Weed Killer Market

Weed Killer Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700252 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

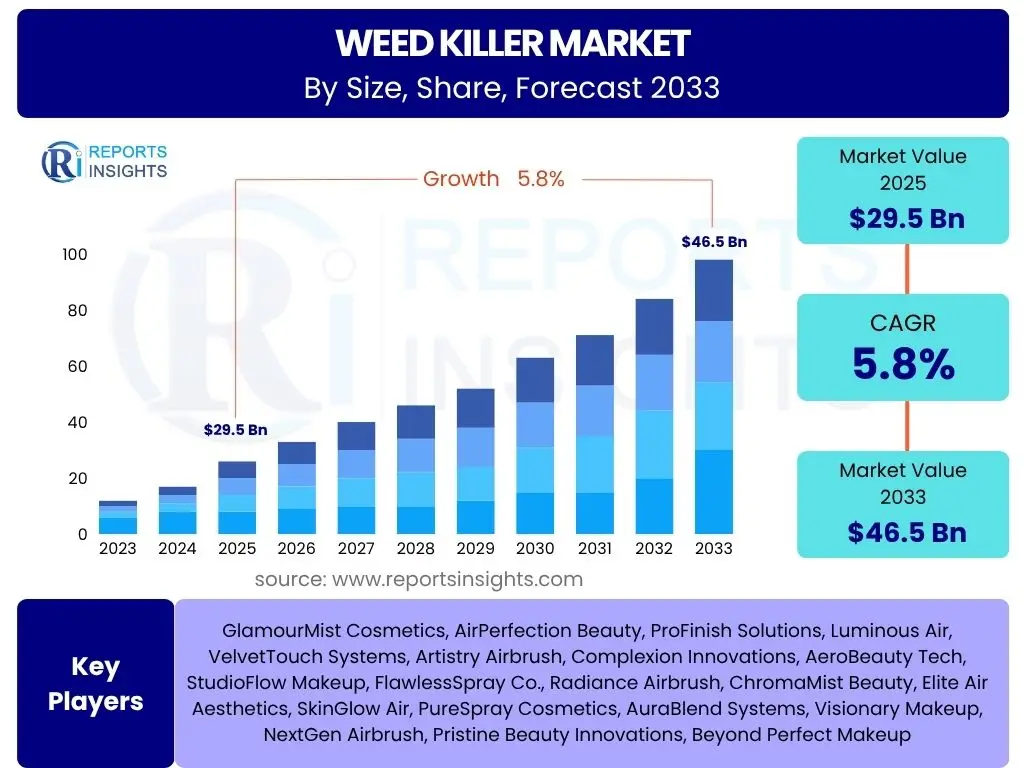

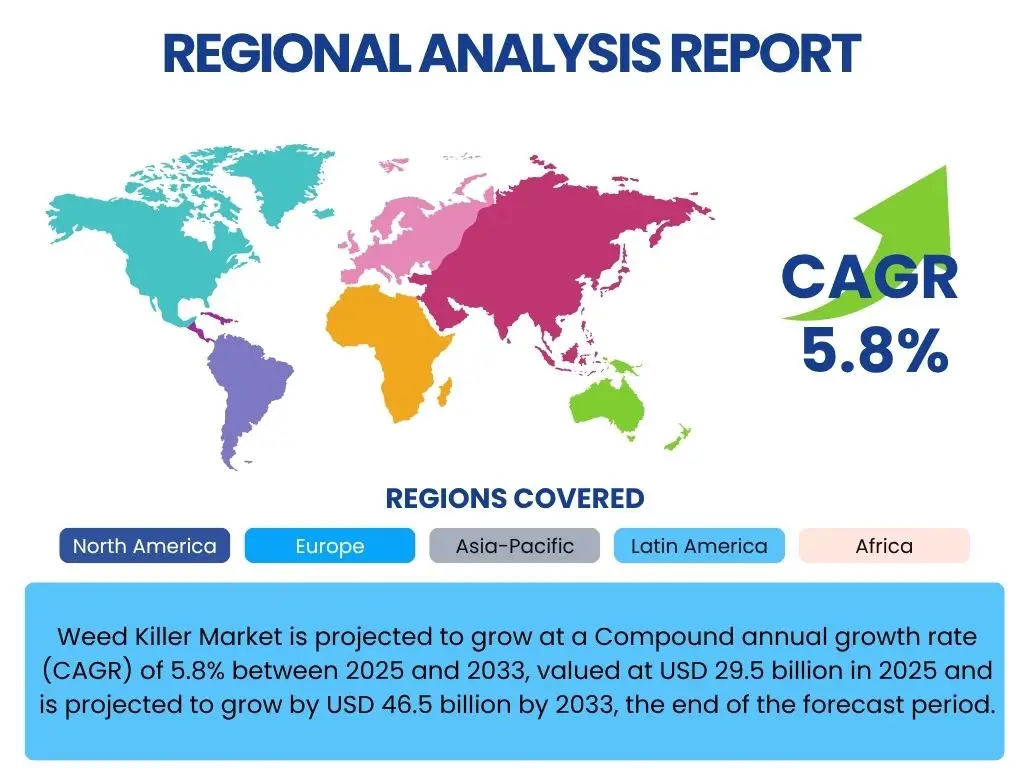

Weed Killer Market is projected to grow at a Compound annual growth rate (CAGR) of 5.8% between 2025 and 2033, current valued at USD 29.5 billion in 2025 and is projected to grow by USD 46.5 billion by 2033, the end of the forecast period.

Key Weed Killer Market Trends & Insights

The global weed killer market is currently undergoing significant transformation, driven by evolving agricultural practices, stringent environmental regulations, and a growing emphasis on sustainable solutions. A prominent trend involves the increasing adoption of biological and bio-based herbicides, reflecting a shift away from traditional synthetic chemicals due to heightened environmental awareness and concerns over herbicide resistance. Concurrently, advancements in precision agriculture technologies are enabling more targeted and efficient application of weed killers, minimizing chemical usage and maximizing efficacy. This integration of smart farming techniques, including drone-based spraying and AI-powered weed detection, is revolutionizing how weed management is approached across various agricultural landscapes.

Another critical insight is the escalating challenge of herbicide resistance in weeds, compelling manufacturers and researchers to innovate and develop new modes of action or explore synergistic formulations. This has spurred investment in research and development for novel chemical compositions and a greater focus on integrated weed management (IWM) strategies that combine chemical, biological, and cultural methods. Furthermore, the market is witnessing a regional divergence in regulatory frameworks, influencing product availability and adoption rates, with developed economies often leading the charge in eco-friendly alternatives while developing regions prioritize yield optimization. These interwoven trends underscore a dynamic market landscape poised for continued innovation and adaptation to global agricultural demands and environmental imperatives.

- Rising demand for sustainable and bio-based herbicides.

- Increasing adoption of precision agriculture and smart spraying technologies.

- Growing incidence of herbicide-resistant weeds necessitating new solutions.

- Integration of digital tools for enhanced weed detection and management.

- Shift towards integrated weed management (IWM) strategies.

- Expansion of specialty crop cultivation requiring tailored weed control.

AI Impact Analysis on Weed Killer

Artificial intelligence (AI) is poised to revolutionize the weed killer market by fundamentally transforming detection, application, and development processes. At the forefront, AI-powered computer vision systems, often integrated with drones or robotic platforms, can accurately identify and differentiate between crops and weeds in real-time, enabling highly localized and precise herbicide application. This capability dramatically reduces overall herbicide consumption, minimizes environmental impact, and addresses concerns about chemical residues, aligning with the growing demand for sustainable agriculture. Furthermore, AI algorithms can analyze vast datasets of weed patterns, soil conditions, and weather forecasts to predict weed infestations, allowing farmers to implement proactive control measures rather than reactive treatments, thereby optimizing resource allocation and improving efficiency across the entire weed management lifecycle.

Beyond precision application, AI significantly impacts the research and development pipeline for new weed killer formulations. Machine learning models can analyze molecular structures and predict their herbicidal efficacy, accelerating the discovery of novel active ingredients and resistance management solutions. This speeds up the traditionally lengthy and costly R&D process, bringing innovative products to market faster. Additionally, AI can assist in optimizing herbicide formulations for enhanced performance, biodegradability, and reduced off-target effects. As AI technologies become more accessible and integrated into farm equipment and decision-making platforms, their influence on the weed killer market will grow, leading to more intelligent, efficient, and environmentally responsible weed control solutions that can significantly shape the future of agriculture.

- Enabling ultra-precision spraying through AI-powered visual detection.

- Optimizing herbicide dosage and reducing overall chemical usage.

- Predictive analytics for early weed infestation warnings.

- Accelerating research and development of novel herbicide formulations.

- Facilitating autonomous weeding systems and robotic applications.

- Improving data-driven decision-making for integrated weed management.

Key Takeaways Weed Killer Market Size & Forecast

- The global weed killer market is projected to reach USD 46.5 billion by 2033.

- Expected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% from 2025 to 2033.

- Market size in 2025 is estimated at USD 29.5 billion.

- Growth is primarily driven by increasing agricultural activities and demand for crop protection.

- Asia Pacific is anticipated to be a significant growth region due to expanding agricultural land and rising food demand.

- Non-selective herbicides and biological formulations are poised for substantial growth.

- The agricultural application segment holds the largest market share.

- Technological advancements in precision agriculture are a key growth accelerator.

- Increasing focus on sustainable and environmentally friendly weed control methods.

Weed Killer Market Drivers Analysis

The weed killer market is propelled by a confluence of critical drivers that underscore its essential role in modern agriculture and land management. A primary driver is the relentless growth in the global population, which places immense pressure on food production systems, necessitating optimized crop yields. Weeds compete with crops for vital resources such as nutrients, water, and sunlight, leading to significant yield losses if not effectively controlled. Consequently, the increasing adoption of herbicides becomes crucial for farmers aiming to maximize productivity and ensure food security. Furthermore, advancements in agricultural practices, including the widespread adoption of no-till and minimum-till farming, rely heavily on effective weed control to preserve soil health and prevent erosion, further stimulating demand for chemical and biological weed management solutions.

Another significant driver is the continuous innovation in herbicide formulations, leading to more effective, crop-selective, and environmentally safer products. Manufacturers are investing heavily in research and development to create herbicides with novel modes of action, enhanced efficacy against resistant weeds, and improved safety profiles for both users and the environment. The expansion of high-value crops and specialty crops also contributes to market growth, as these crops often require precise and specialized weed control measures to protect their economic value. Additionally, the growing awareness among farmers about the economic benefits of timely and effective weed management, coupled with supportive governmental policies and agricultural extension services promoting efficient farming techniques, collectively serves to bolster the global weed killer market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Food Demand & Population Growth | +1.5% | Global, particularly Asia Pacific, Latin America, Africa | Long-term (2025-2033) |

| Rising Crop Losses Due to Weed Infestation | +1.2% | Global, especially emerging agricultural economies | Mid-term (2025-2030) |

| Advancements in Herbicide Formulations and Application Technologies | +1.0% | North America, Europe, China | Mid to Long-term (2025-2033) |

| Growing Adoption of Precision Agriculture and Integrated Weed Management (IWM) | +1.1% | North America, Europe, parts of Asia Pacific | Mid to Long-term (2025-2033) |

| Expansion of Cultivated Land and Commercial Farming | +1.0% | Latin America, Africa, Southeast Asia | Long-term (2025-2033) |

Weed Killer Market Restraints Analysis

Despite robust growth drivers, the weed killer market faces several significant restraints that could temper its expansion. Foremost among these are the increasingly stringent environmental regulations and public concerns regarding the ecological impact of chemical herbicides. Governments and regulatory bodies worldwide are imposing stricter limits on the use of certain active ingredients, particularly those linked to water contamination, biodiversity loss, or potential health risks. This often leads to product bans or lengthy approval processes, increasing the time and cost associated with bringing new formulations to market. Public perception and consumer demand for organic or chemical-free produce also exert pressure, prompting farmers and food producers to explore alternative weed control methods that do not rely on synthetic chemicals, thereby limiting the growth of conventional herbicide segments.

Another major restraint is the widespread development of herbicide resistance in weed populations. Continuous and widespread use of herbicides with the same mode of action has led many common weed species to evolve resistance, rendering previously effective products less potent or entirely ineffective. This necessitates the development of new, more complex, and often more expensive solutions, increasing the financial burden on farmers and R&D costs for manufacturers. Furthermore, the high initial investment required for sophisticated application equipment, especially for precision agriculture technologies, can be a barrier for small and medium-sized farmers in developing regions. Volatility in raw material prices and the complex global supply chain for agrochemicals also pose ongoing challenges, potentially impacting production costs and product availability, collectively acting as significant impediments to market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations and Bans on Certain Chemicals | -1.3% | Europe, North America, Japan | Long-term (2025-2033) |

| Development of Herbicide Resistance in Weed Populations | -1.0% | Global, especially regions with intensive agriculture | Mid to Long-term (2025-2033) |

| Growing Public & Consumer Preference for Organic/Sustainable Farming | -0.8% | North America, Europe, Urban centers in Asia Pacific | Mid-term (2025-2030) |

| High R&D Costs for New Product Development | -0.6% | Global, impacting market entry for new players | Long-term (2025-2033) |

| Volatility in Raw Material Prices and Supply Chain Disruptions | -0.5% | Global, impacting manufacturing hubs | Short to Mid-term (2025-2028) |

Weed Killer Market Opportunities Analysis

Significant opportunities are emerging within the weed killer market, largely driven by the imperative for sustainable agriculture and technological innovation. The most promising avenue lies in the development and commercialization of biological and bio-herbicides. As environmental concerns intensify and regulatory landscapes shift, there is a substantial unmet demand for effective, non-chemical weed control alternatives. These bio-based solutions, derived from natural sources like plant extracts, microbes, or fungi, offer reduced environmental impact and lower risks of resistance development, appealing to both eco-conscious consumers and farmers facing stringent chemical regulations. Investment in research and development for these novel biological formulations represents a lucrative growth pathway for market players seeking to align with future agricultural trends and environmental stewardship.

Furthermore, the integration of advanced technologies such as artificial intelligence, drone technology, and robotics presents immense opportunities for precision weed management. These technologies enable ultra-targeted application of herbicides, whether chemical or biological, minimizing waste and maximizing efficacy. The concept of "spot spraying" where only weeds are treated, rather than entire fields, significantly reduces input costs and environmental footprint. This technological leap allows for more efficient resource utilization and offers solutions to the challenge of herbicide resistance by enabling diverse and adaptive weed control strategies. Beyond technology, untapped potential exists in emerging economies, particularly in Asia Pacific, Latin America, and Africa, where agricultural practices are rapidly modernizing, and the adoption of effective weed control solutions is still in its nascent stages. These regions offer vast agricultural lands and a growing need for enhanced productivity, presenting a ripe market for both established and novel weed killer products and technologies.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and Adoption of Biological & Bio-Herbicides | +1.5% | Global, particularly North America, Europe | Long-term (2025-2033) |

| Integration of Precision Agriculture and Digital Farming Technologies | +1.3% | Developed economies, tech-forward agricultural regions | Mid to Long-term (2025-2033) |

| Expansion into Emerging Markets with Growing Agricultural Sectors | +1.0% | Asia Pacific, Latin America, Africa | Long-term (2025-2033) |

| Demand for Targeted & Crop-Specific Herbicide Solutions | +0.8% | Global, especially high-value crop regions | Mid-term (2025-2030) |

| Synergistic Solutions combining Chemical and Biological Agents | +0.7% | Global, fostering integrated pest management | Mid to Long-term (2025-2033) |

Weed Killer Market Challenges Impact Analysis

The weed killer market faces multifaceted challenges that demand strategic responses from industry players. One pervasive challenge is the increasing complexity of the regulatory landscape across different countries and regions. Harmonizing product approvals, adhering to varying residue limits, and navigating bans on specific active ingredients create significant hurdles for manufacturers operating globally. This regulatory fragmentation can delay market entry for new products, increase compliance costs, and limit product portfolios in certain geographies, impacting overall market penetration and profitability. Furthermore, the continuous and escalating evolution of herbicide-resistant weeds presents a persistent biological challenge, requiring constant investment in new research and development efforts to identify novel modes of action and circumvent resistance mechanisms. Failure to address resistance effectively can lead to reduced product efficacy and farmer dissatisfaction.

Another critical challenge revolves around the increasing cost of research and development for new weed killer molecules. The rigorous testing, long approval timelines, and high failure rates associated with discovering and commercializing novel active ingredients translate into substantial financial outlays. This escalating R&D cost often deters smaller players and concentrates innovation among a few large agrochemical corporations, potentially limiting market diversity. Moreover, climate change introduces unpredictability into agricultural cycles, affecting weed emergence patterns, herbicide efficacy, and application windows, thus complicating weed management strategies. Supply chain disruptions, often exacerbated by geopolitical tensions or global health crises, can also impede the availability of raw materials and finished products, leading to price volatility and constrained supply. Addressing these challenges effectively will be crucial for companies seeking sustained growth and leadership within the dynamic weed killer market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Regulatory Complexity and Diversified Approval Processes | -0.9% | Global, particularly Europe and North America | Long-term (2025-2033) |

| Escalating Herbicide Resistance and Need for New Solutions | -0.8% | Global, affecting major agricultural regions | Long-term (2025-2033) |

| High Investment in R&D and Long Product Development Cycles | -0.7% | Global, affecting major market players | Long-term (2025-2033) |

| Climate Change Impact on Weed Emergence and Herbicide Efficacy | -0.6% | Global, impacting vulnerable agricultural zones | Long-term (2025-2033) |

| Supply Chain Disruptions and Raw Material Scarcity | -0.5% | Global, impacting manufacturing and distribution | Short to Mid-term (2025-2028) |

Weed Killer Market - Updated Report Scope

The updated scope of this comprehensive market research report provides a granular analysis of the Weed Killer Market, offering critical insights into its current dynamics and future projections. It meticulously details market size estimations, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. The report leverages a robust research methodology to deliver actionable intelligence for stakeholders, enabling informed strategic decision-making in a rapidly evolving agricultural landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 29.5 Billion |

| Market Forecast in 2033 | USD 46.5 Billion |

| Growth Rate | 5.8% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Leading Global Agrochemical Company A, Major Crop Protection Innovator B, Global Agricultural Solutions Provider C, Specialty Chemicals Manufacturer D, Leading Agribusiness Corporation E, Diverse Agricultural Science Company F, Innovative Crop Care Solutions G, Renowned Agrochemicals Producer H, Global Seed and Crop Protection Firm I, Key Agricultural Biotechnology Player J, Integrated Agribusiness Company K, Regional Crop Protection Specialist L, Environmental Science & Solutions M, Advanced Agriscience Solutions N, Sustainable Agrochemicals Partner O, Global Agricultural Input Supplier P, Crop Health & Nutrition Provider Q, Modern Agriculture Technology Firm R, Advanced Formulation Developer S, Global Agroscience Partner T |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

:The Weed Killer Market is meticulously segmented to provide a granular understanding of its diverse components, enabling stakeholders to identify key growth pockets and strategic opportunities. These segmentations are critical for analyzing market dynamics across various dimensions, from the chemical properties of herbicides to their specific applications and formulations. Understanding how these segments interact and grow individually provides a holistic view of the market's evolving landscape and future trajectories, guiding investment and product development decisions.

Each segmentation delves into distinct market characteristics, offering insights into product preferences, user behavior, and regional adoption patterns. For instance, the 'By Type' segmentation distinguishes between herbicides that target specific weeds versus those that eradicate all plant growth, highlighting different market needs. Similarly, 'By Crop Type' illustrates how weed killer demand varies based on the specific requirements of major agricultural commodities and specialty crops. This detailed breakdown allows for a comprehensive assessment of market potential within each niche, crucial for companies aiming to optimize their product portfolios and market entry strategies to align with the most promising growth areas.

- By Type:

- Selective: Herbicides designed to control specific weed species without harming the cultivated crop. These are crucial for targeted weed management in diverse cropping systems.

- Non-selective: Herbicides that kill all plant material they come into contact with. They are widely used for total vegetation control in non-agricultural areas, fallow land, or before planting.

- By Mode of Action:

- Photosynthesis Inhibitors: Herbicides that disrupt the plant's ability to perform photosynthesis, leading to plant death.

- Amino Acid Inhibitors: Chemicals that block the synthesis of essential amino acids in weeds, vital for their growth and survival.

- Growth Regulators: Herbicides that mimic or interfere with plant hormones, causing uncontrolled and abnormal growth that leads to death.

- Lipid Synthesis Inhibitors: Chemicals that prevent the formation of lipids, which are crucial components of plant cell membranes.

- Cell Membrane Disruptors: Herbicides that cause rapid destruction of plant cell membranes, leading to desiccation and death.

- Others: Includes various other modes of action such as cell division inhibitors, pigment inhibitors, and root growth inhibitors.

- By Crop Type:

- Cereals & Grains:

- Wheat

- Rice

- Corn

- Barley

- Oilseeds & Pulses:

- Soybean

- Cotton

- Rapeseed

- Sunflower

- Fruits & Vegetables: Herbicides designed for delicate fruit and vegetable crops, emphasizing crop safety and residue limits.

- Turf & Ornamentals: Weed killers for lawns, golf courses, nurseries, and ornamental plants, focusing on aesthetic quality and plant health.

- Others: Includes a range of minor crops, specialty crops, and plantation crops requiring specific weed management.

- Cereals & Grains:

- By Application:

- Agricultural:

- Crop-based: Applied directly to crops or crop fields to protect specific cultivations.

- Non-Crop based: Used in agricultural settings but not directly on food crops, such as farm roads, fence lines, or storage areas.

- Non-Agricultural:

- Industrial: Used in industrial sites, railways, power lines, and infrastructure areas for vegetation control and safety.

- Commercial: Applied in commercial landscapes, parks, sports fields, and public spaces for aesthetic maintenance and weed prevention.

- Residential: For home gardens, lawns, and driveways, catering to individual consumer needs.

- Aquatic: Specifically designed for weed control in ponds, lakes, rivers, and drainage canals.

- Agricultural:

- By Formulation:

- Liquid: Includes soluble concentrates (SL), emulsifiable concentrates (EC), and suspension concentrates (SC), known for ease of application.

- Granular: Solid formulations that can be broadcast or applied directly to the soil, offering sustained release.

- Wettable Powder: Fine dry powders that disperse in water to form a suspension, commonly used for broad-spectrum control.

- Others: Encompasses dusts, aerosols, and other specialized formulations catering to specific application methods or environments.

Regional Highlights

The global weed killer market exhibits distinct regional dynamics, influenced by diverse agricultural practices, climatic conditions, regulatory environments, and economic development levels. Each region presents unique growth drivers and challenges, shaping its contribution to the overall market trajectory. A deep understanding of these regional nuances is crucial for strategic market positioning and resource allocation.

North America and Europe are characterized by advanced agricultural technologies, stringent environmental regulations, and a growing emphasis on precision farming and sustainable solutions. Asia Pacific, on the other hand, stands out due to its vast agricultural land, burgeoning population, and increasing adoption of modern farming techniques, making it a pivotal growth engine. Latin America benefits from its significant agricultural exports and the expansion of cash crops, while the Middle East and Africa represent emerging markets with considerable untapped agricultural potential and a rising focus on food security.

- North America: This region is a mature market driven by the adoption of advanced farming practices, genetically modified (GM) crops, and a strong focus on high-yield agriculture. The demand for selective herbicides and precision application technologies is particularly high. Stringent environmental regulations also drive innovation towards safer, more sustainable formulations, including bio-herbicides. The presence of major agrochemical companies and extensive R&D facilities contributes to its market leadership.

- Europe: Characterized by highly stringent environmental and health regulations concerning chemical use, leading to a strong push towards biological and integrated weed management solutions. The market here emphasizes residue-free produce and sustainable farming practices, stimulating demand for low-impact herbicides and innovative application methods. Despite regulatory hurdles, the region maintains significant market value due to its advanced agricultural sector and high input usage.

- Asia Pacific (APAC): Expected to be the fastest-growing region in the weed killer market. This growth is propelled by a rapidly expanding population, increasing food demand, and government initiatives promoting agricultural modernization and productivity. Countries like China, India, and Southeast Asian nations are witnessing substantial growth due to vast arable land, rising awareness among farmers about efficient weed management, and the increasing adoption of modern farming techniques. The region presents significant opportunities for both traditional and new-generation herbicides.

- Latin America: A major hub for agricultural exports, particularly for soybeans, corn, and sugarcane, which drives substantial demand for weed killers. The adoption of no-till farming practices, which heavily rely on herbicides for weed control, is prevalent here. Brazil and Argentina are key contributors to the market, with increasing investment in agricultural infrastructure and technology. The region's vast agricultural land and favorable climatic conditions support robust market growth.

- Middle East and Africa (MEA): An emerging market for weed killers, driven by increasing efforts to enhance food security, modernize agricultural practices, and expand cultivated land. While currently smaller, the region offers significant growth potential as governments and international organizations invest in agricultural development. Challenges such as water scarcity and diverse climatic conditions also necessitate efficient and targeted weed management solutions.

Top Key Players:

The market research report covers the analysis of key stake holders of the Weed Killer Market. Some of the leading players profiled in the report include -:- Leading Global Agrochemical Company A

- Major Crop Protection Innovator B

- Global Agricultural Solutions Provider C

- Specialty Chemicals Manufacturer D

- Leading Agribusiness Corporation E

- Diverse Agricultural Science Company F

- Innovative Crop Care Solutions G

- Renowned Agrochemicals Producer H

- Global Seed and Crop Protection Firm I

- Key Agricultural Biotechnology Player J

- Integrated Agribusiness Company K

- Regional Crop Protection Specialist L

- Environmental Science & Solutions M

- Advanced Agriscience Solutions N

- Sustainable Agrochemicals Partner O

- Global Agricultural Input Supplier P

- Crop Health & Nutrition Provider Q

- Modern Agriculture Technology Firm R

- Advanced Formulation Developer S

- Global Agroscience Partner T

Frequently Asked Questions:

What are the primary types of weed killers available in the market?

The primary types of weed killers are generally categorized into selective and non-selective herbicides. Selective weed killers are designed to target and eliminate specific weed species while leaving desired crops unharmed. Non-selective weed killers, on the other hand, eradicate all plant material they come into contact with, commonly used for total vegetation control in non-cropped areas or before planting. Further classifications include contact herbicides, which kill plants directly upon contact, and systemic herbicides, which are absorbed by the plant and translocated throughout its system to kill it.How do environmental regulations impact the weed killer market?

Environmental regulations significantly impact the weed killer market by influencing product development, sales, and application. Stricter regulations, particularly in regions like Europe and North America, lead to bans or restrictions on certain active ingredients, compelling manufacturers to invest heavily in research and development of more environmentally benign and sustainable formulations, such as biological herbicides. These regulations also drive the adoption of precision application technologies to minimize off-target chemical drift and reduce overall chemical usage, pushing the market towards eco-friendlier and more responsible weed control practices.What role does precision agriculture play in the weed killer market?

Precision agriculture plays a transformative role in the weed killer market by enabling highly targeted and efficient herbicide application. Technologies like GPS-guided sprayers, drone-based imaging, and AI-powered weed detection systems allow farmers to apply weed killers only where needed, rather than broadcasting over entire fields. This "spot spraying" approach significantly reduces herbicide consumption, lowers input costs, minimizes environmental impact, and addresses concerns about chemical residues. It also contributes to mitigating herbicide resistance by enabling more diverse and adaptive weed management strategies tailored to specific weed patches.What are the key growth drivers for the weed killer market?

The key growth drivers for the weed killer market include the increasing global population and the resultant escalating demand for food production, which necessitates higher crop yields. Rising crop losses due to uncontrolled weed infestations further drive the adoption of effective herbicides. Additionally, continuous advancements in herbicide formulations, leading to more efficacious and selective products, along with the growing adoption of precision agriculture technologies and integrated weed management (IWM) practices, are significant contributors to market expansion. The expansion of cultivated land and commercial farming in developing economies also fuels demand.What are the emerging trends in weed control beyond traditional chemicals?

Emerging trends in weed control extend beyond traditional chemical herbicides, focusing on sustainability and technological integration. Key trends include the rapid rise of biological and bio-herbicides, which utilize natural organisms or their byproducts for weed suppression. There is also a significant shift towards integrated weed management (IWM) strategies, combining chemical, cultural, mechanical, and biological methods for holistic control. Furthermore, the increasing adoption of smart farming technologies, such as AI-driven robotics for autonomous weeding and predictive analytics for weed emergence, represents a significant move towards precise, data-driven, and environmentally conscious weed management solutions.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted