Zero Turn Mower Market

Zero Turn Mower Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705093 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

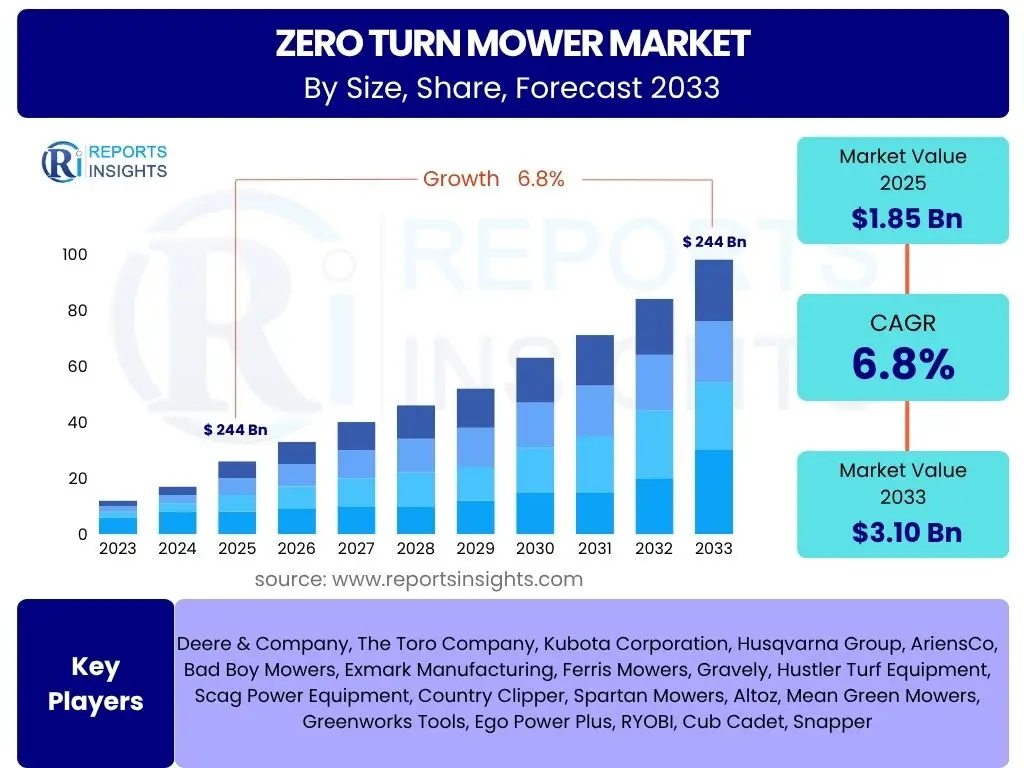

Zero Turn Mower Market Size

According to Reports Insights Consulting Pvt Ltd, The Zero Turn Mower Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 3.10 Billion by the end of the forecast period in 2033.

Key Zero Turn Mower Market Trends & Insights

User inquiries frequently highlight the rapid evolution of the zero turn mower market, particularly concerning advancements in power sources, automation, and design. There is a strong interest in understanding how sustainability initiatives, such as the adoption of electric models, are shaping the market, alongside the growing demand for features that enhance operational efficiency and user comfort. Consumers and businesses alike are seeking insights into the long-term viability and cost-effectiveness of newer technologies, indicating a shift towards performance-driven and environmentally conscious purchasing decisions.

The market is experiencing a significant pivot towards battery-powered and electric zero turn mowers, driven by increasing environmental regulations and a consumer preference for quieter, emission-free operation. This trend is not merely about compliance but also about enhanced user experience, reducing noise pollution in residential areas, and lowering operational costs through reduced fuel consumption and maintenance. Furthermore, advancements in battery technology, including longer run times and faster charging capabilities, are making electric models increasingly competitive with traditional gasoline-powered counterparts, addressing previous limitations that hindered widespread adoption.

Beyond electrification, the integration of smart technologies and automation features represents another dominant trend. Features such as GPS-guided mowing, remote diagnostics, and telematics are becoming more prevalent, offering users greater control, efficiency, and predictive maintenance capabilities. The demand for robust, ergonomic designs that offer superior comfort and ease of use for extended periods is also a key driver. This focus on user-centric design reflects a broader market trend where the overall operator experience, including reduced vibration and improved seating, significantly influences purchasing decisions for both professional landscapers and homeowners.

- Electrification and Battery-Powered Models: Growing adoption of electric zero turn mowers due to environmental benefits, reduced noise, and lower operating costs.

- Smart Technology Integration: Implementation of GPS, IoT, and telematics for enhanced efficiency, autonomous features, and remote monitoring.

- Ergonomics and User Comfort: Focus on improved seating, reduced vibration, and intuitive controls to enhance operator experience.

- Hybrid Models Development: Introduction of hybrid electric-gasoline models offering a balance of power and efficiency.

- Advanced Cutting Deck Technology: Innovations in deck design for improved cut quality, mulching capabilities, and debris management.

AI Impact Analysis on Zero Turn Mower

Common user questions regarding AI's influence on zero turn mowers center on the potential for autonomous operation, enhanced efficiency, and improved safety features. There is significant interest in how AI can optimize mowing patterns, predict maintenance needs, and integrate with broader smart landscaping systems. Users are keen to understand the practical applications of AI in real-world scenarios, particularly concerning cost implications, reliability, and the learning curve associated with adopting such advanced technologies. The underlying theme is a desire for less human intervention and more precise, consistent landscaping results.

The integration of artificial intelligence into zero turn mowers is poised to revolutionize the landscaping industry by enabling a new generation of smart, highly efficient, and increasingly autonomous machines. AI algorithms can process sensor data in real-time to optimize mowing paths, minimizing overlaps and missed areas, thereby significantly reducing fuel consumption and operational time. This level of precision not only enhances the quality of the cut but also contributes to greater productivity for commercial operations and more pristine results for residential users. Furthermore, AI-driven predictive maintenance capabilities can analyze operational data to identify potential equipment failures before they occur, reducing downtime and extending the lifespan of the machinery.

Beyond operational efficiency, AI plays a crucial role in enhancing the safety and user-friendliness of zero turn mowers. AI-powered obstacle detection systems can identify people, pets, or objects in the mowing path, initiating automatic shutdowns or evasive maneuvers to prevent accidents. This is particularly valuable in dynamic environments where human error can lead to significant hazards. As the technology matures, AI could facilitate fully autonomous mowing solutions for large commercial properties or even complex residential landscapes, allowing operators to focus on more intricate tasks or manage multiple machines simultaneously. The development of AI-driven user interfaces could also simplify complex operations, making advanced features accessible to a broader range of users, thereby lowering the barrier to entry for high-performance equipment.

- Autonomous Operation: AI enables self-driving capabilities for pre-programmed routes and obstacle avoidance, reducing manual labor.

- Predictive Maintenance: AI algorithms analyze machine data to forecast potential component failures, optimizing maintenance schedules and reducing downtime.

- Optimized Mowing Patterns: AI can determine the most efficient mowing paths based on terrain and obstacles, saving time and fuel.

- Enhanced Safety Features: AI-powered sensors and cameras detect objects and people, preventing collisions and improving operator safety.

- Smart Fleet Management: AI facilitates monitoring and managing multiple mowers simultaneously, optimizing resource allocation for commercial landscaping businesses.

Key Takeaways Zero Turn Mower Market Size & Forecast

User inquiries concerning market takeaways frequently focus on the primary growth drivers, the segment exhibiting the most significant expansion, and the overarching implications of technological advancements on future market dynamics. There is a keen interest in understanding the balance between residential and commercial demand, the impact of sustainability trends on purchasing decisions, and the long-term forecast regarding profitability and market saturation. Consumers and industry stakeholders are seeking clear, concise summaries that highlight critical factors influencing market trajectory and investment opportunities.

The Zero Turn Mower market is poised for sustained growth, primarily propelled by increasing landscaping and lawn care activities across both residential and commercial sectors. The ergonomic benefits, speed, and maneuverability offered by zero turn mowers continue to attract a diverse customer base, solidifying their position as a preferred choice over traditional riding mowers. The market's upward trajectory is further supported by innovations in battery technology and automation, which are making these machines more appealing to environmentally conscious consumers and businesses seeking operational efficiencies. This growth is not uniform across all segments, with specific power source types and applications experiencing accelerated adoption due to evolving consumer preferences and regulatory landscapes.

A significant takeaway from the market forecast is the pronounced shift towards electric and battery-powered zero turn mowers. While gasoline models currently dominate, the exponential growth predicted for electric variants underscores a fundamental transformation in the industry. This shift is driven by stringent emission regulations, rising fuel costs, and a growing societal emphasis on sustainable practices. The commercial segment is expected to remain a dominant force, with landscaping professionals continually investing in advanced, efficient machinery to enhance productivity and service quality. Concurrently, the increasing disposable income and growing demand for well-maintained private properties contribute substantially to residential market expansion, indicating a robust and diversified demand for zero turn mowers.

- Consistent Market Expansion: The market is projected for robust growth, driven by increasing demand in both residential and commercial landscaping.

- Shift to Electric: Electric zero turn mowers are anticipated to be the fastest-growing segment, fueled by environmental concerns and technological advancements.

- Commercial Sector Dominance: Professional landscaping companies will remain key consumers, valuing efficiency, speed, and durability.

- Technological Innovation as a Catalyst: Continued R&D in AI, automation, and battery life will further accelerate market adoption and enhance product capabilities.

- High Initial Investment: Despite long-term cost savings, the higher upfront cost of zero turn mowers, especially electric models, remains a key consideration for buyers.

Zero Turn Mower Market Drivers Analysis

The global Zero Turn Mower market is primarily driven by the escalating demand for efficient and time-saving lawn care solutions from both commercial and residential sectors. As urban and suburban areas expand, the need for professional landscaping services grows, prompting commercial operators to invest in high-performance equipment that can cover large areas quickly and effectively. Concurrently, homeowners with larger properties are increasingly opting for zero turn mowers due to their superior maneuverability around obstacles and significantly reduced mowing times compared to traditional riding mowers.

Technological advancements also serve as a crucial driver, particularly the innovations in battery technology and the integration of smart features. The development of more powerful, longer-lasting, and rapidly charging electric batteries is addressing previous limitations of electric models, making them a viable and attractive alternative to gasoline-powered mowers. Furthermore, the inclusion of features like GPS navigation, IoT connectivity, and improved ergonomic designs enhances user experience and operational efficiency, thereby increasing consumer willingness to invest in these advanced machines. These innovations cater to a market that values convenience, performance, and environmental responsibility.

Changing consumer preferences towards sustainable and quieter equipment further propels market growth. Growing environmental awareness and stricter noise regulations in many regions are accelerating the adoption of electric zero turn mowers, which produce zero emissions and significantly less noise compared to their internal combustion engine counterparts. This trend is particularly evident in densely populated residential areas and commercial zones where noise reduction is a priority, influencing purchasing decisions and fostering a transition towards greener landscaping solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand for Efficient Lawn Care | +1.5% | North America, Europe, Asia Pacific | Short to Medium Term |

| Technological Advancements (Battery & Smart Features) | +1.2% | Global | Medium to Long Term |

| Growing Adoption of Electric Mowers | +1.0% | North America, Western Europe, Australia | Medium Term |

| Expansion of Landscaping Services | +0.8% | North America, Asia Pacific, Latin America | Short to Medium Term |

| Urbanization and Property Development | +0.7% | Asia Pacific, Latin America, Middle East | Long Term |

Zero Turn Mower Market Restraints Analysis

Despite the robust growth trajectory, the Zero Turn Mower market faces several notable restraints, primarily concerning the high initial investment cost. Zero turn mowers, especially models equipped with advanced features or electric powertrains, represent a significant capital outlay compared to traditional riding mowers. This higher upfront cost can deter price-sensitive residential consumers and smaller landscaping businesses, particularly in emerging economies where budget constraints are more pronounced, thus limiting market penetration.

Another significant restraint is the requirement for specialized maintenance and the availability of skilled technicians. The sophisticated engineering behind zero turn mowers, particularly those integrating complex electronic systems and battery management units, necessitates expert knowledge for servicing and repairs. A shortage of adequately trained service personnel, especially in remote or less developed regions, can lead to increased downtime and higher maintenance costs for owners, negatively impacting overall product satisfaction and market adoption.

Furthermore, the fluctuating prices of raw materials, such as steel and electronic components, contribute to manufacturing cost volatility, which can be passed on to consumers, further impacting affordability. Regulatory challenges, particularly those related to battery disposal and charging infrastructure for electric models, also present hurdles. While these regulations aim for environmental protection, they can impose additional costs on manufacturers and consumers, potentially slowing down the transition to more sustainable mowers if not adequately supported by infrastructure development.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Purchase Cost | -0.9% | Global, particularly Emerging Markets | Short to Medium Term |

| Complexity of Maintenance and Repairs | -0.7% | Global | Medium Term |

| Limited Awareness in Some Regions | -0.5% | Asia Pacific, Latin America, Africa | Short Term |

| Availability of Alternative Lawn Care Solutions | -0.4% | Global | Short to Medium Term |

| Raw Material Price Volatility | -0.3% | Global | Short Term |

Zero Turn Mower Market Opportunities Analysis

Significant opportunities exist within the Zero Turn Mower market, largely stemming from the burgeoning demand for electric and autonomous models. The increasing emphasis on environmental sustainability and noise reduction, coupled with advancements in battery technology, creates a fertile ground for manufacturers to innovate and expand their electric product lines. As battery range and charging times improve, electric zero turn mowers will become even more attractive to both commercial landscapers, seeking to meet eco-friendly standards, and residential users, desiring quieter operation. This trend opens pathways for market penetration into new segments and geographies.

The expansion into developing economies also presents a substantial growth opportunity. Rapid urbanization and the rise of middle-class incomes in regions such as Asia Pacific and Latin America are fueling the demand for professional landscaping services and improved residential property aesthetics. As these markets mature, there will be an increasing adoption of advanced lawn care equipment, including zero turn mowers, presenting a new customer base for market players. Tailoring products to meet the specific needs and price points of these emerging markets, perhaps through localized manufacturing or distribution partnerships, can unlock considerable untapped potential.

Furthermore, the integration of Internet of Things (IoT) and AI technologies into zero turn mowers creates avenues for value-added services and product differentiation. Opportunities include developing mowers with predictive maintenance capabilities, remote diagnostics, and fleet management solutions for commercial users, thereby enhancing efficiency and reducing operational costs. The emergence of smart cities and green infrastructure initiatives also opens up possibilities for zero turn mowers equipped for municipal landscaping contracts, particularly those with autonomous capabilities, offering a compelling proposition for large-scale, efficient land management.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Electric and Autonomous Mowers | +1.8% | Global, particularly Developed Markets | Medium to Long Term |

| Expansion into Emerging Markets | +1.3% | Asia Pacific, Latin America, Middle East & Africa | Long Term |

| Integration of IoT and AI for Smart Features | +1.1% | Global | Medium Term |

| Development of Rental and Leasing Services | +0.9% | North America, Europe | Short to Medium Term |

| Focus on Customization for Niche Applications | +0.6% | Global | Short to Medium Term |

Zero Turn Mower Market Challenges Impact Analysis

The Zero Turn Mower market faces several critical challenges that could impact its growth trajectory. One significant hurdle is the intense competition from alternative lawn care equipment and the proliferation of various mower types, including robotic lawn mowers, which are gaining traction, especially in the residential segment. This broad array of choices necessitates continuous innovation and differentiation for zero turn mower manufacturers to maintain their market share and attract new customers amidst evolving consumer preferences and technological shifts.

Supply chain disruptions and volatility in raw material prices present another persistent challenge. The global supply chain has been prone to instabilities, affecting the availability of critical components such as semiconductors, batteries, and steel, which are essential for zero turn mower manufacturing. These disruptions can lead to production delays, increased manufacturing costs, and ultimately higher retail prices, making the products less competitive. Managing these external factors requires robust supply chain strategies and diversified sourcing, adding complexity to operations.

Furthermore, the need for extensive dealer networks and after-sales support poses a significant operational challenge. Zero turn mowers are complex machines that require specialized maintenance, parts, and technical assistance. Building and maintaining a widespread network of trained dealers and service centers, particularly in geographically diverse markets, demands substantial investment and coordination. Ensuring consistent quality of service across this network is crucial for customer satisfaction and brand loyalty, but it remains an ongoing logistical and training challenge for manufacturers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Competition from Alternative Mowers | -0.8% | Global | Medium to Long Term |

| Supply Chain Disruptions & Material Costs | -0.6% | Global | Short to Medium Term |

| Need for Extensive After-Sales Support Network | -0.5% | Global | Long Term |

| Skilled Labor Shortage for Maintenance | -0.4% | North America, Europe | Medium Term |

| Regulatory Hurdles and Compliance Costs | -0.3% | Europe, North America | Short to Medium Term |

Zero Turn Mower Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Zero Turn Mower market, covering market size, trends, drivers, restraints, opportunities, and challenges across various segments and regions. It offers a detailed forecast from 2025 to 2033, meticulously examining the industry's historical performance, current dynamics, and future potential. The report delves into the impact of technological advancements, particularly AI and electrification, on the market landscape, providing actionable insights for stakeholders seeking to navigate the evolving industry. It aims to equip readers with a holistic understanding of market forces and strategic considerations for competitive positioning.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 3.10 Billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Deere & Company, The Toro Company, Kubota Corporation, Husqvarna Group, AriensCo, Bad Boy Mowers, Exmark Manufacturing, Ferris Mowers, Gravely, Hustler Turf Equipment, Scag Power Equipment, Country Clipper, Spartan Mowers, Altoz, Mean Green Mowers, Greenworks Tools, Ego Power Plus, RYOBI, Cub Cadet, Snapper |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Zero Turn Mower market is meticulously segmented to provide a granular understanding of its diverse components, enabling stakeholders to identify specific growth opportunities and tailor strategies. These segmentations are primarily based on the mower's power source, cutting width, and intended application, reflecting distinct user needs and operational requirements. Understanding these segments is crucial for manufacturers to innovate and for distributors to target specific customer demographics effectively.

Segmentation by type, encompassing Gas Zero Turn Mowers and Electric Zero Turn Mowers, highlights the industry's transition towards sustainable solutions. While gasoline models currently hold a larger market share due to their established presence and raw power, the electric segment is projected for substantial growth, driven by environmental concerns, reduced operating costs, and advancements in battery technology. This distinction is critical for forecasting future market share shifts and investment priorities.

Further segmentation by cutting width (Less than 48 inches, 48-60 inches, More than 60 inches) directly correlates with the scale of the area to be mowed and the efficiency required. Smaller widths are typically preferred for residential properties with intricate landscapes, while larger widths are favored by commercial operators for expansive areas, offering higher productivity. Application-based segmentation into Residential and Commercial categories delineates consumer behavior and purchasing drivers, with residential users prioritizing ease of use and quiet operation, and commercial users focusing on durability, performance, and fleet management capabilities. Each segment offers unique challenges and opportunities for product development and market penetration.

- By Type:

- Gas Zero Turn Mowers

- Electric Zero Turn Mowers

- By Cutting Width:

- Less than 48 inches

- 48-60 inches

- More than 60 inches

- By Application:

- Residential

- Commercial

- By End-User:

- Landscaping Professionals

- Homeowners

- Government & Institutions

- Golf Courses

- By Distribution Channel:

- Dealers & Distributors

- Online Retail

- Retail Stores

Regional Highlights

The Zero Turn Mower market exhibits distinct regional dynamics, influenced by varying economic conditions, consumer preferences, landscaping practices, and environmental regulations. North America currently dominates the market, largely due to a well-established landscaping industry, a high prevalence of large properties, and strong consumer awareness and acceptance of advanced lawn care equipment. The early adoption of zero turn technology and a robust commercial landscaping sector contribute significantly to the region's leading position, with a growing interest in electric models further bolstering market growth.

Europe represents another significant market, characterized by stricter environmental regulations and a growing emphasis on sustainable and quieter outdoor power equipment. This region is witnessing a steady shift towards electric zero turn mowers, driven by urban noise ordinances and a strong consumer preference for eco-friendly solutions. While residential properties might be smaller on average, the demand from municipalities, parks, and professional landscaping services for efficient and environmentally compliant equipment sustains market expansion. Germany, France, and the UK are key contributors to the European market's trajectory.

Asia Pacific is projected to be the fastest-growing region, fueled by rapid urbanization, increasing disposable incomes, and the emergence of modern landscaping trends in countries like China, India, and Australia. As commercial infrastructure and residential developments expand, the demand for efficient lawn care solutions rises. While the adoption of zero turn mowers is currently lower compared to Western markets, the increasing awareness and the benefits offered by these machines are creating substantial growth opportunities. Latin America and the Middle East & Africa regions are also expected to show gradual growth, driven by infrastructure development and evolving agricultural and landscaping practices.

- North America: Dominant market share due to extensive landscaping industry, large property sizes, high consumer adoption, and robust commercial demand.

- Europe: Significant growth driven by stringent environmental regulations, increasing adoption of electric mowers, and demand from professional and municipal sectors.

- Asia Pacific (APAC): Fastest-growing region, propelled by rapid urbanization, rising disposable incomes, and increasing professional landscaping services, especially in China, India, and Australia.

- Latin America: Emerging market with growing adoption influenced by economic development, increasing property maintenance needs, and evolving landscaping practices.

- Middle East & Africa (MEA): Gradual growth anticipated, primarily driven by infrastructure development, expanding commercial and residential properties, and selective adoption of modern landscaping equipment.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Zero Turn Mower Market.- Deere & Company

- The Toro Company

- Kubota Corporation

- Husqvarna Group

- AriensCo

- Bad Boy Mowers

- Exmark Manufacturing

- Ferris Mowers

- Gravely

- Hustler Turf Equipment

- Scag Power Equipment

- Country Clipper

- Spartan Mowers

- Altoz

- Mean Green Mowers

- Greenworks Tools

- Ego Power Plus

- RYOBI

- Cub Cadet

- Snapper

Frequently Asked Questions

Analyze common user questions about the Zero Turn Mower market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a zero turn mower and what are its primary benefits?

A zero turn mower is a type of lawn mower designed with a turning radius of effectively zero, allowing it to pivot on its own axis. Its primary benefits include superior maneuverability around obstacles, significantly reduced mowing time compared to traditional mowers, and a high-quality cut, making it ideal for properties with complex landscaping or large areas.

How do electric zero turn mowers compare to gasoline models?

Electric zero turn mowers offer zero emissions, significantly quieter operation, and lower long-term operating costs due to reduced fuel and maintenance needs. While their initial purchase price can be higher and battery run times are a consideration, gasoline models typically offer longer continuous operation and higher power for very demanding tasks. Both are evolving rapidly.

What are the main factors driving the growth of the zero turn mower market?

Key growth drivers include the increasing demand for efficient and time-saving lawn care solutions, technological advancements such as improved battery life and smart features, the expansion of professional landscaping services, and a growing consumer preference for environmentally friendly and quieter equipment.

What challenges does the zero turn mower market face?

The market faces challenges such as the high initial purchase cost, which can deter some buyers, the complexity of maintenance requiring specialized technicians, intense competition from alternative lawn care equipment, and potential supply chain disruptions affecting component availability and pricing.

What are the key opportunities in the zero turn mower market for manufacturers?

Significant opportunities lie in the continued development and adoption of electric and autonomous zero turn mowers, expansion into emerging markets with growing landscaping needs, integration of IoT and AI technologies for enhanced smart features, and the development of flexible business models such as rental and leasing services.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted