Wireless Backhaul and 5G via Satellite Market

Wireless Backhaul and 5G via Satellite Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701399 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

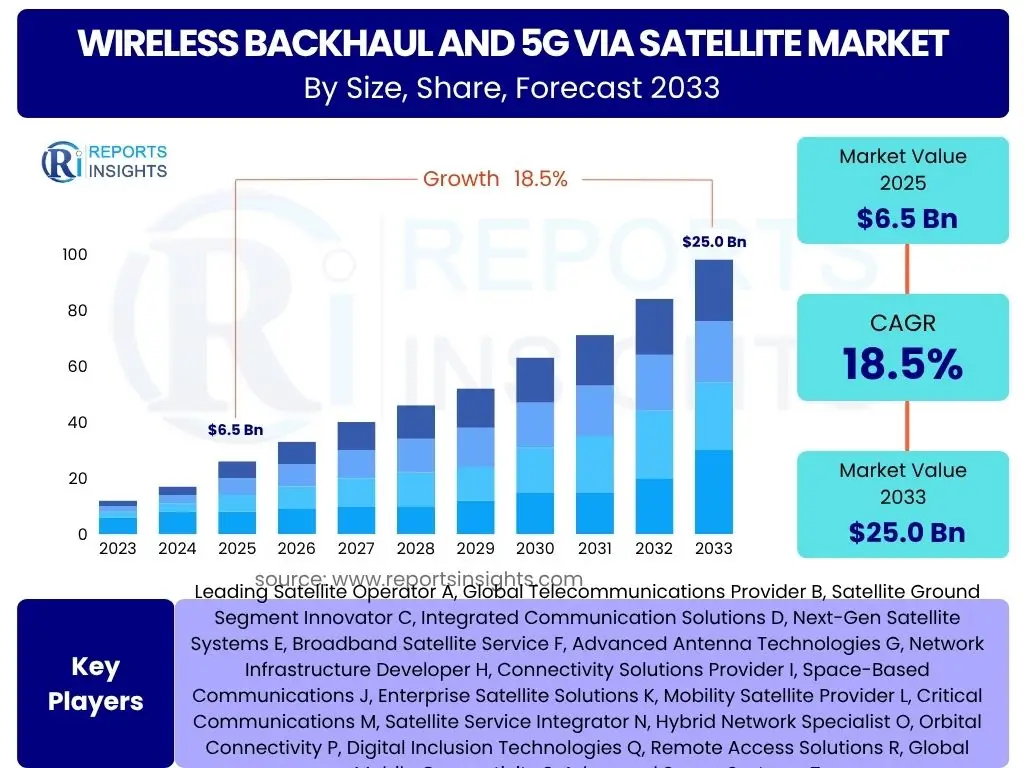

Wireless Backhaul and 5G via Satellite Market Size

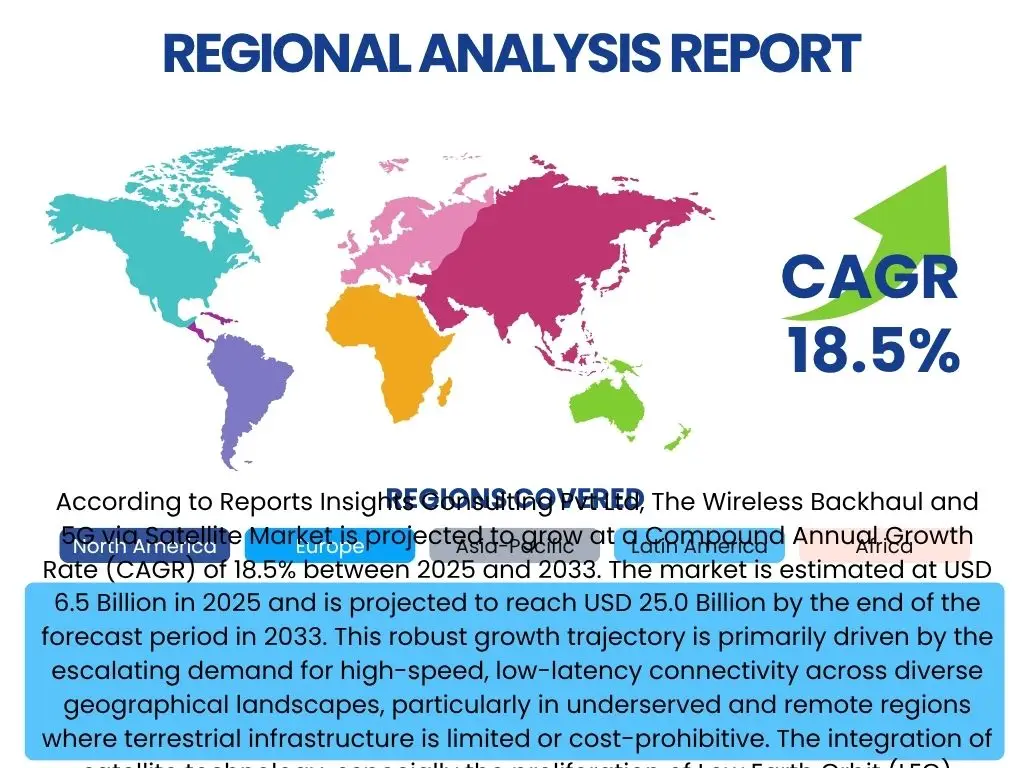

According to Reports Insights Consulting Pvt Ltd, The Wireless Backhaul and 5G via Satellite Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033. The market is estimated at USD 6.5 Billion in 2025 and is projected to reach USD 25.0 Billion by the end of the forecast period in 2033. This robust growth trajectory is primarily driven by the escalating demand for high-speed, low-latency connectivity across diverse geographical landscapes, particularly in underserved and remote regions where terrestrial infrastructure is limited or cost-prohibitive. The integration of satellite technology, especially the proliferation of Low Earth Orbit (LEO) constellations, is significantly enhancing the viability and performance of wireless backhaul solutions for 5G networks.

The expansion of 5G networks globally necessitates ubiquitous high-bandwidth backhaul solutions that can support the increased data traffic and stringent latency requirements of next-generation applications. While fiber optic and microwave links serve as primary backhaul in urban and suburban areas, satellites offer an unparalleled advantage in extending 5G coverage to rural, maritime, and aerial environments. This inherent capability positions satellite-based backhaul as a critical enabler for true 5G ubiquitous connectivity, driving considerable investment and innovation within the sector. The market's expansion is further supported by the growing need for reliable communication in critical infrastructure, disaster recovery, and specialized enterprise applications.

Key Wireless Backhaul and 5G via Satellite Market Trends & Insights

User inquiries frequently highlight the transformative shifts occurring in the Wireless Backhaul and 5G via Satellite market, emphasizing the move towards more integrated and dynamic network architectures. Common questions revolve around the impact of new satellite constellations, the convergence of satellite and terrestrial communication standards, and the adoption patterns across different industry verticals. There is significant interest in how these trends are addressing connectivity gaps, improving network resilience, and enabling new service models, particularly in challenging environments. Users seek to understand the implications of these developments for network operators, service providers, and end-users, focusing on efficiency, cost-effectiveness, and performance enhancements.

A prominent trend is the increasing deployment and operationalization of Low Earth Orbit (LEO) and Medium Earth Orbit (MEO) satellite constellations. These non-geostationary orbit (NGSO) satellites offer significantly lower latency and higher bandwidth capacities compared to traditional Geostationary Earth Orbit (GEO) satellites, making them more suitable for latency-sensitive 5G applications such as real-time video, augmented reality, and industrial IoT. This shift is not only improving performance but also driving down the cost per bit, making satellite backhaul a more competitive and attractive option for mobile network operators (MNOs) seeking to expand their 5G footprint globally. The ability of LEO/MEO constellations to provide global coverage also simplifies network planning and deployment for operators targeting widespread connectivity.

Another critical trend is the growing convergence between satellite and terrestrial communication infrastructures. This involves the development of hybrid networks that seamlessly integrate satellite links into existing 5G core networks, utilizing common standards and protocols. Initiatives like 3GPP Release 17 and beyond are actively defining specifications for Non-Terrestrial Networks (NTN) integration into 5G, fostering interoperability and enabling a unified network experience. This convergence facilitates seamless handovers between terrestrial and satellite networks, optimizes resource utilization, and enhances overall network resilience by providing redundant communication paths. Furthermore, the increasing adoption of Software-Defined Networking (SDN) and Network Function Virtualization (NFV) principles within satellite ground segments is allowing for greater flexibility, automation, and efficiency in managing complex hybrid networks.

- Proliferation of LEO and MEO satellite constellations for lower latency and higher throughput.

- Deepening convergence and integration of satellite and terrestrial 5G networks, driven by 3GPP NTN standards.

- Increased adoption of hybrid network architectures for enhanced resilience and extended coverage.

- Growth in demand for satellite backhaul from enterprise and private 5G networks.

- Advancements in phased array antennas and ground segment technology reducing costs and simplifying deployment.

- Focus on software-defined satellites and virtualized ground infrastructure for flexible service delivery.

- Emergence of satellite-as-a-service models and managed backhaul solutions.

AI Impact Analysis on Wireless Backhaul and 5G via Satellite

User inquiries concerning AI's influence on Wireless Backhaul and 5G via Satellite primarily focus on how artificial intelligence can optimize network performance, enhance operational efficiency, and mitigate complex challenges within these intricate systems. Common themes include the role of AI in intelligent resource allocation, predictive maintenance for satellite assets, dynamic spectrum management, and bolstering network security. Users are keen to understand how AI can move beyond traditional automation to enable truly autonomous network operations, reduce human intervention, and deliver superior quality of service, particularly given the dynamic nature of satellite links and the diverse demands of 5G applications.

Artificial intelligence is poised to revolutionize the management and optimization of wireless backhaul and 5G via satellite networks by enabling unprecedented levels of automation and intelligence. AI algorithms can analyze vast amounts of real-time network data, including traffic patterns, satellite link performance, weather conditions, and hardware health, to predict potential issues and dynamically reconfigure network resources. For instance, AI-driven systems can optimize satellite beamforming, adjust power levels, and re-route traffic to minimize latency and maximize throughput, ensuring consistent connectivity even in challenging conditions. This predictive capability significantly reduces downtime, enhances network reliability, and improves the overall quality of experience for end-users, which is crucial for 5G's demanding applications.

Beyond network optimization, AI also plays a critical role in enhancing the security and resilience of satellite-enabled 5G backhaul. With the increasing complexity of hybrid networks and the growing threat landscape, AI-powered anomaly detection systems can identify and respond to cyber threats in real-time, protecting sensitive data and preventing service disruptions. Furthermore, AI contributes to efficient spectrum management by dynamically allocating frequencies based on demand and interference levels, maximizing spectrum utilization and preventing congestion. The application of AI extends to autonomous network orchestration, where intelligent agents can manage network slices, automate provisioning, and even handle self-healing mechanisms, paving the way for highly adaptive and self-sustaining satellite-5G ecosystems.

- AI-driven network optimization for dynamic resource allocation and traffic management.

- Predictive maintenance for satellite ground stations and space assets, reducing operational costs.

- Intelligent fault detection and self-healing capabilities for enhanced network resilience.

- AI-powered cybersecurity solutions for real-time threat detection and response.

- Dynamic spectrum sharing and interference management for efficient spectrum utilization.

- Automated provisioning and orchestration of network slices in hybrid satellite-terrestrial environments.

- Enhanced quality of service (QoS) and experience (QoE) through AI-informed network adjustments.

Key Takeaways Wireless Backhaul and 5G via Satellite Market Size & Forecast

User inquiries regarding the market size and forecast for Wireless Backhaul and 5G via Satellite often seek confirmation of the market's growth drivers, the strategic importance of satellite technology in future communication infrastructures, and the tangible benefits for various stakeholders. There is a clear interest in understanding how the projected market expansion aligns with global connectivity initiatives, particularly for unserved and underserved populations. Users also aim to grasp the commercial viability and technological readiness that underpin this growth, seeking reassurance about the long-term investment prospects and the ability of satellite solutions to meet the evolving demands of 5G and beyond.

The Wireless Backhaul and 5G via Satellite market is poised for substantial expansion, reflecting its pivotal role in realizing global 5G ubiquitous connectivity. The forecast growth rate of 18.5% CAGR indicates a significant market acceleration, primarily fueled by the imperative to extend high-speed broadband to areas lacking robust terrestrial infrastructure. This growth underscores the increasing recognition among mobile network operators (MNOs) and internet service providers (ISPs) that satellite technology is not merely a fallback option but a primary, cost-effective, and scalable solution for backhauling 5G traffic from remote base stations, fixed wireless access points, and moving platforms. The shift towards LEO and MEO constellations is a critical enabler, providing the necessary low latency and high throughput to support advanced 5G use cases.

A key takeaway from the market forecast is the growing strategic importance of satellite communication in building resilient and inclusive digital ecosystems. As 5G deployments intensify, the demand for versatile backhaul solutions that can adapt to diverse geographic and demographic needs will continue to surge. Satellite backhaul facilitates the rapid deployment of 5G networks in rural and remote areas, promotes digital inclusion, and supports critical applications such as disaster recovery and emergency communications where terrestrial networks may fail. Furthermore, the market's trajectory suggests increasing integration of satellite capabilities into the core network architecture of telecommunication providers, moving beyond niche applications to become an integral component of the global 5G infrastructure.

- The market is experiencing robust growth, driven by the global expansion of 5G and the need for pervasive connectivity.

- Satellite technology, particularly LEO and MEO constellations, is becoming indispensable for extending 5G coverage to remote and underserved areas.

- High-throughput and low-latency satellite solutions are addressing key 5G requirements for diverse applications.

- Investment in satellite infrastructure and ground segment technologies is accelerating to support demand.

- Satellite backhaul is crucial for enabling digital inclusion and bridging the connectivity gap globally.

Wireless Backhaul and 5G via Satellite Market Drivers Analysis

The Wireless Backhaul and 5G via Satellite market is primarily driven by the escalating global demand for high-speed, reliable connectivity, particularly in areas beyond the reach of traditional terrestrial networks. As 5G technology continues its rapid deployment worldwide, the need for robust backhaul solutions capable of handling increased data volumes and stricter latency requirements becomes paramount. Satellite-based backhaul offers an ideal solution for extending 5G coverage to rural populations, remote enterprises, and mobility platforms such as maritime vessels and aircraft, where fiber or microwave deployment is impractical or prohibitively expensive.

The significant advancements in satellite technology, notably the advent of Low Earth Orbit (LEO) and Medium Earth Orbit (MEO) constellations, are transforming the landscape of satellite communication. These next-generation satellites offer substantially lower latency and higher throughput compared to traditional Geostationary Earth Orbit (GEO) satellites, making them highly compatible with the performance demands of 5G networks. This technological evolution has significantly improved the economic viability and technical performance of satellite backhaul, making it a more attractive and competitive option for mobile network operators (MNOs) and internet service providers (ISPs).

Furthermore, the increasing adoption of IoT devices and the growing need for critical communication networks are significant market drivers. IoT applications, particularly in industrial, agricultural, and logistics sectors, often require connectivity in remote locations, making satellite backhaul an indispensable component. Similarly, government and defense sectors increasingly rely on resilient, ubiquitous communication for disaster response, national security, and remote operations, for which satellite-enabled 5G backhaul provides unparalleled reliability and reach.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global demand for high-speed 5G connectivity in remote areas | +5.0% | Global, particularly Sub-Saharan Africa, parts of Asia Pacific, Latin America | 2025-2033 |

| Proliferation of LEO and MEO satellite constellations | +4.5% | Global, with emphasis on North America, Europe, Asia Pacific | 2025-2033 |

| Increased adoption of IoT and critical communication applications | +3.5% | Global, with focus on industrial hubs, developing economies | 2026-2033 |

| Government initiatives for digital inclusion and broadband access | +3.0% | Developing nations in APAC, Africa, Latin America | 2025-2030 |

| Growing demand for enterprise private 5G networks in remote sites | +2.5% | North America, Europe, parts of Asia Pacific | 2027-2033 |

| Technological advancements in ground segment equipment (e.g., flat panel antennas) | +2.0% | Global | 2025-2030 |

| Need for resilient networks for disaster recovery and business continuity | +1.5% | Regions prone to natural disasters (e.g., Southeast Asia, Caribbean) | 2025-2033 |

Wireless Backhaul and 5G via Satellite Market Restraints Analysis

Despite the significant growth potential, the Wireless Backhaul and 5G via Satellite market faces several notable restraints that could temper its expansion. One of the primary barriers is the high initial capital expenditure required for deploying satellite ground infrastructure, including antennas, modems, and associated network equipment. While satellite service costs are becoming more competitive, the upfront investment for a comprehensive satellite backhaul solution can be substantial, particularly for smaller mobile network operators or enterprises. This financial hurdle can slow down adoption, especially in price-sensitive emerging markets where budget constraints are more pronounced.

Another significant restraint is the inherent latency associated with Geostationary Earth Orbit (GEO) satellites. Although LEO and MEO constellations dramatically reduce latency, a substantial portion of existing satellite infrastructure still relies on GEO satellites, which introduce a noticeable delay in communication due. This latency can be a bottleneck for extremely time-sensitive 5G applications such as real-time gaming, autonomous vehicles, or industrial control systems, where even milliseconds of delay can impact performance. While LEO/MEO systems are addressing this, the widespread transition and full utilization of these new constellations take time and significant investment.

Furthermore, regulatory complexities and spectrum allocation challenges pose considerable hurdles. The assignment and management of satellite spectrum are governed by international and national bodies, often leading to intricate licensing processes and potential conflicts with terrestrial spectrum usage. Harmonizing regulatory frameworks across different countries and ensuring equitable access to crucial frequency bands remains a persistent challenge. These regulatory intricacies can delay deployments, increase compliance costs, and limit the scalability of satellite backhaul solutions, thereby impacting market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High initial capital expenditure for ground infrastructure | -3.5% | Global, particularly developing regions | 2025-2030 |

| Latency challenges, especially with GEO satellites | -2.0% | Global, impacting latency-sensitive applications | 2025-2028 |

| Regulatory complexities and spectrum allocation challenges | -2.5% | Global, with varied impact by regional regulatory bodies | 2025-2033 |

| Competition from established terrestrial backhaul solutions (fiber, microwave) | -1.5% | Developed urban and suburban areas | 2025-2033 |

| Interoperability and standardization challenges for hybrid networks | -1.0% | Global, affecting integration efforts | 2025-2029 |

| Cybersecurity vulnerabilities in complex satellite-terrestrial networks | -1.0% | Global | 2025-2033 |

| Skilled workforce shortage for advanced satellite network management | -0.8% | Global, especially in specialized technical roles | 2026-2033 |

Wireless Backhaul and 5G via Satellite Market Opportunities Analysis

The Wireless Backhaul and 5G via Satellite market is rich with opportunities, primarily driven by the vast untapped potential in connecting underserved and unserved populations globally. Billions of people still lack reliable internet access, particularly in rural and remote areas where deploying traditional fiber or cellular infrastructure is economically unfeasible. Satellite backhaul, leveraging new LEO and MEO constellations, offers a scalable and cost-effective solution to bridge this digital divide, enabling mobile network operators and internet service providers to expand their reach into these previously inaccessible markets and unlock new revenue streams.

The growth of enterprise private 5G networks presents another significant opportunity. Industries such as mining, oil and gas, agriculture, logistics, and manufacturing often operate in remote locations requiring dedicated, high-performance connectivity for IoT, automation, and real-time data processing. Satellite backhaul can provide the foundational connectivity for these private networks, ensuring seamless communication between on-site devices and cloud-based applications, enhancing operational efficiency and safety. This specialized application segment is expected to see substantial growth as more enterprises embrace digitalization and require robust, independent communication infrastructures.

Furthermore, the increasing emphasis on network resilience and disaster recovery planning creates substantial opportunities for satellite backhaul. In scenarios where terrestrial networks are compromised due to natural disasters, cyber-attacks, or infrastructure failures, satellite links can provide immediate and reliable communication continuity. Governments, emergency services, and critical infrastructure providers are increasingly recognizing the importance of redundant communication pathways, making satellite-enabled 5G backhaul a vital component of robust national and international communication strategies. The demand for such resilient solutions is projected to grow consistently across all regions, positioning satellite technology as an indispensable tool for maintaining connectivity in unforeseen circumstances.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expanding connectivity to unserved and underserved rural/remote areas | +4.0% | Developing economies (Africa, parts of Asia, Latin America), remote areas in developed nations | 2025-2033 |

| Growth of enterprise private 5G networks in remote industrial sites | +3.5% | Global, particularly industries like mining, oil & gas, agriculture | 2026-2033 |

| Increased demand for disaster recovery and network resilience solutions | +3.0% | Regions prone to natural disasters, critical infrastructure providers globally | 2025-2033 |

| Integration with edge computing for localized processing in remote areas | +2.5% | Global | 2027-2033 |

| New mobility applications (maritime, aviation, rail) requiring constant connectivity | +2.0% | Global shipping lanes, flight paths, remote rail corridors | 2025-2033 |

| Development of satellite direct-to-device communication services | +1.8% | Global consumer and enterprise markets | 2028-2033 |

| Partnerships between satellite operators and terrestrial MNOs for hybrid network expansion | +1.5% | Global | 2025-2033 |

Wireless Backhaul and 5G via Satellite Market Challenges Impact Analysis

The Wireless Backhaul and 5G via Satellite market, while promising, faces significant challenges that could impede its seamless development and widespread adoption. One critical challenge is ensuring seamless interoperability between diverse satellite systems, terrestrial 5G networks, and various ground segment equipment from different vendors. As 5G networks are designed to be highly flexible and dynamic, integrating disparate satellite technologies into a unified, end-to-end network architecture requires robust standardization and significant collaborative efforts. Lack of standardized interfaces and protocols can lead to integration complexities, higher deployment costs, and reduced network efficiency, hindering the seamless user experience promised by 5G.

Another major challenge revolves around managing the inherently complex hybrid network architectures that combine satellite and terrestrial components. These networks present intricate issues related to traffic routing, network slicing, spectrum management, and quality of service (QoS) assurance. Optimizing performance across different link characteristics (e.g., varying latency, bandwidth, and availability of satellite vs. terrestrial links) requires advanced network orchestration and management tools. Ensuring consistent and reliable service delivery in such complex environments, especially for latency-sensitive 5G applications, demands sophisticated automation and intelligent control systems, which are still evolving.

Cybersecurity also remains a paramount concern in the Wireless Backhaul and 5G via Satellite market. As satellite networks become integral to critical national infrastructure and directly connect to 5G cores, they become attractive targets for cyber threats. The distributed nature of satellite ground networks, combined with the vast attack surface of 5G infrastructure, increases vulnerability to sophisticated cyber-attacks, including jamming, spoofing, and data breaches. Protecting sensitive data, maintaining network integrity, and ensuring service continuity against evolving cyber threats requires continuous investment in advanced security measures, robust threat intelligence, and a vigilant operational posture across the entire satellite-terrestrial ecosystem.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Ensuring seamless interoperability between satellite and terrestrial 5G components | -2.0% | Global | 2025-2030 |

| Managing complex hybrid network architectures and orchestration | -1.8% | Global | 2025-2033 |

| Cybersecurity threats and vulnerabilities across the satellite-5G ecosystem | -1.5% | Global | 2025-2033 |

| Competition for radio spectrum with other wireless technologies | -1.2% | Global, with regional variations | 2025-2033 |

| High power consumption of ground terminals and network infrastructure | -0.9% | Global, impacting operational costs | 2025-2030 |

| Regulatory hurdles and varying national policies for satellite services | -0.7% | Global, varying by country/region | 2025-2033 |

| Public perception and awareness of satellite connectivity capabilities | -0.5% | Global, affecting market acceptance | 2025-2028 |

Wireless Backhaul and 5G via Satellite Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Wireless Backhaul and 5G via Satellite Market, offering critical insights into its current landscape, future growth trajectories, and key influencing factors. The scope encompasses detailed market sizing, forecast analysis, and identification of significant market trends, drivers, restraints, opportunities, and challenges. It includes a thorough segmentation analysis across various components, satellite orbits, applications, and end-users, alongside regional breakdowns to highlight diverse market dynamics. The report also profiles leading industry players, offering a holistic view for stakeholders seeking to understand and capitalize on the evolving satellite-enabled 5G ecosystem.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 6.5 Billion |

| Market Forecast in 2033 | USD 25.0 Billion |

| Growth Rate | 18.5% CAGR |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Leading Satellite Operator A, Global Telecommunications Provider B, Satellite Ground Segment Innovator C, Integrated Communication Solutions D, Next-Gen Satellite Systems E, Broadband Satellite Service F, Advanced Antenna Technologies G, Network Infrastructure Developer H, Connectivity Solutions Provider I, Space-Based Communications J, Enterprise Satellite Solutions K, Mobility Satellite Provider L, Critical Communications M, Satellite Service Integrator N, Hybrid Network Specialist O, Orbital Connectivity P, Digital Inclusion Technologies Q, Remote Access Solutions R, Global Mobile Connectivity S, Advanced Space Systems T |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Wireless Backhaul and 5G via Satellite market is segmented to provide a granular understanding of its diverse components and applications, enabling a comprehensive analysis of market dynamics across different facets. This segmentation highlights key areas of growth, technological shifts, and strategic opportunities. The market is primarily broken down by component, distinguishing between the hardware necessary for connectivity, the software managing network operations, and the array of services that facilitate deployment and ongoing support. Each segment plays a crucial role in the overall ecosystem, contributing to the delivery of robust and efficient satellite-enabled 5G backhaul solutions. Understanding these distinctions is vital for stakeholders to identify their niche and develop targeted strategies.

Further segmentation by satellite orbit (GEO, MEO, LEO) reflects the evolving technological landscape, as the market increasingly shifts towards lower-orbit constellations for enhanced performance. Application-based segmentation illustrates the diverse use cases, ranging from traditional cellular backhaul to specialized enterprise connectivity and critical government services. This breakdown provides insight into the primary demand drivers and the industries poised for significant adoption. Lastly, end-user segmentation categorizes the market by the types of organizations leveraging these solutions, including telecom operators, internet service providers, and various enterprises, helping to identify key customer bases and their specific requirements.

This multi-dimensional segmentation facilitates a detailed assessment of market trends, competitive positioning, and future growth prospects within each sub-market. It allows for a more precise analysis of where investment is flowing, which technologies are gaining traction, and how different industry verticals are integrating satellite communication into their 5G strategies. Such detailed insight is essential for market players to tailor their offerings, optimize resource allocation, and strategically position themselves for long-term success in this rapidly expanding and technologically complex market.

- By Component:

- Hardware

- Antennas (VSAT, Flat Panel, Phased Array)

- Modems and Routers

- Transceivers and Converters

- Network Equipment (Switches, Gateways, Baseband Units)

- Software

- Network Management Software (NMS)

- Orchestration and Automation Software

- Analytics Software

- Services

- Managed Services

- Professional Services (Consulting, Integration, Deployment)

- Support & Maintenance Services

- Hardware

- By Satellite Orbit:

- Geostationary Earth Orbit (GEO)

- Medium Earth Orbit (MEO)

- Low Earth Orbit (LEO)

- By Application:

- Cellular Backhaul

- Trunking

- Enterprise Connectivity (Oil & Gas, Mining, Construction, Utilities, Maritime, Aviation)

- Government & Defense

- Broadcast & Media

- Internet of Things (IoT) Backhaul

- Disaster Recovery & Emergency Services

- By End-User:

- Telecom Operators (Mobile Network Operators, Fixed Network Operators)

- Internet Service Providers (ISPs)

- Enterprises

- Government

- Military

Regional Highlights

- North America: This region is a leading adopter of advanced communication technologies, with significant investments in 5G infrastructure and satellite constellations. The presence of major satellite operators and ground equipment manufacturers, coupled with robust government and enterprise demand for high-speed, reliable connectivity in remote areas, drives market growth. Early adoption of LEO services and extensive research and development activities position North America as a key innovation hub.

- Europe: Characterized by strong regulatory frameworks and a focus on digital inclusion, Europe is witnessing increasing integration of satellite technology into national 5G strategies. The region benefits from ongoing initiatives to connect underserved rural communities and strengthen critical national infrastructure. Collaborative efforts between terrestrial and satellite operators, alongside investments in advanced ground segment technologies, are propelling market expansion.

- Asia Pacific (APAC): APAC represents a rapidly expanding market due to its vast geographical diversity, large rural populations, and surging demand for broadband connectivity. Countries like India, China, and Southeast Asian nations are investing heavily in 5G deployment, often relying on satellite backhaul to bridge connectivity gaps in remote or challenging terrains. The growing number of mobile subscribers and increasing digitalization across industries are significant drivers.

- Latin America: This region presents substantial opportunities for satellite backhaul and 5G integration, particularly in countries with extensive rural and remote areas where terrestrial infrastructure is underdeveloped. Governments and telecom operators are increasingly looking to satellite solutions to extend 5G coverage, enhance emergency communications, and support digital education initiatives, addressing the significant digital divide.

- Middle East and Africa (MEA): MEA is a burgeoning market for wireless backhaul and 5G via satellite, driven by the imperative to improve connectivity in vast, sparsely populated regions and for critical industrial applications in sectors like oil and gas. Investments in new satellite services and the deployment of 5G networks, alongside government efforts to improve socio-economic development through enhanced connectivity, are fostering rapid growth.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Wireless Backhaul and 5G via Satellite Market.- Leading Satellite Operator A

- Global Telecommunications Provider B

- Satellite Ground Segment Innovator C

- Integrated Communication Solutions D

- Next-Gen Satellite Systems E

- Broadband Satellite Service F

- Advanced Antenna Technologies G

- Network Infrastructure Developer H

- Connectivity Solutions Provider I

- Space-Based Communications J

- Enterprise Satellite Solutions K

- Mobility Satellite Provider L

- Critical Communications M

- Satellite Service Integrator N

- Hybrid Network Specialist O

- Orbital Connectivity P

- Digital Inclusion Technologies Q

- Remote Access Solutions R

- Global Mobile Connectivity S

- Advanced Space Systems T

Frequently Asked Questions

What is the projected growth rate of the Wireless Backhaul and 5G via Satellite Market?

The market is projected to grow at a Compound Annual Growth Rate (CAGR) of 18.5% between 2025 and 2033, driven by expanding 5G networks and the increasing need for ubiquitous connectivity.

How do LEO/MEO satellites impact 5G backhaul compared to GEO satellites?

LEO and MEO satellites offer significantly lower latency and higher bandwidth, making them more suitable for latency-sensitive 5G applications and enhancing the overall performance and viability of satellite backhaul solutions.

What are the primary drivers of growth in this market?

Key drivers include the escalating demand for high-speed 5G connectivity in remote areas, the proliferation of advanced LEO/MEO satellite constellations, and the growing adoption of IoT and critical communication applications.

What role does AI play in Wireless Backhaul and 5G via Satellite networks?

AI is crucial for network optimization, enabling dynamic resource allocation, predictive maintenance, intelligent traffic management, enhanced cybersecurity, and automated orchestration across complex hybrid satellite-terrestrial networks.

What are the main challenges facing the market?

Major challenges include high initial capital expenditure, ensuring seamless interoperability between satellite and terrestrial 5G components, managing complex hybrid network architectures, and addressing cybersecurity threats.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted