Wind Turbine Pitch System Market

Wind Turbine Pitch System Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700975 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

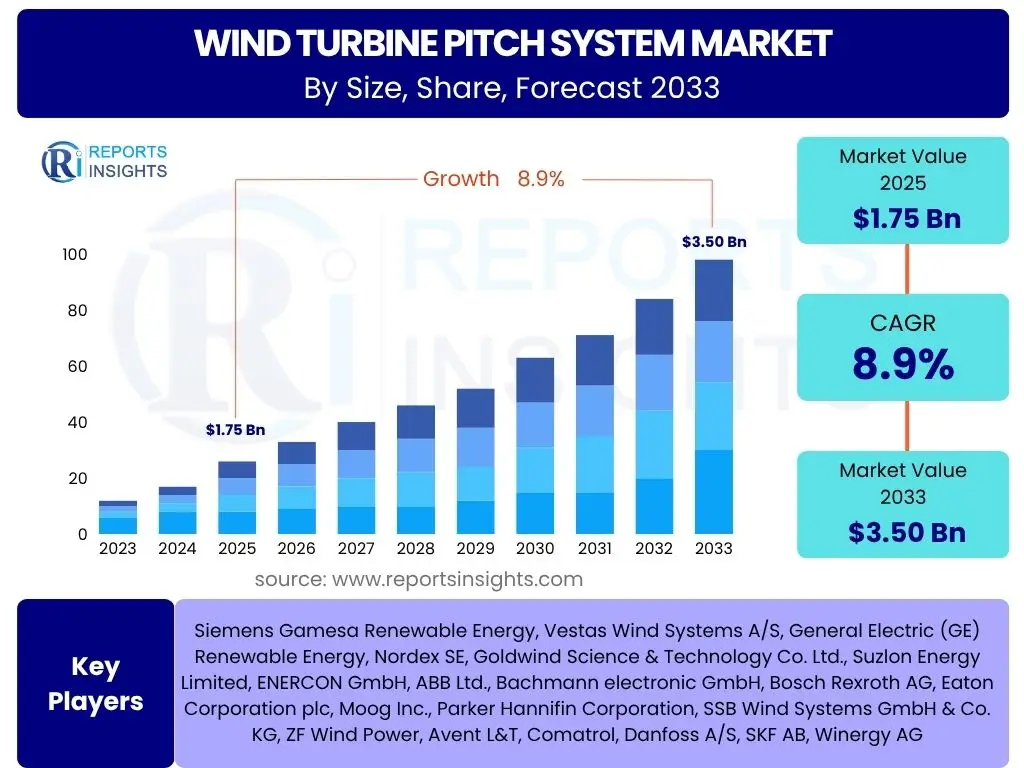

Wind Turbine Pitch System Market Size

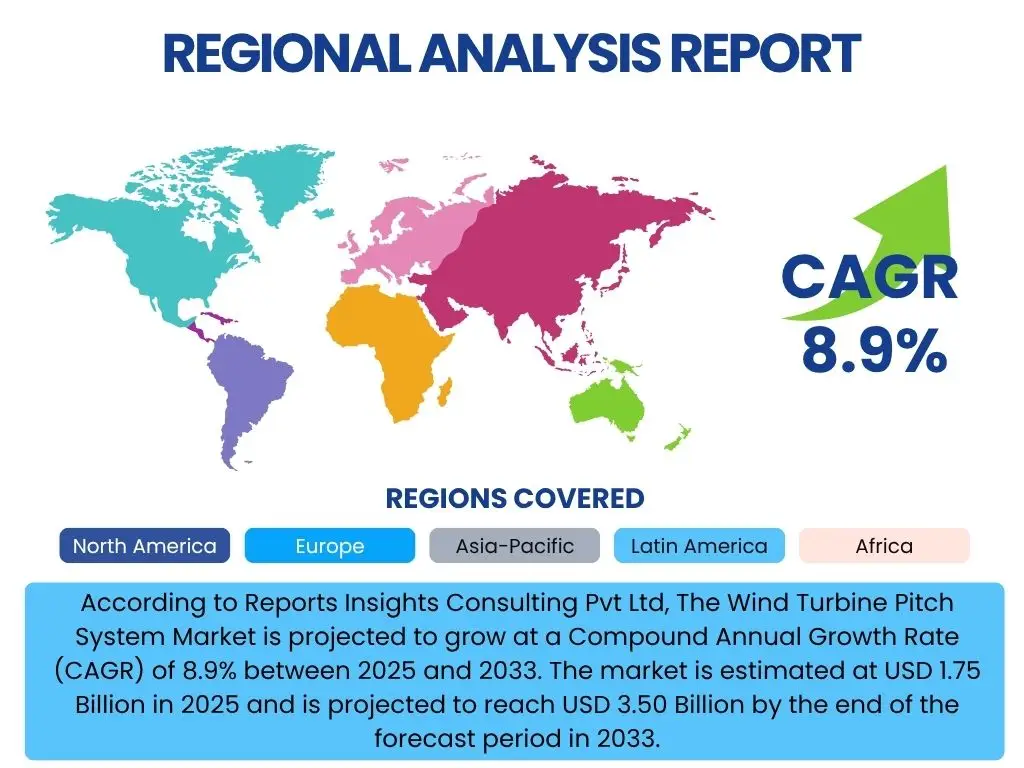

According to Reports Insights Consulting Pvt Ltd, The Wind Turbine Pitch System Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.9% between 2025 and 2033. The market is estimated at USD 1.75 Billion in 2025 and is projected to reach USD 3.50 Billion by the end of the forecast period in 2033.

Key Wind Turbine Pitch System Market Trends & Insights

Common inquiries about the Wind Turbine Pitch System market often revolve around technological advancements, sustainability initiatives, and the integration of smart solutions. Users are keen to understand how innovations in pitch control mechanisms, sensor technologies, and material science are contributing to enhanced turbine performance and reliability. There is significant interest in the shift towards more efficient and environmentally friendly systems, alongside the adoption of predictive maintenance strategies that leverage real-time data for optimized operations. The overall trend indicates a strong drive towards maximizing energy capture and minimizing operational expenditures across the wind energy sector.

Furthermore, discussions frequently highlight the increasing sophistication of pitch system design to accommodate larger turbine capacities and harsher operating environments, particularly in offshore applications. The industry is witnessing a focus on reducing the weight and complexity of these systems while improving their responsiveness and accuracy. Stakeholders are exploring advanced control algorithms and modular designs to facilitate easier installation, maintenance, and upgrades. These developments are critical for the continued expansion and economic viability of wind power globally, addressing the growing demand for renewable energy sources and grid stability.

- Integration of advanced sensor technologies for precise blade angle adjustments.

- Development of lightweight and durable materials for pitch components.

- Shift towards electric pitch systems due to higher efficiency and reduced maintenance.

- Emphasis on predictive maintenance through data analytics and IoT integration.

- Increasing demand for pitch systems capable of operating in extreme offshore conditions.

- Customization of pitch control strategies for varying wind profiles and turbine designs.

AI Impact Analysis on Wind Turbine Pitch System

User questions concerning the impact of Artificial Intelligence (AI) on Wind Turbine Pitch Systems frequently center on performance optimization, predictive capabilities, and autonomous operation. Stakeholders are interested in how AI algorithms can enhance the precision of blade pitch adjustments, leading to improved energy capture and reduced load on turbine components. There is a strong focus on AI's role in developing highly accurate predictive maintenance models, which can anticipate component failures, optimize maintenance schedules, and significantly minimize turbine downtime. This proactive approach is seen as crucial for improving the overall reliability and economic efficiency of wind farms.

Additionally, inquiries often touch upon the potential for AI-driven systems to enable more adaptive and self-optimizing pitch control strategies, allowing turbines to respond dynamically to changing wind conditions and grid demands. Users are also keen to understand the implications for cybersecurity and data privacy as more critical control functions become AI-dependent. The overarching expectation is that AI will revolutionize the operational efficiency and longevity of wind turbine pitch systems, moving towards a future where turbines are smarter, more resilient, and require less manual intervention. This evolution is vital for making wind energy even more competitive and reliable within the global energy mix.

- Optimized blade angle control for maximum aerodynamic efficiency and power output.

- Enhanced predictive maintenance capabilities for early fault detection and reduced downtime.

- Real-time load reduction on turbine components, extending asset lifespan.

- Adaptive pitch strategies based on changing wind patterns and weather conditions.

- Automated anomaly detection and self-correction in pitch system operations.

- Improved energy capture and Annual Energy Production (AEP) through intelligent control.

Key Takeaways Wind Turbine Pitch System Market Size & Forecast

Common user questions regarding the key takeaways from the Wind Turbine Pitch System market size and forecast often highlight the market's robust growth trajectory and its critical role in the broader renewable energy landscape. Users are keen to understand the primary drivers behind the projected expansion, such as the global push for decarbonization and increasing investments in wind energy infrastructure. A key insight is that the market's growth is intrinsically linked to advancements in turbine technology, particularly the development of larger and more efficient wind turbines that require sophisticated pitch control systems for optimal performance. The forecast indicates sustained demand, driven by both new installations and the retrofitting of existing assets to enhance their operational life and efficiency.

Another significant takeaway is the emphasis on technological innovation and digitalization as central themes influencing market dynamics. The integration of advanced sensors, AI-driven analytics, and IoT solutions within pitch systems is not merely a trend but a fundamental shift towards smarter, more resilient, and self-optimizing wind turbines. This technological evolution is poised to enhance the economic viability of wind power, making it a more attractive investment. Furthermore, the market's regional dynamics reveal a strong growth potential in emerging economies, alongside continued expansion in established wind power markets, underscoring the global nature of this vital component in the renewable energy transition.

- The market exhibits robust growth, primarily driven by increasing global wind energy installations.

- Technological advancements in pitch control are crucial for enhancing turbine efficiency and reliability.

- Significant opportunities exist in both onshore and offshore wind segments, especially with larger turbines.

- Predictive maintenance and AI integration are pivotal for optimizing pitch system performance and reducing operational costs.

- Europe and Asia Pacific are expected to remain key growth regions due to supportive policies and large-scale projects.

Wind Turbine Pitch System Market Drivers Analysis

The global shift towards renewable energy sources is a primary driver for the Wind Turbine Pitch System market. Governments worldwide are implementing ambitious targets for decarbonization and providing incentives for wind power development, leading to a substantial increase in wind turbine installations. As the installed capacity of wind energy grows, so does the demand for sophisticated pitch systems, which are essential for optimizing energy capture and ensuring the safe operation of turbines. This escalating demand is further fueled by the need for more efficient and reliable wind farms to meet rising electricity consumption and achieve energy independence.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Global Renewable Energy Deployment | +2.5% | Global, particularly Europe, APAC, North America | Long-term (2025-2033) |

| Increasing Average Turbine Capacity and Size | +2.0% | Global, especially Offshore regions (Europe, US, Asia) | Mid to Long-term (2025-2033) |

| Technological Advancements in Pitch Control & Sensors | +1.8% | Globally, driven by R&D hubs (Germany, Denmark, US) | Mid-term (2025-2030) |

| Government Policies and Financial Incentives for Wind Power | +1.5% | China, India, US, EU Member States | Mid to Long-term (2025-2033) |

Wind Turbine Pitch System Market Restraints Analysis

Despite robust growth prospects, the Wind Turbine Pitch System market faces several restraints that could impede its expansion. One significant challenge is the high initial capital expenditure required for installing advanced pitch systems, which can be a barrier for smaller project developers or regions with limited funding. The complexity of these systems also necessitates specialized labor for installation and maintenance, contributing to overall operational costs. Furthermore, the long lead times for manufacturing and delivering critical components, coupled with potential supply chain disruptions, can affect project timelines and increase development risks, particularly in a globally interconnected industry.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Capital Costs | -1.2% | Emerging Markets, Developing Countries | Short to Mid-term (2025-2028) |

| Supply Chain Disruptions and Component Shortages | -1.0% | Global, particularly critical for specialized components | Short-term (2025-2027) |

| Stringent Regulatory and Permitting Processes | -0.8% | Europe, North America (specific countries) | Long-term (Ongoing) |

Wind Turbine Pitch System Market Opportunities Analysis

The burgeoning offshore wind energy sector presents a significant opportunity for the Wind Turbine Pitch System market. As offshore wind farms become larger and are deployed in more challenging environments, the demand for highly reliable, durable, and sophisticated pitch systems designed for marine conditions is surging. These systems must withstand harsh weather, corrosive saltwater, and intense operational loads, driving innovation in material science and system design. This expansion offshore provides a lucrative avenue for manufacturers to develop specialized solutions with enhanced resilience and extended service life, catering to the unique requirements of this rapidly growing segment. The increasing focus on floating offshore wind technologies further amplifies this opportunity.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Offshore Wind Energy Projects | +2.2% | Europe, North America (US), Asia Pacific (China, Japan) | Long-term (2025-2033) |

| Retrofitting and Modernization of Existing Turbines | +1.5% | Mature Wind Markets (Europe, North America) | Mid to Long-term (2026-2033) |

| Integration of IoT, AI, and Big Data for Smart Pitch Control | +1.0% | Global, driven by technology innovators | Mid-term (2025-2030) |

Wind Turbine Pitch System Market Challenges Impact Analysis

The Wind Turbine Pitch System market faces challenges related to intense market competition and the need for continuous technological innovation. The highly competitive landscape puts pressure on manufacturers to offer cost-effective yet high-performance solutions, often leading to squeezed profit margins. Moreover, the dynamic nature of wind energy technology demands ongoing research and development to keep pace with evolving turbine designs and operational requirements. This continuous need for innovation, combined with the complexities of integrating new technologies into existing infrastructure, represents a significant hurdle for market players, particularly those with limited R&D budgets or slower adoption cycles.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition and Price Pressures | -0.9% | Global, particularly in established markets | Short to Mid-term (2025-2028) |

| Durability and Reliability in Harsh Operating Environments | -0.7% | Offshore and Remote Onshore locations | Long-term (Ongoing) |

| Integration Complexities with Advanced Turbine Systems | -0.6% | Global, as turbines become more sophisticated | Mid-term (2025-2030) |

Wind Turbine Pitch System Market - Updated Report Scope

This report provides a comprehensive analysis of the Wind Turbine Pitch System market, offering detailed insights into market size, growth trends, drivers, restraints, opportunities, and challenges. It covers a forecast period from 2025 to 2033, with 2024 as the base year, and includes historical data from 2019 to 2023. The scope encompasses an in-depth segmentation analysis by type, component, application, and turbine capacity, alongside a thorough regional assessment across North America, Europe, Asia Pacific, Latin America, and the Middle East & Africa. Additionally, the report profiles leading market players, highlighting their strategies and contributions to the market landscape, aiming to provide a strategic roadmap for stakeholders in the wind energy sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.75 Billion |

| Market Forecast in 2033 | USD 3.50 Billion |

| Growth Rate | 8.9% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Siemens Gamesa Renewable Energy, Vestas Wind Systems A/S, General Electric (GE) Renewable Energy, Nordex SE, Goldwind Science & Technology Co. Ltd., Suzlon Energy Limited, ENERCON GmbH, ABB Ltd., Bachmann electronic GmbH, Bosch Rexroth AG, Eaton Corporation plc, Moog Inc., Parker Hannifin Corporation, SSB Wind Systems GmbH & Co. KG, ZF Wind Power, Avent L&T, Comatrol, Danfoss A/S, SKF AB, Winergy AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Wind Turbine Pitch System market is comprehensively segmented to provide a granular understanding of its diverse components and applications. This segmentation is crucial for identifying specific growth drivers, technological preferences, and market dynamics within each category. The primary segmentation includes analysis by type (hydraulic, electric, hybrid), by component (various mechanical and electronic parts), by application (onshore vs. offshore wind turbines), and by turbine capacity, reflecting the varying demands based on turbine size and power output. Each segment provides unique insights into market trends and investment opportunities.

Understanding these distinct segments is vital for stakeholders to tailor their product development, marketing strategies, and investment decisions effectively. For instance, the growing demand for offshore wind power is significantly influencing the development of robust and high-capacity pitch systems, while the increasing focus on efficiency and reliability drives innovation across all component categories. This detailed segmentation allows for a precise evaluation of market potential and competitive landscapes within specific niches of the wind energy sector, facilitating targeted business strategies and optimized resource allocation.

- By Type: Hydraulic Pitch System, Electric Pitch System, Hybrid Pitch System

- By Component: Pitch Bearings, Pitch Motors, Pitch Gearboxes, Pitch Cylinders, Pitch Control Units, Sensors, Accumulators, Brakes, Other Components

- By Application: Onshore Wind Turbines, Offshore Wind Turbines

- By Turbine Capacity: Less than 1 MW, 1-3 MW, 3-5 MW, Above 5 MW

Regional Highlights

North America: The North American market for Wind Turbine Pitch Systems is driven by significant investments in renewable energy infrastructure, particularly in the United States and Canada. Both countries have robust wind power capacities and are actively pursuing policies to expand their renewable energy portfolios. The US, with its Production Tax Credit (PTC) and growing interest in offshore wind projects, is a key market, demanding advanced pitch systems for larger turbines. Canada's commitment to clean energy and vast land availability also contribute to market growth, with an emphasis on enhancing the efficiency and longevity of existing and new wind farms. Regional innovation in smart grid integration and energy storage further supports the adoption of sophisticated pitch technologies.

Europe: Europe remains a powerhouse in the Wind Turbine Pitch System market, largely due to its pioneering role in offshore wind development and ambitious decarbonization targets set by the European Union. Countries like Germany, the UK, Denmark, and the Netherlands are leading the charge in deploying multi-megawatt offshore turbines, which require highly robust and precise pitch systems. Strong government support, well-established supply chains, and continuous technological advancements in turbine design and control mechanisms are fueling market expansion. The focus on repowering older onshore wind farms also creates demand for modern pitch solutions that can enhance the performance and extend the operational life of existing assets.

Asia Pacific (APAC): The Asia Pacific region is projected to be the fastest-growing market for Wind Turbine Pitch Systems, primarily led by China and India. China holds the largest installed wind power capacity globally and continues to invest heavily in both onshore and offshore wind projects. India is also rapidly expanding its renewable energy sector, with significant government initiatives promoting wind energy. Other emerging markets in the region, such as Australia, Japan, and South Korea, are increasingly focusing on wind power to diversify their energy mix and reduce carbon emissions. The region's rapid industrialization, growing energy demand, and supportive policies are key factors driving the adoption of advanced pitch systems, with a strong emphasis on cost-effectiveness and reliability.

Latin America: The Latin American market for Wind Turbine Pitch Systems is gaining traction, driven by countries like Brazil, Mexico, Chile, and Argentina. These nations possess significant wind energy potential and are actively investing in large-scale wind farm projects to meet their burgeoning energy demands and diversify away from fossil fuels. Government auctions and renewable energy targets are stimulating growth, although challenges related to infrastructure development and financing can impact the pace of adoption. As the region continues to prioritize sustainable energy, the demand for reliable and efficient pitch systems will steadily increase, particularly for onshore applications.

Middle East & Africa (MEA): The Middle East and Africa region represents an emerging market for Wind Turbine Pitch Systems, albeit from a lower base. Countries like South Africa, Morocco, and the UAE are increasingly recognizing the potential of wind energy as part of their national energy strategies. While oil and gas dominate the energy landscape, growing concerns over climate change and the need for energy diversification are driving investments in renewable projects. Development is slower compared to other regions, but significant government-backed initiatives and international partnerships are expected to accelerate the adoption of wind power, thereby creating a nascent yet growing demand for pitch systems in the long term.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Wind Turbine Pitch System Market.- Siemens Gamesa Renewable Energy

- Vestas Wind Systems A/S

- General Electric (GE) Renewable Energy

- Nordex SE

- Goldwind Science & Technology Co. Ltd.

- Suzlon Energy Limited

- ENERCON GmbH

- ABB Ltd.

- Bachmann electronic GmbH

- Bosch Rexroth AG

- Eaton Corporation plc

- Moog Inc.

- Parker Hannifin Corporation

- SSB Wind Systems GmbH & Co. KG

- ZF Wind Power

- Avent L&T

- Comatrol

- Danfoss A/S

- SKF AB

- Winergy AG

Frequently Asked Questions

Analyze common user questions about the Wind Turbine Pitch System market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a wind turbine pitch system?

A wind turbine pitch system is a critical mechanism that adjusts the angle of a wind turbine's rotor blades relative to the wind direction. This adjustment, known as pitching, is essential for controlling the turbine's rotational speed, optimizing power output under varying wind conditions, and ensuring safe operation, especially during high winds or shutdown procedures.

Why are pitch systems crucial for wind turbine efficiency?

Pitch systems are crucial because they enable a wind turbine to capture maximum energy efficiently across a wide range of wind speeds. By precisely adjusting blade angles, they optimize the aerodynamic forces, prevent damage from excessive loads, and maintain a stable power output, thereby maximizing Annual Energy Production (AEP) and extending the turbine's operational life.

What are the main types of wind turbine pitch systems?

The primary types of wind turbine pitch systems are hydraulic, electric, and hybrid. Hydraulic systems use fluid pressure for blade adjustment, offering high torque. Electric systems use motors and gearboxes, providing precise control and lower maintenance. Hybrid systems combine elements of both, aiming to leverage their respective advantages for optimized performance.

What challenges do wind turbine pitch systems face?

Pitch systems face challenges such as harsh operating environments (extreme temperatures, moisture, vibrations), demanding high durability and reliability. They also contend with the complexity of integrating advanced control algorithms, the need for continuous technological innovation, and the pressure to reduce manufacturing and maintenance costs while ensuring peak performance.

How does AI impact wind turbine pitch system performance?

AI significantly enhances pitch system performance by enabling predictive maintenance, optimizing blade angles in real-time, and improving fault detection. AI algorithms analyze vast datasets to anticipate component failures, fine-tune blade positions for maximum energy capture, and reduce operational downtime, leading to increased efficiency and lower overall costs for wind farms.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted