Water and Wastewater Pipe Market

Water and Wastewater Pipe Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_705160 | Last Updated : August 11, 2025 |

Format : ![]()

![]()

![]()

![]()

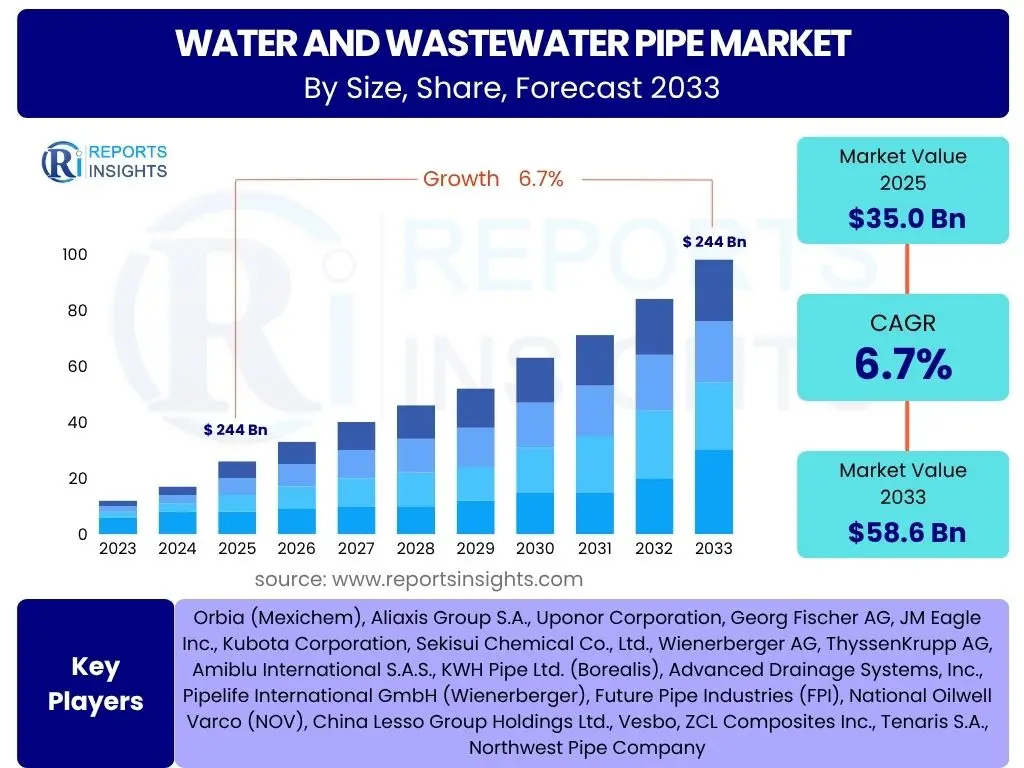

Water and Wastewater Pipe Market Size

According to Reports Insights Consulting Pvt Ltd, The Water and Wastewater Pipe Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.7% between 2025 and 2033. The market is estimated at USD 35.0 billion in 2025 and is projected to reach USD 58.6 billion by the end of the forecast period in 2033.

Key Water and Wastewater Pipe Market Trends & Insights

The Water and Wastewater Pipe market is currently shaped by several transformative trends, driven by global urbanization, aging infrastructure, and increasing environmental concerns. A significant trend involves the adoption of advanced materials such as high-density polyethylene (HDPE) and polyvinyl chloride (PVC) due to their durability, corrosion resistance, and ease of installation, gradually replacing traditional materials like cast iron and concrete. Furthermore, there is a growing emphasis on smart water infrastructure, incorporating sensors and IoT devices for real-time monitoring of pipe integrity, leak detection, and efficient water management, which is crucial for reducing water loss and optimizing operational efficiency.

Another key insight highlights the expanding application of trenchless technologies for pipe installation and rehabilitation. These methods, including horizontal directional drilling (HDD) and pipe bursting, minimize disruption to urban environments and reduce construction time and costs, addressing challenges associated with conventional open-cut methods. Additionally, the market is experiencing increased investment in water reuse and recycling projects, particularly in water-stressed regions, necessitating new and specialized piping systems. This shift is also influencing demand for sustainable and recyclable pipe materials, aligning with global efforts towards circular economy principles and resource conservation.

- Shift towards advanced materials like HDPE and PVC.

- Integration of smart technologies and IoT for network monitoring.

- Rising adoption of trenchless pipe installation and rehabilitation.

- Increased focus on water reuse and recycling infrastructure.

- Growing demand for sustainable and recyclable pipe solutions.

- Emphasis on leakage detection and reduction strategies.

AI Impact Analysis on Water and Wastewater Pipe

The Water and Wastewater Pipe sector is increasingly recognizing the transformative potential of Artificial intelligence (AI) to address longstanding challenges such as aging infrastructure, water loss, and operational inefficiencies. Common user questions revolve around how AI can enhance predictive maintenance, improve leak detection accuracy, and optimize overall network management. AI-powered algorithms are being deployed to analyze vast datasets from sensors, flow meters, and historical maintenance records, enabling utilities to identify patterns, predict potential failures, and schedule proactive repairs before major issues escalate. This shift from reactive to predictive maintenance significantly reduces operational costs, minimizes service disruptions, and extends the lifespan of critical infrastructure.

Beyond predictive maintenance, AI is revolutionizing leak detection by processing acoustic data, satellite imagery, and pressure readings to pinpoint leaks with unprecedented accuracy, thereby conserving precious water resources. Generative AI models are also being explored for optimizing pipe network designs, simulating various scenarios for resilience against climate change impacts, and forecasting water demand more precisely. Furthermore, AI contributes to enhanced water quality monitoring by analyzing chemical and biological data in real-time, ensuring compliance with health standards. The integration of AI is poised to make water infrastructure more resilient, efficient, and sustainable, fundamentally altering how water and wastewater systems are managed and maintained globally.

- Predictive maintenance using AI for proactive pipe repair and replacement.

- Enhanced leak detection through AI analysis of acoustic, pressure, and imagery data.

- Optimization of water distribution networks and pumping stations.

- Real-time water quality monitoring and anomaly detection.

- Improved demand forecasting and resource allocation.

- Automation of inspection processes using AI-powered robotics.

Key Takeaways Water and Wastewater Pipe Market Size & Forecast

The Water and Wastewater Pipe market is poised for robust expansion, driven primarily by the escalating demand for reliable water infrastructure globally. User inquiries often center on the primary factors propelling this growth and identifying the most promising investment areas. A significant takeaway is the critical role of aging infrastructure replacement and rehabilitation, particularly in developed economies, where decades-old pipes are failing and leading to substantial water losses and environmental concerns. This necessitates continuous investment in upgrading existing networks, creating a stable baseline demand for various pipe materials and technologies.

Another crucial insight is the impact of rapid urbanization and industrialization, especially across emerging economies in Asia Pacific and Latin America. These regions require extensive new infrastructure development to support growing populations and industrial activities, leading to high demand for new pipe installations for potable water supply and wastewater collection. The market forecast highlights a consistent growth trajectory, underscoring the indispensable nature of water and wastewater systems. Furthermore, the increasing focus on water conservation and sustainable water management practices worldwide will continue to stimulate innovation in pipe materials, smart technologies, and efficient installation methods, ensuring long-term market vitality and attractiveness for stakeholders.

- Significant growth attributed to aging infrastructure replacement.

- Strong demand from rapid urbanization and industrial expansion in developing regions.

- Sustained investments in new water and wastewater infrastructure projects globally.

- Increasing adoption of advanced materials and smart technologies for efficiency.

- Focus on water conservation driving demand for leak-proof and durable piping.

- Resilient market demand due to essential nature of water utility services.

Water and Wastewater Pipe Market Drivers Analysis

The growth of the Water and Wastewater Pipe market is fundamentally driven by an array of global and regional factors that necessitate robust and expanded infrastructure. Population growth and urbanization, particularly in emerging economies, are exerting immense pressure on existing water supply and sanitation systems, requiring extensive new piping networks to accommodate increased demand. Concurrently, the aging water infrastructure in developed nations, often decades or even a century old, is a critical driver for replacement and rehabilitation projects aimed at reducing water loss, preventing pipe failures, and ensuring public health and safety. Governments worldwide are responding to these challenges with significant investments and regulatory frameworks to modernize water treatment and distribution systems.

Furthermore, heightened environmental concerns and the imperative for water conservation are pushing for more efficient and leak-proof piping solutions. Climate change impacts, such as prolonged droughts and increased frequency of extreme weather events, further emphasize the need for resilient and adaptable water infrastructure. Industrial development and expansion also contribute significantly, as industries require large volumes of water for their processes and generate wastewater that needs efficient collection and treatment, driving demand for specialized pipe materials and systems. The cumulative effect of these drivers creates a sustained and growing need for advanced and durable water and wastewater pipe solutions globally.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Aging Infrastructure Replacement | +0.8% | North America, Europe, Oceania | 2025-2033 |

| Population Growth & Urbanization | +0.7% | Asia Pacific, Africa, Latin America | 2025-2033 |

| Government Investments & Regulations | +0.6% | Global, particularly developed nations | 2025-2033 |

| Increasing Water Scarcity & Conservation Efforts | +0.5% | Global, especially arid regions | 2025-2033 |

| Industrial Development | +0.4% | Asia Pacific, Latin America, Middle East | 2025-2033 |

Water and Wastewater Pipe Market Restraints Analysis

Despite the strong growth drivers, the Water and Wastewater Pipe market faces several notable restraints that can impede its expansion. One primary concern is the substantial capital investment required for new infrastructure projects and the extensive rehabilitation of existing networks. The high upfront costs associated with materials, installation, and labor can lead to project delays or cancellations, particularly in regions with limited public funding or private sector participation. Moreover, complex and fragmented regulatory frameworks across different countries and regions can create bureaucratic hurdles, prolonging project timelines and increasing compliance costs for manufacturers and service providers. This regulatory landscape often necessitates adherence to varied standards and specifications, adding to operational complexities.

Another significant restraint is the volatility in raw material prices, especially for petroleum-derived plastics (like PVC and PE) and metals (like iron and steel). Fluctuations in these commodity prices directly impact the manufacturing costs of pipes, leading to unpredictable project budgets and potentially squeezing profit margins for market players. Furthermore, the shortage of skilled labor for pipe installation, maintenance, and the operation of advanced water management systems poses a challenge, particularly in regions experiencing an aging workforce or lacking specialized training programs. Environmental concerns related to the disposal of old pipe materials and the carbon footprint associated with manufacturing and transportation also present long-term challenges, driving the need for more sustainable, albeit potentially costlier, solutions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Capital Investment & Funding Gaps | -0.7% | Global, especially developing nations | 2025-2033 |

| Raw Material Price Volatility | -0.5% | Global | 2025-2033 |

| Complex Regulatory Frameworks | -0.4% | Europe, North America | 2025-2033 |

| Skilled Labor Shortages | -0.3% | Global, particularly developed economies | 2025-2033 |

| Environmental Regulations on Production & Disposal | -0.2% | Europe, North America, parts of Asia | 2025-2033 |

Water and Wastewater Pipe Market Opportunities Analysis

Significant opportunities exist within the Water and Wastewater Pipe market, primarily driven by technological advancements and evolving infrastructure needs. One major area of growth lies in the increasing adoption of smart water infrastructure solutions. The integration of sensors, IoT, and AI for real-time monitoring, leak detection, and predictive maintenance of pipe networks presents a lucrative avenue for market participants. These technologies enable utilities to optimize operations, reduce water losses, and extend asset lifecycles, offering a compelling value proposition that encourages investment in upgraded piping systems capable of integrating such smart components. The drive towards digital transformation in utility management provides a substantial long-term growth trajectory.

Another burgeoning opportunity is the expanding market for trenchless technologies. As urban areas become denser and the costs and disruptions associated with traditional open-cut methods escalate, trenchless pipe rehabilitation and installation techniques offer a more efficient, less invasive, and often more cost-effective alternative. This includes methods like pipe bursting, sliplining, and horizontal directional drilling, which are gaining traction globally. Furthermore, the global push for sustainability is creating demand for innovative, eco-friendly pipe materials, such as recycled plastics, bio-based polymers, and composite materials that offer enhanced durability and reduced environmental footprints. Public-Private Partnerships (PPPs) are also emerging as a viable funding model, especially in developing countries, allowing for accelerated infrastructure development and providing new avenues for market participation by private entities, fostering innovation and efficiency in project execution.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Smart Water Infrastructure & IoT Integration | +0.9% | North America, Europe, Developed Asia Pacific | 2025-2033 |

| Trenchless Technology Adoption | +0.8% | Global, especially urban areas | 2025-2033 |

| Sustainable & Eco-Friendly Pipe Materials | +0.7% | Europe, North America, Asia Pacific | 2025-2033 |

| Public-Private Partnerships (PPPs) | +0.6% | Developing Economies, Global | 2025-2033 |

| Water Reuse & Recycling Projects | +0.5% | Arid Regions, Densely Populated Areas | 2025-2033 |

Water and Wastewater Pipe Market Challenges Impact Analysis

The Water and Wastewater Pipe market, while poised for growth, navigates several significant challenges that can affect its trajectory and operational efficiency. One of the primary challenges is securing adequate funding for large-scale infrastructure projects, especially given the extensive investment required for pipe replacement and new network development. Many municipalities and governments face budget constraints, leading to deferred maintenance and slow project initiation, which in turn exacerbates the problem of aging infrastructure and can delay market growth. The complexity and long payback periods of water infrastructure projects often deter private investment, necessitating creative financing models and strong government backing.

Another considerable challenge stems from the increasing impact of climate change, including extreme weather events like floods and prolonged droughts. These events can severely damage pipe networks, requiring emergency repairs and resilient new installations, but also create unpredictable demand cycles and strain resources. Additionally, supply chain disruptions, as seen in recent years, can lead to material shortages and price increases, impacting manufacturing and project timelines. Cybersecurity threats to increasingly smart and interconnected water infrastructure systems also pose a growing concern, as breaches could compromise operational integrity and public safety, requiring significant investment in robust security measures. Finally, public resistance to tariff increases, which are often necessary to fund infrastructure upgrades, can further complicate financing and project approvals, slowing down essential improvements and the adoption of new technologies.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Funding Shortfalls & Budget Constraints | -0.8% | Global | 2025-2033 |

| Climate Change Impacts & Resilient Infrastructure | -0.6% | Global, especially vulnerable regions | 2025-2033 |

| Supply Chain Disruptions & Material Availability | -0.5% | Global | 2025-2033 |

| Cybersecurity Threats to Smart Water Systems | -0.4% | Developed Economies | 2025-2033 |

| Public Acceptance & Tariff Increases | -0.3% | Global | 2025-2033 |

Water and Wastewater Pipe Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Water and Wastewater Pipe market, offering a detailed overview of market dynamics, growth drivers, restraints, opportunities, and challenges across various segments and key geographical regions. It includes historical data, current market estimations, and future projections to provide a holistic view of the industry landscape. The study covers key market trends, the impact of emerging technologies like AI, and strategic insights for market participants, aiming to equip stakeholders with actionable intelligence for informed decision-making.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 35.0 billion |

| Market Forecast in 2033 | USD 58.6 billion |

| Growth Rate | 6.7% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Orbia (Mexichem), Aliaxis Group S.A., Uponor Corporation, Georg Fischer AG, JM Eagle Inc., Kubota Corporation, Sekisui Chemical Co., Ltd., Wienerberger AG, ThyssenKrupp AG, Amiblu International S.A.S., KWH Pipe Ltd. (Borealis), Advanced Drainage Systems, Inc., Pipelife International GmbH (Wienerberger), Future Pipe Industries (FPI), National Oilwell Varco (NOV), China Lesso Group Holdings Ltd., Vesbo, ZCL Composites Inc., Tenaris S.A., Northwest Pipe Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Water and Wastewater Pipe market is meticulously segmented to provide a granular understanding of its diverse components and their respective growth dynamics. These segmentations allow for a detailed examination of market performance based on material type, enabling insights into the dominance of specific polymers or metals and their suitability for various applications. The application-based segmentation helps delineate demand from potable water networks versus wastewater management systems, reflecting distinct infrastructure requirements and investment priorities. Furthermore, segmenting by pipe diameter sheds light on the demand for different pipe sizes, ranging from small distribution lines to large transmission mains, critical for urban and rural development projects.

The end-use segmentation provides a clear picture of demand from different sectors, including municipal, industrial, commercial, and residential, each with unique needs and purchasing patterns. This comprehensive segmentation framework is crucial for identifying niche markets, understanding competitive landscapes, and formulating targeted strategies. By analyzing each segment in detail, stakeholders can better understand market opportunities, allocate resources effectively, and develop products and services that cater to specific market requirements, contributing to overall market growth and efficiency.

- By Material: PVC (Polyvinyl Chloride), PE (Polyethylene), Ductile Iron, Concrete, Steel, Fiberglass, Composite, Other Materials

- By Application: Potable Water Distribution, Wastewater Collection, Stormwater Drainage, Irrigation, Industrial Use

- By Diameter: Small Diameter (Up to 12 inches), Medium Diameter (12-36 inches), Large Diameter (Above 36 inches)

- By End-Use: Municipal, Industrial, Commercial, Residential

Regional Highlights

- North America: This region is characterized by an urgent need for infrastructure upgrades due to aging water and wastewater networks. Significant investments are directed towards replacing old pipes and adopting trenchless technologies to minimize disruption. The focus is also on smart water systems for leak detection and efficient management.

- Europe: Driven by stringent environmental regulations and a strong emphasis on water quality, Europe is a mature market focusing on rehabilitation and modernization. Adoption of sustainable materials and advanced technologies for leakage reduction and water reuse is prominent, alongside cross-border infrastructure projects.

- Asia Pacific (APAC): APAC is projected to be the fastest-growing market due to rapid urbanization, industrialization, and population growth. Countries like China, India, and Southeast Asian nations are investing heavily in new infrastructure to meet increasing demand for water supply and sanitation, driving massive new pipe installations.

- Latin America: This region presents considerable growth potential due to ongoing efforts to expand access to clean water and sanitation services, particularly in rural and underserved areas. Government initiatives and international funding aim to bridge the infrastructure gap, leading to sustained demand for pipes.

- Middle East and Africa (MEA): Marked by severe water scarcity and ambitious development projects, MEA is investing in desalination plants, long-distance water transmission pipelines, and modern wastewater treatment facilities. Climate change adaptation and efficient water management are critical drivers for pipe market growth in this region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Water and Wastewater Pipe Market.- Orbia (Mexichem)

- Aliaxis Group S.A.

- Uponor Corporation

- Georg Fischer AG

- JM Eagle Inc.

- Kubota Corporation

- Sekisui Chemical Co., Ltd.

- Wienerberger AG

- ThyssenKrupp AG

- Amiblu International S.A.S.

- KWH Pipe Ltd. (Borealis)

- Advanced Drainage Systems, Inc.

- Pipelife International GmbH (Wienerberger)

- Future Pipe Industries (FPI)

- National Oilwell Varco (NOV)

- China Lesso Group Holdings Ltd.

- Vesbo

- ZCL Composites Inc.

- Tenaris S.A.

- Northwest Pipe Company

Frequently Asked Questions

Analyze common user questions about the Water and Wastewater Pipe market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current market size of the Water and Wastewater Pipe industry?

The Water and Wastewater Pipe market is estimated at USD 35.0 billion in 2025, with projections indicating significant growth to USD 58.6 billion by 2033, driven by global infrastructure needs.

What are the primary factors driving the growth of the Water and Wastewater Pipe market?

Key drivers include aging infrastructure replacement, rapid urbanization and population growth, increasing government investments in water management, industrial development, and growing concerns over water scarcity and conservation.

How is technology, especially AI, impacting the Water and Wastewater Pipe sector?

AI is transforming the sector by enabling predictive maintenance, enhancing leak detection accuracy, optimizing network operations, and improving water quality monitoring, leading to more efficient and resilient water infrastructure.

Which regions are leading the demand for Water and Wastewater Pipes?

Asia Pacific is the fastest-growing region due to extensive new infrastructure development. North America and Europe are significant markets driven by ongoing rehabilitation and modernization of existing networks.

What are the major challenges faced by the Water and Wastewater Pipe market?

Challenges include high capital investment requirements, volatility in raw material prices, complex regulatory frameworks, skilled labor shortages, and the increasing impact of climate change on infrastructure resilience.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted