Wood Pulp Market

Wood Pulp Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_704335 | Last Updated : August 05, 2025 |

Format : ![]()

![]()

![]()

![]()

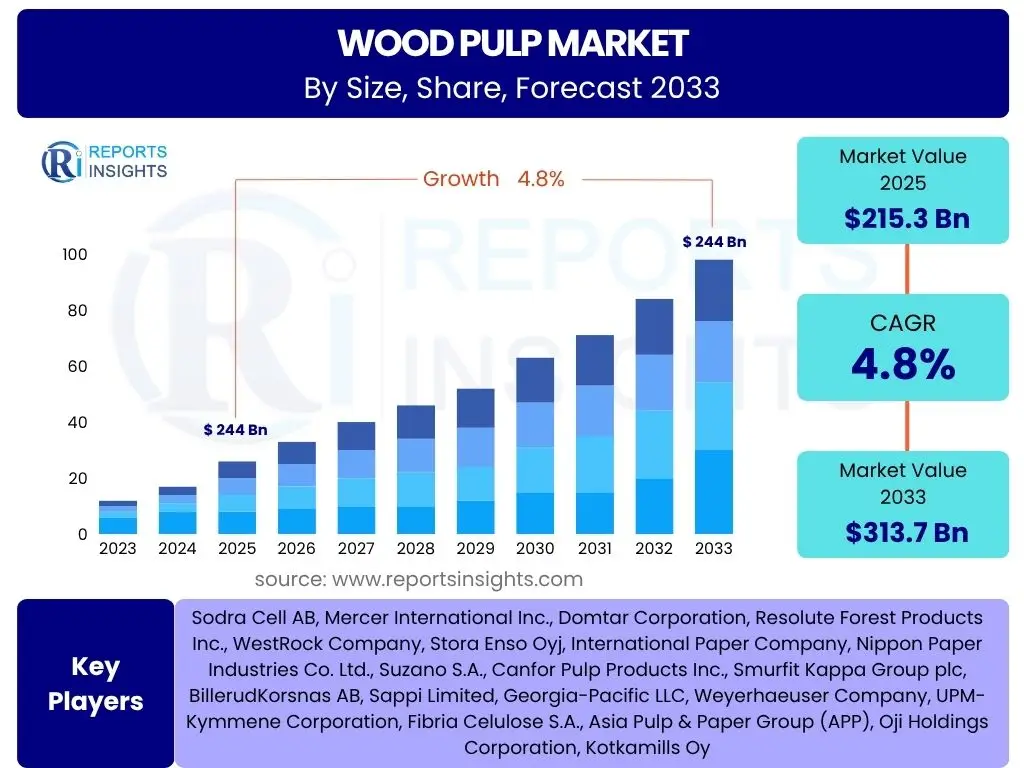

Wood Pulp Market Size

According to Reports Insights Consulting Pvt Ltd, The Wood Pulp Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033. The market is estimated at USD 215.3 billion in 2025 and is projected to reach USD 313.7 billion by the end of the forecast period in 2033.

Key Wood Pulp Market Trends & Insights

Common user inquiries regarding the Wood Pulp market trends frequently center on sustainability, the integration of advanced manufacturing technologies, and the evolving demand landscape. Users are keen to understand how environmental regulations are shaping production processes, the impact of digitalization on supply chains, and the shift in consumer preferences towards eco-friendly packaging solutions. There is also significant interest in the adoption of circular economy principles within the industry and the development of novel applications for wood pulp beyond traditional paper products.

The market is witnessing a notable emphasis on eco-friendly production methods, including the adoption of closed-loop systems and reduced water consumption, driven by stricter environmental mandates and corporate sustainability goals. Additionally, the increasing demand for sustainable packaging materials, particularly within the e-commerce sector, is a crucial trend influencing pulp production. Innovation in pulp types, such as dissolving pulp for textiles and specialty pulps for absorbents, is also expanding the market's horizons and diversifying its revenue streams.

- Growing demand for sustainable packaging solutions, especially from the e-commerce sector.

- Increasing adoption of advanced pulping technologies for improved efficiency and reduced environmental footprint.

- Expansion of wood pulp applications into new areas like bio-composites and biodegradable plastics.

- Emphasis on circular economy principles, promoting pulp recycling and resource efficiency.

- Shifting consumer preference towards eco-friendly and responsibly sourced products.

- Digitization and automation enhancing supply chain transparency and operational efficiency.

AI Impact Analysis on Wood Pulp

Common user questions concerning the impact of Artificial Intelligence (AI) on the Wood Pulp industry primarily revolve around its potential to optimize manufacturing processes, enhance supply chain management, and improve quality control. Users are interested in how AI can lead to more efficient resource utilization, predict maintenance needs for machinery, and streamline complex logistical operations. There is also an expectation that AI will contribute to better data analysis for market forecasting and sustainable forest management, addressing both operational efficiency and environmental stewardship concerns.

AI's influence is increasingly evident in optimizing operational parameters within pulp mills, from digester control to bleaching processes, leading to significant reductions in energy and chemical consumption. Predictive analytics, powered by AI, allows for proactive maintenance of machinery, minimizing downtime and increasing productivity across the production line. Furthermore, AI-driven solutions are being deployed to enhance supply chain visibility, enabling better inventory management and more efficient transportation of raw materials and finished products, thereby contributing to overall cost reduction and increased responsiveness to market demands.

- Optimization of pulp production processes, leading to reduced energy and chemical consumption.

- Predictive maintenance of machinery, minimizing downtime and extending equipment lifespan.

- Enhanced supply chain management through demand forecasting and logistics optimization.

- Improved quality control and consistency of pulp products using AI-driven vision systems.

- Data-driven insights for sustainable forest management and resource allocation.

- Automation of routine tasks, freeing up human resources for more complex problem-solving.

Key Takeaways Wood Pulp Market Size & Forecast

Analysis of common user questions regarding the Wood Pulp market size and forecast highlights key aspects such as sustained growth, the influence of evolving end-use industries, and the critical role of sustainability. Users frequently inquire about the primary growth drivers, the segments expected to exhibit the most significant expansion, and the long-term viability of the market amidst environmental pressures. Understanding regional market dynamics and the impact of technological advancements on future market trajectory are also common themes, indicating a holistic interest in the market's comprehensive outlook.

The market is poised for steady expansion, driven by the increasing global population and the persistent demand for hygiene products, packaging, and specialty papers. While traditional graphic paper demand faces shifts, the surge in e-commerce necessitates more packaging materials, predominantly fiber-based, providing a significant impetus for pulp growth. Furthermore, the commitment to sustainable practices and the innovation in bio-based products offer new avenues for market penetration and value creation, ensuring the long-term relevance and growth of the wood pulp industry beyond conventional applications.

- The Wood Pulp market is projected for substantial growth, driven by diverse applications and global demand.

- Sustainable practices and eco-friendly product development are critical factors influencing market direction.

- Evolving consumer preferences and the growth of e-commerce are reshaping demand for fiber-based packaging.

- Technological advancements in pulping and biorefineries are unlocking new market opportunities.

- Asia Pacific is expected to be a key growth region due to industrial expansion and population growth.

- The market is resilient, adapting to shifts in traditional paper consumption by diversifying into new segments.

Wood Pulp Market Drivers Analysis

The Wood Pulp market is propelled by a confluence of factors, primarily the robust demand from the packaging industry, significant growth in e-commerce, and the increasing global focus on hygiene and health. The rising disposable incomes in emerging economies are leading to higher consumption of tissue and sanitary products, directly impacting pulp demand. Furthermore, the push for sustainable and biodegradable packaging alternatives, driven by environmental consciousness and regulatory pressures, positions wood pulp as a preferred material over plastics.

Technological advancements in pulping processes, which enhance efficiency and reduce environmental impact, also serve as a crucial driver. These innovations enable the production of diverse pulp grades, catering to specific industry needs and opening up new application areas. The global population growth further contributes to the demand for paper-based products, ensuring a steady requirement for wood pulp across various sectors, from construction materials to specialized industrial applications.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Packaging and E-commerce Demand | +1.5% | Global, especially Asia Pacific, North America, Europe | 2025-2033 |

| Increased Demand for Tissue & Hygiene Products | +1.2% | Global, particularly Emerging Economies | 2025-2033 |

| Shift Towards Sustainable & Bio-based Materials | +1.0% | Europe, North America, Asia Pacific | 2027-2033 |

| Technological Advancements in Pulping Processes | +0.7% | Global | 2025-2033 |

Wood Pulp Market Restraints Analysis

Despite robust growth drivers, the Wood Pulp market faces several significant restraints that could temper its expansion. Environmental regulations, particularly those concerning deforestation, water usage, and carbon emissions, impose strict operational limitations and increase compliance costs for pulp manufacturers. Public perception and activist pressure regarding sustainable forest management also challenge the industry, demanding greater transparency and accountability in sourcing practices.

The volatility of raw material prices, primarily wood logs, presents a significant economic challenge, impacting profit margins and investment decisions. Additionally, the increasing shift towards digital media and communication in certain sectors continues to reduce the demand for traditional graphic papers, necessitating a strategic pivot for pulp producers. High capital investment required for establishing and upgrading pulp mills also acts as a barrier to entry and expansion, limiting the growth potential for smaller players.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations | -0.8% | Europe, North America, China | 2025-2033 |

| Volatility of Raw Material Prices | -0.6% | Global | 2025-2033 |

| Declining Demand for Graphic Paper | -0.5% | North America, Europe | 2025-2030 |

| High Capital Investment and Operating Costs | -0.4% | Global | 2025-2033 |

Wood Pulp Market Opportunities Analysis

The Wood Pulp market is presented with significant opportunities arising from the global pivot towards sustainability and the innovation in material science. The increasing demand for biodegradable and compostable materials in packaging and consumer goods offers a fertile ground for pulp-based alternatives to plastics. Furthermore, advancements in biotechnology are enabling the development of novel applications for cellulose, such as nanocellulose and microfibrillated cellulose, which can be utilized in advanced composites, electronics, and medical devices.

Emerging economies, particularly in Asia Pacific and Latin America, represent substantial growth potential due to rapid industrialization, urbanization, and rising disposable incomes driving increased consumption of paper and hygiene products. Investment in sustainable forest management and responsible sourcing practices can also open new markets and enhance brand reputation. The circular economy model, emphasizing recycling and resource efficiency, provides avenues for the industry to innovate and create higher-value products from recycled fibers, further reducing environmental impact while boosting profitability.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Bio-based Products & Nanocellulose | +1.3% | Global, particularly R&D Hubs in Europe, North America | 2027-2033 |

| Growth in Emerging Markets | +1.1% | Asia Pacific, Latin America, Africa | 2025-2033 |

| Increasing Investment in Sustainable Forestry | +0.9% | Global, especially key forestry regions | 2025-2033 |

| Circular Economy Initiatives & Recycling Technologies | +0.8% | Europe, North America, Japan | 2026-2033 |

Wood Pulp Market Challenges Impact Analysis

The Wood Pulp market faces a range of challenges that require strategic responses from industry players. Intense global competition, coupled with oversupply in certain pulp grades, can lead to price erosion and reduced profit margins. Supply chain disruptions, often caused by geopolitical events, natural disasters, or pandemics, pose significant risks to raw material availability and timely delivery of finished products, impacting operational stability and costs.

The rising energy costs and the need for significant investments in energy-efficient technologies present a substantial hurdle for manufacturers, especially given the energy-intensive nature of pulp production. Moreover, skilled labor shortages in forestry and mill operations can impede production capacity and efficiency. Adherence to increasingly complex and varying international trade regulations and tariffs further complicates global operations and market access for wood pulp producers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global Supply Chain Disruptions | -0.7% | Global | 2025-2028 |

| Rising Energy Costs and Sustainability Pressure | -0.6% | Europe, North America, Asia Pacific | 2025-2033 |

| Intense Competition and Price Volatility | -0.5% | Global | 2025-2033 |

| Labor Shortages and Skill Gaps | -0.4% | North America, Europe | 2025-2033 |

Wood Pulp Market - Updated Report Scope

This market research report provides an in-depth analysis of the global Wood Pulp market, covering historical data, current market conditions, and future projections. It includes comprehensive insights into market size, growth drivers, restraints, opportunities, and challenges. The scope encompasses detailed segmentation by pulp type, application, end-use industry, and geography, offering a holistic view of market dynamics. The report also profiles key market players, analyzes competitive landscapes, and addresses the impact of emerging technologies and sustainability trends on the industry's trajectory. It serves as an essential resource for stakeholders seeking strategic guidance and a deeper understanding of the Wood Pulp sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 215.3 Billion |

| Market Forecast in 2033 | USD 313.7 Billion |

| Growth Rate | 4.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Sodra Cell AB, Mercer International Inc., Domtar Corporation, Resolute Forest Products Inc., WestRock Company, Stora Enso Oyj, International Paper Company, Nippon Paper Industries Co. Ltd., Suzano S.A., Canfor Pulp Products Inc., Smurfit Kappa Group plc, BillerudKorsnas AB, Sappi Limited, Georgia-Pacific LLC, Weyerhaeuser Company, UPM-Kymmene Corporation, Fibria Celulose S.A., Asia Pulp & Paper Group (APP), Oji Holdings Corporation, Kotkamills Oy |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Wood Pulp market is meticulously segmented to provide a granular understanding of its diverse components and their respective contributions to the overall market dynamics. This segmentation facilitates detailed analysis of specific product types, their applications across various industries, and the end-use sectors driving demand. Such a comprehensive breakdown allows for targeted strategic planning and investment decisions within the complex value chain of the wood pulp industry.

Understanding these segments is crucial for identifying emerging niches, assessing competitive intensity within sub-markets, and forecasting future growth trajectories. The market is not monolithic; rather, it is a mosaic of specialized pulps catering to distinct needs, from high-strength packaging to absorbent materials and innovative biomaterials. This detailed segmentation highlights the adaptability and evolving nature of wood pulp products in response to technological advancements and changing consumer and industrial demands.

- By Pulp Type: Chemical Pulp (Kraft Pulp, Sulfite Pulp), Mechanical Pulp (Groundwood Pulp, Refiner Mechanical Pulp, Thermomechanical Pulp, Chemi-Thermomechanical Pulp), Dissolving Pulp, Market Pulp, Other Specialty Pulps.

- By Application: Paper & Paperboard Production, Tissue & Towel Production, Packaging, Textiles (Viscose Fibers), Specialty & Absorbent Products, Building & Construction Materials, Biomaterials & Composites.

- By End-Use Industry: Printing & Writing Paper, Packaging Industry, Hygiene & Personal Care, Textile Industry, Building Materials, Food & Beverage, Others.

Regional Highlights

- North America: A mature market characterized by strong emphasis on sustainable forestry practices, advanced pulping technologies, and high demand for specialty and absorbent pulps. The region is a hub for innovation in wood-based biomaterials.

- Europe: Driven by stringent environmental regulations and a robust circular economy framework, Europe is a leader in sustainable pulp production and consumption. The region shows increasing demand for eco-friendly packaging and dissolving pulp for textile applications.

- Asia Pacific (APAC): The largest and fastest-growing market due to rapid industrialization, urbanization, increasing disposable incomes, and booming e-commerce. Significant demand for packaging, tissue, and printing & writing paper in countries like China and India.

- Latin America: Possesses abundant forest resources, making it a key producer and exporter of wood pulp. The region benefits from competitive production costs and growing domestic demand from the packaging and hygiene sectors.

- Middle East and Africa (MEA): An emerging market with growing demand for packaging and hygiene products, supported by infrastructure development and population growth. The region relies heavily on imports but is exploring opportunities for domestic production and sustainable sourcing.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Wood Pulp Market.- Sodra Cell AB

- Mercer International Inc.

- Domtar Corporation

- Resolute Forest Products Inc.

- WestRock Company

- Stora Enso Oyj

- International Paper Company

- Nippon Paper Industries Co. Ltd.

- Suzano S.A.

- Canfor Pulp Products Inc.

- Smurfit Kappa Group plc

- BillerudKorsnas AB

- Sappi Limited

- Georgia-Pacific LLC

- Weyerhaeuser Company

- UPM-Kymmene Corporation

- Fibria Celulose S.A.

- Asia Pulp & Paper Group (APP)

- Oji Holdings Corporation

- Kotkamills Oy

Frequently Asked Questions

Analyze common user questions about the Wood Pulp market and generate a concise list of summarized FAQs reflecting key topics and concerns.

What is wood pulp primarily used for?

Wood pulp is predominantly used in the production of various paper-based products, including printing and writing paper, packaging materials (like cardboard and corrugated boxes), tissue and hygiene products, and specialty papers. Increasingly, it is also utilized in textiles (as dissolving pulp for rayon/viscose), and in emerging applications such as bio-composites and sustainable building materials.

How is wood pulp manufactured?

Wood pulp is primarily manufactured through mechanical or chemical processes. Mechanical pulping involves grinding wood chips, while chemical pulping (e.g., Kraft process or Sulfite process) uses chemicals to separate cellulose fibers from lignin. These processes break down wood into a fibrous slurry, which is then washed, screened, and bleached to produce various grades of pulp.

What are the key types of wood pulp?

The key types of wood pulp include Chemical Pulp (such as Kraft pulp and Sulfite pulp, known for strength), Mechanical Pulp (like Groundwood pulp and Thermomechanical pulp, offering bulk and opacity), Dissolving Pulp (used for textiles and specialty chemicals), and Market Pulp (pulp sold on the open market, not integrated into a paper mill).

What are the environmental impacts associated with wood pulp production?

Environmental impacts include deforestation (if not from sustainable sources), water pollution from effluent discharge, air emissions from chemical processes, and high energy consumption. However, the industry is increasingly adopting sustainable forestry, closed-loop systems, and advanced treatment technologies to mitigate these impacts and promote circular economy principles.

What is the future outlook for the Wood Pulp market?

The future outlook for the Wood Pulp market is positive, driven by sustained demand from the packaging and hygiene sectors, particularly with the rise of e-commerce. Growth is also fueled by the shift towards sustainable and bio-based materials as alternatives to plastics, and by innovations in pulp applications such as nanocellulose and advanced biomaterials. Ongoing investments in sustainable forestry and cleaner production technologies will further support market expansion.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted