Warehouse and Storage Market

Warehouse and Storage Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708277 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

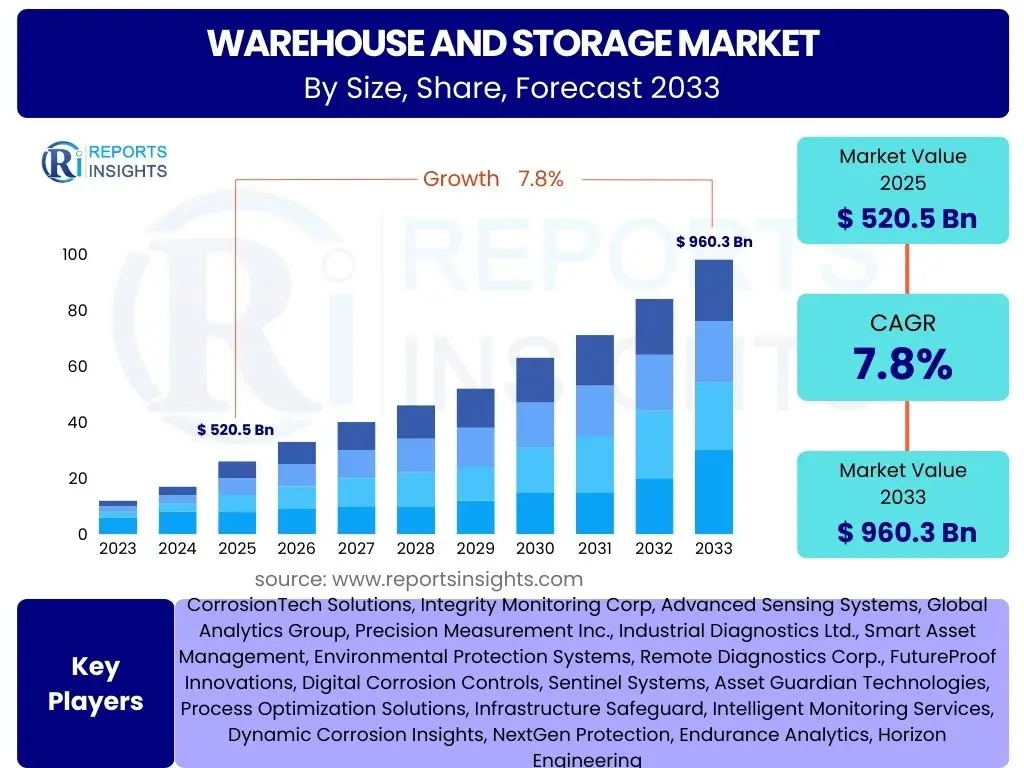

Warehouse and Storage Market Size

According to Reports Insights Consulting Pvt Ltd, The Warehouse and Storage Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 7.8% between 2025 and 2033. The market is estimated at USD 520.5 billion in 2025 and is projected to reach USD 960.3 billion by the end of the forecast period in 2033. This growth trajectory is underpinned by evolving global trade dynamics, the exponential expansion of e-commerce, and increasing demand for sophisticated supply chain solutions. The market's expansion reflects a critical need for efficient and resilient infrastructure to support modern distribution networks.

The substantial market valuation in 2025, exceeding half a trillion US dollars, highlights the foundational role that warehouse and storage facilities play in the global economy. As economies become more interconnected and consumer expectations for rapid delivery intensify, the demand for advanced warehousing capabilities, including temperature-controlled storage, automated facilities, and strategic urban distribution centers, continues to surge. This foundational demand is a primary driver behind the consistent and robust growth forecast through 2033.

Key Warehouse and Storage Market Trends & Insights

Users frequently inquire about the transformative forces shaping the warehouse and storage sector, seeking to understand how new technologies and shifting market demands are influencing operational strategies and investment priorities. A dominant theme revolves around the integration of automation and data analytics to enhance efficiency and decision-making. There is also significant interest in sustainable practices and the evolving role of warehousing in supporting direct-to-consumer fulfillment and resilient supply chains. Furthermore, the convergence of physical and digital infrastructure, often termed "phygital," is a key area of discussion, as operators strive for seamless integration across their networks.

The market is experiencing a profound shift towards intelligent and adaptive storage solutions, moving beyond mere physical space provision. Stakeholders are increasingly focused on optimizing every aspect of warehouse operations, from inbound logistics to outbound distribution, to meet stringent service level agreements and mitigate disruptions. This includes a growing emphasis on predictive maintenance, real-time inventory visibility, and flexible storage models that can scale with fluctuating demand. The imperative to reduce operational costs while improving service quality is driving innovation across the board, resulting in more sophisticated and integrated warehouse management ecosystems.

- Automation and Robotics Integration: Significant adoption of autonomous mobile robots (AMRs), automated guided vehicles (AGVs), and robotic picking systems to enhance operational efficiency, reduce labor dependency, and improve throughput.

- Data Analytics and Predictive Intelligence: Leveraging big data, AI, and machine learning to optimize inventory placement, forecast demand, streamline routing, and identify operational bottlenecks proactively.

- E-commerce Fulfillment Specialization: Development of purpose-built warehouses and micro-fulfillment centers designed to support rapid, direct-to-consumer delivery and handle high volumes of diverse SKUs.

- Sustainability and Green Warehousing: Growing emphasis on energy-efficient designs, renewable energy sources, waste reduction, and sustainable logistics practices to reduce environmental impact and operational costs.

- Flexible and On-Demand Warehousing: Emergence of flexible storage solutions, including shared warehousing models and on-demand space provisioning, to adapt to fluctuating market demands and seasonal peaks.

AI Impact Analysis on Warehouse and Storage

Common user questions regarding AI's impact on warehouse and storage typically center on how artificial intelligence can optimize operational workflows, enhance decision-making, and address labor challenges. There is considerable interest in AI's role in automating complex tasks, improving predictive capabilities for inventory and demand, and enabling more intelligent resource allocation. Concerns often include the initial investment costs, the complexity of integration with existing systems, and the potential impact on the workforce. Users are eager to understand tangible benefits such as cost reduction, efficiency gains, and improved customer satisfaction that AI technologies can deliver within the warehousing ecosystem.

The integration of AI into warehouse and storage operations is rapidly transforming the sector, pushing the boundaries of what is possible in terms of efficiency, accuracy, and responsiveness. AI algorithms are proving instrumental in tasks ranging from optimizing storage layouts and picking routes to managing complex inventory profiles and predicting equipment maintenance needs. This technological shift not only streamlines existing processes but also unlocks new capabilities, allowing warehouses to operate more autonomously and adaptively. As the technology matures and becomes more accessible, its pervasive influence is expected to redefine the competitive landscape, making AI proficiency a critical differentiator for market participants.

- Enhanced Inventory Management: AI-driven systems provide real-time inventory visibility, optimize stock levels, minimize obsolescence, and facilitate dynamic slotting based on demand patterns.

- Predictive Maintenance: AI algorithms analyze data from warehouse equipment to predict potential failures, enabling proactive maintenance and minimizing costly downtime.

- Optimized Routing and Picking: AI powers efficient route planning for human pickers and autonomous robots, reducing travel time and improving order fulfillment speed and accuracy.

- Demand Forecasting: Advanced AI models leverage historical data, seasonal trends, and external factors to generate highly accurate demand forecasts, informing purchasing and storage strategies.

- Automated Quality Control: AI-enabled vision systems can automatically inspect goods for damage or defects, ensuring product quality and reducing human error in the receiving and shipping processes.

- Robotics and Automation Orchestration: AI serves as the brain for managing and coordinating fleets of robots, AGVs, and other automated systems, ensuring harmonious and efficient operation.

Key Takeaways Warehouse and Storage Market Size & Forecast

Users frequently seek high-level conclusions from market analyses, particularly regarding the overarching growth prospects and the fundamental drivers propelling the warehouse and storage sector forward. Key questions revolve around the sustainability of the projected growth, the primary factors contributing to market expansion, and the long-term strategic implications for businesses operating within or relying on this market. The emphasis is on understanding the core narrative of market evolution and identifying the most significant influences that will shape its future trajectory, providing a concise summary of the market's health and direction.

The warehouse and storage market is poised for significant and sustained growth, driven by a confluence of macroeconomic factors and technological advancements. This expansion underscores the increasing complexity and critical importance of logistics infrastructure in supporting global commerce. The forecast indicates not merely an increase in capacity but a transformation in how storage and distribution are managed, with intelligence and adaptability becoming paramount. Businesses engaging with this sector must therefore prioritize strategic investments in automation, data capabilities, and sustainable practices to remain competitive and capitalize on emerging opportunities.

- Robust and Consistent Growth: The market is projected for strong and steady growth through 2033, indicating resilient demand across various end-use industries.

- E-commerce as a Primary Catalyst: The exponential rise of online retail continues to be the most significant driver, demanding sophisticated fulfillment and last-mile delivery capabilities.

- Technological Transformation: Automation, AI, and data analytics are not just trends but fundamental shifts redefining operational efficiency and competitive advantage in the sector.

- Investment in Modernization: Significant capital expenditure is expected in upgrading existing infrastructure and building new, intelligent warehouses to meet evolving demands.

- Increased Supply Chain Complexity: Globalization and diversified product portfolios necessitate more agile and resilient storage solutions, pushing innovation in logistics.

Warehouse and Storage Market Drivers Analysis

The global warehouse and storage market is propelled by a multitude of factors, each contributing significantly to its robust expansion. A primary driver is the relentless growth of e-commerce, which necessitates vast and strategically located storage facilities to manage burgeoning online orders and complex fulfillment demands. This surge in online retail directly translates into increased requirements for inventory holding, order picking, and efficient distribution networks. Coupled with this is the increasing complexity of global supply chains, requiring flexible and resilient storage solutions to mitigate risks and ensure smooth operations across international borders.

Furthermore, advancements in technology, particularly in automation, robotics, and data analytics, are acting as powerful catalysts for market growth. These innovations enable warehouse operators to achieve unprecedented levels of efficiency, accuracy, and throughput, making investments in modern storage solutions highly attractive. The rising demand for specialized storage, such as temperature-controlled facilities for pharmaceuticals and food & beverages, also plays a crucial role. Urbanization and industrialization in emerging economies further amplify the need for sophisticated warehousing infrastructure, supporting both manufacturing and consumption centers.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| E-commerce Boom & Online Retail Growth | +2.5% | Global, particularly North America, APAC (China, India), Europe | Short to Long-term (2025-2033) |

| Increasing Complexity of Global Supply Chains | +1.8% | Global, especially cross-border trade hubs | Medium to Long-term (2026-2033) |

| Technological Advancements (Automation, AI, IoT) | +1.5% | Developed regions (North America, Europe), rapidly adopting emerging markets | Medium to Long-term (2026-2033) |

| Growth in Manufacturing and Industrial Output | +1.0% | APAC (China, India, Vietnam), Europe, North America | Medium to Long-term (2026-2033) |

Warehouse and Storage Market Restraints Analysis

Despite the positive growth outlook, the warehouse and storage market faces several significant restraints that could temper its expansion. One of the primary challenges is the substantial capital investment required for developing and equipping modern, automated warehouses. The high upfront costs associated with land acquisition, construction, advanced robotics, and sophisticated IT infrastructure can be prohibitive, especially for smaller players or in regions with limited access to financing. This often leads to slower adoption rates of cutting-edge technologies and limits market entry for new participants.

Another major restraint is the scarcity of suitable land, particularly in urban and peri-urban areas where demand for efficient last-mile logistics is highest. Escalating land costs, coupled with restrictive zoning regulations and environmental concerns, make it increasingly difficult to develop new large-scale warehousing facilities in prime locations. Furthermore, a growing shortage of skilled labor, particularly for operating complex automated systems and managing intricate supply chain processes, poses an ongoing operational challenge. This labor deficit impacts efficiency and can drive up operational costs, thus acting as a dampener on overall market potential.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Capital Investment for Automation & Infrastructure | -1.2% | Global, more pronounced in developing economies | Short to Medium-term (2025-2030) |

| Land Scarcity & Increasing Real Estate Costs | -0.9% | Urban and peri-urban areas globally, especially in Europe, North America, APAC | Medium to Long-term (2026-2033) |

| Labor Shortages & Skill Gap for Advanced Operations | -0.7% | Developed economies (North America, Europe) | Short to Long-term (2025-2033) |

| Regulatory Hurdles and Environmental Compliance | -0.5% | Europe, North America, some APAC countries | Medium-term (2026-2031) |

Warehouse and Storage Market Opportunities Analysis

Significant opportunities abound in the warehouse and storage market, offering avenues for sustained growth and innovation. The escalating demand for cold chain logistics, driven by the expanding pharmaceutical and food & beverage industries, presents a lucrative niche for specialized temperature-controlled storage solutions. As global populations grow and dietary preferences evolve, the need for robust cold storage infrastructure will only intensify, offering a consistent revenue stream for specialized operators. This specialization represents a high-value segment with increasing regulatory requirements and technological sophistication.

Moreover, the increasing adoption of sustainable warehousing practices offers a dual advantage: meeting environmental corporate social responsibility goals while simultaneously reducing long-term operational costs through energy efficiency and waste reduction. This includes investments in renewable energy, green building certifications, and sustainable material handling equipment. The burgeoning e-commerce sector further fuels opportunities for urban and micro-fulfillment centers, strategically located close to consumers for rapid last-mile delivery. These smaller, highly automated facilities are critical for addressing the immediate delivery expectations of online shoppers and optimizing delivery routes in dense urban environments, providing a competitive edge.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of Cold Chain Logistics (Pharma, F&B) | +1.8% | Global, particularly APAC, Latin America, Europe | Long-term (2027-2033) |

| Development of Urban & Micro-Fulfillment Centers | +1.5% | Major metropolitan areas globally (North America, Europe, APAC) | Short to Long-term (2025-2033) |

| Adoption of Sustainable & Green Warehousing Practices | +1.0% | Europe, North America, leading corporate entities globally | Medium to Long-term (2026-2033) |

| Integration of Advanced IoT and AI for Predictive Operations | +0.8% | Developed markets, technologically advanced companies | Medium to Long-term (2026-2033) |

Warehouse and Storage Market Challenges Impact Analysis

The warehouse and storage market is confronted by several complex challenges that demand innovative solutions and strategic foresight. Cybersecurity threats pose a significant risk, as increasingly interconnected and automated warehouses become attractive targets for cybercriminals. Breaches can lead to data loss, operational downtime, and severe reputational damage, necessitating robust security protocols and continuous vigilance. The rising cost of energy, driven by geopolitical factors and fluctuating supply, directly impacts operational expenses, particularly for energy-intensive facilities like cold storage, challenging profitability margins for operators.

Furthermore, managing the increasing volatility and unpredictability of global supply chains presents a constant challenge. Events such as natural disasters, pandemics, or geopolitical tensions can disrupt inventory flows, leading to stockouts or excess inventory, requiring agile and resilient warehousing strategies. The rapid pace of technological change also creates a challenge, as companies must continuously invest in upgrades and training to remain competitive, often facing a steep learning curve and significant integration complexities. Effectively navigating these challenges is crucial for sustained success and growth in the dynamic warehouse and storage sector.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising Cybersecurity Threats to Automated Systems | -0.8% | Global, particularly in regions with high automation adoption | Short to Long-term (2025-2033) |

| Fluctuating Energy Costs & Operational Expenses | -0.7% | Global, more acutely felt in energy-intensive operations (e.g., cold storage) | Short to Medium-term (2025-2030) |

| Supply Chain Disruptions & Volatility | -0.6% | Global, impacting interconnected economies | Short to Medium-term (2025-2030) |

| Complexity of Integrating New Technologies with Legacy Systems | -0.5% | Developed markets with established infrastructure | Medium-term (2026-2031) |

Warehouse and Storage Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global Warehouse and Storage Market, offering critical insights into its current landscape and future growth trajectory. The scope encompasses detailed market sizing, trend analysis, impact assessments of key drivers, restraints, opportunities, and challenges, along with a thorough examination of segmentation across various categories. It also includes regional spotlights and profiles of leading market participants, delivering a holistic view of the market's dynamics and competitive environment. The report is designed to equip stakeholders with actionable intelligence for strategic decision-making and investment planning within this evolving sector.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 520.5 billion |

| Market Forecast in 2033 | USD 960.3 billion |

| Growth Rate | 7.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Prologis, Americold Logistics, DHL Supply Chain, Kuehne + Nagel, Lineage Logistics, GXO Logistics, Nippon Express, UPS Supply Chain Solutions, Ryder System, XPO Logistics, C.H. Robinson, FedEx Supply Chain, Singapore Post, CEVA Logistics, DSV, DB Schenker, GEODIS, J.B. Hunt Transport Services, Panalpina World Transport, Bollore Logistics |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The warehouse and storage market is broadly segmented to provide a granular understanding of its diverse operational models and end-use applications. This segmentation allows for a detailed analysis of specific market niches, helping stakeholders identify areas of high growth, emerging demand, and competitive intensity. By understanding how different types of warehousing, ownership structures, and technological adoptions contribute to the overall market, businesses can tailor their strategies to target specific customer needs and operational requirements. This multi-faceted approach to market analysis ensures comprehensive coverage of the sector's complex dynamics.

The segmentation extends to various industry verticals, recognizing that the demands for storage and logistics vary significantly across sectors like retail, manufacturing, healthcare, and automotive. Each industry presents unique challenges and opportunities, influencing the type of warehousing services required, from standard ambient storage to highly specialized temperature-controlled or bonded facilities. Furthermore, the increasing adoption of advanced technologies like Warehouse Management Systems (WMS), robotics, and Artificial Intelligence (AI) for optimizing operations forms a critical segmentation, reflecting the market's ongoing digital transformation and the drive towards intelligent logistics solutions.

- By Type:

- Ambient

- Temperature-Controlled (Cold Storage, Chilled Storage)

- Bonded

- Automated

- By Ownership:

- Private Warehousing

- Public Warehousing

- Third-Party Logistics (3PL) Warehousing

- Contract Warehousing

- By End-Use Industry:

- Retail & E-commerce

- Manufacturing

- Food & Beverage

- Healthcare & Pharmaceuticals

- Automotive

- Consumer Goods

- Chemicals

- Others (e.g., Electronics, Agriculture)

- By Technology:

- Warehouse Management Systems (WMS)

- Warehouse Control Systems (WCS)

- Automated Storage and Retrieval Systems (AS/RS)

- Robotics (AMRs, AGVs, Robotic Picking)

- Conveyors and Sortation Systems

- Internet of Things (IoT)

- Artificial Intelligence (AI) & Machine Learning (ML)

- Enterprise Resource Planning (ERP) Integration

Regional Highlights

- North America: This region is characterized by high levels of automation adoption, particularly in the US and Canada, driven by the robust e-commerce sector and a strong focus on supply chain efficiency. Significant investment in advanced warehouse technologies and last-mile delivery infrastructure is prevalent.

- Europe: Known for its stringent regulatory environment and emphasis on sustainable logistics, Europe exhibits strong demand for green warehousing solutions and high-tech automation. Germany, UK, France, and Benelux countries are key hubs for innovation and investment in logistics infrastructure.

- Asia Pacific (APAC): The fastest-growing market globally, fueled by rapid industrialization, burgeoning e-commerce markets (especially in China, India, and Southeast Asia), and increasing foreign direct investment in manufacturing. There is a strong push towards developing modern logistics parks and adopting automation to handle massive volumes.

- Latin America: This region is experiencing significant growth in warehousing infrastructure, driven by expanding trade, improving economic conditions, and the rise of organized retail and e-commerce. Brazil and Mexico are leading markets, with increasing demand for modern storage and distribution centers.

- Middle East and Africa (MEA): Characterized by substantial investments in developing logistics hubs, particularly in the UAE and Saudi Arabia, aiming to become global trade gateways. Infrastructure development projects, coupled with growing e-commerce and manufacturing sectors, are driving demand for advanced warehousing solutions.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Warehouse and Storage Market.- Prologis

- Americold Logistics

- DHL Supply Chain

- Kuehne + Nagel

- Lineage Logistics

- GXO Logistics

- Nippon Express

- UPS Supply Chain Solutions

- Ryder System

- XPO Logistics

- C.H. Robinson

- FedEx Supply Chain

- Singapore Post

- CEVA Logistics

- DSV

- DB Schenker

- GEODIS

- J.B. Hunt Transport Services

- Panalpina World Transport

- Bollore Logistics

Frequently Asked Questions

What are the primary factors driving growth in the Warehouse and Storage Market?

The market's growth is primarily driven by the exponential expansion of e-commerce, the increasing complexity of global supply chains, rapid technological advancements in automation and AI, and the rising demand for specialized storage solutions like cold chain logistics. These factors collectively necessitate more efficient, scalable, and technologically advanced warehousing infrastructure.

How is artificial intelligence impacting warehouse operations?

AI significantly impacts warehouse operations by enabling enhanced inventory management through predictive analytics, optimizing picking and routing strategies, facilitating predictive maintenance for equipment, and improving demand forecasting accuracy. It also plays a crucial role in orchestrating robotics and automation, leading to greater efficiency, reduced errors, and lower operational costs.

What are the main challenges faced by the warehouse and storage industry?

Key challenges include the high initial capital investment required for modern, automated facilities, increasing land scarcity and costs in prime locations, a persistent shortage of skilled labor to operate advanced systems, escalating energy costs, and the growing threat of cybersecurity breaches targeting interconnected warehouse technologies. Additionally, navigating supply chain disruptions adds complexity.

What is the role of sustainability in modern warehousing?

Sustainability is becoming a critical component of modern warehousing, driving the adoption of energy-efficient designs, renewable energy sources, waste reduction programs, and sustainable material handling equipment. This focus not only helps meet environmental goals and regulatory compliance but also offers long-term operational cost savings and enhances corporate reputation.

Which regions are leading in warehouse and storage market growth and innovation?

Asia Pacific (APAC), particularly China and India, is experiencing the fastest market growth due to its booming e-commerce and manufacturing sectors. North America and Europe lead in innovation and automation adoption, driven by sophisticated logistics demands and significant investments in advanced warehousing technologies and green logistics initiatives.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted