Wood Pellet Market

Wood Pellet Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702115 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

Wood Pellet Market Size

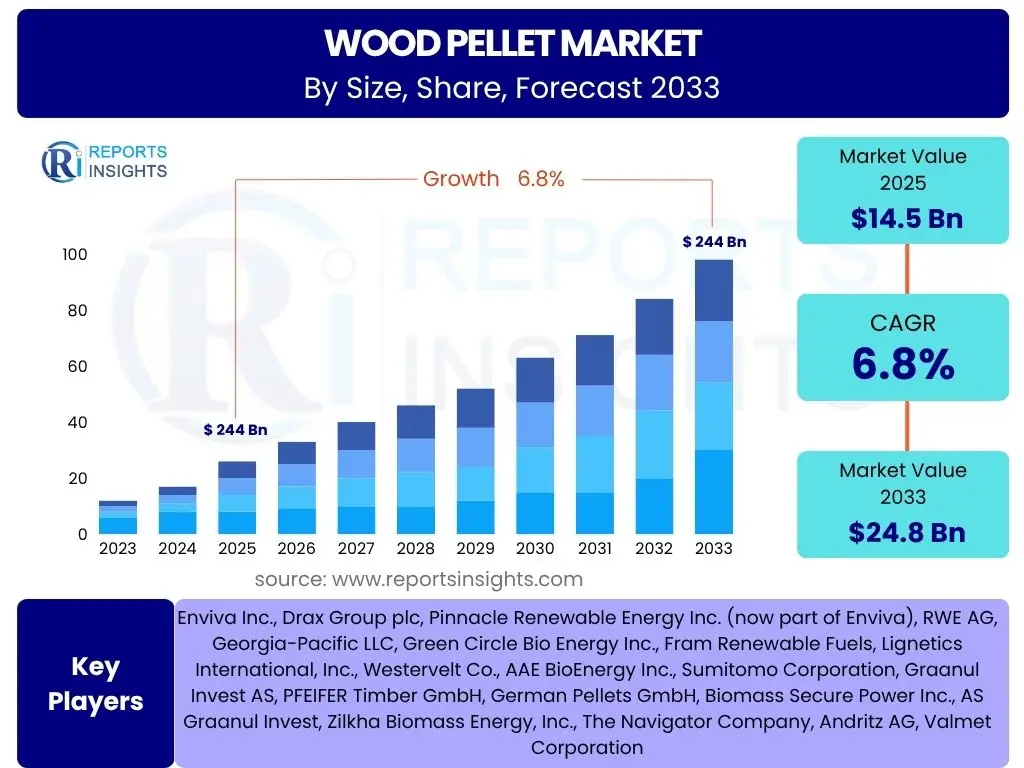

According to Reports Insights Consulting Pvt Ltd, The Wood Pellet Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 14.5 Billion in 2025 and is projected to reach USD 24.8 Billion by the end of the forecast period in 2033.

Key Wood Pellet Market Trends & Insights

The wood pellet market is experiencing dynamic shifts, driven primarily by an accelerated global transition towards sustainable energy sources and increasing regulatory support for biomass utilization. Common user questions frequently revolve around the sustainability of wood pellets, their primary applications beyond residential heating, and the technological advancements in their production and logistics. Industry insights indicate a strong focus on enhancing efficiency across the supply chain, from sourcing raw materials to delivery, alongside a burgeoning interest in certified sustainable products.

A significant trend is the expanding adoption of wood pellets in industrial co-firing, where they replace or supplement fossil fuels in large power plants and industrial facilities. This application is a major growth driver, particularly in Europe and parts of Asia, as countries strive to meet ambitious renewable energy targets. Furthermore, the residential and commercial heating sectors continue to provide a stable demand base, with consumers increasingly favoring wood pellets due to their cost-effectiveness relative to traditional fossil fuels and their reduced carbon footprint.

Beyond these established uses, the market is witnessing innovation in pellet applications, including their use in animal bedding, as absorbents, and in the production of biochemicals. The development of advanced pelletizing technologies is improving pellet quality, energy density, and moisture resistance, making them more attractive for diverse end-uses. Supply chain optimization, driven by digital technologies, is another key trend, aimed at reducing transportation costs and improving overall market responsiveness.

- Increased demand for industrial co-firing in power generation.

- Growing adoption in residential and commercial heating sectors due to cost-effectiveness and sustainability.

- Rising focus on certified sustainable wood pellets (e.g., ENplus, SBP) to meet environmental standards.

- Technological advancements in pellet production, enhancing efficiency and quality.

- Optimization of supply chain logistics to reduce costs and improve delivery times.

- Diversification of applications beyond energy, including animal bedding and absorbents.

AI Impact Analysis on Wood Pellet

User inquiries regarding the impact of Artificial Intelligence (AI) on the wood pellet industry often center on how AI can enhance operational efficiency, optimize resource utilization, and improve market forecasting. The consensus points to AI's potential to revolutionize various stages of the value chain, from raw material procurement and processing to logistics and sales. Implementing AI-driven solutions is seen as critical for maintaining competitiveness, improving sustainability metrics, and adapting to fluctuating market demands.

AI's influence is primarily observed in predictive maintenance for manufacturing equipment, significantly reducing downtime and operational costs by anticipating machinery failures. In raw material sourcing, AI algorithms can optimize forest management, predict timber yields, and identify the most efficient collection routes, thereby ensuring a consistent and sustainable supply. Furthermore, AI-powered systems are being developed for quality control, leveraging computer vision and machine learning to analyze pellet characteristics (density, moisture, ash content) in real-time, ensuring adherence to strict quality standards.

The strategic application of AI extends to optimizing supply chain management, enabling better demand forecasting, inventory management, and route planning, which can drastically reduce transportation costs and carbon emissions. AI can also facilitate dynamic pricing strategies based on real-time market data and weather patterns, empowering producers and distributors to make more informed decisions. While challenges exist in data integration and the initial investment required, the long-term benefits of AI in the wood pellet sector include enhanced profitability, improved sustainability, and greater operational resilience.

- Predictive maintenance for pelletizing equipment, reducing downtime.

- Optimized raw material sourcing and forest management through data analytics.

- Enhanced quality control systems using AI for real-time pellet characteristic analysis.

- Improved supply chain logistics, including route optimization and inventory management.

- Accurate demand forecasting and market trend prediction for strategic planning.

- Automated energy management and process optimization in production facilities.

Key Takeaways Wood Pellet Market Size & Forecast

Analysis of common user questions regarding the wood pellet market size and forecast consistently reveals an interest in understanding the primary drivers of growth, the resilience of the market to external shocks, and its long-term sustainability. Insights suggest that the market is on a robust growth trajectory, largely underpinned by global decarbonization efforts and supportive regulatory frameworks. Stakeholders are keen to identify the most promising regional markets and application segments that will fuel future expansion.

A significant takeaway is the pivotal role of industrial demand, particularly from power generation and large-scale industrial heating, in driving market expansion. This segment offers substantial growth potential due to ongoing conversions from fossil fuels to biomass. Concurrently, the steady demand from residential and commercial heating sectors, influenced by consumer preferences for cleaner and more affordable energy, provides a foundational base for market stability and incremental growth.

The forecast highlights continued investment in sustainable sourcing and advanced production technologies as crucial for market competitiveness. Regulatory policies, such as carbon pricing and renewable energy mandates, will remain key enablers for market development across various regions. Overall, the wood pellet market is poised for sustained growth, characterized by increasing industrial adoption, evolving sustainability standards, and technological innovation aimed at optimizing the value chain.

- Strong growth trajectory driven by global renewable energy policies and decarbonization targets.

- Industrial co-firing in power plants and large industries is a primary growth engine.

- Sustained demand from residential and commercial heating markets.

- Europe remains the leading consumer, while North America is a major producer and exporter.

- Growing importance of sustainable sourcing and certification schemes.

- Increasing integration of advanced technologies for production efficiency and supply chain optimization.

Wood Pellet Market Drivers Analysis

The wood pellet market is significantly driven by global efforts to transition to renewable energy sources, fueled by increasing environmental consciousness and supportive government policies. The rising cost of fossil fuels also makes wood pellets an attractive alternative, particularly for heating and industrial power generation. Technological advancements in pellet production have improved efficiency and reduced costs, further enhancing their competitiveness. The consistent demand from established markets like Europe, coupled with emerging markets in Asia, contributes to robust growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand for renewable energy sources | +2.1% | Global, particularly Europe & Asia Pacific | Long-term (2025-2033) |

| Supportive government policies and incentives for biomass energy | +1.8% | EU member states, UK, Japan, South Korea | Mid-to-Long term (2025-2030) |

| Rising fossil fuel prices and energy security concerns | +1.5% | Global, particularly import-dependent nations | Short-to-Mid term (2025-2028) |

| Increasing adoption in industrial co-firing applications | +1.2% | Europe, North America, Japan, South Korea | Long-term (2025-2033) |

| Technological advancements in pellet manufacturing and logistics | +0.8% | North America, Europe, Key Manufacturing Hubs | Mid-to-Long term (2025-2033) |

Wood Pellet Market Restraints Analysis

Despite significant growth drivers, the wood pellet market faces several restraints that could impede its expansion. Fluctuations in raw material supply, often influenced by seasonal availability and competition from other forest product industries, can lead to price volatility and supply chain instability. High transportation costs, especially for intercontinental shipments, remain a significant barrier, increasing the final cost of pellets for end-users. Additionally, competition from other established and emerging renewable energy sources, such as solar and wind, poses a challenge to market penetration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Fluctuations in raw material prices and availability | -1.3% | Global, particularly regions with limited forest resources | Short-to-Mid term (2025-2028) |

| High transportation and logistics costs | -1.0% | Cross-continental trade routes, Remote consumption areas | Long-term (2025-2033) |

| Competition from other renewable energy sources (solar, wind) | -0.8% | Developed economies with diversified energy portfolios | Long-term (2025-2033) |

| Concerns over sustainable forest management practices | -0.6% | Europe (importing regions), North America (sourcing regions) | Mid-to-Long term (2025-2030) |

| High initial investment costs for pellet production facilities | -0.5% | Developing countries, New market entrants | Short-to-Mid term (2025-2027) |

Wood Pellet Market Opportunities Analysis

Opportunities in the wood pellet market are emerging from several directions, including the expansion into new geographic markets and the development of innovative applications. Developing economies, particularly in Asia, represent significant untapped potential as they increasingly prioritize sustainable energy solutions. Continuous research and development are opening new avenues for wood pellets beyond traditional heating and power generation, such as in biorefineries for the production of biofuels and biochemicals. Furthermore, the increasing global emphasis on circular economy principles and waste utilization creates opportunities for sourcing raw materials from agricultural residues and urban wood waste.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Untapped potential in emerging Asian markets (e.g., China, India) | +1.5% | Asia Pacific | Long-term (2027-2033) |

| Development of new applications (e.g., bio-chemicals, animal bedding) | +1.2% | Global | Mid-to-Long term (2026-2033) |

| Increased focus on biomass for district heating systems | +0.9% | Europe, North America | Mid-term (2025-2030) |

| Advancements in supply chain efficiency and storage technologies | +0.7% | Global | Mid-to-Long term (2025-2033) |

| Utilization of diverse raw material sources (e.g., agricultural residues) | +0.6% | Regions with abundant agricultural waste | Short-to-Mid term (2025-2028) |

Wood Pellet Market Challenges Impact Analysis

The wood pellet market is not without its challenges, which can impact its growth trajectory and operational stability. Ensuring the consistent quality and standardization of pellets across different producers and regions remains a hurdle, impacting efficiency and equipment lifespan for end-users. The significant capital investment required for establishing new production facilities, coupled with the long payback periods, can deter new entrants and limit expansion. Furthermore, public perception regarding the environmental impact of biomass sourcing, particularly concerning deforestation, necessitates robust sustainability certifications and transparent reporting to maintain social license to operate.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring consistent quality and standardization of pellets | -0.9% | Global, particularly importing markets | Long-term (2025-2033) |

| Infrastructure limitations for storage and transportation | -0.7% | Developing markets, Remote production areas | Mid-to-Long term (2025-2030) |

| Volatile energy prices affecting price competitiveness | -0.6% | Global | Short-term (2025-2026) |

| Regulatory complexities and varying certification requirements | -0.5% | International trade, Diverse regional markets | Mid-term (2025-2028) |

| Public perception and sustainability debates (e.g., land use, deforestation) | -0.4% | Europe, North America | Long-term (2025-2033) |

Wood Pellet Market - Updated Report Scope

This report provides an in-depth analysis of the global wood pellet market, offering comprehensive insights into its current state, historical performance, and future growth projections. It covers market size, key trends, drivers, restraints, opportunities, and challenges influencing the industry's evolution. The scope extends to a detailed segmentation analysis by various criteria, along with regional highlights, to provide a holistic view of the market dynamics. Special attention is given to the impact of emerging technologies like AI and the overall sustainability landscape affecting the industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 14.5 Billion |

| Market Forecast in 2033 | USD 24.8 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Enviva Inc., Drax Group plc, Pinnacle Renewable Energy Inc. (now part of Enviva), RWE AG, Georgia-Pacific LLC, Green Circle Bio Energy Inc., Fram Renewable Fuels, Lignetics International, Inc., Westervelt Co., AAE BioEnergy Inc., Sumitomo Corporation, Graanul Invest AS, PFEIFER Timber GmbH, German Pellets GmbH, Biomass Secure Power Inc., AS Graanul Invest, Zilkha Biomass Energy, Inc., The Navigator Company, Andritz AG, Valmet Corporation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

Market segmentation for wood pellets is crucial for understanding the diverse applications, end-user preferences, and raw material dynamics that shape the industry. This analysis categorizes the market based on primary application areas, the type of end-user, and the origin of raw materials used in pellet production. Such detailed segmentation helps stakeholders identify specific growth opportunities, tailor product offerings, and develop targeted market strategies. It also highlights the varied demands across different sectors, from large-scale industrial consumers to individual residential users.

By dissecting the market into distinct segments such as heating, power generation, and other applications, the report reveals the varying growth rates and drivers within each category. The end-use segmentation differentiates between industrial, residential, and commercial consumers, each with unique purchasing behaviors and requirements. Furthermore, understanding the raw material sources, whether from forest wood or agricultural residues, provides insights into supply chain resilience, sustainability practices, and the potential for diversification in raw material procurement. This multi-faceted view is essential for a comprehensive market assessment.

The segmentation also extends to pellet types, distinguishing between white pellets and black pellets, which differ in their processing and energy characteristics, catering to different industrial and commercial needs. Each segment is influenced by distinct regulatory landscapes, technological advancements, and economic factors. Analyzing these segments provides a granular understanding of market dynamics, enabling businesses to prioritize investments and innovation in areas with the highest potential return. This structured approach underpins strategic decision-making and fosters sustainable growth across the wood pellet value chain.

- By Application:

- Heating (Residential, Commercial, Industrial)

- Power Generation (Industrial Co-firing, Dedicated Power Plants)

- Animal Bedding

- Others (Absorbents, Biochemicals)

- By End-use:

- Industrial

- Residential

- Commercial

- By Raw Material:

- Forest Wood & Woody Biomass (Sawdust, Wood Chips, Forest Residues)

- Agricultural Residues (Corn Stover, Wheat Straw, Bagasse)

- By Type:

- White Pellets

- Black Pellets

Regional Highlights

The global wood pellet market exhibits distinct regional dynamics, influenced by varying energy policies, resource availability, and demand patterns. Europe stands as the dominant consuming region, driven by ambitious renewable energy targets and established biomass energy infrastructure. North America, particularly the United States and Canada, leads in production and export, leveraging abundant forest resources to supply international markets. These regional disparities create unique trade flows and market opportunities, with significant cross-border movement of pellets to meet demand where local supply is insufficient.

In Europe, countries like the UK, Denmark, Belgium, and the Netherlands are major importers for industrial co-firing in power plants, while Scandinavian countries and Germany show strong residential and district heating demand. The stringent sustainability criteria and certification schemes (e.g., Sustainable Biomass Program - SBP, ENplus) in Europe significantly shape global trade practices and incentivize sustainable sourcing. This region's commitment to decarbonization continues to solidify its position as the primary growth driver for industrial-grade pellets.

Asia Pacific, particularly Japan and South Korea, represents a rapidly emerging market for wood pellets, driven by new renewable energy mandates and a shift away from nuclear and fossil fuels. While demand is growing, infrastructure development for import and consumption is still evolving. Latin America and the Middle East & Africa regions currently have smaller market shares but offer long-term potential as awareness of biomass energy benefits increases and energy transition policies gain traction. These regions possess substantial untapped biomass resources that could contribute to future supply.

- Europe: Dominant consuming region, driven by industrial co-firing and residential heating; strict sustainability standards (ENplus, SBP) influence global supply chains. Key importers include the UK, Denmark, Belgium, Netherlands.

- North America: Leading producer and exporter, primarily the US and Canada, leveraging vast forest resources; significant supplier to European and Asian markets.

- Asia Pacific: Emerging market with rapid growth, especially Japan and South Korea, due to new renewable energy targets; increasing demand for industrial power generation.

- Latin America: Growing production capabilities, particularly in countries like Brazil; potential for increased domestic consumption and exports.

- Middle East & Africa (MEA): Nascent market with long-term growth potential as renewable energy adoption increases; focus on local resource utilization for energy security.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Wood Pellet Market.

- Enviva Inc.

- Drax Group plc

- Pinnacle Renewable Energy Inc.

- RWE AG

- Georgia-Pacific LLC

- Green Circle Bio Energy Inc.

- Fram Renewable Fuels

- Lignetics International, Inc.

- Westervelt Co.

- AAE BioEnergy Inc.

- Sumitomo Corporation

- Graanul Invest AS

- PFEIFER Timber GmbH

- German Pellets GmbH

- Biomass Secure Power Inc.

- AS Graanul Invest

- Zilkha Biomass Energy, Inc.

- The Navigator Company

- Andritz AG

- Valmet Corporation

Frequently Asked Questions

What are wood pellets primarily used for?

Wood pellets are primarily used as a renewable fuel source for heating and power generation. In residential and commercial settings, they serve as a clean and efficient fuel for pellet stoves and boilers. Industrially, they are widely used in large-scale power plants for co-firing with coal or as a dedicated biomass fuel, significantly reducing carbon emissions. Beyond energy, they also find applications in animal bedding, as absorbents, and increasingly, as a raw material in the production of biochemicals and biofuels.

Are wood pellets environmentally friendly?

The environmental friendliness of wood pellets is a complex topic, but generally, they are considered a carbon-neutral or low-carbon fuel when sourced sustainably. The carbon dioxide released during combustion is considered to be reabsorbed by new forest growth, forming part of the natural carbon cycle. However, their sustainability depends heavily on responsible forest management, avoiding clear-cutting of old-growth forests, and minimizing transportation distances. Certification schemes like ENplus and Sustainable Biomass Program (SBP) ensure adherence to strict environmental and social standards, verifying sustainable sourcing and production practices.

What factors influence the price of wood pellets?

The price of wood pellets is influenced by several factors. Raw material availability and cost, primarily wood waste from sawmills and forestry operations, play a significant role. Energy costs associated with the pelletization process, which includes drying and pressing, also contribute. Transportation and logistics expenses, particularly for international trade, can add substantially to the final price. Furthermore, seasonal demand for heating, global fossil fuel prices, and government policies or subsidies for renewable energy all impact market prices. Market competition and exchange rates can also cause price fluctuations.

Where are wood pellets typically sourced from?

Wood pellets are typically sourced from sustainable forest management practices, including residues from sawmills (sawdust, wood chips) and forest thinnings. In some cases, agricultural residues like corn stover or wheat straw are also used. Major producing regions include North America (especially the U.S. Southeast and Canada), which exports significantly to Europe and Asia. Europe also has substantial domestic production, particularly in Scandinavian countries and Central Europe, but remains a net importer to meet its high demand for biomass energy.

What is the difference between white and black pellets?

The primary difference between white and black pellets lies in their processing and properties. White pellets are standard wood pellets, typically light in color, made from virgin wood or wood residues. They are dried and compressed but not torrefied. Black pellets, also known as torrefied pellets, undergo an additional thermal treatment called torrefaction. This process removes moisture and volatile organic compounds, resulting in a more hydrophobic, energy-dense, and durable pellet that behaves more like coal, making it particularly suitable for industrial co-firing applications and easier, safer storage.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted