Vision Insurance Market

Vision Insurance Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709063 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

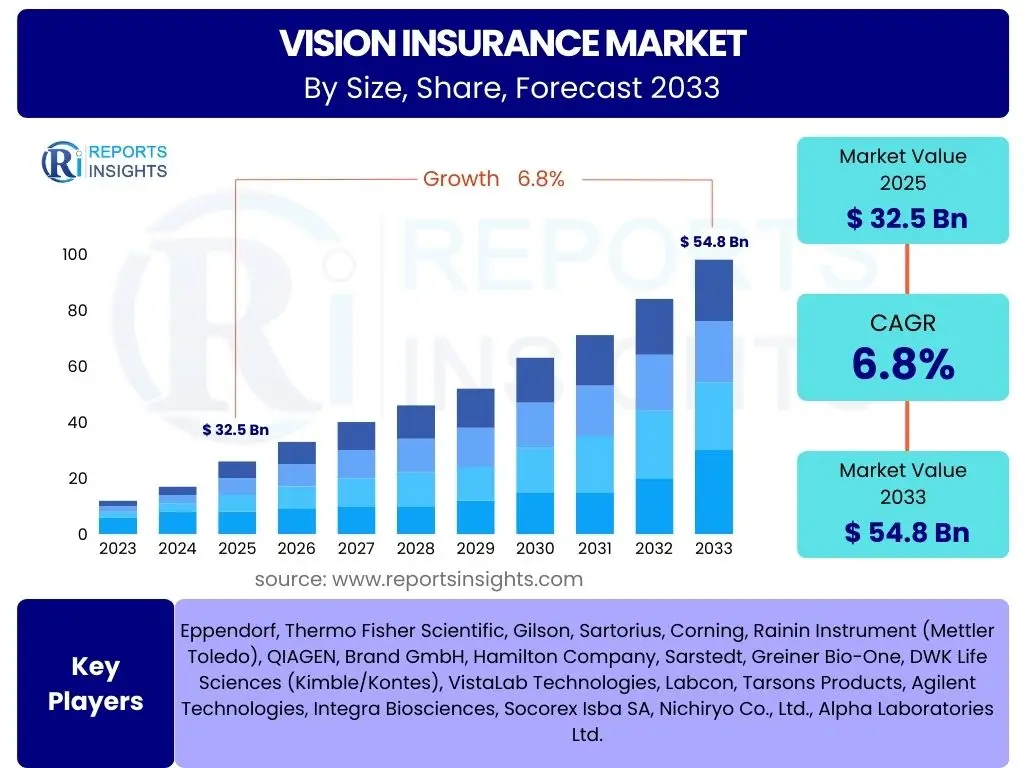

Vision Insurance Market Size

According to Reports Insights Consulting Pvt Ltd, The Vision Insurance Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 32.5 Billion in 2025 and is projected to reach USD 54.8 Billion by the end of the forecast period in 2033.

Key Vision Insurance Market Trends & Insights

User inquiries frequently highlight an interest in understanding the evolving landscape of vision insurance, with a particular focus on how the market is adapting to new consumer demands and technological advancements. The industry is experiencing a notable shift towards integrated wellness solutions, where vision care is increasingly viewed as a critical component of overall health. This trend reflects a broader consumer understanding of the interconnectedness of ocular health with systemic conditions such as diabetes and hypertension.

Another significant trend gaining traction is the personalization of vision insurance plans. Consumers are seeking more flexible and customizable options that cater to their specific lifestyle, visual needs, and budget constraints, moving away from one-size-fits-all policies. The growing adoption of digital platforms for policy management, claims processing, and virtual eye care consultations also underscores a broader digital transformation impacting how services are delivered and accessed. This digitalization not only enhances user convenience but also drives operational efficiencies for providers.

Preventive eye care is emerging as a central theme, with a heightened emphasis on early detection and management of eye conditions before they escalate. This proactive approach is being driven by increased awareness campaigns and the economic benefits of preventing severe vision impairment. Furthermore, the market is observing a steady rise in employer-sponsored vision benefits, reflecting a corporate commitment to employee well-being and productivity, recognizing vision care as a valuable component of comprehensive benefits packages.

- Increased focus on preventive eye care and early detection.

- Growing demand for personalized and flexible vision insurance plans.

- Digital transformation enhancing access and claims processing.

- Integration of vision care with broader wellness programs.

- Rising prevalence of employer-sponsored vision benefits.

AI Impact Analysis on Vision Insurance

User queries regarding the influence of Artificial Intelligence (AI) on the vision insurance sector predominantly revolve around efficiency gains, personalized service delivery, and fraud detection capabilities. There is a strong expectation that AI technologies will streamline complex administrative processes, such as claims adjudication and policy underwriting, thereby reducing operational costs and improving response times. This automation is anticipated to free up human resources to focus on more intricate client support and strategic initiatives, ultimately enhancing overall service quality.

Moreover, consumers and industry professionals alike are keenly interested in AI's potential to revolutionize personalized vision care and insurance offerings. By leveraging vast datasets, AI algorithms can analyze individual health profiles, lifestyle choices, and vision history to recommend highly tailored insurance plans and preventive care strategies. This level of personalization promises to optimize benefits for policyholders while also allowing insurers to more accurately assess risks and develop innovative product offerings that meet diverse needs.

Concerns also exist regarding data privacy and the ethical implications of AI deployment, particularly in the handling of sensitive health information. However, the overarching sentiment is one of optimism regarding AI's ability to foster a more proactive and efficient vision insurance ecosystem. From automating customer service interactions through chatbots to employing predictive analytics for identifying potential eye health risks, AI is poised to significantly enhance both the policyholder experience and the operational robustness of vision insurance providers, driving a new era of data-driven decision-making and service innovation.

- Enhanced claims processing and fraud detection through automation.

- Personalized plan recommendations and risk assessment leveraging data analytics.

- Automated customer service and support via AI-powered chatbots.

- Predictive analytics for identifying and managing ocular health risks.

- Operational efficiency improvements in policy administration and underwriting.

Key Takeaways Vision Insurance Market Size & Forecast

Analysis of common user questions reveals a strong desire for clarity on the most critical insights derived from the vision insurance market size and forecast. Users are primarily concerned with understanding the market's growth trajectory, the underlying factors driving this expansion, and the implications for both consumers and industry stakeholders. The sustained Compound Annual Growth Rate projected for the market signals a robust and expanding sector, indicating increasing consumer awareness and a growing demand for specialized vision care benefits.

A significant takeaway is the expanding role of vision insurance beyond basic corrective lenses, encompassing a broader spectrum of preventive services and advanced eye care technologies. This evolution is driven by demographic shifts, such as an aging global population prone to age-related eye conditions, and a heightened recognition of the importance of early intervention. The market's consistent growth underscores its resilience and its increasing integration into comprehensive health and wellness strategies for individuals and organizations.

Furthermore, the forecast emphasizes the importance of technological integration and product diversification as key strategies for market players. Companies that adapt to digital trends, offer flexible and personalized plans, and leverage data for enhanced customer experience are positioned for greater success. The regional disparities in market maturity also present strategic opportunities for expansion in underserved areas, highlighting a dynamic environment ripe for innovation and strategic investment across various geographical segments.

- The vision insurance market is projected for robust and sustained growth through 2033.

- Increased consumer and employer awareness is a primary catalyst for market expansion.

- Technological advancements and personalization are critical for market leadership.

- Preventive care and holistic wellness integration are shaping future offerings.

- Significant growth opportunities exist in emerging markets and through digital channels.

Vision Insurance Market Drivers Analysis

The vision insurance market is propelled by a confluence of factors that underscore the increasing recognition of ocular health as integral to overall well-being. A primary driver is the global rise in the prevalence of various eye conditions, including myopia, presbyopia, cataracts, and glaucoma. This escalating incidence, particularly in an aging global population, necessitates more frequent eye examinations and corrective measures, thereby increasing the demand for vision insurance to mitigate associated costs.

Another significant driver is the heightened awareness surrounding the importance of preventive eye care. Public health campaigns and educational initiatives are increasingly emphasizing the benefits of regular eye check-ups for early detection and management of potential issues, even for individuals without noticeable symptoms. This proactive approach encourages more individuals to enroll in vision insurance plans, viewing them as essential for maintaining long-term eye health and preventing more severe conditions.

The increasing focus by employers on comprehensive employee benefits packages also plays a crucial role. Companies are recognizing that offering vision insurance can enhance employee satisfaction, improve productivity by addressing vision-related issues, and serve as a valuable tool for talent attraction and retention. This corporate endorsement significantly expands the market reach of vision insurance, moving it from a perceived luxury to a standard component of employment benefits.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rising prevalence of eye conditions | +1.8% | Global, particularly Asia Pacific & North America | Short to Long-term (2025-2033) |

| Increasing awareness of preventive eye care | +1.5% | North America, Europe, Developed Asia Pacific | Mid to Long-term (2026-2033) |

| Growing geriatric population | +1.2% | Global, particularly Europe & Asia Pacific | Short to Long-term (2025-2033) |

| Employer initiatives for employee benefits | +1.0% | North America, Western Europe | Short to Mid-term (2025-2029) |

| Technological advancements in eye care | +0.8% | Global, especially urban areas | Mid to Long-term (2027-2033) |

Vision Insurance Market Restraints Analysis

Despite robust growth prospects, the vision insurance market faces several significant restraints that could impede its expansion. One prominent challenge is the relatively high cost of premiums, particularly for comprehensive plans that offer extensive coverage for frames, lenses, and specialized procedures. For many consumers, especially those with limited discretionary income, the perceived cost-benefit ratio of vision insurance may not be immediately apparent, leading to reluctance in adoption, particularly in regions with lower average incomes.

Another crucial restraint is the limited scope of coverage in some basic or standard vision insurance plans. Many policies may not fully cover advanced procedures like LASIK surgery, specific therapeutic treatments for chronic eye conditions, or high-end optical products, requiring significant out-of-pocket expenses for policyholders. This limited coverage can deter individuals who anticipate needing such specialized care, making them question the overall value proposition of the insurance.

Furthermore, a lack of widespread awareness and understanding about the benefits of vision insurance, especially in developing regions and among younger demographics, acts as a significant barrier to market penetration. Unlike general health insurance, vision insurance is often viewed as an optional benefit rather than a necessity, leading to lower adoption rates in populations unfamiliar with its long-term health and financial advantages. This perception requires extensive educational efforts to overcome, which can be resource-intensive for providers.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High cost of premiums | -1.5% | Global, particularly emerging economies | Short to Long-term (2025-2033) |

| Limited coverage scope in some plans | -1.0% | Global, but more pronounced in price-sensitive markets | Short to Mid-term (2025-2029) |

| Lack of awareness in developing regions | -0.8% | Africa, parts of Asia Pacific, Latin America | Long-term (2028-2033) |

| Competition from general health insurance plans | -0.5% | North America, Europe | Short-term (2025-2027) |

| Economic uncertainties impacting discretionary spending | -0.7% | Global, varies by economic cycle | Short to Mid-term (2025-2030) |

Vision Insurance Market Opportunities Analysis

The vision insurance market is poised for significant growth through various strategic opportunities that align with evolving consumer needs and technological advancements. One key area of opportunity lies in the expansion into emerging markets, where awareness of vision health is growing and disposable incomes are on the rise. These regions represent largely untapped populations with increasing demand for healthcare services, including specialized vision care, offering substantial long-term growth potential for insurers willing to adapt their offerings to local contexts and economic realities.

Another compelling opportunity involves the deeper integration with digital health platforms and telemedicine solutions. The increasing adoption of virtual consultations and online health management tools provides a pathway for vision insurance providers to enhance accessibility, reduce administrative overheads, and deliver services more efficiently. Leveraging these platforms allows for seamless claims processing, policy management, and even preliminary virtual eye screenings, which can significantly improve customer experience and market reach, particularly in remote areas.

Furthermore, the development of highly specialized plans tailored for specific demographics or needs presents a robust opportunity for market differentiation. This includes creating plans specifically for children with evolving vision requirements, seniors prone to age-related eye conditions, or individuals with professions requiring intense visual acuity. By addressing these niche segments with targeted benefits and services, insurers can capture specific market shares, enhance customer loyalty, and demonstrate a commitment to comprehensive, personalized care.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into emerging markets | +1.7% | Asia Pacific, Latin America, Middle East & Africa | Mid to Long-term (2027-2033) |

| Integration with digital health platforms | +1.4% | Global, especially developed markets | Short to Mid-term (2025-2029) |

| Development of specialized plans for specific demographics | +1.1% | North America, Europe, Urban Asia Pacific | Short to Long-term (2025-2033) |

| Partnerships with optometrists and ophthalmologists | +0.9% | Global, particularly local markets | Mid-term (2026-2030) |

| Focus on wellness and preventive care programs | +0.7% | North America, Europe | Long-term (2028-2033) |

Vision Insurance Market Challenges Impact Analysis

The vision insurance market, while growing, faces a range of challenges that could hinder its full potential and necessitate strategic responses from industry players. Navigating the complex landscape of regulatory hurdles and compliance requirements across different regions and countries presents a significant challenge. Variations in healthcare policies, insurance regulations, and consumer protection laws can make it difficult for providers to standardize offerings and expand internationally, leading to increased operational costs and administrative complexities. Ensuring adherence to these diverse legal frameworks is critical but resource-intensive.

Data privacy and security concerns represent another major impediment, particularly with the increasing digitalization of health records and claims processing. Vision insurance providers handle sensitive personal health information, making them prime targets for cyberattacks and data breaches. Maintaining robust cybersecurity infrastructure and adhering to stringent data protection regulations, such as GDPR or HIPAA, is paramount. Any lapse in data security can lead to severe reputational damage, financial penalties, and a loss of consumer trust, thereby impacting market growth.

Furthermore, the challenge of maintaining profitability amidst rising healthcare costs and competitive pressures is constant. As the costs of eye care services, optical products, and advanced treatments continue to escalate, insurers must carefully balance offering attractive benefits to policyholders with ensuring the financial viability of their plans. This balancing act is further complicated by intense competition from both specialized vision insurers and general health insurance providers offering integrated vision benefits, necessitating innovative pricing strategies and cost-management initiatives to sustain market presence and profitability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Regulatory hurdles and compliance | -1.2% | Global, highly localized impact | Short to Long-term (2025-2033) |

| Data privacy and security concerns | -1.0% | Global, especially developed markets | Short to Long-term (2025-2033) |

| Maintaining profitability amidst rising healthcare costs | -0.9% | Global | Short to Long-term (2025-2033) |

| Educating consumers on the value of vision insurance | -0.7% | Emerging markets, younger demographics | Mid to Long-term (2026-2033) |

| Attracting and retaining talent in a specialized market | -0.5% | Global | Mid-term (2026-2030) |

Vision Insurance Market - Updated Report Scope

This report provides an in-depth analysis of the Vision Insurance Market, encompassing historical data, current market dynamics, and future projections. It delivers comprehensive insights into market size, growth drivers, restraints, opportunities, and challenges, offering a strategic framework for stakeholders to navigate the evolving industry landscape. The report meticulously segments the market by coverage type, provider type, application, and end-use, complemented by a detailed regional analysis to provide a holistic view of market performance and potential.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 32.5 Billion |

| Market Forecast in 2033 | USD 54.8 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | VSP Global, EyeMed Vision Care, UnitedHealthcare, Humana, MetLife, Cigna, Aetna, Guardian Life Insurance, Ameritas, Anthem, Davis Vision, Spectera, Superior Vision, Blue Cross Blue Shield, National Vision, Versant Health, Delta Dental, Principal Financial Group, Lincoln Financial Group, Trustmark Insurance Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The vision insurance market is comprehensively segmented to provide a granular understanding of its diverse components and dynamics. This segmentation facilitates targeted analysis and strategic planning for market participants by highlighting specific areas of growth and opportunity. Understanding these segments is crucial for tailoring product offerings, optimizing marketing strategies, and identifying underserved niches within the broader market.

- Coverage Type: This segment includes Individual plans, catering to single policyholders or families purchasing directly, and Group plans, typically offered by employers, associations, or other organizations to their members. Group plans often benefit from lower premiums and broader participation.

- Provider Type: Segmented into Eye Care Clinics, Hospitals, Optical Shops, and Online Retailers. This categorization reflects the diverse channels through which vision care services and products are accessed, from traditional brick-and-mortar establishments to rapidly growing digital platforms.

- Application: This segment focuses on the primary uses of vision insurance, including Corrective Lenses (glasses), Contact Lenses, Eye Exams for routine check-ups and diagnostic purposes, and Other applications such as discounts on refractive surgeries (e.g., LASIK) or therapeutic care for specific eye conditions.

- End Use: Divided by demographic groups, this segment includes Adults (18-64), Children (0-17), and Seniors (65+). Each age group has distinct vision care needs and prevalence of eye conditions, influencing the types of insurance plans and benefits most relevant to them.

- Region: The market is geographically segmented into North America, Europe, Asia Pacific (APAC), Latin America, and Middle East, and Africa (MEA), recognizing the significant variations in market maturity, regulatory environments, and consumer behaviors across these territories.

Regional Highlights

- North America: This region consistently leads the vision insurance market, driven by high consumer awareness, widespread employer-sponsored health benefits, and advanced healthcare infrastructure. The United States, in particular, exhibits high penetration rates due to a strong emphasis on preventive care and comprehensive benefit packages. Regulatory support and the presence of major industry players further bolster market growth.

- Europe: Characterized by diverse healthcare systems, Europe demonstrates steady growth in vision insurance adoption. Countries like the UK, Germany, and France show significant demand, often integrated with broader health insurance schemes or offered as supplementary benefits. Increased awareness of eye health and an aging population contribute to the sustained demand.

- Asia Pacific (APAC): Expected to be the fastest-growing region, APAC offers immense growth opportunities due to its large population base, rising disposable incomes, and improving healthcare infrastructure. Countries like China, India, and South Korea are witnessing increasing adoption, driven by a growing middle class and expanding corporate sector offering employee benefits. However, market penetration remains lower than in developed regions, indicating significant untapped potential.

- Latin America: This region is experiencing nascent growth, with increasing awareness and economic development stimulating demand for vision insurance. Brazil and Mexico are key markets, where improving access to healthcare and a growing understanding of preventive health are gradually expanding the market. Challenges include economic volatility and varying regulatory frameworks.

- Middle East and Africa (MEA): The MEA region is at an early stage of market development but shows promising growth. Increased healthcare spending, particularly in GCC countries, and a rising prevalence of non-communicable diseases affecting eye health, are contributing to demand. However, limited awareness and disparities in healthcare access across the region remain key challenges.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Vision Insurance Market.- VSP Global

- EyeMed Vision Care

- UnitedHealthcare

- Humana

- MetLife

- Cigna

- Aetna

- Guardian Life Insurance

- Ameritas

- Anthem

- Davis Vision

- Spectera

- Superior Vision

- Blue Cross Blue Shield

- National Vision

- Versant Health

- Delta Dental

- Principal Financial Group

- Lincoln Financial Group

- Trustmark Insurance Company

Frequently Asked Questions

What is vision insurance and how does it work?

Vision insurance is a supplemental health benefit designed to reduce the costs associated with routine eye care, prescription eyewear, and sometimes even specific eye health treatments. It typically covers expenses for eye exams, prescription glasses, and contact lenses, often with co-pays or allowances. Policyholders pay a monthly or annual premium, and in return, receive coverage for services and products from a network of eye care professionals and optical retailers, making eye care more affordable and accessible.

What are the primary benefits of having vision insurance?

The primary benefits of vision insurance include significant cost savings on regular eye exams, which are crucial for detecting eye conditions early and maintaining overall health. It also helps reduce out-of-pocket expenses for corrective lenses such as glasses and contact lenses, which can be costly. Beyond financial savings, vision insurance promotes preventive eye care, ensuring individuals maintain optimal vision and address potential issues before they become severe, contributing to better quality of life and productivity.

How is AI impacting the future of vision insurance?

Artificial Intelligence is significantly impacting vision insurance by enhancing efficiency and personalization. AI can automate claims processing, improving speed and accuracy while reducing fraud. It also enables highly personalized plan recommendations by analyzing individual health data and needs. Furthermore, AI-powered tools can assist in predictive analytics for identifying at-risk individuals and improving customer service through chatbots, ultimately creating a more streamlined, responsive, and tailored vision insurance experience.

What are the key factors driving the growth of the vision insurance market?

The growth of the vision insurance market is primarily driven by several key factors: the increasing global prevalence of eye conditions such as myopia and presbyopia, a heightened awareness regarding the importance of preventive eye care, and the rising global geriatric population which requires more frequent eye health monitoring. Additionally, the expansion of employer-sponsored benefits and continuous technological advancements in eye care further stimulate market demand by making services more accessible and effective.

What challenges does the vision insurance market face?

The vision insurance market faces several challenges, including the high cost of premiums which can deter potential policyholders, and limitations in coverage scope for certain advanced procedures or high-end products. A lack of widespread awareness about the benefits of vision insurance, particularly in developing regions, also hinders market penetration. Additionally, providers must navigate complex regulatory environments, manage data privacy concerns, and maintain profitability amidst rising healthcare costs and intense competition.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted