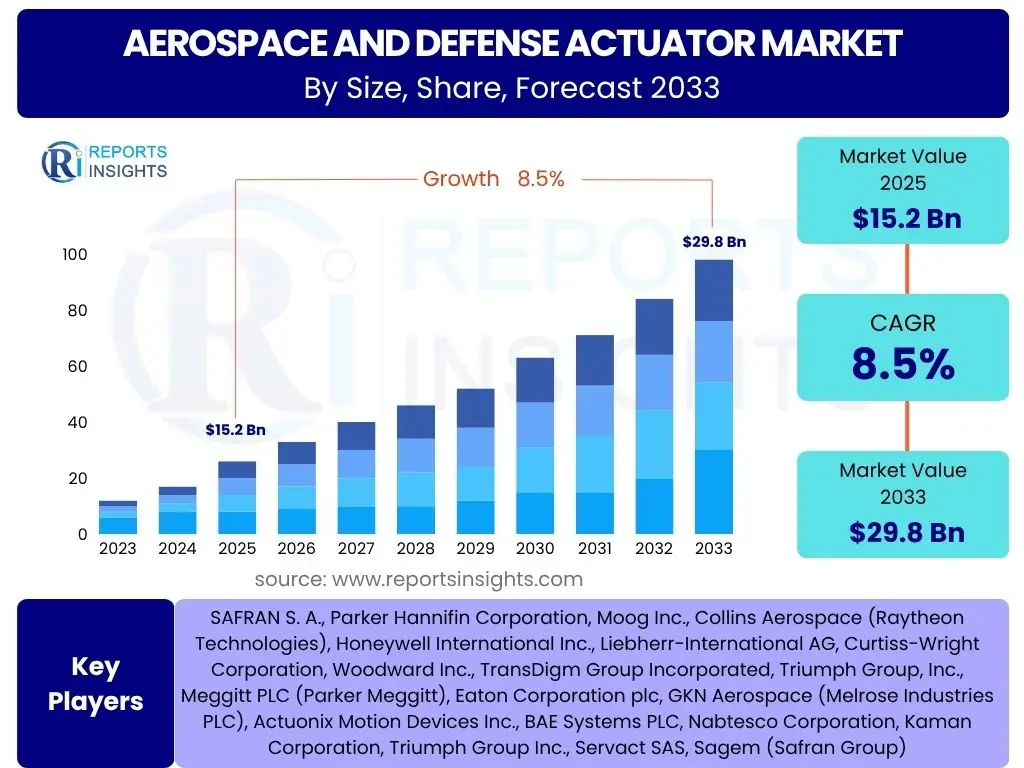

Aerospace and Defense Actuator Market Size

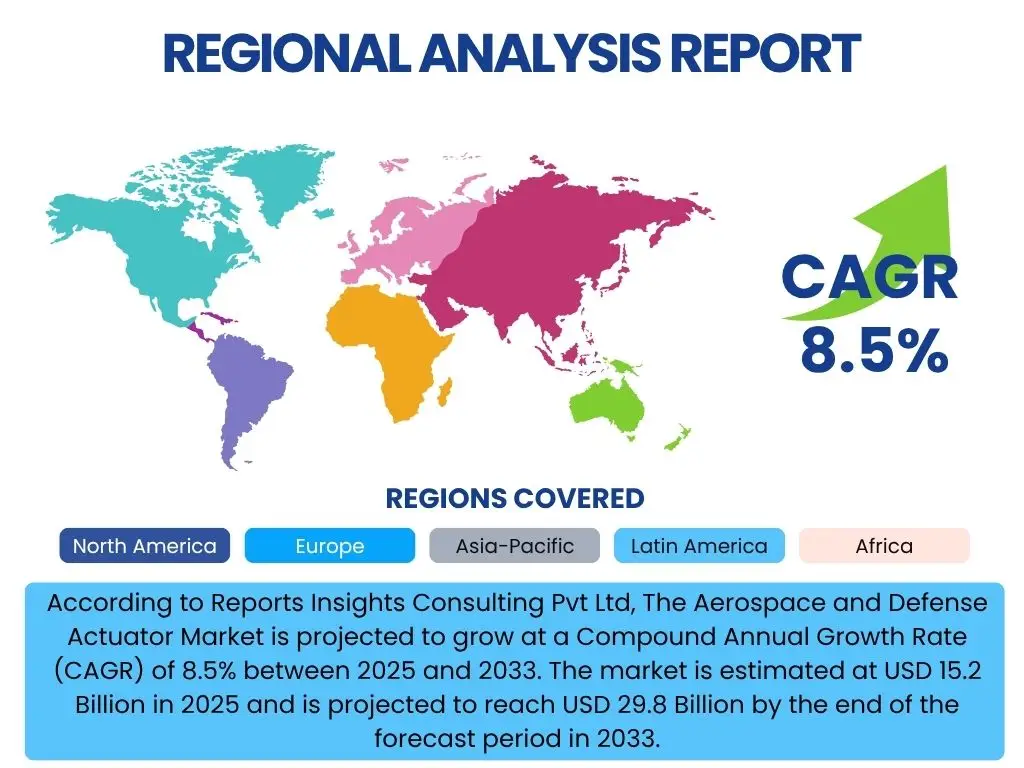

According to Reports Insights Consulting Pvt Ltd, The Aerospace and Defense Actuator Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 15.2 Billion in 2025 and is projected to reach USD 29.8 Billion by the end of the forecast period in 2033.

Key Aerospace and Defense Actuator Market Trends & Insights

The aerospace and defense actuator market is experiencing significant transformation, driven by technological advancements and evolving operational requirements. Users frequently inquire about the adoption of more electric aircraft (MEA) architectures, the increasing integration of smart and connected actuators, and the growing emphasis on lightweight materials and miniaturization. These trends reflect a broader industry push towards enhanced efficiency, reduced maintenance, and improved performance across both commercial and military applications.

Furthermore, there is a strong interest in how digital technologies, such as predictive maintenance and condition monitoring, are being applied to actuator systems. This allows for proactive identification of potential failures, significantly improving operational safety and reducing downtime. The market is also seeing a shift towards modular and standardized actuator designs, facilitating easier integration and maintenance within complex aerospace and defense platforms.

- Transition towards More Electric Aircraft (MEA) systems enhancing efficiency.

- Increased demand for smart and connected actuators with integrated sensors.

- Emphasis on lightweight materials and miniaturization for improved performance and fuel efficiency.

- Growing adoption of predictive maintenance and health monitoring for actuators.

- Integration of advanced control algorithms and software for enhanced precision.

- Development of quieter and more environmentally friendly hydraulic and electro-mechanical systems.

- Surge in demand for actuators in unmanned aerial vehicles (UAVs) and advanced air mobility (AAM).

AI Impact Analysis on Aerospace and Defense Actuator

The integration of Artificial Intelligence (AI) is a prominent topic for stakeholders in the aerospace and defense actuator market, with common questions centering on its potential to revolutionize design, operation, and maintenance. Users are keen to understand how AI can enhance predictive capabilities for actuator health, optimize system performance in real-time, and streamline manufacturing processes. The underlying expectation is that AI will significantly improve reliability, reduce operational costs, and accelerate innovation cycles within the sector.

Concerns often revolve around data security, the complexity of integrating AI into safety-critical systems, and the need for robust validation and certification processes. However, the overarching theme is optimism regarding AI's ability to create more autonomous, adaptive, and resilient actuator systems. AI's influence is anticipated to extend from initial design optimization and simulation to advanced fault detection and intelligent control, paving the way for a new generation of sophisticated aerospace and defense platforms.

- Enabling predictive maintenance through AI-driven anomaly detection and prognostics.

- Optimizing actuator design and material selection using AI-powered simulation tools.

- Enhancing real-time control and adaptive performance of actuator systems.

- Automating quality inspection and assembly processes in actuator manufacturing.

- Improving supply chain efficiency and inventory management for actuator components.

- Facilitating the development of autonomous flight control systems through AI algorithms.

- Increasing cybersecurity resilience for networked and smart actuator systems.

Key Takeaways Aerospace and Defense Actuator Market Size & Forecast

Key takeaways from the aerospace and defense actuator market size and forecast consistently highlight the robust growth trajectory driven by both commercial and military aviation expansion. Users are particularly interested in understanding the primary catalysts behind this growth, such as increasing aircraft deliveries, modernization programs, and the rising adoption of advanced technological solutions. The forecast indicates a sustained upward trend, underpinned by innovation in electric and smart actuation systems.

Furthermore, the market's resilience against economic fluctuations, largely due to long-term defense commitments and a backlog of commercial aircraft orders, is a significant point of interest. The insights suggest that strategic investments in research and development, particularly in areas like electrification and intelligent control, will be crucial for competitive advantage. The market is poised for significant expansion, offering substantial opportunities for both established players and new entrants specializing in next-generation actuation technologies.

- Significant growth projected, driven by increasing aircraft production and fleet modernization.

- Electro-mechanical and electro-hydraulic actuators gaining prominence over traditional hydraulic systems.

- Defense sector spending on advanced platforms contributes substantially to market expansion.

- Technological advancements in lightweight, durable, and smart actuators are crucial for market differentiation.

- North America and Asia Pacific are expected to remain key growth regions due to strong aerospace industries.

- Emphasis on reducing lifecycle costs and improving operational efficiency through advanced actuator solutions.

Aerospace and Defense Actuator Market Drivers Analysis

The aerospace and defense actuator market is propelled by several potent drivers that reflect the dynamic nature of both the commercial aviation and military sectors. A primary driver is the accelerating demand for new aircraft, both commercial and military, necessitating a continuous supply of advanced actuation systems. This includes large orders from airlines for fuel-efficient narrow-body and wide-body jets, as well as ongoing military procurement and upgrade programs globally.

Technological advancements also play a critical role, particularly the shift towards more electric aircraft (MEA) architectures. This transition is driving the development of sophisticated electro-mechanical and electro-hydraulic actuators that offer improved efficiency, reduced weight, and simplified maintenance compared to traditional hydraulic systems. Additionally, geopolitical tensions and the need for enhanced defense capabilities are fueling increased military spending, leading to higher demand for reliable and high-performance actuators in a variety of defense platforms.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for New Aircraft | +2.5% | Global, particularly North America, Asia Pacific | Short to Long-term |

| Technological Advancements (e.g., MEA) | +2.0% | Global, particularly developed economies | Medium to Long-term |

| Rising Defense Budgets and Modernization | +1.8% | North America, Europe, Asia Pacific | Short to Medium-term |

| Growth in Unmanned Aerial Vehicles (UAVs) | +1.5% | Global | Medium to Long-term |

Aerospace and Defense Actuator Market Restraints Analysis

Despite the robust growth prospects, the aerospace and defense actuator market faces several significant restraints that could temper its expansion. High development and certification costs are a major barrier, as new actuator technologies must undergo rigorous testing and meet stringent regulatory standards before deployment. This extended and expensive validation process can delay market entry and limit investment in smaller, innovative firms.

Furthermore, the long product lifecycles of aerospace and defense platforms mean that actuator designs often remain unchanged for decades, limiting the pace of new technology adoption. Supply chain disruptions, exacerbated by global events and geopolitical tensions, also pose a considerable challenge, impacting the availability of critical raw materials and components. These factors collectively contribute to a complex operating environment for actuator manufacturers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Development & Certification Costs | -1.2% | Global | Long-term |

| Long Product Lifecycles of Aircraft | -0.9% | Global | Long-term |

| Stringent Regulatory Frameworks | -0.8% | Global | Medium to Long-term |

| Supply Chain Vulnerabilities | -0.7% | Global | Short to Medium-term |

Aerospace and Defense Actuator Market Opportunities Analysis

Numerous opportunities are emerging in the aerospace and defense actuator market, poised to fuel future growth and innovation. The burgeoning sector of Urban Air Mobility (UAM) and Electrical Vertical Take-Off and Landing (eVTOL) aircraft presents a significant new demand avenue for compact, efficient, and highly reliable actuators. These emerging platforms require novel actuation solutions tailored to their unique design and operational parameters, opening doors for specialized manufacturers.

Additionally, the increasing adoption of additive manufacturing, or 3D printing, offers transformative potential for actuator component production. This technology allows for the creation of complex geometries, reduced part count, and lighter components, which can significantly enhance actuator performance and efficiency. Furthermore, the push towards digitalization and the integration of the Internet of Things (IoT) in aerospace systems create opportunities for smart, connected actuators that offer real-time data and predictive capabilities, optimizing maintenance and operational insights.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of UAM and eVTOL Aircraft | +1.5% | North America, Europe, Asia Pacific | Medium to Long-term |

| Advancements in Additive Manufacturing | +1.0% | Global | Medium to Long-term |

| Digitalization and IoT Integration | +0.9% | Global | Medium-term |

| Retrofitting and Upgrading Existing Fleets | +0.8% | Global | Short to Medium-term |

Aerospace and Defense Actuator Market Challenges Impact Analysis

The aerospace and defense actuator market contends with several notable challenges that require strategic responses from manufacturers and stakeholders. One pressing concern is the growing threat of cybersecurity attacks, as modern actuators become increasingly integrated into networked aircraft systems. Ensuring the integrity and security of these critical components against sophisticated digital threats is paramount for operational safety and national security.

Another significant challenge is the ongoing shortage of skilled labor, particularly engineers and technicians specialized in advanced aerospace manufacturing and maintenance. This talent gap can impede production capacity and the development of next-generation actuator technologies. Additionally, volatility in the prices of raw materials, such as specialized alloys and rare earth elements, can impact production costs and supply chain stability, posing a continuous challenge for cost-efficient manufacturing and long-term planning within the industry.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Cybersecurity Threats to Integrated Systems | -1.0% | Global | Ongoing |

| Skilled Labor Shortage | -0.8% | North America, Europe | Long-term |

| Raw Material Price Volatility | -0.7% | Global | Short to Medium-term |

| Integration Complexity of Advanced Systems | -0.6% | Global | Medium-term |

Aerospace and Defense Actuator Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the global aerospace and defense actuator market, providing a detailed analysis of its size, trends, drivers, restraints, opportunities, and challenges. It offers a forward-looking perspective, forecasting market growth from 2025 to 2033, and incorporates insights on technological advancements such as AI integration and the shift towards more electric aircraft. The scope also includes an exhaustive segmentation analysis and regional highlights, offering a holistic view of the market landscape for strategic decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.2 Billion |

| Market Forecast in 2033 | USD 29.8 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | SAFRAN S. A., Parker Hannifin Corporation, Moog Inc., Collins Aerospace (Raytheon Technologies), Honeywell International Inc., Liebherr-International AG, Curtiss-Wright Corporation, Woodward Inc., TransDigm Group Incorporated, Triumph Group, Inc., Meggitt PLC (Parker Meggitt), Eaton Corporation plc, GKN Aerospace (Melrose Industries PLC), Actuonix Motion Devices Inc., BAE Systems PLC, Nabtesco Corporation, Kaman Corporation, Triumph Group Inc., Servact SAS, Sagem (Safran Group) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The aerospace and defense actuator market is meticulously segmented to provide a granular understanding of its diverse components and drivers. These segments encompass various types of actuators, their specific applications across different aircraft and defense platforms, and the end-use sectors they serve. This detailed breakdown allows for a precise analysis of market dynamics, identifying key growth areas and technological preferences within each category.

Understanding these segments is critical for stakeholders to pinpoint niche opportunities, tailor product development, and formulate targeted market strategies. The shift from traditional hydraulic systems to advanced electro-mechanical and electro-hydraulic actuators across multiple applications signifies an important technological evolution. Furthermore, the segmentation by platform highlights the varied requirements and adoption rates of actuators across commercial aircraft, military jets, rotary-wing vehicles, and emerging UAVs, each with unique performance and reliability demands.

- By Type: Hydraulic, Pneumatic, Electro-Mechanical (EMA), Electro-Hydraulic (EHA), and Other Actuators, reflecting the technological evolution and preferred solutions for different applications.

- By Application: Flight Control Actuation, Landing Gear Actuation, Thrust Reverser Actuation, Utility Actuation, Brake Actuation, Missile Fin Control, and Other Applications, indicating the critical functions performed by actuators.

- By Platform: Fixed-Wing Aircraft (Commercial, Military, UAVs), Rotary-Wing Aircraft (Commercial, Military), Missiles, Spacecraft, Naval Vessels, and Ground Vehicles, showcasing the diverse range of platforms reliant on these systems.

- By End-Use: Commercial Aviation, Military Aviation, Space, Naval Defense, and Ground Defense, defining the primary industries and operational environments for actuator deployment.

Regional Highlights

North America currently dominates the aerospace and defense actuator market, primarily driven by the significant presence of major aircraft manufacturers, robust defense spending, and continuous technological innovation in the United States. The region benefits from substantial investment in research and development, particularly in advanced materials and more electric aircraft initiatives. The strong demand for both commercial and military aircraft, coupled with ongoing fleet modernization programs, ensures a sustained market leadership for North America.

Europe represents another key region, characterized by established aerospace and defense industries in countries such as France, the UK, Germany, and Italy. European nations are actively involved in joint defense programs and commercial aircraft manufacturing, fostering consistent demand for sophisticated actuator systems. The region is also at the forefront of developing sustainable aviation technologies, which in turn drives innovation in lightweight and energy-efficient actuators.

The Asia Pacific region is projected to exhibit the highest growth rate during the forecast period, largely attributed to the rapid expansion of its commercial aviation sector, increasing defense budgets, and growing domestic manufacturing capabilities in countries like China and India. The surging demand for new aircraft deliveries to meet rising passenger traffic, coupled with significant investments in military modernization, positions APAC as a high-potential market. Latin America, the Middle East, and Africa (LAMEA) are emerging markets, with growing demand from developing commercial fleets and increasing defense procurements, although on a smaller scale compared to other major regions. Investment in infrastructure and strategic partnerships will be crucial for these regions to further their market presence.

- North America: Leading market share due to strong military expenditure, large commercial aircraft fleets, and presence of key industry players. Focus on advanced EMA and EHA systems.

- Europe: Significant market presence driven by established aerospace manufacturers, collaborative defense projects, and emphasis on environmental sustainability in aviation.

- Asia Pacific (APAC): Fastest-growing market, fueled by expanding commercial aviation, rising defense budgets, and increasing domestic aircraft production in countries like China and India.

- Latin America: Growing demand from fleet expansion and modernization in commercial aviation, alongside moderate defense spending.

- Middle East and Africa (MEA): Emerging market driven by strategic defense investments, commercial airline expansion, and the development of new aviation hubs.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Aerospace and Defense Actuator Market.- SAFRAN S. A.

- Parker Hannifin Corporation

- Moog Inc.

- Collins Aerospace (Raytheon Technologies)

- Honeywell International Inc.

- Liebherr-International AG

- Curtiss-Wright Corporation

- Woodward Inc.

- TransDigm Group Incorporated

- Triumph Group, Inc.

- Meggitt PLC (Parker Meggitt)

- Eaton Corporation plc

- GKN Aerospace (Melrose Industries PLC)

- Actuonix Motion Devices Inc.

- BAE Systems PLC

- Nabtesco Corporation

- Kaman Corporation

- Servact SAS

- Sagem (Safran Group)

Frequently Asked Questions

What is an aerospace and defense actuator?

An aerospace and defense actuator is a mechanical or electromechanical device designed to control a mechanism or system by converting energy (e.g., electrical, hydraulic, pneumatic) into mechanical motion. These devices are critical for controlling various functions in aircraft, missiles, spacecraft, and ground defense vehicles, including flight surfaces, landing gear, engine components, and weapon systems.

What are the primary types of actuators used in the aerospace and defense sector?

The primary types include hydraulic, pneumatic, electro-mechanical (EMA), and electro-hydraulic (EHA) actuators. Hydraulic systems are robust for high force applications, while EMAs and EHAs are increasingly favored for their higher efficiency, reduced weight, and simplified maintenance in modern more electric aircraft (MEA) architectures.

How is AI impacting the development and performance of aerospace and defense actuators?

AI is significantly impacting actuators by enabling advanced predictive maintenance, optimizing design and manufacturing processes, enhancing real-time control for improved performance, and contributing to the development of more autonomous systems. AI algorithms analyze data from integrated sensors to forecast potential failures and ensure operational reliability.

What are the key factors driving the growth of the aerospace and defense actuator market?

Key drivers include the global increase in commercial aircraft deliveries and backlogs, ongoing military modernization programs, the transition towards more electric aircraft systems, and technological advancements in lightweight materials and smart actuation solutions. Geopolitical considerations also contribute to increased defense spending and demand for robust systems.

Which regions are leading in the aerospace and defense actuator market, and why?

North America currently leads due to substantial defense budgets, the presence of major aerospace manufacturers, and continuous innovation. Asia Pacific is the fastest-growing region, driven by rapid commercial aviation expansion and increasing military investments, particularly in China and India. Europe also holds a significant share due to its established aerospace industry and collaborative defense initiatives.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted