Water Infrastructure Measurement and Control Market

Water Infrastructure Measurement and Control Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700568 | Last Updated : July 25, 2025 |

Format : ![]()

![]()

![]()

![]()

Water Infrastructure Measurement and Control Market Size

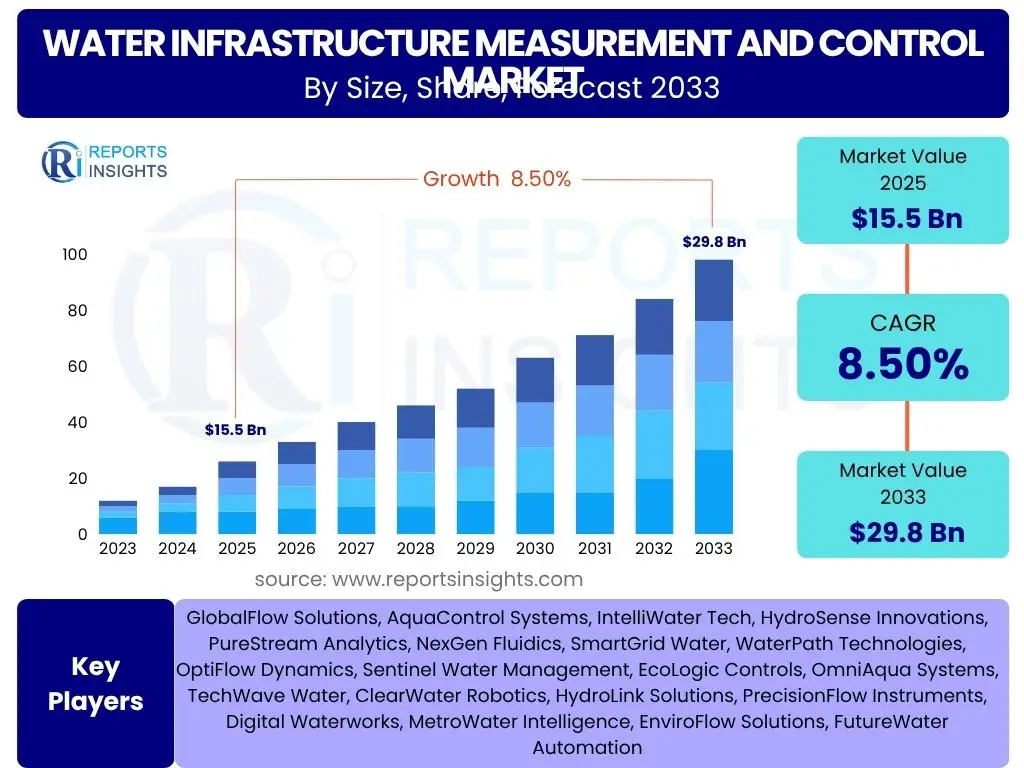

Water Infrastructure Measurement and Control Market is projected to grow at a Compound annual growth rate (CAGR) of 8.5% between 2025 and 2033, reaching an estimated USD 15.5 Billion in 2025 and is projected to grow to USD 29.8 Billion by 2033, marking the end of the forecast period.

Key Water Infrastructure Measurement and Control Market Trends & Insights

The water infrastructure measurement and control market is undergoing significant transformation driven by advancements in technology and increasing global demands. Key trends shaping this market include:

- Integration of advanced Internet of Things (IoT) sensors for real-time data collection.

- Escalating adoption of Artificial Intelligence (AI) and Machine Learning (ML) for predictive analytics and operational optimization.

- Growing focus on smart water solutions and digital twin technologies to enhance system efficiency.

- Increasing investment in leakage detection and pressure management systems to combat water loss.

- Shift towards cloud-based platforms for centralized data management and remote monitoring capabilities.

- Emphasis on sustainable water management practices and resource conservation initiatives globally.

- Rising demand for robust cybersecurity measures to protect critical water infrastructure from digital threats.

AI Impact Analysis on Water Infrastructure Measurement and Control

Artificial Intelligence is profoundly influencing the water infrastructure measurement and control sector by enabling unprecedented levels of operational intelligence and automation. The impact of AI includes:

- Enhanced predictive maintenance capabilities for pumps, pipes, and other critical assets, minimizing downtime.

- Real-time anomaly detection and rapid fault isolation through sophisticated pattern recognition algorithms.

- Optimized water flow and pressure management, leading to significant energy savings and reduced water loss.

- Improved water quality monitoring with AI analyzing complex sensor data for contaminant detection.

- Automated decision-making for reservoir management and distribution network optimization, ensuring efficient resource allocation.

- Predictive modeling for demand forecasting, helping utilities proactively manage supply and prevent shortages.

- Streamlined data analysis from diverse sources, providing actionable insights for strategic planning and capital expenditure.

Key Takeaways Water Infrastructure Measurement and Control Market Size & Forecast

- Significant market growth anticipated from 2025 to 2033, driven by global water challenges and technological advancements.

- Strong CAGR of 8.5% indicates robust expansion across various segments of water management.

- Projected market value of nearly USD 30 billion by 2033 highlights substantial investment potential.

- Technological integration, particularly IoT and AI, is central to future market development and efficiency gains.

- Increased focus on smart solutions, leak detection, and sustainable practices will be paramount for stakeholders.

Water Infrastructure Measurement and Control Market Drivers Analysis

The global water infrastructure measurement and control market is propelled by a confluence of critical factors, primarily stemming from escalating global water crises, the imperative for operational efficiency, and the rapid pace of technological innovation. Aging water infrastructure worldwide necessitates modernization and the integration of advanced measurement and control systems to prevent leaks, reduce non-revenue water, and ensure reliable supply. Furthermore, the increasing global population and rapid urbanization are placing unprecedented stress on existing water resources, driving demand for more efficient and sustainable water management practices. Stringent environmental regulations and growing public awareness regarding water quality and conservation also play a pivotal role, compelling utilities and industrial users to adopt sophisticated monitoring and control solutions. The advent of smart city initiatives, which often integrate smart water grids, provides a significant ecosystem for the deployment and expansion of these technologies, further accelerating market growth.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Aging Water Infrastructure Modernization | +2.1% | North America, Europe | Medium to Long Term |

| Increasing Water Scarcity and Population Growth | +1.8% | Asia Pacific, Middle East & Africa | Long Term |

| Stringent Environmental Regulations & Standards | +1.5% | Europe, North America | Short to Medium Term |

| Smart City Initiatives and Digital Transformation | +1.4% | Global (Emerging Economies) | Medium Term |

| Rising Industrial and Agricultural Water Demand | +1.2% | Asia Pacific, Latin America | Long Term |

Water Infrastructure Measurement and Control Market Restraints Analysis

Despite significant growth drivers, the water infrastructure measurement and control market faces several formidable restraints that could impede its full potential. The substantial upfront capital investment required for implementing advanced measurement and control systems is a major barrier, particularly for smaller municipalities or utilities with limited budgets. The complexity involved in integrating these new technologies with legacy infrastructure poses significant technical and operational challenges, often leading to prolonged deployment times and increased costs. Furthermore, the critical nature of water infrastructure makes it a prime target for cyber threats, and concerns over data security and privacy can deter adoption. A prevailing shortage of skilled personnel capable of managing, maintaining, and analyzing data from these sophisticated systems also limits market expansion, especially in regions with developing technical expertise. Finally, the fragmented nature of the water utility sector, with numerous small and medium-sized operators, can hinder widespread standardization and adoption of advanced solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment | -1.9% | Developing Regions, Municipalities | Short to Medium Term |

| Integration Challenges with Legacy Infrastructure | -1.7% | North America, Europe | Medium Term |

| Cybersecurity Concerns and Data Privacy | -1.5% | Global | Short to Long Term |

| Shortage of Skilled Workforce | -1.3% | Global, Particularly Asia Pacific | Long Term |

| Regulatory Hurdles and Bureaucracy | -1.0% | Varies by Country | Short to Medium Term |

Water Infrastructure Measurement and Control Market Opportunities Analysis

The water infrastructure measurement and control market presents numerous promising opportunities for growth and innovation. The increasing global emphasis on sustainable water management and resource conservation initiatives creates a fertile ground for advanced solutions that minimize waste and optimize usage. The rapid adoption of cloud computing and advanced analytics platforms allows for more centralized, real-time data processing and decision-making, opening new avenues for efficiency and service delivery. Emerging markets, characterized by rapid urbanization and the need for new infrastructure development, offer significant untapped potential for deploying modern water measurement and control systems from the ground up. Furthermore, the development of Water-as-a-Service (WaaS) models, where technology providers offer comprehensive solutions rather than just products, can lower the barrier to entry for utilities and accelerate adoption. Finally, retrofitting existing, often outdated, water infrastructure with smart measurement and control technologies represents a substantial and ongoing opportunity across developed economies.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Advancements in Data Analytics and Cloud Computing | +2.0% | Global | Short to Medium Term |

| Expansion into Smart Agriculture Solutions | +1.7% | Asia Pacific, Latin America | Medium to Long Term |

| Rise of Water-as-a-Service (WaaS) Models | +1.5% | North America, Europe | Medium Term |

| Retrofitting Existing Infrastructure | +1.3% | Developed Economies (e.g., US, Germany) | Long Term |

| Growing Emphasis on Non-Revenue Water Reduction | +1.1% | Global, Particularly Developing Nations | Short to Medium Term |

Water Infrastructure Measurement and Control Market Challenges Impact Analysis

The water infrastructure measurement and control market, while promising, contends with significant challenges that necessitate strategic navigation. One primary challenge is the lack of standardized protocols and interoperability between various measurement devices, control systems, and data platforms, making seamless integration difficult and costly. The ever-present threat of cyberattacks on critical infrastructure demands continuous investment in robust security measures, adding to operational expenses and requiring specialized expertise. Additionally, the rapid pace of technological innovation can lead to technological obsolescence, meaning systems installed today might be outdated in a few years, requiring constant upgrades. Public-private partnership complexities, including funding issues, regulatory hurdles, and risk allocation, can impede large-scale project deployments. Finally, resistance to change within traditional utility operational models, often characterized by a conservative approach to technology adoption, slows down the implementation of new, efficient measurement and control solutions. Overcoming these challenges will be crucial for the sustained growth and wider adoption of these technologies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Data Interoperability and Standardization Issues | -1.8% | Global | Medium to Long Term |

| Escalating Cybersecurity Threats | -1.6% | Global | Short to Long Term |

| Technological Obsolescence and Upgrade Costs | -1.4% | Developed Economies | Medium Term |

| Complexities in Public-Private Partnerships | -1.2% | Varies by Country | Long Term |

| Resistance to Change and Traditional Mindsets | -0.9% | Mature Markets | Long Term |

Water Infrastructure Measurement and Control Market - Updated Report Scope

This comprehensive report delves into the intricate dynamics of the Water Infrastructure Measurement and Control Market, offering an updated scope that captures the latest trends, technological advancements, and market projections. It provides a detailed analysis of market size, growth drivers, restraints, opportunities, and challenges, segmented across various components, applications, technologies, and end-users. The report also highlights regional market performance and profiles key industry players, offering a holistic view for stakeholders seeking strategic insights and competitive intelligence.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 15.5 Billion |

| Market Forecast in 2033 | USD 29.8 Billion |

| Growth Rate | 8.5% CAGR from 2025 to 2033 |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | GlobalFlow Solutions, AquaControl Systems, IntelliWater Tech, HydroSense Innovations, PureStream Analytics, NexGen Fluidics, SmartGrid Water, WaterPath Technologies, OptiFlow Dynamics, Sentinel Water Management, EcoLogic Controls, OmniAqua Systems, TechWave Water, ClearWater Robotics, HydroLink Solutions, PrecisionFlow Instruments, Digital Waterworks, MetroWater Intelligence, EnviroFlow Solutions, FutureWater Automation |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Water Infrastructure Measurement and Control Market is meticulously segmented to provide a granular view of its diverse landscape, enabling a comprehensive understanding of various market facets. This segmentation allows for targeted analysis of specific product categories, application areas, technological adoptions, and end-user demands, offering invaluable insights for strategic planning and investment decisions. Each segment plays a crucial role in the overall market ecosystem, reflecting the varied needs and technological maturity across different parts of the water management value chain.

By Component: This segment includes the essential hardware and software elements forming the backbone of water infrastructure measurement and control systems. Sensors are fundamental, encompassing devices that measure parameters like flow, pressure, level, and water quality. Meters, including smart meters, electromagnetic, and ultrasonic types, are critical for accurate consumption and flow measurement. Controllers like PLCs (Programmable Logic Controllers), RTUs (Remote Terminal Units), and DCS (Distributed Control Systems) process data and manage operations. Software solutions, such as SCADA (Supervisory Control and Data Acquisition), HMI (Human-Machine Interface), advanced analytics, and asset management systems, provide the intelligence and interface for managing complex networks. Communication systems, both wireless and wired, facilitate data transmission, while actuators enable physical control over valves and pumps. This granular breakdown helps in understanding the technological complexity and interconnectedness of modern water systems.

By Application: This segmentation focuses on the diverse operational areas where water infrastructure measurement and control technologies are deployed. Water treatment applications involve monitoring and controlling processes to ensure water purity and safety. Water distribution applications concentrate on efficient delivery and network management, including pressure regulation. Wastewater collection and wastewater treatment are crucial for environmental protection, requiring precise measurement and control of discharge and treatment processes. Leak detection and pressure management are vital for reducing non-revenue water and preserving resources. Quality monitoring ensures compliance with health and environmental standards. Each application area has specific requirements for measurement accuracy and control responsiveness, driving distinct market demands.

By End-User: This segment categorizes the primary beneficiaries and implementers of water infrastructure measurement and control solutions. The municipal sector is a dominant end-user, encompassing residential, commercial, and public water utilities responsible for potable water supply and wastewater services. The industrial sector includes various industries such as manufacturing, power generation, chemical processing, and food & beverage, each with unique water requirements for production, cooling, or waste discharge. The agricultural sector increasingly utilizes these technologies for efficient irrigation, water resource management, and crop yield optimization, especially in regions facing water scarcity. Understanding end-user specific needs helps in tailoring solutions and market approaches.

By Technology: This segment highlights the advanced technological underpinnings driving innovation and efficiency in the market. Internet of Things (IoT) integration enables ubiquitous connectivity and real-time data collection from distributed sensors and devices. Artificial Intelligence (AI) and Machine Learning (ML) are pivotal for predictive analytics, anomaly detection, optimization, and automated decision-making. Cloud computing provides scalable infrastructure for data storage, processing, and remote access, facilitating centralized management. Geographic Information Systems (GIS) offer spatial data analysis and visualization, crucial for network mapping and asset management. Digital Twins create virtual replicas of physical infrastructure, enabling simulations, predictive modeling, and optimized operations. These technologies collectively enhance the intelligence, efficiency, and resilience of water systems.

Regional Highlights

The Water Infrastructure Measurement and Control Market exhibits diverse growth patterns and adoption rates across different geographical regions, influenced by varying regulatory landscapes, economic development stages, and existing infrastructure conditions.- North America: This region stands as a significant market, primarily driven by the imperative to upgrade aging infrastructure and the early adoption of advanced technologies. Countries like the United States and Canada are witnessing substantial investments in smart water initiatives, including smart meters, advanced leak detection systems, and integrated data analytics platforms. Strict environmental regulations and a strong emphasis on operational efficiency further bolster market growth. The presence of key technology providers and ongoing research and development activities contribute to its leading position.

- Europe: Europe is a mature but highly innovative market, characterized by stringent environmental regulations, a strong focus on water conservation, and widespread smart city development. Countries such as Germany, the UK, and the Netherlands are at the forefront of implementing intelligent water networks and digital twin technologies. The region prioritizes reducing non-revenue water and improving water quality through advanced measurement and control solutions. Collaborative initiatives and supportive government policies play a crucial role in market expansion.

- Asia Pacific (APAC): The APAC region is projected to be the fastest-growing market, propelled by rapid urbanization, industrialization, and significant investments in new water infrastructure development. Countries like China, India, and Australia are facing increasing water scarcity and pollution challenges, driving the demand for efficient water management solutions. Government initiatives to develop smart cities and improve water supply reliability are creating vast opportunities for advanced measurement and control technologies. The sheer scale of population and economic growth ensures sustained market expansion.

- Latin America: This region is an emerging market with substantial growth potential, driven by the need for improved water and wastewater infrastructure and efficient resource management. Countries such as Brazil and Mexico are investing in modernizing their water utilities to address issues like water loss, unreliable supply, and inadequate sanitation. While facing challenges related to funding and political stability, the increasing awareness of water conservation and the adoption of basic automation solutions are fostering market development.

- Middle East and Africa (MEA): The MEA region presents unique opportunities due to severe water scarcity issues, particularly in the Gulf Cooperation Council (GCC) countries, and ongoing large-scale infrastructure projects. Investments in desalination plants and efficient water distribution networks are driving the adoption of advanced measurement and control systems. Countries like Saudi Arabia, UAE, and South Africa are focusing on developing resilient water infrastructure to ensure long-term water security. While still in early stages for some areas, the critical need for water resources is a strong market driver.

Top Key Players:

The market research report covers the analysis of key stake holders of the Water Infrastructure Measurement and Control Market. Some of the leading players profiled in the report include -- GlobalFlow Solutions

- AquaControl Systems

- IntelliWater Tech

- HydroSense Innovations

- PureStream Analytics

- NexGen Fluidics

- SmartGrid Water

- WaterPath Technologies

- OptiFlow Dynamics

- Sentinel Water Management

- EcoLogic Controls

- OmniAqua Systems

- TechWave Water

- ClearWater Robotics

- HydroLink Solutions

- PrecisionFlow Instruments

- Digital Waterworks

- MetroWater Intelligence

- EnviroFlow Solutions

- FutureWater Automation

Frequently Asked Questions:

What is the Water Infrastructure Measurement and Control Market?

The Water Infrastructure Measurement and Control Market encompasses the technologies, systems, and services used to monitor, measure, and manage various parameters within water and wastewater networks. This includes sensors, meters, controllers, software (like SCADA and analytics platforms), and communication systems designed to optimize water treatment, distribution, collection, and quality, ensuring efficiency, reducing losses, and enhancing overall system reliability.What are the primary drivers of growth for this market?

The market's growth is primarily driven by the global need to modernize aging water infrastructure, increasing water scarcity due to population growth and climate change, stringent environmental regulations requiring better water quality and discharge management, and the widespread adoption of smart city initiatives that integrate intelligent water grids. The demand for operational efficiency and reduced non-revenue water also significantly contributes to market expansion.How does AI impact water infrastructure measurement and control?

Artificial intelligence (AI) profoundly impacts this market by enabling advanced predictive maintenance, real-time anomaly detection, and optimized resource allocation. AI algorithms analyze vast datasets from sensors to forecast demand, detect leaks, identify potential equipment failures before they occur, and manage water flow and pressure more efficiently, leading to significant cost savings and improved service delivery.Which regions are leading in the adoption of these technologies?

North America and Europe are leading regions in the adoption of water infrastructure measurement and control technologies, driven by aging infrastructure upgrade needs, stringent regulations, and strong commitments to smart water initiatives. Asia Pacific is emerging as the fastest-growing market, propelled by rapid urbanization and significant new infrastructure investments, particularly in countries facing severe water stress.What are the key challenges faced by the Water Infrastructure Measurement and Control Market?

Key challenges include the high initial capital investment required for implementation, complexities in integrating new technologies with existing legacy systems, growing cybersecurity threats targeting critical water infrastructure, and a persistent shortage of skilled personnel to manage and operate sophisticated systems. Data interoperability issues and resistance to change within traditional utility models also pose significant hurdles.| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted