Wet Pet Food Market

Wet Pet Food Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709045 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

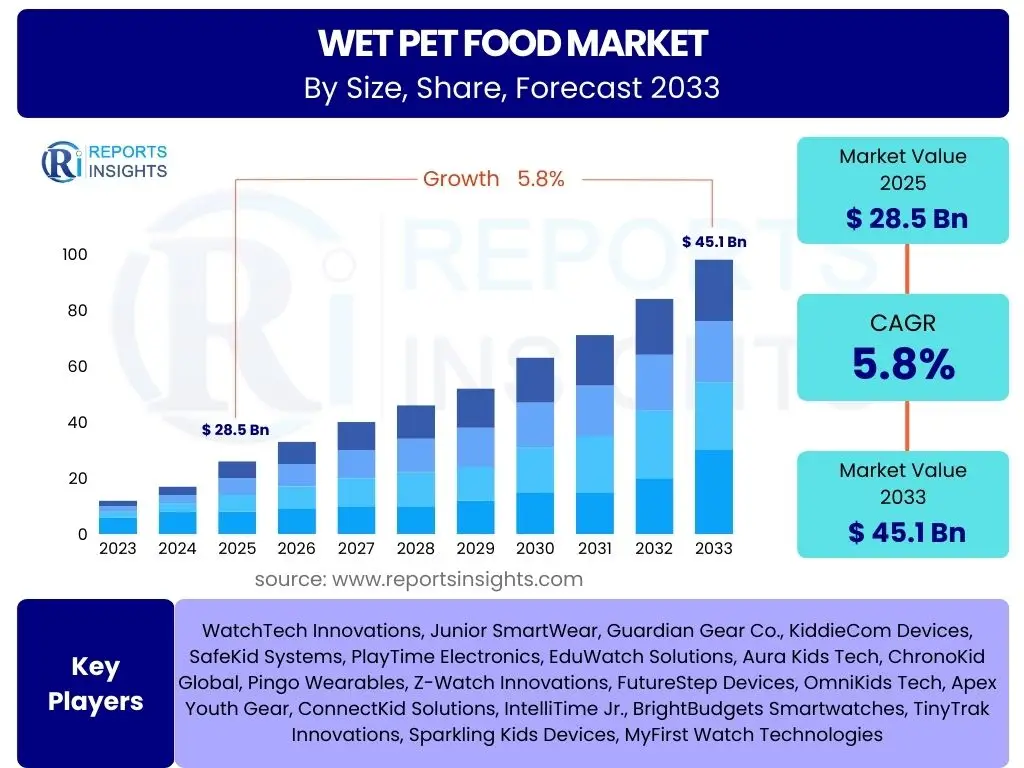

Wet Pet Food Market Size

According to Reports Insights Consulting Pvt Ltd, The Wet Pet Food Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 28.5 billion in 2025 and is projected to reach USD 45.1 billion by the end of the forecast period in 2033.

Key Wet Pet Food Market Trends & Insights

User queries regarding the Wet Pet Food Market frequently center on evolving consumer preferences, product innovation, and the influence of humanization of pets. Consumers are increasingly seeking premium, natural, and specialized diets for their pets, mirroring their own dietary choices. This trend drives manufacturers to invest in research and development, focusing on novel ingredients, enhanced nutritional profiles, and sustainable sourcing. The market is also experiencing a shift towards convenient packaging formats and subscription-based delivery models, reflecting modern lifestyle demands.

Another significant trend is the rising awareness among pet owners about specific dietary needs and health conditions, leading to increased demand for therapeutic and condition-specific wet pet food. This includes formulations for allergies, digestive sensitivities, weight management, and age-specific requirements. Furthermore, the expansion of e-commerce platforms has democratized access to a wider variety of specialized wet pet food products, allowing niche brands to reach a broader audience and fostering competitive innovation within the sector. Manufacturers are also exploring functional ingredients such as probiotics and prebiotics to support pet gut health.

- Humanization of pets driving demand for premium and specialized wet food.

- Increased focus on natural, organic, and limited ingredient formulations.

- Growth in e-commerce and direct-to-consumer (D2C) sales channels.

- Demand for functional wet pet food addressing specific health concerns (e.g., digestive, skin, joint).

- Development of sustainable and ethically sourced ingredient options.

- Innovative packaging solutions for convenience and portion control.

AI Impact Analysis on Wet Pet Food

User questions related to the impact of AI on the Wet Pet Food industry primarily revolve around enhanced product development, optimized supply chains, and personalized pet nutrition. Pet food manufacturers are exploring how artificial intelligence can analyze vast datasets, including pet health records, consumer purchasing patterns, and ingredient efficacy, to identify emerging trends and formulate highly targeted products. This data-driven approach allows for the creation of innovative recipes that cater to specific breed needs, age groups, and health conditions with greater precision than traditional methods.

Furthermore, AI is poised to revolutionize operational efficiencies within the sector. Applications include predictive analytics for demand forecasting, optimizing inventory management, and streamlining manufacturing processes to reduce waste and improve production yields. AI-powered tools can also monitor product quality in real-time and automate quality control checks, ensuring consistency and safety. In terms of consumer engagement, AI can facilitate personalized recommendations through online platforms and even power virtual assistants to help pet owners choose the best products for their companions, thereby enhancing customer satisfaction and loyalty.

- AI-driven personalized pet nutrition recommendations based on health data.

- Optimized supply chain and inventory management through predictive analytics.

- Enhanced product development and formulation using data analysis for ingredient efficacy.

- Automated quality control and real-time monitoring in manufacturing.

- Improved customer engagement and loyalty through AI-powered recommendation engines.

- Forecasting market trends and consumer preferences with higher accuracy.

Key Takeaways Wet Pet Food Market Size & Forecast

The primary insights from the Wet Pet Food Market size and forecast indicate a robust and consistent growth trajectory driven by the increasing humanization of pets and the associated willingness of owners to invest in high-quality nutrition. The substantial projected growth in market value underscores a fundamental shift in consumer behavior, where pets are increasingly viewed as family members deserving of premium care. This translates into a sustained demand for products that offer superior nutritional benefits, convenience, and specialized formulations.

Moreover, the forecast highlights the market's resilience and adaptability to evolving consumer demands, with innovation in product types and distribution channels playing a crucial role. The estimated expansion of the market presents significant opportunities for both established players and new entrants to capitalize on a growing consumer base that is increasingly informed and discerning about pet food choices. Strategic focus on research and development, alongside effective marketing and distribution, will be paramount for securing market share in this expanding landscape.

- Consistent market expansion driven by premiumization and pet humanization.

- Significant growth potential, indicating sustained investment opportunities.

- Increasing consumer demand for specialized and therapeutic wet pet food.

- E-commerce and direct-to-consumer channels are critical for market reach.

- Innovation in ingredients, formulations, and packaging remains a key competitive factor.

Wet Pet Food Market Drivers Analysis

The Wet Pet Food Market is significantly propelled by the global trend of pet humanization, where pets are increasingly considered integral family members. This cultural shift leads pet owners to prioritize their pets' health and well-being, driving demand for premium, high-quality, and nutritionally balanced wet food products. Owners are more willing to invest in products that mimic human food standards, including natural ingredients, specialized diets, and superior palatability, fostering a consistent upward trajectory in market value and product innovation.

Another major driver is the inherent palatability and hydration benefits offered by wet pet food. Many pet owners opt for wet food due to its higher moisture content, which contributes to better hydration, particularly for cats who often have lower thirst drives. The texture and aroma of wet food are also highly appealing to pets, making it an excellent choice for finicky eaters or older pets with dental issues. These inherent product advantages ensure a steady consumer base and encourage repeat purchases, further solidifying market growth across various regions, especially in developed economies where pet ownership is high and disposable income allows for premium choices.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Pet Humanization & Premiumization | +1.5% | North America, Europe, Asia Pacific | Long-term (2025-2033) |

| Enhanced Palatability & Hydration Benefits | +1.2% | Global | Long-term (2025-2033) |

| Growing Awareness of Pet Health & Nutrition | +1.0% | North America, Europe, Asia Pacific | Mid to Long-term (2025-2030) |

| Expansion of E-commerce & Online Sales Channels | +0.8% | Global, especially emerging economies | Mid-term (2025-2028) |

| Product Innovation & Variety (e.g., grain-free, limited ingredient) | +0.7% | North America, Europe | Long-term (2025-2033) |

Wet Pet Food Market Restraints Analysis

Despite robust growth, the Wet Pet Food Market faces several significant restraints, notably the higher cost associated with wet pet food compared to dry kibble. The manufacturing processes, packaging, and shipping of wet food often incur greater expenses, which are then passed on to consumers. For price-sensitive pet owners, particularly those with multiple pets or larger breeds requiring substantial food quantities, the cost differential can be a major deterrent, prompting them to opt for more economical dry food alternatives or a mixed feeding approach.

Another challenge is the relatively shorter shelf life of wet pet food once opened and its storage requirements. Unlike dry food, opened wet pet food needs to be refrigerated and consumed within a few days to prevent spoilage, which can be inconvenient for some pet owners. The weight and bulkiness of wet pet food cans or pouches also present logistical challenges in terms of storage space at home and transportation from retail outlets. These factors, combined with concerns about environmental impact from single-use packaging, can temper the market's growth potential by limiting adoption among certain consumer segments.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Cost Compared to Dry Pet Food | -1.0% | Global | Long-term (2025-2033) |

| Shorter Shelf Life & Storage Requirements (post-opening) | -0.7% | Global | Long-term (2025-2033) |

| Perceived Environmental Impact of Packaging | -0.5% | Europe, North America | Mid to Long-term (2025-2030) |

| Competition from Raw & Fresh Pet Food Trends | -0.4% | North America, Europe | Mid-term (2025-2028) |

| Limited Retail Space for Bulky Wet Food Products | -0.3% | Urban areas, developing markets | Long-term (2025-2033) |

Wet Pet Food Market Opportunities Analysis

Significant opportunities in the Wet Pet Food Market stem from the increasing consumer demand for functional and therapeutic pet food. As pet owners become more educated about their pets' health needs, there is a growing market for wet food formulations designed to address specific conditions such as digestive issues, allergies, joint health, and urinary tract support. Manufacturers who can innovate with scientifically backed ingredients and offer a range of specialized products stand to capture a substantial share of this growing segment. This includes developing solutions for pets with chronic illnesses or age-related dietary requirements, which often require soft, palatable food formats.

Another major opportunity lies in expanding into emerging markets, particularly in Asia Pacific and Latin America, where pet ownership is on the rise, and disposable incomes are increasing. As these regions develop, pet owners are gradually adopting Western pet care practices, including feeding premium wet pet food. Companies that can effectively localize their products, adapt to regional tastes, and establish strong distribution networks in these nascent markets can achieve considerable growth. Furthermore, the development of sustainable and eco-friendly packaging solutions offers a competitive advantage, appealing to environmentally conscious consumers and potentially mitigating some of the restraints related to packaging waste.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Functional & Therapeutic Wet Foods | +1.3% | Global | Long-term (2025-2033) |

| Penetration of Emerging Markets (APAC, LATAM) | +1.1% | Asia Pacific, Latin America | Long-term (2025-2033) |

| Development of Sustainable & Biodegradable Packaging | +0.9% | Europe, North America | Mid to Long-term (2025-2030) |

| Growth in Online Subscription & D2C Models | +0.8% | Global | Mid-term (2025-2028) |

| Targeting Niche Segments (e.g., breed-specific, exotic pets) | +0.6% | North America, Europe | Mid to Long-term (2025-2030) |

Wet Pet Food Market Challenges Impact Analysis

A significant challenge in the Wet Pet Food Market is the intense competition from alternative pet food formats, particularly dry kibble, raw food, and fresh pet food. Dry kibble often offers a more economical price point and longer shelf life, making it a preferred choice for many consumers. The rising popularity of raw and fresh pet food, perceived as more natural and less processed, also draws a segment of the premium market away from traditional wet food. This diverse competitive landscape necessitates continuous innovation and differentiation for wet pet food manufacturers to maintain and grow market share.

Another critical challenge involves regulatory complexities and ingredient sourcing issues. Ensuring compliance with stringent food safety standards, animal welfare guidelines, and ingredient labeling requirements across different regions can be complex and costly. Volatility in raw material prices, particularly for meat and fish proteins, can impact production costs and profit margins. Additionally, consumer skepticism regarding ingredient transparency and sourcing ethics requires manufacturers to be highly accountable and communicative about their supply chains. Addressing these challenges effectively requires robust quality control, strategic supplier relationships, and clear communication with consumers.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Competition from Alternative Pet Food Formats | -0.9% | Global | Long-term (2025-2033) |

| Volatile Raw Material Prices & Supply Chain Disruptions | -0.8% | Global | Mid-term (2025-2028) |

| Regulatory Hurdles & Compliance Costs | -0.6% | Europe, North America | Long-term (2025-2033) |

| Consumer Skepticism Regarding Ingredient Transparency | -0.5% | Developed markets | Mid to Long-term (2025-2030) |

| Logistical Challenges for Storage & Distribution (weight/bulk) | -0.4% | Global, especially dense urban areas | Long-term (2025-2033) |

Wet Pet Food Market - Updated Report Scope

This comprehensive market report provides an in-depth analysis of the global Wet Pet Food Market, covering historical data, current market dynamics, and future projections. It delves into critical aspects such as market size, growth drivers, restraints, opportunities, and challenges affecting the industry. The report also offers detailed segmentation analysis by product type, animal type, ingredient type, packaging type, and distribution channel, providing a granular view of market performance. Regional insights highlight key growth pockets and competitive landscapes across major geographical areas. This scope ensures stakeholders receive actionable intelligence to make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 28.5 billion |

| Market Forecast in 2033 | USD 45.1 billion |

| Growth Rate | 5.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Mars Petcare Inc., Nestle Purina PetCare, Hill's Pet Nutrition (Colgate-Palmolive), Smucker Pet Foods, Blue Buffalo Co. Ltd. (General Mills), Diamond Pet Foods, Inc., Merrick Pet Care, Inc. (Nestle Purina), Wellness Pet Company, The J.M. Smucker Company, Affinity Petcare S.A., Sunshine Mills, Inc., Almo Nature S.p.A., Freshpet, Inc., White Wave Foods (Danone), General Mills, Archer Daniels Midland Company (ADM), PLB International, Thai Union Group PCL, Instinct Pet Food. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Wet Pet Food Market is extensively segmented to provide a detailed understanding of its various components and dynamics. This granular analysis allows for a precise evaluation of consumer preferences, product innovation areas, and distribution channel effectiveness across different categories. Each segment reflects specific aspects of the pet food industry, from the type of animal being fed to the packaging format chosen by manufacturers and consumers, directly impacting market trends and growth opportunities. Understanding these segments is crucial for identifying niche markets and developing targeted strategies.

The segmentation further assists in comprehending how different product attributes resonate with varied demographics and regional consumer bases. For instance, the demand for grain-free or plant-based wet food may be higher in regions with strong health and wellness trends, while convenience in packaging might be a primary driver in urbanized areas. By dissecting the market into these core segments, the report offers comprehensive insights into the evolving landscape of pet nutrition and consumption patterns, enabling stakeholders to navigate the market effectively.

- By Product Type:

- Gravy: Preferred for palatability and ease of consumption.

- Jelly: Offers a unique texture and often used for specific formulations.

- Pate: Dense, smooth consistency, highly palatable for many pets.

- Stew: Features recognizable chunks of meat and vegetables, appealing to human-like meal preferences.

- Other (Mousse, Flakes): Niche textures catering to specific pet preferences or medical needs.

- By Animal Type:

- Cats: High demand due to natural preference for wet food for hydration and specific nutritional needs.

- Dogs: Significant market share, especially for smaller breeds, senior dogs, or those with dental issues.

- Other Pets: Includes wet food formulations for ferrets, small mammals, or exotic pets in specialized markets.

- By Ingredient Type:

- Meat-based: Dominant segment, includes chicken, beef, lamb, pork, and turkey.

- Fish-based: Popular for cats and specific dog breeds, offering Omega-3 fatty acids.

- Plant-based: Growing segment catering to vegan/vegetarian pet owners and pets with allergies.

- Grain-free: Addresses concerns about grain sensitivities and allergies in pets.

- Limited Ingredient: Simplistic formulations for pets with extreme sensitivities or specific dietary restrictions.

- By Packaging Type:

- Cans: Traditional, offering long shelf life and robust protection.

- Pouches: Convenient, single-serving, and environmentally friendlier alternatives to cans.

- Trays: Easy-to-serve, often used for gourmet or premium single portions.

- Other (e.g., plastic containers, bulk packaging): Specialized formats for specific products or large volume purchases.

- By Distribution Channel:

- Supermarkets/Hypermarkets: Major retail channel for conventional wet pet food.

- Pet Specialty Stores: Offer a wide range of premium and specialized wet pet food, expert advice.

- Online Retail: Rapidly growing channel, providing convenience and access to diverse brands, including D2C.

- Veterinary Clinics: Distribute therapeutic and prescription wet pet food for specific medical conditions.

- Other (e.g., convenience stores, farm stores, club stores): Secondary channels catering to specific consumer segments.

Regional Highlights

- North America: This region maintains a dominant position in the Wet Pet Food Market, primarily driven by the high prevalence of pet ownership, significant disposable incomes, and the strong humanization trend. Consumers in North America are highly receptive to premium, natural, and specialized pet food products, including those with functional benefits. The extensive presence of major pet food manufacturers and well-established distribution channels, particularly online retail and pet specialty stores, further solidifies its market leadership. Innovation in grain-free and limited-ingredient diets is also a key characteristic of this market.

- Europe: Europe represents another substantial market for wet pet food, characterized by a mature pet care industry and high awareness regarding pet health. Countries such as Germany, the UK, and France are key contributors to market growth, showing strong demand for ethically sourced, sustainably packaged, and gourmet wet pet food options. Regulatory standards are stringent, encouraging manufacturers to focus on high-quality ingredients and transparent labeling. The shift towards sustainable and eco-friendly products is particularly pronounced in this region, influencing packaging and ingredient choices.

- Asia Pacific (APAC): The APAC region is projected to exhibit the highest growth rate, fueled by an expanding middle class, increasing disposable incomes, and a cultural shift towards pet ownership in countries like China, Japan, and India. While traditionally a smaller market for wet pet food compared to dry, the humanization of pets is rapidly gaining traction, leading to a surge in demand for premium and convenient wet food formats. E-commerce platforms are playing a pivotal role in market penetration, making international brands accessible to a broader consumer base. Investment in pet care infrastructure and localized product offerings are key to unlocking the full potential of this dynamic region.

- Latin America: This region is experiencing steady growth in the wet pet food market, driven by urbanization and rising pet ownership. Brazil and Mexico are leading the charge, with increasing consumer awareness about pet nutrition. While economic factors can influence purchasing power, there is a growing segment of pet owners willing to spend on higher-quality pet food. Brands focusing on affordable yet nutritious wet food options, along with educational campaigns on pet health, are likely to succeed here.

- Middle East and Africa (MEA): The MEA region is an emerging market for wet pet food, with growth spurred by increasing disposable incomes and a gradual rise in pet ownership, particularly in urban centers of the GCC countries and South Africa. The market is still in its nascent stages but presents opportunities for international players as local pet care infrastructure develops. Cultural preferences and climate considerations often influence product types and packaging needs in this diverse region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Wet Pet Food Market.- Mars Petcare Inc.

- Nestle Purina PetCare

- Hill's Pet Nutrition (Colgate-Palmolive)

- Smucker Pet Foods

- Blue Buffalo Co. Ltd. (General Mills)

- Diamond Pet Foods, Inc.

- Merrick Pet Care, Inc. (Nestle Purina)

- Wellness Pet Company

- The J.M. Smucker Company

- Affinity Petcare S.A.

- Sunshine Mills, Inc.

- Almo Nature S.p.A.

- Freshpet, Inc.

- White Wave Foods (Danone)

- General Mills

- Archer Daniels Midland Company (ADM)

- PLB International

- Thai Union Group PCL

- Instinct Pet Food

- Cargill, Incorporated

Frequently Asked Questions

Analyze common user questions about the Wet Pet Food market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current growth outlook for the Wet Pet Food Market?

The Wet Pet Food Market is projected for robust growth, with a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. It is estimated to reach USD 45.1 billion by 2033, up from USD 28.5 billion in 2025.

What key trends are shaping the Wet Pet Food industry?

Key trends include the humanization of pets driving demand for premium products, increased focus on natural and functional ingredients, the expansion of e-commerce, and a growing emphasis on sustainable packaging and ethical sourcing.

How does AI impact the Wet Pet Food Market?

AI impacts the market through personalized nutrition recommendations, optimized supply chain management, enhanced product development based on data analysis, automated quality control, and improved customer engagement.

What are the main drivers of growth in the Wet Pet Food Market?

Primary drivers include the increasing humanization of pets and associated premiumization, the inherent palatability and hydration benefits of wet food, and growing consumer awareness of pet health and nutrition.

Which regions are key contributors to the Wet Pet Food Market?

North America and Europe are significant contributors due to high pet ownership and disposable incomes, while the Asia Pacific region is expected to show the fastest growth due to rising pet adoption and increasing affluence.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted