Wind Turbine Rotor Blade Market

Wind Turbine Rotor Blade Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700534 | Last Updated : July 25, 2025 |

Format : ![]()

![]()

![]()

![]()

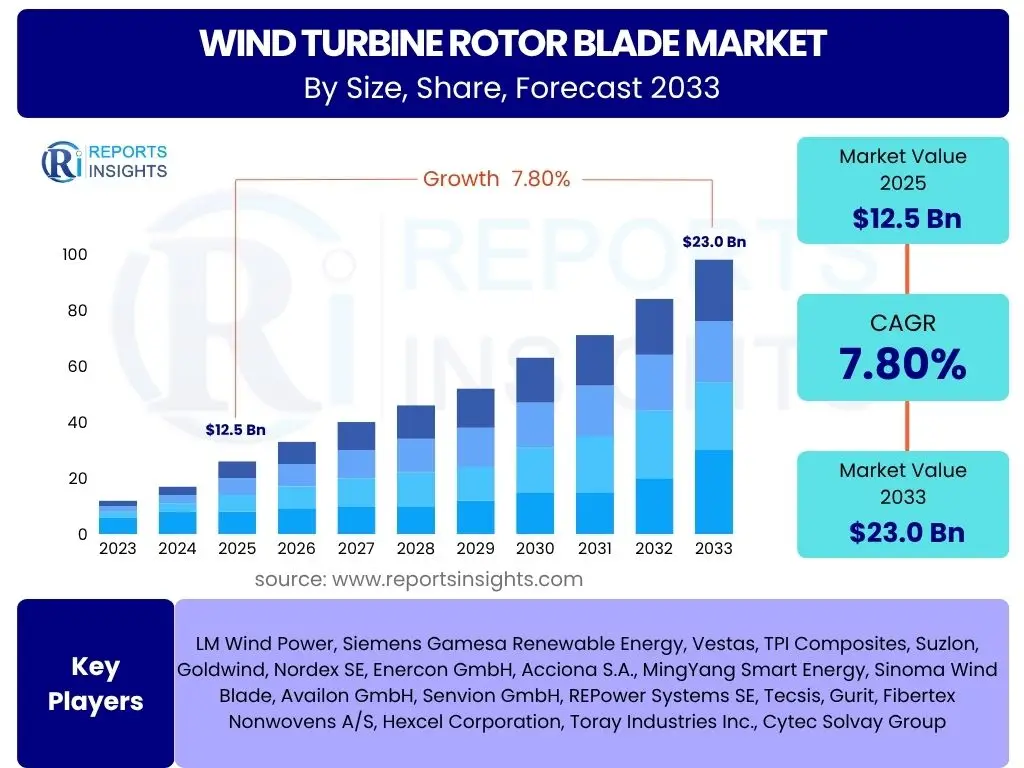

Wind Turbine Rotor Blade Market Size

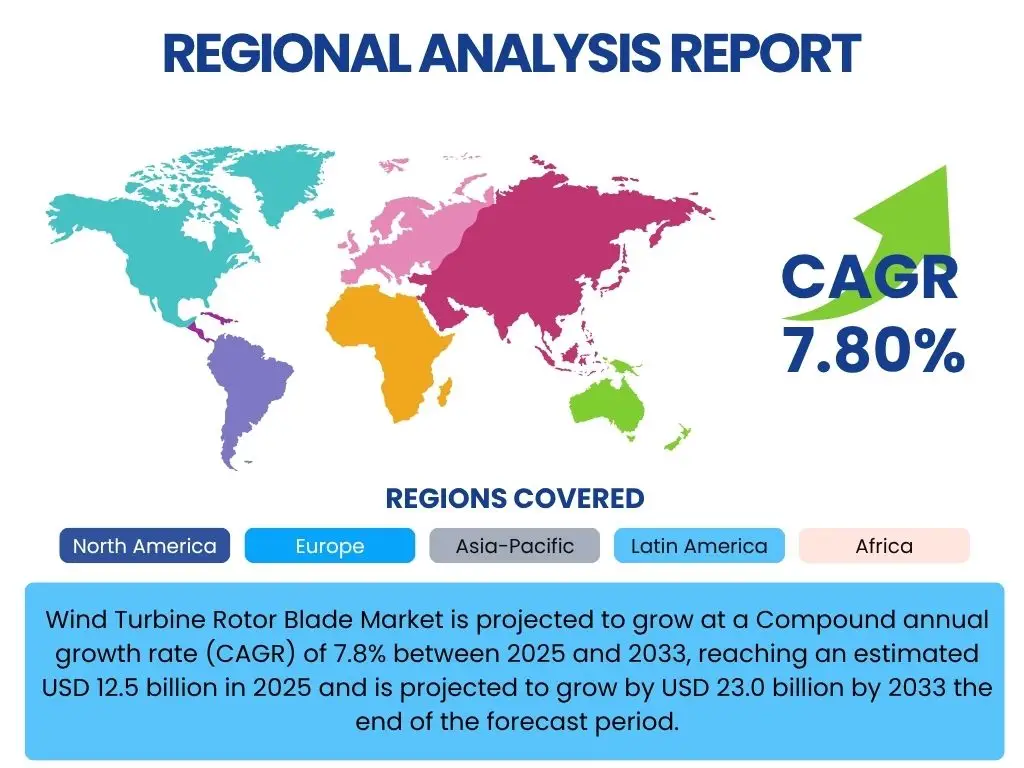

Wind Turbine Rotor Blade Market is projected to grow at a Compound annual growth rate (CAGR) of 7.8% between 2025 and 2033, reaching an estimated USD 12.5 billion in 2025 and is projected to grow by USD 23.0 billion by 2033 the end of the forecast period.

Key Wind Turbine Rotor Blade Market Trends & Insights

The global Wind Turbine Rotor Blade Market is experiencing transformative shifts driven by technological advancements, sustainability imperatives, and evolving energy landscapes. Key trends include the development of larger blades for enhanced energy capture, the adoption of advanced composite materials, and a growing emphasis on blade recyclability. Innovations in manufacturing processes, such as automation and modular designs, are also optimizing production efficiency and reducing costs. Furthermore, the expansion of offshore wind projects and the integration of smart technologies for blade monitoring and maintenance are significantly influencing market dynamics, positioning the sector for substantial growth.

- Development of longer and more aerodynamic blades for higher energy yields.

- Increased adoption of advanced composite materials like carbon fiber for enhanced strength and reduced weight.

- Growing focus on sustainable manufacturing practices and blade recyclability.

- Integration of smart sensors and IoT for predictive maintenance and performance optimization.

- Modular and segmented blade designs to ease transport and installation challenges.

- Proliferation of offshore wind farm development driving demand for specialized large blades.

- Advanced additive manufacturing techniques for rapid prototyping and repair.

AI Impact Analysis on Wind Turbine Rotor Blade

Artificial Intelligence (AI) is rapidly transforming the Wind Turbine Rotor Blade Market across its entire lifecycle, from design and manufacturing to operation and maintenance. In the design phase, AI algorithms optimize blade aerodynamics and structural integrity by simulating countless iterations, leading to more efficient and durable designs. During manufacturing, AI-powered systems enable predictive quality control, anomaly detection, and robotic automation, significantly reducing defects and improving production throughput. For operational performance, AI-driven analytics enhance predictive maintenance, identifying potential blade failures before they occur, thereby maximizing uptime and extending blade lifespan. Furthermore, AI contributes to supply chain optimization, improving logistics and inventory management for blade components. This comprehensive integration of AI is not only boosting operational efficiency and reducing costs but also fostering innovation in blade technology.

- AI-driven optimization of blade design for enhanced aerodynamic efficiency and structural integrity.

- Predictive maintenance analytics for early detection of blade damage, reducing downtime.

- Automated quality control and defect detection during manufacturing using computer vision.

- Supply chain optimization for raw materials and finished blades, improving logistics.

- Smart monitoring systems leveraging AI for real-time blade performance assessment.

- Robotics and AI in automated blade manufacturing processes, enhancing precision and speed.

Key Takeaways Wind Turbine Rotor Blade Market Size & Forecast

- The global Wind Turbine Rotor Blade Market is poised for robust growth, projected to nearly double in value between 2025 and 2033, driven by increasing renewable energy adoption.

- Technological advancements, particularly in material science and aerodynamic design, are central to enhancing blade efficiency and longevity, directly impacting market expansion.

- The significant global push for offshore wind energy development serves as a primary catalyst for demand, especially for larger, specialized rotor blades.

- AI integration is becoming crucial for optimizing the entire blade lifecycle, from design and manufacturing precision to predictive maintenance and operational efficiency.

- Sustainability and recyclability of composite materials are emerging as critical factors shaping future market strategies and material innovation.

- The market's future trajectory will be heavily influenced by overcoming logistical challenges associated with transporting and installing increasingly larger blades, alongside managing end-of-life disposal.

Wind Turbine Rotor Blade Market Drivers Analysis

The Wind Turbine Rotor Blade Market is experiencing significant propulsion from several key drivers that collectively underscore its expansion. The most prominent among these is the escalating global imperative to transition towards renewable energy sources, driven by climate change concerns and energy security agendas. This transition inherently increases demand for wind energy infrastructure, directly translating into higher demand for rotor blades. Furthermore, supportive government policies, including subsidies, tax incentives, and renewable energy mandates, play a pivotal role in creating a conducive environment for wind power development. Continuous technological advancements in blade design, materials, and manufacturing processes are leading to more efficient and cost-effective blades, making wind energy increasingly competitive. The substantial growth in offshore wind projects, characterized by larger turbines and longer blades, also represents a significant demand driver. Lastly, the falling Levelized Cost of Electricity (LCOE) for wind power makes it an attractive investment, further stimulating market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Global Renewable Energy Demand | +2.1% | Global, especially APAC (China, India), Europe, North America | Long-term (2025-2033) |

| Supportive Government Policies & Regulations | +1.8% | Europe (EU Green Deal), North America (IRA), Asia Pacific (national targets) | Medium- to Long-term |

| Technological Advancements in Blade Design & Materials | +1.5% | Global, concentrated in R&D hubs (Europe, North America, China) | Continuous, Medium-term impact |

| Expansion of Offshore Wind Power Capacity | +1.4% | Europe (North Sea), Asia Pacific (China, Vietnam, Japan), North America (East Coast) | Long-term, significant growth |

| Declining Levelized Cost of Electricity (LCOE) for Wind | +1.0% | Global, making wind competitive across diverse markets | Medium-term, increasing adoption |

Wind Turbine Rotor Blade Market Restraints Analysis

Despite the robust growth trajectory, the Wind Turbine Rotor Blade Market faces several significant restraints that could temper its expansion. One primary concern is the substantial upfront capital expenditure required for establishing large-scale blade manufacturing facilities and the subsequent high costs associated with materials and specialized production processes. This economic barrier can limit new entrants and slow down capacity expansion. Supply chain vulnerabilities, particularly for critical raw materials like fiberglass, carbon fiber, and resins, pose another challenge, leading to price volatility and potential delays in production. Furthermore, the increasing size of rotor blades, while beneficial for energy capture, introduces considerable logistical challenges related to transportation, installation, and end-of-life disposal, often requiring specialized infrastructure and innovative solutions. The environmental impact of non-recyclable composite materials at the end of a blade's operational life also presents a growing societal and regulatory pressure, demanding sustainable alternatives and recycling infrastructure.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Capital Investment & Manufacturing Costs | -1.2% | Global, affects new projects and smaller players | Medium-term |

| Supply Chain Vulnerabilities & Raw Material Volatility | -0.9% | Global, particularly regions dependent on specific material imports | Short- to Medium-term |

| Logistical Challenges of Transporting Large Blades | -0.8% | Global, more pronounced in landlocked or infrastructure-limited regions | Long-term, ongoing |

| End-of-Life Disposal & Recycling Challenges for Composite Blades | -0.7% | Primarily Europe, North America, and other regions with aging fleets and stringent environmental regulations | Long-term, increasing urgency |

Wind Turbine Rotor Blade Market Opportunities Analysis

The Wind Turbine Rotor Blade Market is ripe with compelling opportunities that can significantly accelerate its growth and evolution. A major opportunity lies in the burgeoning advancements in blade recycling technologies and the development of truly circular economy solutions for composite materials. This addresses a key restraint and opens new revenue streams while enhancing sustainability credentials. The expansion into emerging markets across Asia Pacific, Latin America, and Africa presents vast untapped potential, as these regions are rapidly industrializing and prioritizing renewable energy integration. Continuous innovation in advanced materials, such as thermoplastic composites or bio-based resins, alongside novel manufacturing techniques like 3D printing or automated modular assembly, promise to revolutionize blade production, improve performance, and reduce costs. The increasing global interest in floating offshore wind technology also represents a distinct and high-value opportunity, requiring specialized blade designs and opening new avenues for market players. Furthermore, the retrofit and repowering of existing wind farms offer a substantial market for new, more efficient blades to upgrade older turbines.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in Blade Recycling Technologies & Circular Economy Solutions | +1.6% | Europe (leading), North America, growing interest globally | Medium- to Long-term |

| Expansion into Emerging Wind Energy Markets | +1.5% | Asia Pacific (Southeast Asia, India), Latin America, Africa | Long-term |

| Innovation in Advanced Materials (e.g., thermoplastics, bio-composites) & Manufacturing Processes | +1.3% | Global, driven by R&D and industry collaboration | Continuous, Medium-term impact |

| Growth of Floating Offshore Wind Technology | +1.0% | Europe (Norway, UK), Asia (Japan, South Korea), North America (West Coast) | Long-term, high growth potential |

| Repowering and Retrofit Market for Existing Wind Farms | +0.8% | Mature wind markets like Europe, North America | Medium-term |

Wind Turbine Rotor Blade Market Challenges Impact Analysis

The Wind Turbine Rotor Blade Market faces a distinct set of challenges that require strategic responses from industry participants. The escalating demand for increasingly larger blades, while enhancing energy capture, presents significant logistical and infrastructural hurdles. Transporting these enormous structures from manufacturing sites to remote installation locations requires specialized heavy-lift equipment, permits, and often, modifications to existing road or port infrastructure, adding complexity and cost. Furthermore, ensuring the long-term durability and structural integrity of these larger blades under diverse environmental stresses (e.g., extreme weather, fatigue) remains a critical engineering challenge. Maintaining stringent quality control throughout the manufacturing process, particularly with complex composite materials and escalating production volumes, is also a persistent challenge. The industry is also grappling with the lack of standardized global regulations and certifications for blade performance and recycling, which can hinder market entry and cross-border trade. Finally, the need for a skilled workforce capable of designing, manufacturing, installing, and maintaining advanced blades poses a training and talent development challenge.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Logistics and Infrastructure for Ultra-Long Blade Transport | -1.0% | Global, especially challenging in developing regions with limited infrastructure | Long-term, ongoing |

| Ensuring Durability and Structural Integrity of Large Blades | -0.9% | Global, impacts R&D and materials science efforts | Continuous, Medium-term |

| Stringent Quality Control and Manufacturing Scalability | -0.8% | Global, particularly for high-volume manufacturers | Medium-term |

| Lack of Standardized Global Regulations & Certifications | -0.6% | Global, affects international trade and project development | Long-term, evolving |

| Shortage of Skilled Workforce in Manufacturing & Installation | -0.5% | Global, especially in regions with rapid wind energy expansion | Medium-term |

Wind Turbine Rotor Blade Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Wind Turbine Rotor Blade Market, offering a detailed understanding of its current landscape, historical performance, and future growth projections. The report delineates market size estimations, growth drivers, restraints, opportunities, and challenges, along with a thorough segmentation analysis. It encompasses a competitive landscape review, profiling key market players, and highlights regional market dynamics. Designed for stakeholders, investors, and industry professionals, this report delivers critical insights to inform strategic decision-making, identify growth avenues, and navigate the evolving market environment for wind turbine rotor blades.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 12.5 Billion |

| Market Forecast in 2033 | USD 23.0 Billion |

| Growth Rate | 7.8% CAGR from 2025 to 2033 |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | LM Wind Power, Siemens Gamesa Renewable Energy, Vestas, TPI Composites, Suzlon, Goldwind, Nordex SE, Enercon GmbH, Acciona S.A., MingYang Smart Energy, Sinoma Wind Blade, Availon GmbH, Senvion GmbH, REPower Systems SE, Tecsis, Gurit, Fibertex Nonwovens A/S, Hexcel Corporation, Toray Industries Inc., Cytec Solvay Group |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis:

The Wind Turbine Rotor Blade Market is comprehensively segmented to provide granular insights into its diverse components and evolving dynamics. This segmentation allows for a precise understanding of market size, growth trends, and opportunities across various dimensions, including the types of materials utilized, the physical dimensions of the blades, their manufacturing methodologies, and their primary application areas. Such a detailed breakdown assists stakeholders in identifying niche markets, tailoring product development, and devising targeted investment strategies within the global wind energy landscape.

-

By Material: This segment categorizes blades based on the primary materials used in their construction, which significantly impacts their weight, strength, durability, and cost.

- Fiberglass: Traditionally dominant due to cost-effectiveness and good performance.

- Carbon Fiber: Gaining traction for its superior strength-to-weight ratio, enabling longer and more efficient blades, particularly for offshore applications.

- Hybrid Composites: Combinations of fiberglass and carbon fiber, offering a balance of performance and cost.

- Others: Includes emerging materials like wood-based composites or thermoplastic composites, focused on sustainability and recyclability.

-

By Blade Length: Segmentation by blade length is critical as it directly correlates with turbine power output and application (onshore vs. offshore).

- Less than 50 meters: Typically used in smaller onshore turbines or older models.

- 50-80 meters: Common for modern onshore and some nearshore offshore turbines, balancing energy capture with logistical constraints.

- More than 80 meters: Predominantly for large-scale offshore wind turbines, designed to capture maximum wind energy in open waters.

-

By Manufacturing Process: This segment examines the various techniques employed in blade production, influencing production efficiency, quality, and material integration.

- Hand Lay-up: A traditional, labor-intensive method suitable for smaller production volumes.

- Vacuum Infusion: A widely adopted technique offering improved material impregnation and reduced air voids, enhancing blade quality.

- Prepreg: Utilizes pre-impregnated materials for precise fiber content and uniformity, common for high-performance blades.

- Others: Encompasses advanced methods such as automated fiber placement, pultrusion, or novel additive manufacturing approaches aimed at automation and speed.

-

By Application: This fundamental segmentation distinguishes between the two primary deployment environments for wind turbines, each having distinct blade requirements.

- Onshore Wind: Blades designed for land-based turbines, often with considerations for transport limitations and noise levels.

- Offshore Wind: Blades engineered for marine environments, emphasizing durability against corrosive elements, larger sizes, and high-wind performance.

Regional Highlights

The global Wind Turbine Rotor Blade Market exhibits distinct regional dynamics, driven by varying renewable energy policies, geographical wind resources, and levels of industrial development. Each region contributes uniquely to the market's overall growth and innovation landscape.

- Asia Pacific (APAC): This region stands as the dominant force in the global wind turbine rotor blade market, primarily led by China, which boasts the world's largest installed wind power capacity and a robust manufacturing ecosystem. India, Australia, and other Southeast Asian nations are also witnessing significant growth due to increasing energy demand, supportive government initiatives for renewable energy, and ample wind resources. The region's focus is on scaling up production and deploying both onshore and increasingly offshore wind farms.

- Europe: A pioneering region in wind energy, Europe continues to be a key market, especially for offshore wind development. Countries like the UK, Germany, Denmark, and the Netherlands are at the forefront of investing in large-scale offshore projects, driving demand for technologically advanced, longer blades. Europe also leads in blade recycling initiatives and sustainable material research, pushing for a circular economy within the wind industry.

- North America: The United States and Canada are significant contributors to the market, propelled by federal and state-level incentives, corporate renewable energy procurement, and the repowering of older wind farms. The U.S. Production Tax Credit (PTC) and Investment Tax Credit (ITC) have historically driven substantial onshore wind growth. There is a growing emphasis on expanding offshore wind capacity, particularly along the East Coast, which will generate demand for specialized offshore blades.

- Latin America: This region offers considerable untapped potential for wind energy, with countries like Brazil, Mexico, Chile, and Argentina investing in wind power to diversify their energy mix and meet growing electricity demand. Favorable wind conditions, particularly in coastal areas and certain interior regions, present opportunities for onshore wind farm development and consequently, the rotor blade market.

- Middle East and Africa (MEA): While nascent compared to other regions, MEA is emerging as a growth market for wind energy, driven by national diversification strategies away from fossil fuels, abundant land for onshore projects, and increasing energy security concerns. Countries like South Africa, Morocco, and Egypt are leading the charge, with planned large-scale wind farms requiring a steady supply of rotor blades.

Top Key Players:

The market research report covers the analysis of key stake holders of the Wind Turbine Rotor Blade Market. Some of the leading players profiled in the report include -

- LM Wind Power (GE Renewable Energy)

- Siemens Gamesa Renewable Energy

- Vestas Wind Systems A/S

- TPI Composites Inc

- Suzlon Energy Limited

- Goldwind Science & Technology Co Ltd

- Nordex SE

- Enercon GmbH

- Acciona S.A.

- MingYang Smart Energy Group Limited

- Sinoma Wind Blade Co Ltd

- Availon GmbH

- Senvion GmbH

- REPower Systems SE

- Tecsis - Technology for Composites and Systems

- Gurit Holding AG

- Fibertex Nonwovens A/S

- Hexcel Corporation

- Toray Industries Inc

- Cytec Solvay Group

Frequently Asked Questions:

What is the primary material used in wind turbine rotor blades?

The primary material traditionally used in wind turbine rotor blades is fiberglass-reinforced polyester or epoxy resins due to their excellent strength-to-weight ratio and cost-effectiveness. However, there is a growing trend towards using carbon fiber composites, especially for larger blades, to achieve greater stiffness, lighter weight, and improved energy capture efficiency.

How long do wind turbine rotor blades typically last?

Wind turbine rotor blades are typically designed for a lifespan of 20 to 25 years. This duration is influenced by factors such as the quality of materials, manufacturing precision, environmental conditions (e.g., wind speed, temperature, humidity, lightning strikes), and the effectiveness of maintenance programs. Advanced monitoring and predictive maintenance can help extend their operational life.

What are the main challenges in recycling wind turbine blades?

The main challenges in recycling wind turbine blades stem from their composite material construction, primarily fiberglass and resin, which are difficult to separate and process. Current methods often involve shredding for use as filler in other products or incineration, which are not ideal circular economy solutions. Developing cost-effective and scalable chemical or mechanical recycling processes that recover valuable materials remains a significant hurdle for the industry.

What innovations are driving the wind turbine rotor blade market?

Key innovations driving the wind turbine rotor blade market include the development of ultra-long and segmented blades for larger turbines, the adoption of advanced materials like thermoplastics and bio-composites for enhanced performance and recyclability, and the integration of smart sensors and AI for real-time monitoring and predictive maintenance. Additionally, advancements in automated manufacturing processes and additive manufacturing for repair are significantly influencing market dynamics.

Which region dominates the global wind turbine rotor blade market?

Asia Pacific (APAC) currently dominates the global wind turbine rotor blade market. This leadership is largely attributable to the expansive wind energy sector in China, which has the world's largest installed wind power capacity and a robust manufacturing base for wind turbine components, including rotor blades. Other countries in the region, such as India, are also experiencing significant growth in wind energy development, further solidifying APAC's market dominance.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted