3D Computer Graphics Software Market

3D Computer Graphics Software Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678269 | Last Updated : July 21, 2025 |

Format : ![]()

![]()

![]()

![]()

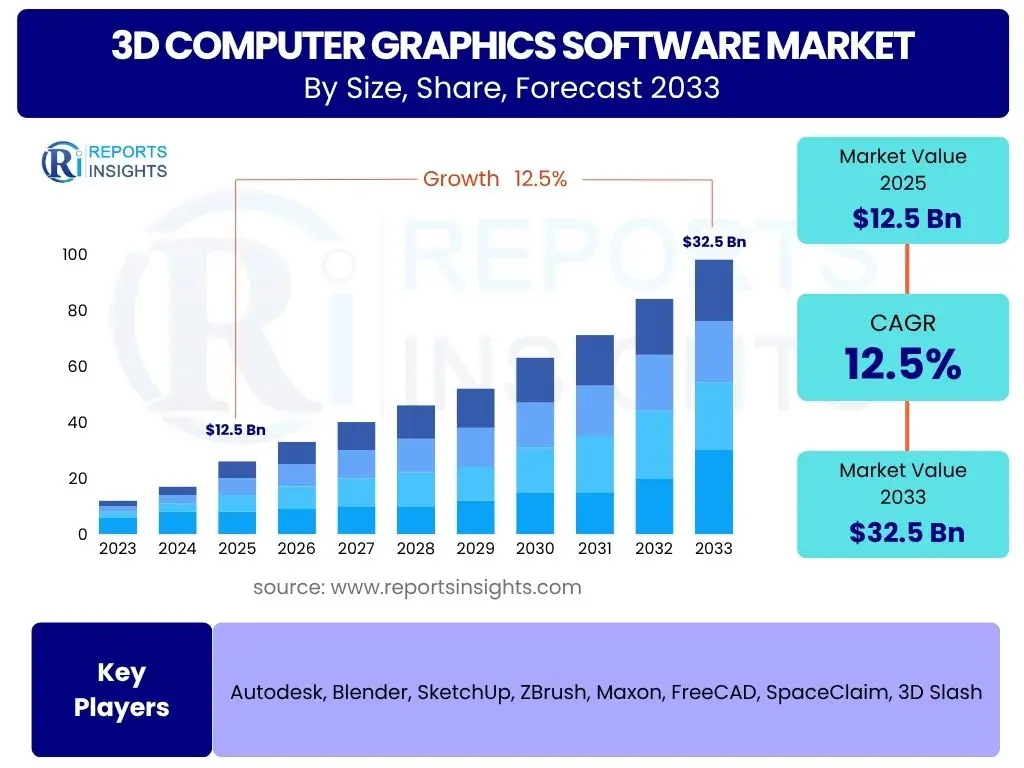

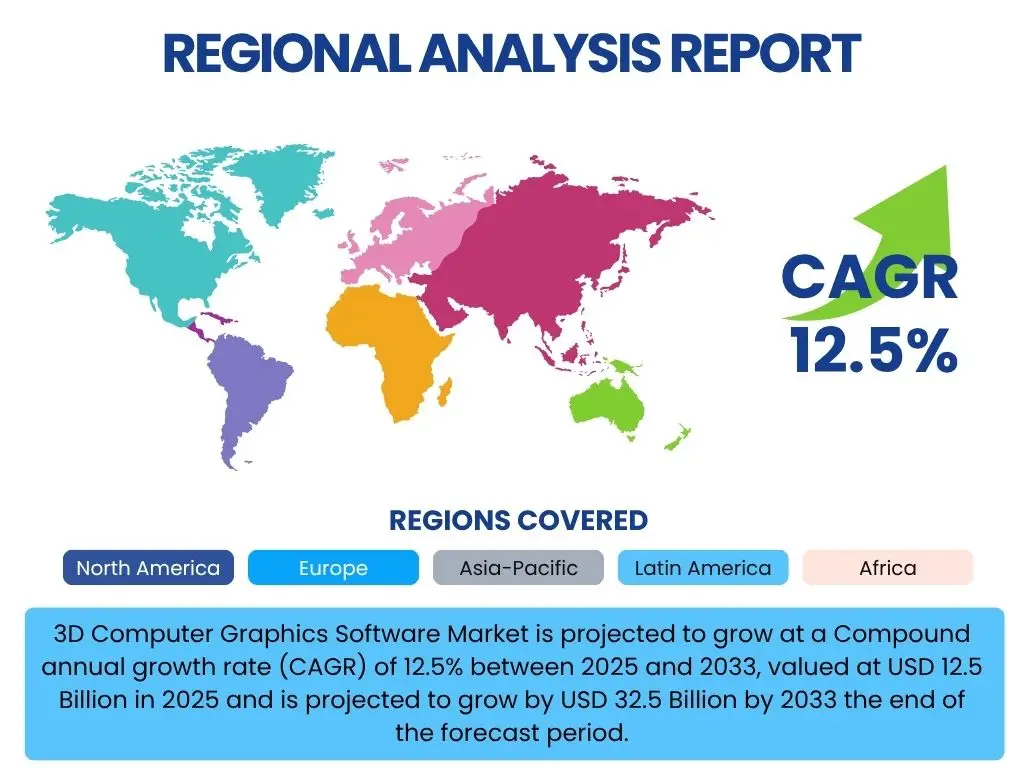

3D Computer Graphics Software Market is projected to grow at a Compound annual growth rate (CAGR) of 12.5% between 2025 and 2033, valued at USD 12.5 Billion in 2025 and is projected to grow by USD 32.5 Billion by 2033 the end of the forecast period.

Key 3D Computer Graphics Software Market Trends & Insights

The 3D Computer Graphics Software Market is undergoing significant transformation driven by rapid technological advancements and evolving industry demands. A prominent trend is the increasing adoption of real-time rendering capabilities, essential for applications in gaming, virtual reality, and augmented reality, enabling more immersive and interactive experiences. This shift is accompanied by a growing emphasis on cloud-based solutions, providing greater accessibility, collaboration features, and scalability for artists, designers, and engineers globally. The integration of artificial intelligence and machine learning is also profoundly impacting the market, automating complex tasks, enhancing design optimization, and enabling more intelligent content creation workflows.

- Real-time rendering adoption for interactive experiences.

- Cloud-based software solutions for enhanced accessibility and collaboration.

- AI and machine learning integration for automated design and optimization.

- Rise of metaverse applications driving demand for realistic 3D content.

- Increasing use in digital twins and industrial simulation.

- Demand for user-friendly interfaces and intuitive workflows.

- Growth in independent game development and creative industries.

- Focus on sustainable design and visualization tools.

AI Impact Analysis on 3D Computer Graphics Software

Artificial Intelligence (AI) is revolutionizing the 3D computer graphics software market by introducing unprecedented levels of automation, intelligence, and efficiency into the content creation pipeline. AI algorithms are increasingly used for tasks such as generative design, where systems can autonomously create complex 3D models based on specified parameters, significantly accelerating the ideation and prototyping phases. Furthermore, AI-powered tools are enhancing texture generation, material creation, and animation, making these processes faster and more realistic. This integration allows artists to focus on creative vision rather than repetitive manual tasks, ultimately democratizing access to sophisticated 3D content creation and fostering innovation across various industries.

- AI-driven generative design for rapid 3D model creation.

- Automated texturing and material generation through machine learning.

- AI-enhanced animation and rigging for realistic character movements.

- Intelligent asset management and content organization.

- Improved rendering efficiency and noise reduction with AI algorithms.

- Personalized user experiences and predictive tool suggestions.

- Development of AI-powered digital human creation tools.

- Streamlined workflows for non-expert users.

Key Takeaways 3D Computer Graphics Software Market Size & Forecast

- The market is projected for substantial growth, driven by digital transformation.

- Anticipated CAGR of 12.5% from 2025 to 2033 signifies robust expansion.

- Valued at USD 12.5 Billion in 2025, indicating a significant current market presence.

- Forecasted to reach USD 32.5 Billion by 2033, highlighting strong future potential.

- The growth trajectory is supported by increasing adoption across diverse industries.

- Technological advancements are key enablers of market expansion.

- Strategic investments in research and development are propelling innovation.

- The market demonstrates resilience and adaptability to evolving demands.

3D Computer Graphics Software Market Drivers Impact Analysis

The proliferation of immersive technologies stands as a primary driver for the 3D computer graphics software market. The explosive growth of virtual reality (VR), augmented reality (AR), and mixed reality (MR) applications across various sectors, including gaming, entertainment, education, and enterprise training, necessitates sophisticated 3D content creation tools. These technologies demand highly realistic, interactive, and optimized 3D models and environments, directly fueling the demand for advanced graphics software capable of real-time rendering and complex scene management.

Furthermore, the escalating demand for high-quality visual content in digital media and advertising significantly propels market expansion. Businesses are increasingly leveraging 3D graphics for product visualization, marketing campaigns, and brand storytelling to capture consumer attention and enhance engagement. This trend extends beyond traditional media into emerging platforms like social media and e-commerce, where interactive 3D product displays are becoming a competitive differentiator, thereby increasing the reliance on robust 3D software solutions for compelling visual output.

The expanding scope of application in professional sectors, such as architecture, engineering, and construction (AEC), manufacturing, and healthcare, also acts as a critical growth catalyst. In AEC, 3D software is indispensable for building information modeling (BIM), architectural visualization, and urban planning. For manufacturing, it is crucial for product design, prototyping, and simulation. In healthcare, it aids in medical imaging, surgical planning, and educational simulations. The versatility and efficiency gains offered by 3D software in these industries underscore its indispensable role and contribute substantially to market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption of Immersive Technologies (VR, AR, MR) | +3.0% | North America, Asia Pacific, Europe | Short to Medium Term |

| Growing Demand for High-Quality Digital Media & Content Creation | +2.5% | Global, particularly developed economies | Short to Medium Term |

| Expansion in Architecture, Engineering, Construction (AEC) & Manufacturing | +2.0% | Europe, Asia Pacific, North America | Medium Term |

| Advancements in AI and Machine Learning Integration | +2.0% | Global, especially tech hubs | Medium to Long Term |

| Rise of Independent Content Creators and Gaming Industry | +1.5% | Global | Short to Medium Term |

3D Computer Graphics Software Market Restraints Impact Analysis

The high cost associated with acquiring and maintaining professional-grade 3D computer graphics software poses a significant restraint on market growth, particularly for individual artists, small studios, and educational institutions with limited budgets. Many advanced software suites come with substantial upfront license fees or recurring subscription costs, alongside the need for powerful hardware specifications to run them efficiently. This financial barrier can deter potential users and lead them towards open-source or lower-cost alternatives, thereby limiting the adoption of premium solutions in certain segments.

Furthermore, the steep learning curve and complexity involved in mastering sophisticated 3D graphics software act as a considerable impediment. These applications often feature intricate interfaces, a multitude of tools, and require a deep understanding of 3D modeling, texturing, rigging, animation, and rendering principles. The time and effort required to become proficient can be daunting for newcomers, necessitating significant training investments which can further increase the overall cost of entry and restrict the pool of skilled professionals, thereby slowing down broader market penetration.

Moreover, concerns related to intellectual property rights and data security, especially with cloud-based 3D software solutions, can restrain market expansion. Users, particularly corporate entities dealing with sensitive design information, may be hesitant to store their proprietary 3D models and project data on external servers due to fears of unauthorized access, data breaches, or misuse. This can lead to a preference for on-premise solutions or a cautious approach to cloud adoption, impacting the scalability and widespread acceptance of modern 3D software delivery models.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Software Licenses and Hardware Requirements | -2.0% | Emerging Markets, Small & Medium Enterprises (SMEs) | Short to Medium Term |

| Steep Learning Curve and Complexity for New Users | -1.5% | Global, individual creators | Short Term |

| Intellectual Property and Data Security Concerns with Cloud Solutions | -1.0% | Globally, particularly large enterprises | Medium Term |

| Interoperability Issues Between Different Software Platforms | -0.8% | Global, collaborative environments | Medium Term |

| Limited Skilled Workforce in Specific Regions | -0.7% | Developing Regions | Long Term |

3D Computer Graphics Software Market Opportunities Impact Analysis

The burgeoning adoption of digital twin technology across various industries presents a significant growth opportunity for the 3D computer graphics software market. Digital twins, virtual replicas of physical assets, processes, or systems, rely heavily on accurate 3D models for their creation, visualization, and simulation. As industries like manufacturing, smart cities, and healthcare increasingly implement digital twins for predictive maintenance, operational optimization, and scenario planning, the demand for sophisticated 3D modeling and rendering software capable of generating and managing these complex virtual environments is poised for substantial growth.

The expansion of the metaverse and Web3 ecosystems also offers a transformative opportunity. The concept of a persistent, interconnected virtual world requires an unprecedented volume of diverse and high-fidelity 3D content, ranging from avatars and virtual assets to entire digital environments. 3D computer graphics software will be foundational to creating, populating, and iterating within these new digital frontiers, driving demand for tools that support interoperability, user-generated content, and real-time collaborative creation within decentralized frameworks. This emerging digital economy represents a vast potential market for content creation tools.

Furthermore, the continuous advancements in cloud computing and subscription-based software models create opportunities for broader market reach and revenue generation. Cloud-based 3D software lowers the barrier to entry by reducing the need for powerful local hardware and enabling more flexible access through subscriptions. This model facilitates collaboration among distributed teams and provides seamless updates, attracting a wider user base, including freelancers, small businesses, and educational institutions, thereby expanding the overall market size and improving accessibility.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Adoption of Digital Twin Technology | +2.5% | North America, Europe, Asia Pacific (Industrial Sectors) | Medium to Long Term |

| Emergence and Expansion of Metaverse and Web3 Ecosystems | +2.0% | Global, tech-forward economies | Long Term |

| Proliferation of Cloud-Based & SaaS 3D Solutions | +1.8% | Global | Short to Medium Term |

| Increasing Demand for 3D Printing & Additive Manufacturing | +1.5% | Europe, North America, Asia Pacific (Manufacturing) | Medium Term |

| Development of AI-Powered Generative Art and Design Tools | +1.2% | Global | Medium to Long Term |

3D Computer Graphics Software Market Challenges Impact Analysis

One of the significant challenges facing the 3D computer graphics software market is the rapid pace of technological evolution, which necessitates constant updates and feature integration. Software developers must continuously innovate to keep pace with advancements in rendering techniques, hardware capabilities, and emerging industry standards, such as those driven by real-time ray tracing or neural graphics. This demands substantial research and development investments and rapid adaptation, placing pressure on development cycles and potentially leading to compatibility issues with older systems or workflows for end-users, thus impacting widespread adoption.

The problem of interoperability and workflow integration across diverse software ecosystems also presents a considerable hurdle. Many projects involve multiple specialized 3D software tools for different stages of content creation, such as modeling, sculpting, texturing, animation, and rendering. Ensuring seamless data exchange and consistent file formats between these varied applications remains a complex challenge. This lack of universal interoperability can lead to inefficient workflows, data loss, and increased production times, creating friction for professional studios and collaborative teams.

Moreover, the growing concern over digital piracy and unauthorized software usage continues to challenge the revenue streams and intellectual property of software vendors. Despite robust digital rights management (DRM) measures, illegal distribution and use of 3D graphics software persist, particularly in regions with less stringent intellectual property enforcement. This not only results in financial losses for legitimate developers but also undermines investment in innovation and fair market competition, thereby impeding the overall growth potential of the market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Evolution and Need for Constant Updates | -1.8% | Global | Ongoing |

| Interoperability Issues and Workflow Integration Complexity | -1.5% | Global, especially large studios | Medium Term |

| Digital Piracy and Unauthorized Software Usage | -1.2% | Developing Regions, Global (SMEs) | Ongoing |

| Data Security and Privacy Concerns in Cloud Environments | -0.9% | Global, regulated industries | Medium Term |

| Competition from Open-Source Alternatives and In-house Tools | -0.7% | Global | Short Term |

3D Computer Graphics Software Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the 3D Computer Graphics Software market, encompassing historical data, current market dynamics, and future projections. It provides a detailed examination of market size, growth drivers, restraints, opportunities, and key trends shaping the industry. The report also includes a thorough segmentation analysis, regional insights, and profiles of leading market participants, equipping stakeholders with actionable intelligence for strategic decision-making and competitive advantage.

| Report Attributes | Report Details |

|---|---|

| Report Name | 3D Computer Graphics Software Market |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 32.5 Billion |

| Growth Rate | CAGR of 2025 to 2033 12.5% |

| Number of Pages | 200 |

| Key Companies Covered | Autodesk, Blender, SketchUp, ZBrush, Maxon, FreeCAD, SpaceClaim, 3D Slash |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

The 3D Computer Graphics Software Market is segmented to provide a granular understanding of its diverse components and application areas. This segmentation helps in identifying key market niches, understanding user preferences, and analyzing growth opportunities across different categories. The market is broadly categorized by product type, reflecting the various operating systems and platforms supported by the software, and by application, delineating the primary use cases and end-user environments for these powerful tools.

Product type segmentation provides insights into which operating systems are most prevalent for 3D graphics software usage. This indicates platform compatibility and user base preferences, which can influence software development and market penetration strategies. Application segmentation, on the other hand, highlights the varied scenarios in which 3D software is deployed, from individual creative pursuits to extensive commercial projects, showcasing the versatility and breadth of the market's reach.

Market Product Type Segmentation:-- Mac OS

- Windows

- Other

- Personal

- Office

- Commercial

Regional Highlights

North America currently holds a significant market share in the 3D Computer Graphics Software market, primarily driven by the presence of major software developers, a thriving entertainment industry (film, gaming, animation), and extensive adoption in AEC and manufacturing sectors. The region benefits from substantial investments in R&D, early adoption of advanced technologies like VR/AR, and a robust digital infrastructure. The United States and Canada are key contributors to this dominance, exhibiting high demand for sophisticated 3D modeling and rendering tools across various professional applications.

Europe also represents a strong market, characterized by its mature design and engineering industries, particularly in Germany, France, and the UK. The region's emphasis on industrial design, automotive manufacturing, and architectural innovation fuels the demand for high-precision 3D software. Furthermore, a growing independent game development scene and burgeoning digital media production contribute to the sustained growth of the market across European countries, with increasing integration of 3D graphics in educational and research institutions.

Asia Pacific is emerging as the fastest-growing region in the 3D Computer Graphics Software market, propelled by rapid urbanization, industrial expansion, and a booming digital entertainment sector, especially in countries like China, Japan, and South Korea. The increasing number of animation studios, game developers, and architectural firms, coupled with government initiatives promoting digital transformation and smart cities, are significantly driving the adoption of 3D graphics software. The large population base and rising disposable incomes also contribute to the expansion of personal and commercial applications.

Latin America and the Middle East & Africa (MEA) are also experiencing steady growth, albeit from a smaller base. In Latin America, the growth is fueled by expanding creative industries, educational initiatives, and increasing foreign investments in infrastructure projects. The MEA region's market expansion is driven by developing smart city initiatives, growth in media and entertainment, and the burgeoning oil & gas and construction sectors requiring advanced visualization tools. Investment in digital infrastructure and technological awareness is progressively boosting the demand for 3D computer graphics software in these evolving markets.

- North America: Leading market share due to strong entertainment industry, robust AEC and manufacturing sectors, and high R&D investments. Key countries include the United States and Canada.

- Europe: Significant market presence driven by mature design and engineering industries, particularly in Germany, France, and the UK, alongside a growing independent game development scene.

- Asia Pacific (APAC): Fastest-growing region, fueled by rapid urbanization, industrial expansion, and a booming digital entertainment sector in countries like China, Japan, and South Korea.

- Latin America: Steady growth propelled by expanding creative industries, educational initiatives, and increasing foreign investments in infrastructure.

- Middle East & Africa (MEA): Emerging market driven by smart city initiatives, growth in media and entertainment, and development in construction and industrial sectors.

Top Key Players:

The market research report covers the analysis of key stake holders of the 3D Computer Graphics Software Market. Some of the leading players profiled in the report include -

- Autodesk

- Blender

- SketchUp

- ZBrush

- Maxon

- FreeCAD

- SpaceClaim

- 3D Slash

Frequently Asked Questions:

What is 3D computer graphics software?

3D computer graphics software is a category of computer programs used to create, manipulate, and render three-dimensional models and animations. These tools enable users to design virtual objects, scenes, and characters, which can then be used in various applications such as gaming, film, architecture, engineering, product design, and medical visualization. The software facilitates processes like modeling, texturing, rigging, animation, and rendering to produce realistic or stylized 3D visuals.

How is AI impacting the 3D computer graphics software market?

AI is significantly impacting the 3D computer graphics software market by automating complex tasks and enhancing creative workflows. It is used for generative design, where AI creates 3D models based on parameters, and for improving aspects like texturing, material creation, and animation. AI-powered tools also contribute to more efficient rendering, intelligent asset management, and the development of highly realistic digital humans, making 3D content creation faster and more accessible.

What are the primary applications of 3D computer graphics software?

3D computer graphics software has a wide range of applications across various industries. Key applications include entertainment (gaming, film, animation, visual effects), architecture, engineering, and construction (AEC) for building information modeling (BIM) and visualization, manufacturing for product design and prototyping, healthcare for medical imaging and surgical planning, education for interactive learning, and marketing/advertising for product visualization and brand engagement.

Which regions are leading the adoption of 3D computer graphics software?

North America currently leads the adoption of 3D computer graphics software, driven by its robust entertainment industry and strong presence in AEC and manufacturing sectors. Europe also holds a significant market share due to its mature design and engineering industries. The Asia Pacific region, particularly China, Japan, and South Korea, is experiencing the fastest growth, fueled by rapid industrial expansion and a booming digital entertainment sector.

What are the key market trends shaping the 3D computer graphics software industry?

Key market trends include the increasing adoption of real-time rendering for immersive experiences in gaming and XR, the shift towards cloud-based software solutions for enhanced accessibility and collaboration, and the deeper integration of AI and machine learning for automated design and content creation. Additionally, the rise of metaverse applications, the growing use in digital twins, and a focus on user-friendly interfaces are significant trends influencing the industry's direction.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted