Water Treatment Equipment Market

Water Treatment Equipment Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709455 | Last Updated : December 09, 2025 |

Format : ![]()

![]()

![]()

![]()

Water Treatment Equipment Market Size

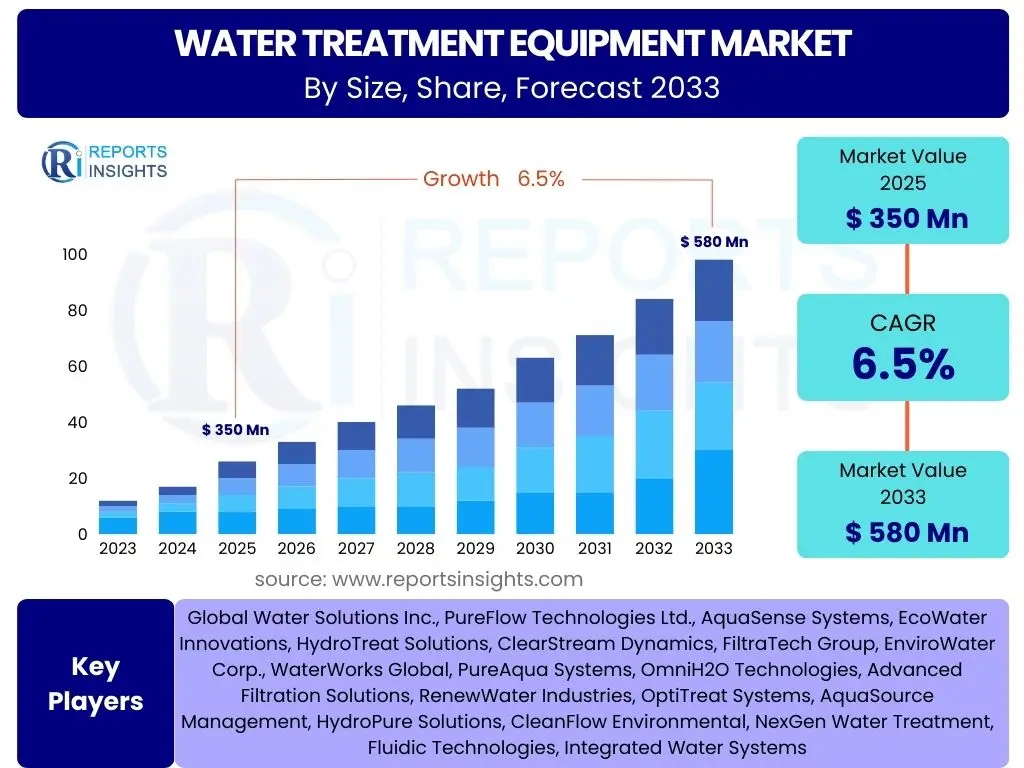

According to Reports Insights Consulting Pvt Ltd, The Water Treatment Equipment Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 350 Billion in 2025 and is projected to reach USD 580 Billion by the end of the forecast period in 2033.

Key Water Treatment Equipment Market Trends & Insights

The global water treatment equipment market is experiencing significant transformation driven by an escalating demand for clean water, growing environmental concerns, and the need for sustainable water management practices across diverse sectors. Key trends revolve around technological advancements that enhance efficiency, reduce operational costs, and promote resource recovery. There is a discernible shift towards integrated and intelligent systems that offer real-time monitoring, predictive analytics, and automated control, moving beyond conventional treatment methodologies to address complex water quality challenges.

Furthermore, stringent regulatory frameworks worldwide, aimed at safeguarding public health and ecosystems, compel industries and municipalities to adopt more advanced and effective water treatment solutions. This regulatory pressure, coupled with increasing public awareness regarding water scarcity and pollution, fuels innovation in areas such as desalination, wastewater recycling, and point-of-use treatment. The market is also seeing a rise in the adoption of modular and compact treatment systems, which provide flexibility and scalability, particularly beneficial for decentralized applications and regions with rapidly developing infrastructure.

Sustainability is a core driver, manifesting in trends like energy-efficient technologies, reduced chemical usage, and the recovery of valuable resources from wastewater, such as nutrients and energy. The integration of digital technologies, including IoT and cloud-based platforms, is enabling smart water networks that optimize distribution, detect leaks, and improve overall system resilience. These interconnected trends collectively shape a market focused on efficiency, environmental stewardship, and robust water security for both industrial and municipal applications.

- Advanced Filtration Technologies: Emergence of ultrafiltration, nanofiltration, and membrane bioreactors for superior contaminant removal.

- Wastewater Reuse and Recycling: Increasing adoption of technologies for treating and reusing industrial and municipal wastewater.

- Smart Water Management Systems: Integration of IoT, sensors, and data analytics for real-time monitoring and optimized plant operations.

- Modular and Decentralized Solutions: Growth in compact, scalable systems for various applications, reducing infrastructure costs.

- Energy-Efficient Treatment Processes: Development of low-energy consumption systems, including advanced oxidation processes and bio-electrochemical systems.

- Resource Recovery: Focus on extracting valuable resources like nutrients, metals, and energy from wastewater streams.

AI Impact Analysis on Water Treatment Equipment

Artificial Intelligence (AI) is poised to significantly revolutionize the water treatment equipment market by enhancing operational efficiency, predictive capabilities, and decision-making processes. Users are increasingly seeking how AI can move water treatment from reactive to proactive, ensuring consistent water quality and optimizing resource utilization. AI algorithms can process vast amounts of data from sensors, operational logs, and environmental conditions to identify patterns, predict equipment failures, and anticipate changes in water quality, thus enabling predictive maintenance and preemptive operational adjustments. This capability is critical for reducing downtime, extending equipment lifespan, and minimizing maintenance costs, addressing key pain points for plant operators.

The application of AI extends to optimizing treatment processes in real-time. By analyzing various parameters such as flow rates, chemical dosages, and contaminant levels, AI systems can fine-tune operational settings to achieve optimal treatment efficacy while minimizing energy consumption and chemical usage. This leads to substantial operational cost savings and a reduced environmental footprint, which are growing priorities for both municipal and industrial stakeholders. Furthermore, AI-powered control systems can adapt to dynamic environmental conditions and varying influent water qualities, ensuring robust and reliable performance under diverse circumstances, thereby improving the overall resilience of water treatment infrastructure.

Looking ahead, the integration of AI will drive the development of more autonomous and intelligent water treatment plants. Users expect AI to facilitate better asset management, improve compliance with stringent discharge regulations, and enable more efficient responses to emergencies. The ability of AI to learn from historical data and continuously improve its decision-making will be a cornerstone for achieving sustainable water management goals, making water treatment more efficient, cost-effective, and environmentally friendly. This transformative impact positions AI as a crucial enabler for next-generation water treatment solutions.

- Predictive Maintenance: AI algorithms analyze sensor data to forecast equipment failures, reducing unplanned downtime and maintenance costs.

- Process Optimization: AI-driven control systems fine-tune chemical dosages and operational parameters in real-time, improving treatment efficiency and reducing energy consumption.

- Real-time Monitoring & Anomaly Detection: AI platforms analyze continuous data streams to identify deviations and potential issues, ensuring consistent water quality.

- Energy Efficiency: Optimization of pump operations and aeration systems through AI leads to significant energy savings.

- Autonomous Operations: Development of self-regulating treatment plants capable of adapting to varying influent conditions and operational demands.

- Data Analytics & Insights: AI provides actionable insights from complex operational data, aiding in better decision-making and long-term planning.

Key Takeaways Water Treatment Equipment Market Size & Forecast

The consistent growth trajectory of the Water Treatment Equipment Market, projected to reach USD 580 Billion by 2033, underscores its critical role in addressing global water challenges and ensuring sustainable development. A primary takeaway is the increasing recognition of water as a finite and indispensable resource, driving both public and private investment into advanced treatment technologies. This sustained growth is not merely incremental but reflective of fundamental shifts in industrial practices, urban planning, and environmental policies, making it a compelling sector for innovation and strategic development across all regions.

Another significant insight is the market's resilience and adaptability to evolving environmental concerns and technological advancements. Stakeholders are actively seeking solutions that are not only effective in purifying water but also contribute to resource efficiency, energy conservation, and the circular economy. This demand for integrated and sustainable solutions means that companies offering cutting-edge filtration, disinfection, and wastewater recycling technologies, especially those incorporating digital and AI components, are positioned for substantial growth and market leadership in the coming years.

Ultimately, the market forecast highlights a dynamic environment where regulatory mandates, technological innovation, and escalating demand for potable and process water converge. Businesses and governments are prioritizing investments in robust water infrastructure, driving demand for a wide array of equipment from small-scale residential units to large-scale municipal and industrial treatment plants. The key takeaway emphasizes that the water treatment equipment market is a foundational pillar for global sustainability, offering significant opportunities for innovation, investment, and strategic partnerships.

- Sustained Growth Momentum: Market projected for robust expansion, reflecting increasing global demand for water security and quality.

- Innovation as a Core Driver: Continuous development in advanced filtration, digital integration, and sustainable treatment processes is crucial for market leadership.

- Regulatory Impact: Stringent environmental and health regulations globally are primary catalysts for technology adoption and market expansion.

- High Investment Potential: The sector presents attractive opportunities for capital investment, driven by infrastructure development and sustainability mandates.

- Resource Efficiency Focus: Growing emphasis on solutions that optimize water usage, reduce energy consumption, and enable resource recovery.

Water Treatment Equipment Market Drivers Analysis

The water treatment equipment market is primarily propelled by an confluence of demographic, environmental, and regulatory factors that collectively intensify the demand for effective water management solutions. Rapid global urbanization and industrialization lead to increased water consumption and, consequently, higher volumes of wastewater requiring treatment before discharge or reuse. Concurrently, the escalating issue of water scarcity, exacerbated by climate change and inefficient water usage, necessitates the development and deployment of advanced treatment technologies, particularly for desalination and wastewater recycling, to augment available water resources.

Furthermore, the implementation and enforcement of increasingly stringent environmental regulations globally play a pivotal role in driving market growth. Governments and international bodies are imposing stricter standards on effluent discharge quality and promoting the reuse of treated water, compelling industries and municipalities to upgrade their existing infrastructure and adopt state-of-the-art treatment equipment. This regulatory push not only ensures compliance but also fosters innovation in the development of more efficient and environmentally friendly treatment processes.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing Water Scarcity | +1.5-2.0% | MEA, Asia Pacific, Western US | Short- to Mid-Term (2025-2030) |

| Strict Environmental Regulations | +1.2-1.8% | Europe, North America, China, India | Mid- to Long-Term (2026-2033) |

| Rapid Industrialization & Urbanization | +1.0-1.5% | Asia Pacific, Latin America, Africa | Ongoing (2025-2033) |

| Increasing Public Health Awareness | +0.8-1.2% | Global, particularly developed regions | Long-Term (2028-2033) |

| Aging Water Infrastructure | +0.7-1.0% | North America, Europe | Short- to Mid-Term (2025-2030) |

Water Treatment Equipment Market Restraints Analysis

Despite significant growth drivers, the water treatment equipment market faces several notable restraints that could temper its expansion. A primary limiting factor is the high initial capital expenditure required for installing advanced water treatment systems. The cost of acquiring sophisticated equipment, along with civil engineering works and installation, can be prohibitive for many municipalities, especially in developing regions, and for smaller industrial facilities. This substantial upfront investment often leads to longer payback periods, making it challenging to secure funding and justify projects without significant governmental support or subsidies.

Furthermore, the operational and maintenance costs associated with water treatment equipment, particularly for membrane-based systems or those requiring specialized chemicals, can be substantial. These ongoing expenses, including energy consumption, replacement of consumables, and skilled labor for operation and servicing, contribute to the overall economic burden. In regions with limited technical expertise or fluctuating energy prices, these costs can render advanced treatment solutions less viable, prompting reliance on less effective or older technologies. These economic barriers often slow down the adoption of innovative solutions, despite their long-term benefits.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Expenditure | -0.8-1.2% | Developing Economies, Small Municipalities | Ongoing (2025-2033) |

| High Operational & Maintenance Costs | -0.7-1.0% | Global, particularly energy-intensive processes | Ongoing (2025-2033) |

| Lack of Skilled Workforce | -0.5-0.8% | Developing Regions, Specialized Tech Adoption | Mid-Term (2026-2031) |

| Complex Regulatory Approval Processes | -0.3-0.6% | Specific Countries with Bureaucracy | Short- to Mid-Term (2025-2030) |

Water Treatment Equipment Market Opportunities Analysis

The water treatment equipment market is rife with opportunities, driven by evolving global needs and technological advancements. One significant area of growth lies in the increasing focus on wastewater reuse and recycling. As water scarcity intensifies, industries and municipalities are increasingly looking to treat and repurpose their wastewater for non-potable uses, such as irrigation, industrial processes, and groundwater recharge. This shift presents vast opportunities for manufacturers of advanced membrane systems, biological treatment units, and disinfection technologies capable of producing high-quality reclaimed water, thereby creating new market segments and expanding existing ones.

Emerging economies, particularly in Asia Pacific, Latin America, and Africa, represent another substantial opportunity. These regions are experiencing rapid population growth, industrial expansion, and urbanization, often coupled with inadequate existing water infrastructure. This scenario necessitates significant investments in new water treatment facilities and equipment, creating a lucrative market for both conventional and advanced treatment solutions. Furthermore, the development of smart water management systems, integrating IoT, AI, and big data analytics, offers opportunities for companies to provide comprehensive digital solutions that enhance efficiency, reduce costs, and improve the resilience of water infrastructure globally.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Wastewater Reuse & Recycling | +1.5-2.0% | Global, especially arid regions | Ongoing (2025-2033) |

| Smart Water Management & Digitalization | +1.2-1.8% | Developed Nations, Smart Cities | Mid- to Long-Term (2026-2033) |

| Untapped Markets in Developing Economies | +1.0-1.5% | Asia Pacific, Latin America, Africa | Long-Term (2027-2033) |

| Desalination Technologies Advancements | +0.8-1.2% | MEA, Coastal Regions, Islands | Mid-Term (2026-2031) |

| Modular & Decentralized Treatment Solutions | +0.7-1.0% | Rural Areas, Industrial Parks, Disaster Relief | Short- to Mid-Term (2025-2030) |

Water Treatment Equipment Market Challenges Impact Analysis

The water treatment equipment market faces several significant challenges that require innovative approaches and strategic planning to overcome. One of the primary hurdles is the complex and often fragmented regulatory landscape across different regions and countries. Variations in water quality standards, discharge limits, and environmental policies can create inconsistencies, making it difficult for manufacturers to develop universally compliant equipment and for operators to navigate diverse legal frameworks. This regulatory complexity can slow down technology adoption and increase compliance costs, especially for global enterprises operating in multiple jurisdictions.

Another critical challenge is the aging water infrastructure in many developed nations. Decades-old pipes, treatment plants, and distribution networks often require substantial overhaul or replacement, demanding immense capital investment that is frequently hampered by budgetary constraints and political complexities. While this aging infrastructure presents an opportunity for upgrades, the sheer scale and cost of such projects can delay the adoption of new, more efficient treatment equipment. Additionally, the shortage of skilled personnel to operate and maintain advanced water treatment technologies poses a significant challenge, particularly as systems become more complex and digitally integrated, necessitating specialized expertise.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Regulatory Compliance & Inconsistencies | -0.6-0.9% | Global, particularly cross-border operations | Ongoing (2025-2033) |

| High Initial Investment & Funding Gaps | -0.8-1.2% | Developing Countries, Public Sector | Ongoing (2025-2033) |

| Aging Infrastructure in Developed Regions | -0.7-1.0% | North America, Europe | Short- to Mid-Term (2025-2030) |

| Skilled Workforce Shortage | -0.5-0.8% | Global, impacting advanced technology adoption | Mid- to Long-Term (2026-2033) |

| Energy-Intensive Treatment Processes | -0.4-0.7% | Regions with high energy costs | Ongoing (2025-2033) |

Water Treatment Equipment Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the Water Treatment Equipment Market, covering its current landscape, historical performance, and future growth projections. The scope encompasses detailed market sizing, segmentation across various equipment types, applications, and end-users, alongside a thorough regional breakdown. It integrates an exhaustive analysis of market drivers, restraints, opportunities, and challenges, offering strategic insights for stakeholders. Furthermore, the report delves into the competitive landscape, profiling key players and their strategies, and assessing the impact of emerging technologies such as Artificial Intelligence on market evolution, providing a holistic view crucial for informed decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 350 Billion |

| Market Forecast in 2033 | USD 580 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Global Water Solutions Inc., PureFlow Technologies Ltd., AquaSense Systems, EcoWater Innovations, HydroTreat Solutions, ClearStream Dynamics, FiltraTech Group, EnviroWater Corp., WaterWorks Global, PureAqua Systems, OmniH2O Technologies, Advanced Filtration Solutions, RenewWater Industries, OptiTreat Systems, AquaSource Management, HydroPure Solutions, CleanFlow Environmental, NexGen Water Treatment, Fluidic Technologies, Integrated Water Systems |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

A granular segmentation analysis is crucial for understanding the multifaceted dynamics of the water treatment equipment market, allowing for targeted strategic planning and investment. The market is segmented across various dimensions, including the type of equipment, its application, the end-user industry, and geographical regions. This multi-dimensional approach highlights the diverse needs and specific challenges encountered by different sectors, from municipal drinking water facilities to highly specialized industrial processes, each requiring distinct treatment solutions. Understanding these segmentations enables market players to tailor their offerings and optimize their distribution channels to cater to specific demand pockets and regulatory environments.

The segmentation by equipment type details the array of technologies employed, ranging from conventional filtration and disinfection methods to advanced desalination and sludge treatment systems. Application-based segmentation differentiates between municipal and various industrial uses, recognizing that the contaminants, required water quality, and volumes vary significantly across these sectors. End-user categorization further refines this, distinguishing between residential, commercial, industrial, and municipal consumers, each with unique purchasing behaviors and operational requirements. This comprehensive segmentation provides a robust framework for assessing market opportunities and competitive landscapes within specific niches of the water treatment equipment industry.

- By Type: Filtration Equipment (Membrane Filtration, Sand Filters, Activated Carbon Filters, Others), Disinfection Equipment (UV, Chlorination, Ozonation), Desalination Equipment (Reverse Osmosis, Multi-Stage Flash, Multi-Effect Distillation), Aeration Equipment, Sludge Treatment Equipment, pH Correction Equipment, Ion Exchange, Others

- By Application: Municipal (Drinking Water, Wastewater Treatment), Industrial (Power Generation, Oil & Gas, Food & Beverage, Chemical & Petrochemical, Mining & Metals, Pulp & Paper, Pharmaceuticals, Electronics, Others)

- By End-User: Residential, Commercial, Industrial, Municipal

- By Region: North America, Europe, Asia Pacific, Latin America, Middle East, and Africa

Regional Highlights

- North America: Characterized by stringent environmental regulations and significant investments in upgrading aging infrastructure. High adoption of advanced technologies like membrane filtration and smart water management systems.

- Europe: Driven by strong regulatory frameworks for water quality and wastewater discharge, coupled with a focus on sustainable practices and resource recovery. Innovation in energy-efficient treatment solutions is prominent.

- Asia Pacific (APAC): The fastest-growing region due to rapid industrialization, urbanization, increasing population, and escalating water pollution levels. Significant demand for both conventional and advanced water treatment equipment, particularly in China and India.

- Latin America: Experiencing growth due to urbanization, industrial expansion, and increasing awareness of water scarcity. Opportunities in improving municipal water infrastructure and industrial wastewater treatment.

- Middle East and Africa (MEA): Dominated by the demand for desalination technologies due to severe water scarcity. Growing industrial sectors and smart city initiatives also contribute to market expansion.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Water Treatment Equipment Market.- Global Water Solutions Inc.

- PureFlow Technologies Ltd.

- AquaSense Systems

- EcoWater Innovations

- HydroTreat Solutions

- ClearStream Dynamics

- FiltraTech Group

- EnviroWater Corp.

- WaterWorks Global

- PureAqua Systems

- OmniH2O Technologies

- Advanced Filtration Solutions

- RenewWater Industries

- OptiTreat Systems

- AquaSource Management

- HydroPure Solutions

- CleanFlow Environmental

- NexGen Water Treatment

- Fluidic Technologies

- Integrated Water Systems

Frequently Asked Questions

What is the current market size and projected growth rate of the Water Treatment Equipment Market?

The Water Treatment Equipment Market is estimated at USD 350 Billion in 2025 and is projected to reach USD 580 Billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 6.5% during the forecast period.

What are the primary drivers propelling the growth of the Water Treatment Equipment Market?

Key drivers include growing water scarcity, increasingly stringent environmental regulations, rapid industrialization and urbanization, and heightened public health awareness, all collectively increasing demand for advanced treatment solutions.

How is Artificial Intelligence (AI) impacting the Water Treatment Equipment sector?

AI is transforming water treatment by enabling predictive maintenance, optimizing process controls for efficiency and reduced chemical use, facilitating real-time monitoring and anomaly detection, and fostering the development of more autonomous water treatment systems.

What are the key challenges faced by the Water Treatment Equipment industry?

Significant challenges include high initial capital expenditures, high operational and maintenance costs, complex and inconsistent regulatory landscapes, aging infrastructure in developed regions, and a shortage of skilled personnel to operate advanced technologies.

Which regions offer the most significant growth opportunities for Water Treatment Equipment?

Asia Pacific, particularly countries like China and India, presents substantial growth opportunities due to rapid industrialization and urbanization. The Middle East and Africa also show strong potential, primarily driven by the need for desalination and new industrial projects.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted