Wireless RAN Market

Wireless RAN Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706205 | Last Updated : August 17, 2025 |

Format : ![]()

![]()

![]()

![]()

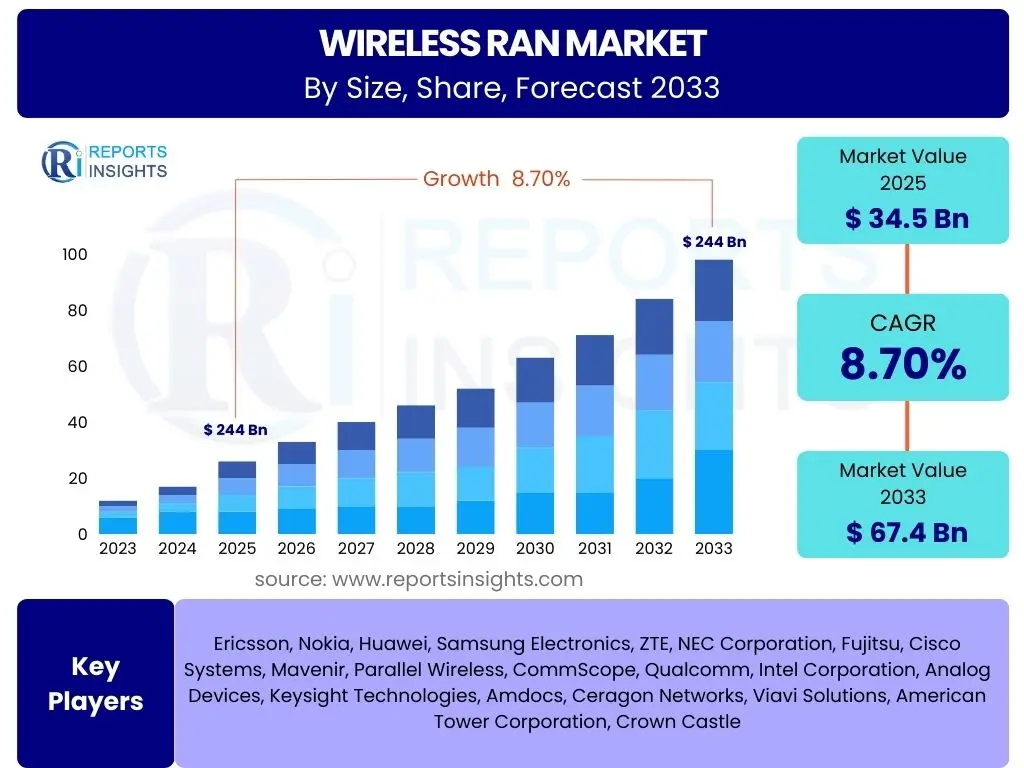

Wireless RAN Market Size

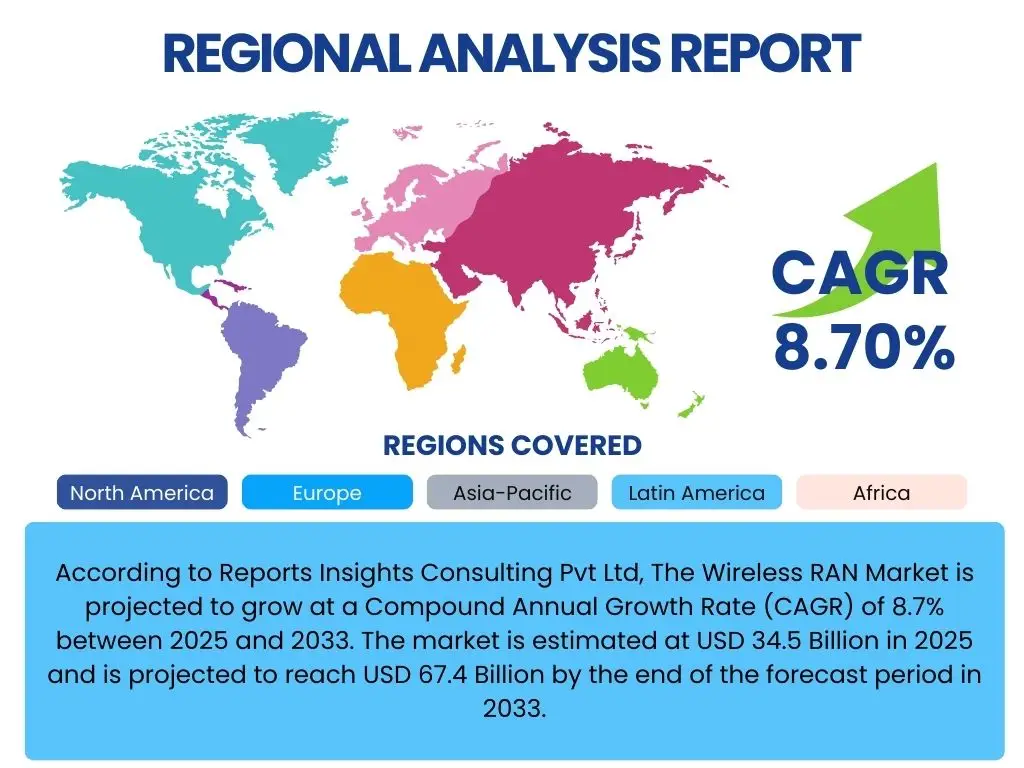

According to Reports Insights Consulting Pvt Ltd, The Wireless RAN Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.7% between 2025 and 2033. The market is estimated at USD 34.5 Billion in 2025 and is projected to reach USD 67.4 Billion by the end of the forecast period in 2033.

Key Wireless RAN Market Trends & Insights

User inquiries frequently highlight the rapid evolution of network architectures and capabilities within the Wireless RAN sector. A dominant theme revolves around the progression from traditional, closed RAN systems towards more open, virtualized, and disaggregated approaches. Stakeholders are keen to understand the implications of 5G Standalone (SA) deployments, the increasing role of private networks, and the integration of artificial intelligence for enhanced network management and optimization. There is significant interest in how these trends will shape future investments, operational efficiencies, and the competitive landscape, emphasizing the shift towards flexible, software-defined infrastructure.

The market is experiencing a significant paradigm shift driven by the demand for higher bandwidth, lower latency, and greater connectivity densities. This includes the accelerated global rollout of 5G networks, which is the primary catalyst for RAN infrastructure upgrades and expansions. Moreover, the emergence of non-traditional deployment models, such as private 5G networks for industrial use cases and fixed wireless access (FWA) solutions, is broadening the application scope of RAN technology beyond conventional mobile broadband services. These developments are fostering innovation in antenna technologies, radio units, and baseband processing, moving towards more distributed and intelligent network edge architectures.

- Accelerated global 5G Standalone (SA) network deployments.

- Increasing adoption of Open RAN architectures for vendor diversification and cost reduction.

- Proliferation of private 5G networks across various industries.

- Integration of artificial intelligence and machine learning for network automation and optimization.

- Expansion of Fixed Wireless Access (FWA) as an alternative to fiber broadband.

- Growing focus on energy efficiency and sustainability in RAN infrastructure.

- Development of intelligent edge computing capabilities within RAN.

AI Impact Analysis on Wireless RAN

User queries regarding artificial intelligence's impact on Wireless RAN consistently point towards expectations of profound operational transformation. Common questions focus on how AI can automate complex network tasks, optimize resource allocation, predict and prevent failures, and enhance overall network performance and security. Users are interested in understanding the specific applications of AI in RAN, ranging from intelligent traffic management and dynamic spectrum sharing to predictive maintenance and anomaly detection. Concerns also include the data requirements for effective AI implementation and the integration challenges with existing infrastructure, highlighting a strong desire for practical, demonstrable benefits in network efficiency and reliability.

Artificial intelligence is poised to revolutionize Wireless RAN operations by enabling unprecedented levels of automation and intelligence. AI algorithms can analyze vast amounts of network data in real-time, identifying patterns, predicting potential issues, and optimizing network parameters autonomously. This capability extends to various aspects of RAN, including dynamic resource allocation for optimal user experience, proactive fault detection and self-healing mechanisms, and intelligent energy management to reduce operational expenditure. The integration of AI also facilitates advanced security protocols, enabling rapid detection and mitigation of cyber threats, thereby making networks more resilient and robust against evolving challenges.

- Enhanced network automation for self-organizing networks (SON).

- Predictive maintenance for proactive fault detection and resolution.

- Optimized resource allocation and dynamic spectrum management.

- Improved energy efficiency through intelligent power management.

- Advanced security threat detection and mitigation.

- Real-time traffic management and anomaly detection.

- Facilitation of network slicing for customized service delivery.

Key Takeaways Wireless RAN Market Size & Forecast

Analysis of common user questions about the Wireless RAN market size and forecast reveals a strong interest in understanding the primary growth drivers, the longevity of current trends, and the potential for disruptive technologies. Users are keenly interested in identifying the key segments poised for significant expansion, the regional hotspots of growth, and the overall trajectory of market valuation. There is a consistent demand for clear insights into how technological advancements, particularly 5G and future generations, will sustain or accelerate market expansion, alongside an assessment of potential market inhibitors and emerging opportunities that could reshape the forecast.

The Wireless RAN market is on a robust growth trajectory, primarily fueled by the pervasive global rollout of 5G infrastructure and the increasing demand for high-speed, low-latency connectivity. The shift towards Open RAN architectures is also a significant factor, promising to lower deployment costs and foster innovation through greater vendor diversity. While substantial investments are required for network upgrades and expansions, the long-term benefits of enhanced capacity, improved service delivery, and the enablement of new applications like IoT and private networks are driving continued market expansion. Regional disparities in 5G adoption and economic development will influence growth rates, with Asia Pacific and North America leading the market in terms of infrastructure deployment and early adoption of advanced RAN technologies.

- Market size projected to nearly double from 2025 to 2033, indicating sustained robust growth.

- 5G network expansion remains the primary growth catalyst across all regions.

- Open RAN and virtualized RAN (vRAN) are key technological shifts driving future market dynamics.

- Emerging opportunities in private networks and industrial IoT will contribute significantly to market expansion.

- North America and Asia Pacific are anticipated to be leading regions in terms of market value and adoption.

- Operational efficiency and energy consumption will be critical focus areas for RAN innovation.

Wireless RAN Market Drivers Analysis

The Wireless RAN market is experiencing significant tailwinds propelled by a confluence of technological advancements and increasing connectivity demands. The pervasive global rollout of 5G networks stands as the foremost driver, necessitating substantial investments in new radio units, antennas, and baseband infrastructure capable of handling higher frequencies, massive MIMO, and beamforming technologies. This deployment is not just about enhancing mobile broadband but also about enabling new services like ultra-reliable low-latency communications (URLLC) and massive machine-type communications (mMTC) that underpin the Internet of Things (IoT) revolution. Furthermore, the growing adoption of cloud-native principles and network virtualization is driving demand for more flexible and scalable RAN solutions, influencing operators to modernize their networks and embrace software-defined approaches.

Beyond core mobile services, the proliferation of connected devices, smart city initiatives, and enterprise digital transformation strategies are creating new avenues for RAN market growth. Industries are increasingly recognizing the value of dedicated private 5G networks to support mission-critical applications, improve operational efficiency, and ensure data security on premise. This bespoke deployment model, often leveraging specific RAN components optimized for industrial environments, represents a burgeoning segment. Additionally, government initiatives and funding programs aimed at improving digital infrastructure and bridging the digital divide are providing crucial impetus for network expansion, particularly in underserved rural areas, further bolstering the demand for Wireless RAN solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global 5G Network Rollouts | +2.5% | Global, particularly North America, Asia Pacific, Europe | 2025-2033 |

| Increasing Mobile Data Traffic & Connected Devices | +1.8% | Global | 2025-2033 |

| Growing Adoption of IoT and Industry 4.0 | +1.5% | North America, Europe, Asia Pacific (China, Japan, South Korea) | 2026-2033 |

| Demand for Private 5G Networks | +1.2% | North America, Europe, parts of Asia Pacific (Germany, USA, Japan) | 2026-2033 | Government Initiatives for Digital Infrastructure Development | +0.8% | Emerging Economies, Rural Areas (India, Southeast Asia, Africa) | 2025-2030 |

Wireless RAN Market Restraints Analysis

Despite the significant growth prospects, the Wireless RAN market faces several inherent challenges that could temper its expansion. One of the primary restraints is the exorbitant capital expenditure (CAPEX) required for network deployment and upgrades. Rolling out new generations of RAN technology, particularly 5G, involves substantial investments in spectrum acquisition, infrastructure, site preparation, and equipment. For many telecom operators, especially in competitive or financially constrained markets, these costs present a significant barrier to rapid and widespread deployment, leading to slower modernization cycles and limited expansion into new areas. This financial burden is compounded by the increasing complexity of modern RAN architectures, which demand specialized skills and sophisticated management tools.

Furthermore, regulatory complexities and spectrum availability issues pose additional hurdles. Governments worldwide control spectrum allocation, and the release of suitable frequencies for 5G and future technologies can be slow, inconsistent, or prohibitively expensive, directly impacting deployment timelines and costs. Strict regulatory environments regarding site acquisition, environmental impact assessments, and public health concerns related to electromagnetic fields can also delay or complicate network rollout. Supply chain disruptions, exacerbated by geopolitical tensions and global events, can lead to shortages of critical components, affecting manufacturing and delivery schedules of RAN equipment. Lastly, intense competition among vendors often leads to price erosion, impacting profitability margins across the value chain, even as R&D costs remain high due to rapid technological evolution.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure for Network Deployments | -1.5% | Global, particularly developing regions | 2025-2033 |

| Spectrum Availability and Cost | -1.0% | Global (varies by country) | 2025-2030 |

| Complex Regulatory Frameworks & Permitting Issues | -0.8% | Europe, parts of North America | 2025-2030 |

| Supply Chain Disruptions and Component Shortages | -0.7% | Global | 2025-2028 |

| Energy Consumption and Sustainability Concerns | -0.5% | Europe, North America, Japan | 2028-2033 |

Wireless RAN Market Opportunities Analysis

The Wireless RAN market is rich with opportunities stemming from evolving network paradigms and the expanding ecosystem of connected services. The advent of Open RAN represents a transformative opportunity, as it promises to disaggregate traditional vendor lock-ins and foster a more open, competitive, and innovative supply chain. This architectural shift allows operators to mix and match components from various vendors, potentially leading to significant cost efficiencies, increased flexibility, and faster deployment cycles for new features. The standardization efforts within the O-RAN Alliance are gaining momentum, paving the way for widespread commercial deployments and attracting a broader range of technology providers, including smaller, specialized companies.

Another significant opportunity lies in the burgeoning market for private 5G networks. As enterprises across manufacturing, logistics, healthcare, and mining seek dedicated, high-performance, and secure wireless connectivity for their specific operational needs, private 5G offers a compelling solution. This allows businesses to deploy their own localized networks, ensuring ultra-low latency, high reliability, and enhanced security for critical applications like automated guided vehicles (AGVs), real-time sensor data collection, and augmented reality (AR) for industrial training. Furthermore, the expansion of Fixed Wireless Access (FWA) as a viable alternative to fiber broadband, particularly in suburban and rural areas, presents a substantial market for RAN equipment, leveraging existing 5G infrastructure to deliver high-speed internet to homes and businesses. The continuous evolution towards 6G research and development also opens long-term opportunities for next-generation RAN technologies.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Adoption of Open RAN Architectures | +1.7% | North America, Europe, Japan | 2026-2033 |

| Expansion of Private 5G Networks for Enterprises | +1.4% | Global, particularly industrial hubs | 2026-2033 |

| Growth in Fixed Wireless Access (FWA) Deployments | +1.1% | North America, Europe, Developing Regions | 2025-2030 |

| Integration with Edge Computing for New Services | +0.9% | Global | 2027-2033 |

| Development of 6G Technology & Standards | +0.6% | North America, Asia Pacific (China, South Korea), Europe | 2030-2033 |

Wireless RAN Market Challenges Impact Analysis

The Wireless RAN market, while growing, confronts several critical challenges that demand strategic responses from industry players. One significant hurdle is the escalating complexity of network management as RAN architectures evolve towards virtualization and disaggregation. Operators face difficulties integrating diverse hardware and software components from multiple vendors in an Open RAN environment, ensuring seamless interoperability, and maintaining optimal performance across the network. This complexity necessitates advanced orchestration tools and skilled personnel, which can be scarce resources, leading to operational inefficiencies and increased operational expenditure (OPEX) in the short term. The transition from legacy systems to new, cloud-native RAN deployments also presents significant migration challenges, requiring careful planning and execution.

Another pressing challenge revolves around cybersecurity. As RAN becomes more software-centric and distributed, the attack surface expands, making networks more vulnerable to sophisticated cyber threats. Ensuring robust security across a multi-vendor, disaggregated RAN, especially in critical infrastructure, is paramount but inherently complex. Furthermore, the high energy consumption of RAN infrastructure, particularly with increased cell density and advanced technologies like massive MIMO, poses a substantial environmental and financial challenge. Operators are under pressure to reduce their carbon footprint and operational costs, driving a need for more energy-efficient RAN solutions. Rapid technological obsolescence and the need for continuous innovation to stay competitive also place a burden on R&D investments and network upgrade cycles, forcing companies to balance cutting-edge development with economic viability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Interoperability and Integration Challenges in Open RAN | -1.2% | Global | 2025-2029 |

| Cybersecurity Threats and Network Vulnerabilities | -1.0% | Global | 2025-2033 |

| Shortage of Skilled Workforce for New Technologies | -0.9% | North America, Europe, parts of Asia Pacific | 2025-2033 |

| High Energy Consumption of RAN Infrastructure | -0.8% | Global | 2025-2033 |

| Rapid Technological Obsolescence | -0.6% | Global | 2025-2033 |

Wireless RAN Market - Updated Report Scope

This report provides an in-depth analysis of the Wireless Radio Access Network (RAN) market, encompassing comprehensive insights into market size, growth trends, and future projections across various segments and key geographical regions. It delves into the underlying drivers propelling market expansion, the significant restraints impacting growth, and the emergent opportunities poised to reshape the industry landscape. The study further incorporates a detailed assessment of the challenges faced by market participants, offering a holistic perspective on the competitive environment and the strategic imperatives for stakeholders. Special emphasis is placed on the transformative impact of artificial intelligence on RAN operations and the evolving architectural shifts such as Open RAN.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 34.5 Billion |

| Market Forecast in 2033 | USD 67.4 Billion |

| Growth Rate | 8.7% CAGR |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Ericsson, Nokia, Huawei, Samsung Electronics, ZTE, NEC Corporation, Fujitsu, Cisco Systems, Mavenir, Parallel Wireless, CommScope, Qualcomm, Intel Corporation, Analog Devices, Keysight Technologies, Amdocs, Ceragon Networks, Viavi Solutions, American Tower Corporation, Crown Castle |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Wireless RAN market is segmented across several critical dimensions, providing a granular view of its structure and growth dynamics. These segments allow for a detailed analysis of market performance based on technology generation, the type of components utilized, the deployment scale, and the diverse end-user applications. This comprehensive segmentation highlights the varying demands and adoption patterns across different facets of the wireless communication ecosystem, from established mobile broadband services to emerging private industrial networks. Understanding these segments is crucial for identifying specific growth pockets and tailoring strategic initiatives within the highly dynamic RAN landscape.

- By Technology: This segment includes different generations of wireless technology.

- 4G (LTE, LTE-Advanced, VoLTE): Represents the established backbone of mobile connectivity, still undergoing upgrades and capacity enhancements.

- 5G (Sub-6 GHz, mmWave): The primary growth driver, encompassing both lower frequency deployments for wide coverage and higher frequency for ultra-high capacity.

- 6G (Emerging): Future generation technology, currently in research and early development phases, signaling long-term innovation.

- By Component: Categorizes the essential parts that constitute a RAN system.

- Hardware (Base Stations, Antennas, RRUs/RRHs, Baseband Units): Physical infrastructure components crucial for signal transmission and processing.

- Software (RAN Software, Orchestration & Management Software, Virtualization Software): Controls network functions, enables automation, and supports cloud-native deployments.

- Services (Deployment, Integration, Maintenance & Support, Professional Services): Encompasses the activities required to set up, manage, and optimize RAN infrastructure.

- By Deployment Type: Differentiates based on the coverage area and capacity requirements.

- Macrocell: Large-scale deployments providing wide area coverage.

- Small Cell (Pico cell, Femtocell, Microcell): Smaller, lower-power deployments used to enhance capacity and coverage in specific, dense areas.

- By End-User: Identifies the primary beneficiaries and adopters of RAN technology.

- Telecom Operators: Traditional mobile network providers.

- Enterprises (Manufacturing, Energy & Utilities, Transportation & Logistics, Healthcare, Retail, Government & Public Safety): Organizations deploying private networks for dedicated use cases.

- Others: Includes academic institutions, research organizations, and niche applications.

Regional Highlights

- North America: This region demonstrates robust growth driven by aggressive 5G deployments, significant investments in private enterprise networks, and strong adoption of Open RAN initiatives. The presence of key technology innovators and a high demand for advanced connectivity solutions characterize this market.

- Europe: Characterized by diverse regulatory landscapes and varying paces of 5G rollout, Europe is increasingly focusing on energy efficiency and sustainable RAN solutions. Open RAN pilot projects and government support for digital infrastructure are key drivers.

- Asia Pacific (APAC): Expected to be the fastest-growing region, led by massive 5G deployments in China, South Korea, Japan, and India. The region benefits from large population bases, rapid urbanization, and significant government investments in digital infrastructure, along with the emergence of local RAN technology providers.

- Latin America: This region shows promising growth as countries accelerate their 5G network rollouts and address the demand for improved digital connectivity, particularly in urban centers and for industrial applications. Investment in infrastructure upgrades is steadily increasing.

- Middle East and Africa (MEA): Marked by substantial investments in smart city projects and digital transformation initiatives, particularly in the Gulf Cooperation Council (GCC) countries. Africa's market is driven by increasing mobile penetration and efforts to bridge the digital divide, making it an attractive region for both traditional and innovative RAN deployments.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Wireless RAN Market.- Ericsson

- Nokia

- Huawei

- Samsung Electronics

- ZTE

- NEC Corporation

- Fujitsu

- Cisco Systems

- Mavenir

- Parallel Wireless

- CommScope

- Qualcomm

- Intel Corporation

- Analog Devices

- Keysight Technologies

- Amdocs

- Ceragon Networks

- Viavi Solutions

- American Tower Corporation

- Crown Castle

Frequently Asked Questions

What is Wireless RAN?

Wireless RAN, or Radio Access Network, is a crucial component of a wireless telecommunications system that connects individual devices (like mobile phones or IoT devices) to other parts of a network through radio connections. It typically includes base stations, antennas, and associated hardware and software that manage radio communication between user equipment and the core network.

What are the primary drivers of the Wireless RAN market growth?

The primary drivers include the accelerated global rollout of 5G networks, the exponential growth in mobile data traffic, the increasing adoption of IoT and Industry 4.0 applications, and the rising demand for private 5G networks for enterprises. Government initiatives and digital transformation efforts also significantly contribute to market expansion.

How is Open RAN impacting the Wireless RAN market?

Open RAN is a disaggregated and open radio access network architecture that allows for greater interoperability between different vendors' hardware and software components. It is significantly impacting the market by fostering vendor diversification, promoting innovation, potentially reducing deployment costs, and offering greater network flexibility and scalability.

What challenges does the Wireless RAN market face?

Key challenges include high capital expenditure for network deployments, complexities in spectrum availability and regulatory frameworks, cybersecurity threats in increasingly disaggregated networks, the high energy consumption of RAN infrastructure, and the continuous need to manage rapid technological obsolescence and skilled workforce shortages.

Which regions are leading the Wireless RAN market in terms of growth?

Asia Pacific is projected to be the fastest-growing region due to extensive 5G deployments in countries like China, South Korea, Japan, and India. North America also remains a dominant market, driven by advanced technological adoption and significant investments in private networks and Open RAN.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted