Vinyl Acetate Monomer Market

Vinyl Acetate Monomer Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702746 | Last Updated : August 01, 2025 |

Format : ![]()

![]()

![]()

![]()

Vinyl Acetate Monomer Market Size

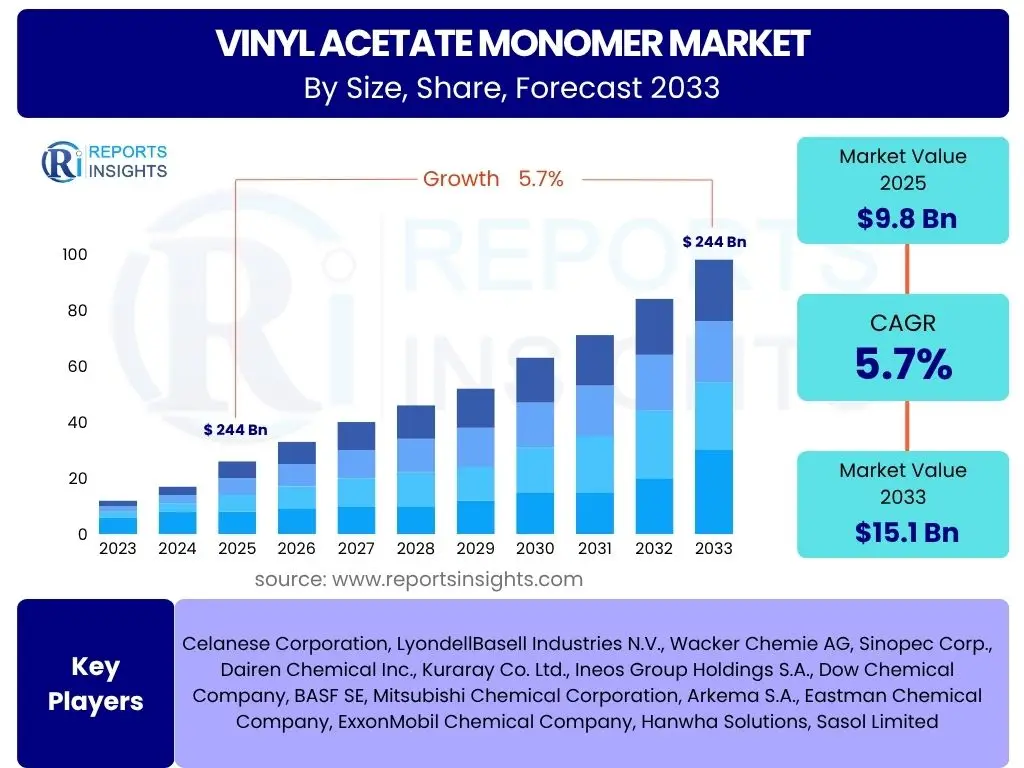

According to Reports Insights Consulting Pvt Ltd, The Vinyl Acetate Monomer Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.7% between 2025 and 2033. The market is estimated at USD 9.8 Billion in 2025 and is projected to reach USD 15.1 Billion by the end of the forecast period in 2033.

Key Vinyl Acetate Monomer Market Trends & Insights

Common user inquiries regarding the Vinyl Acetate Monomer (VAM) market trends frequently highlight the increasing demand from packaging and construction sectors, particularly in emerging economies. Users are keenly interested in understanding how sustainability initiatives and the development of bio-based VAM alternatives are reshaping the industry landscape. Furthermore, there is significant curiosity about the impact of fluctuating raw material prices and geopolitical factors on supply chain stability and market dynamics. The shift towards more specialized and high-performance VAM derivatives also represents a key area of public interest, reflecting the market's continuous evolution beyond traditional applications.

Another prevalent theme in user questions concerns the technological advancements in VAM production processes. Users seek information on innovations that enhance production efficiency, reduce environmental footprint, and lower operational costs. The adoption of advanced catalytic technologies and process optimization techniques is consistently a topic of discussion. Additionally, the increasing focus on circular economy principles within the chemical industry leads to questions about VAM recycling and waste reduction strategies, indicating a growing awareness of environmental responsibility among stakeholders.

- Growing demand from packaging, construction, and automotive industries.

- Rising adoption of bio-based Vinyl Acetate Monomer solutions.

- Technological advancements in VAM production efficiency and sustainability.

- Increasing focus on high-performance VAM derivatives for specialized applications.

- Strategic expansions and partnerships by key market players in high-growth regions.

AI Impact Analysis on Vinyl Acetate Monomer

User queries regarding the impact of Artificial Intelligence (AI) on the Vinyl Acetate Monomer (VAM) sector frequently revolve around its potential to optimize production processes and enhance supply chain resilience. Stakeholders are keen to understand how AI-driven predictive analytics can improve plant efficiency, reduce energy consumption, and minimize waste in VAM manufacturing. There is also significant interest in AI's role in forecasting raw material price fluctuations and managing inventory, which are critical for an industry highly susceptible to supply chain disruptions. The expectation is that AI will provide greater precision in process control, leading to higher product quality and reduced operational costs.

Furthermore, common user questions address AI's application in research and development for new VAM derivatives and sustainable production methods. Users are exploring how AI algorithms can accelerate the discovery of novel catalysts or optimize formulation for specific end-use applications. Concerns often include data privacy, the need for skilled labor to manage AI systems, and the initial investment required for AI implementation. Despite these challenges, the prevailing sentiment is that AI will be a transformative force, enabling more agile decision-making, predictive maintenance, and overall increased competitiveness within the VAM market by fostering innovation and operational excellence.

- Optimized production processes through AI-driven predictive analytics, enhancing efficiency and reducing waste.

- Improved supply chain management and logistics planning via AI forecasting and real-time data analysis.

- Accelerated research and development for new VAM derivatives and sustainable alternatives using AI algorithms.

- Enhanced quality control and product consistency through AI-powered monitoring and anomaly detection.

- Predictive maintenance for manufacturing equipment, minimizing downtime and increasing operational reliability.

Key Takeaways Vinyl Acetate Monomer Market Size & Forecast

Common user questions regarding key takeaways from the Vinyl Acetate Monomer (VAM) market size and forecast frequently center on the primary drivers sustaining its projected growth. Users consistently seek to understand which end-use industries are the most significant contributors to demand and why. Insights into the sustained expansion of the construction, packaging, and textile industries are often highlighted as crucial factors underpinning the market's positive outlook. The forecast also reveals a robust expansion driven by increasing industrialization and urbanization, particularly in Asia Pacific, making it a critical region for future growth.

Another significant area of user interest pertains to the resilience of the VAM market against potential restraints, such as raw material price volatility and stringent environmental regulations. The market's ability to adapt through technological innovations, including the development of bio-based alternatives and more efficient production methods, is perceived as vital for mitigating these challenges. The overall takeaway is a market poised for steady growth, supported by diversified applications and a proactive approach towards sustainability, ensuring its relevance across a wide array of industrial applications despite inherent complexities.

- The Vinyl Acetate Monomer market is set for robust growth, driven by escalating demand from diverse end-use industries.

- Asia Pacific is anticipated to remain the dominant and fastest-growing region, fueled by rapid industrialization and infrastructure development.

- Innovations in sustainable and bio-based VAM production methods are gaining traction, supporting long-term market sustainability.

- Fluctuations in raw material prices and stringent environmental regulations represent ongoing challenges requiring strategic adaptation.

- Expansion of applications in adhesives, paints and coatings, films, and textiles will continue to propel market expansion.

Vinyl Acetate Monomer Market Drivers Analysis

The global Vinyl Acetate Monomer (VAM) market is primarily driven by the escalating demand from various end-use industries, particularly the burgeoning construction sector and the expanding packaging industry. VAM is a crucial building block for producing polyvinyl acetate (PVA), ethylene vinyl acetate (EVA), and polyvinyl alcohol (PVOH), which are extensively used in adhesives, paints, coatings, films, and textiles. The rapid urbanization and infrastructure development in emerging economies, notably in the Asia Pacific region, are significantly boosting the consumption of these derivatives, thereby fueling VAM market growth.

Furthermore, the increasing adoption of VAM-based polymers in diverse applications, ranging from automotive components to consumer goods, contributes substantially to market expansion. The demand for durable, high-performance, and versatile materials is consistently rising, which in turn necessitates higher VAM production. Innovations in product formulations and the development of specialized VAM derivatives for niche applications also act as significant market drivers, allowing VAM to cater to evolving industrial requirements and maintain its competitive edge in the chemical landscape.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand from the construction industry (adhesives, paints, coatings) | +1.8% | Asia Pacific, North America, Europe | 2025-2033 |

| Rising consumption in packaging and film applications | +1.5% | Global, particularly Asia Pacific | 2025-2033 |

| Increasing use in textile and non-woven fabric production | +0.9% | Asia Pacific, Latin America | 2025-2033 |

| Expansion of automotive and consumer goods sectors | +0.8% | Global | 2025-2033 |

| Technological advancements in VAM production processes | +0.7% | Developed regions (Europe, North America) | 2025-2033 |

Vinyl Acetate Monomer Market Restraints Analysis

The Vinyl Acetate Monomer (VAM) market faces significant restraints primarily due to the volatility of raw material prices, particularly ethylene and acetic acid. These petrochemical feedstocks are subject to global supply-demand dynamics, geopolitical tensions, and crude oil price fluctuations, leading to unpredictable production costs. Such instability directly impacts manufacturers' profitability and can compel them to defer investment decisions, thereby hindering market expansion. The high capital expenditure required for establishing and maintaining VAM production facilities also acts as a barrier to entry for new players, limiting overall market growth and innovation.

Another considerable restraint is the increasingly stringent environmental regulations concerning chemical production and volatile organic compound (VOC) emissions. Governments worldwide are imposing stricter norms on industrial processes to reduce pollution and promote sustainability, which necessitates significant investments in cleaner technologies and waste management for VAM manufacturers. This regulatory burden can increase operational costs and complexity, particularly for older facilities, potentially slowing down production capacity expansions or leading to plant closures in some regions. The availability of substitute materials, although limited, also poses a minor restraint, compelling manufacturers to continually innovate and demonstrate VAM's superior performance in various applications.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile raw material prices (ethylene, acetic acid) | -1.2% | Global | 2025-2033 |

| Stringent environmental regulations and emission controls | -0.8% | Europe, North America, China | 2025-2033 |

| High capital expenditure for plant setup and maintenance | -0.5% | Global | 2025-2033 |

| Potential oversupply in certain regional markets | -0.4% | Asia Pacific (e.g., China) | Short-term to Mid-term (2025-2028) |

| Competition from substitute materials in niche applications | -0.3% | Global | 2025-2033 |

Vinyl Acetate Monomer Market Opportunities Analysis

Significant opportunities in the Vinyl Acetate Monomer (VAM) market arise from the increasing focus on sustainability and the development of bio-based VAM. As environmental concerns grow, there is a rising demand for chemical products derived from renewable resources, presenting a substantial opening for manufacturers to invest in research and development of sustainable VAM production methods. This shift aligns with global efforts to reduce carbon footprint and move towards a circular economy, attracting investments and partnerships aimed at developing greener alternatives. Early movers in this segment can gain a considerable competitive advantage and appeal to environmentally conscious consumers and industries.

Furthermore, the expansion into emerging applications and niche markets offers lucrative growth avenues for VAM. Innovations leading to new uses for VAM derivatives in specialized coatings, high-performance polymers, and advanced composite materials can unlock untapped revenue streams. Strategic collaborations between VAM producers and end-use industries to co-develop tailored solutions will be crucial for capitalizing on these opportunities. Geographic expansion into underdeveloped markets with growing industrial bases also represents a vital opportunity, as these regions are likely to experience increased demand for VAM-derived products in their infrastructure and manufacturing sectors over the forecast period.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and commercialization of bio-based VAM | +1.3% | Europe, North America, Asia Pacific | Mid- to Long-term (2027-2033) |

| Expansion into new and specialized applications (e.g., advanced materials) | +1.1% | Global | 2025-2033 |

| Increasing demand from emerging economies for infrastructure development | +1.0% | Asia Pacific, Latin America, MEA | 2025-2033 |

| Strategic collaborations and partnerships for supply chain optimization | +0.7% | Global | 2025-2033 |

| Recycling and circular economy initiatives for VAM derivatives | +0.5% | Europe, North America | Long-term (2029-2033) |

Vinyl Acetate Monomer Market Challenges Impact Analysis

The Vinyl Acetate Monomer (VAM) market faces significant challenges related to supply chain disruptions, which can stem from various global factors such as geopolitical instability, natural disasters, or pandemics. These disruptions lead to erratic availability of raw materials, transportation bottlenecks, and sudden shifts in demand and supply, causing price volatility and impacting manufacturing schedules. The inherent complexity of global supply chains for petrochemicals makes the VAM market particularly vulnerable, forcing companies to invest in more resilient and diversified sourcing strategies to mitigate these risks. Maintaining a stable and predictable production environment amidst these external variables remains a critical challenge for VAM producers.

Another key challenge is the intense competition within the VAM industry, characterized by the presence of a few large, established players and ongoing capacity expansions, particularly in Asia. This competitive landscape often leads to pricing pressures and reduced profit margins, compelling manufacturers to continually innovate and seek cost efficiencies. Furthermore, the high energy intensity of VAM production processes presents a challenge, as fluctuations in energy prices can significantly impact operational costs. Adherence to increasingly strict product safety standards and regulations across different regions also adds a layer of complexity and cost, requiring continuous investment in compliance and quality assurance measures.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global supply chain disruptions and logistics complexities | -1.0% | Global | 2025-2030 |

| Intense market competition and pricing pressures | -0.7% | Asia Pacific, Global | 2025-2033 |

| High energy consumption and fluctuating energy prices | -0.6% | Global | 2025-2033 |

| Adherence to evolving product safety and environmental compliance | -0.5% | Europe, North America | 2025-2033 |

| Management of production overcapacity in specific regions | -0.4% | Asia Pacific (especially China) | Short-term (2025-2027) |

Vinyl Acetate Monomer Market - Updated Report Scope

This market research report provides an in-depth analysis of the global Vinyl Acetate Monomer (VAM) market, offering comprehensive insights into its current size, historical performance, and future growth projections. The scope encompasses detailed segmentation analysis by application, end-use industry, and geography, alongside a thorough examination of market drivers, restraints, opportunities, and challenges. It also includes an assessment of the competitive landscape, profiling key players and their strategic initiatives, to deliver a holistic understanding of the market dynamics and future outlook for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 9.8 Billion |

| Market Forecast in 2033 | USD 15.1 Billion |

| Growth Rate | 5.7% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Celanese Corporation, LyondellBasell Industries N.V., Wacker Chemie AG, Sinopec Corp., Dairen Chemical Inc., Kuraray Co. Ltd., Ineos Group Holdings S.A., Dow Chemical Company, BASF SE, Mitsubishi Chemical Corporation, Arkema S.A., Eastman Chemical Company, ExxonMobil Chemical Company, Hanwha Solutions, Sasol Limited |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Vinyl Acetate Monomer (VAM) market is comprehensively segmented to provide a granular understanding of its diverse applications and end-use industries. This segmentation is crucial for identifying key growth areas and targeted market strategies. By application, the market is primarily driven by the production of polyvinyl acetate (PVA), ethylene vinyl acetate (EVA), and polyvinyl alcohol (PVOH), which are foundational polymers in numerous industries. Each application segment showcases distinct growth trajectories influenced by specific market demands and technological advancements.

Further segmentation by end-use industry allows for a detailed analysis of VAM consumption across sectors such as paints and coatings, adhesives and sealants, films and packaging, textiles, and construction. The varying growth rates and demand patterns within these industries directly impact the overall VAM market dynamics. This detailed breakdown enables stakeholders to pinpoint sectors with high growth potential and tailor product offerings or investment strategies accordingly, optimizing their market penetration and revenue generation efforts across the global landscape.

- By Application:

- Polyvinyl Acetate (PVA)

- Ethylene Vinyl Acetate (EVA)

- Polyvinyl Alcohol (PVOH)

- Ethylene Vinyl Alcohol (EVOH)

- Vinyl Acetate Ethylene (VAE)

- Other Applications (e.g., Vinyl Acetate-Acrylic Ester Copolymer)

- By End-Use Industry:

- Paints and Coatings

- Adhesives and Sealants

- Films and Packaging

- Textiles

- Construction

- Automotive

- Paper

- Others (e.g., Medical, Electrical & Electronics)

Regional Highlights

- Asia Pacific: Expected to be the largest and fastest-growing market due to rapid industrialization, burgeoning construction activities, and increasing demand from the packaging and textile industries in countries like China, India, and Southeast Asian nations. Significant investments in infrastructure and manufacturing facilities are propelling VAM consumption.

- North America: A mature market characterized by stable demand from established industries such as paints and coatings, adhesives, and automotive. Focus on advanced materials and sustainable solutions drives innovation. Regulatory frameworks influence production and application trends.

- Europe: Exhibits a steady growth rate, largely driven by strict environmental regulations fostering demand for eco-friendly and high-performance VAM derivatives. The region is a hub for research and development in sustainable chemistry and advanced materials, influencing global VAM innovations.

- Latin America: Showing promising growth fueled by developing economies, increasing industrial output, and rising consumer spending. Brazil and Mexico are key contributors, with expanding construction and packaging sectors.

- Middle East and Africa (MEA): Emerging as a region with potential growth due to ongoing industrial diversification efforts and increasing investments in infrastructure and manufacturing capabilities, particularly in the GCC countries.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Vinyl Acetate Monomer Market.- Celanese Corporation

- LyondellBasell Industries N.V.

- Wacker Chemie AG

- Sinopec Corp.

- Dairen Chemical Inc.

- Kuraray Co. Ltd.

- Ineos Group Holdings S.A.

- Dow Chemical Company

- BASF SE

- Mitsubishi Chemical Corporation

- Arkema S.A.

- Eastman Chemical Company

- ExxonMobil Chemical Company

- Hanwha Solutions

- Sasol Limited

- PTT Global Chemical Public Company Limited

- Formosa Plastics Corporation

- Reliance Industries Limited

- Sibur Holding JSC

- Sumitomo Chemical Co., Ltd.

Frequently Asked Questions

Common user questions about the Vinyl Acetate Monomer market indicate a strong interest in understanding market fundamentals, growth prospects, and influencing factors. The queries frequently touch upon the market's size, its primary drivers, key applications, and the major companies operating within this chemical sector. Users also often inquire about environmental aspects and the future outlook of the VAM industry in the context of sustainability and technological advancements.What is Vinyl Acetate Monomer (VAM) and its primary uses?

Vinyl Acetate Monomer (VAM) is a colorless organic liquid and a crucial chemical intermediate. Its primary uses involve polymerization to produce various essential polymers such as polyvinyl acetate (PVA), ethylene vinyl acetate (EVA), and polyvinyl alcohol (PVOH), which are widely utilized in adhesives, paints and coatings, films, textiles, and paper manufacturing.

What are the main factors driving the growth of the VAM market?

The main factors driving VAM market growth include the escalating demand from the construction industry for adhesives and coatings, robust expansion in the packaging and film sectors, and increasing consumption in the textile and non-woven industries. Rapid industrialization and urbanization in emerging economies also significantly contribute to market expansion.

Which region currently dominates the Vinyl Acetate Monomer market?

Asia Pacific currently dominates the Vinyl Acetate Monomer market, driven by substantial manufacturing and industrial growth, extensive infrastructure development, and high demand from key end-use industries like construction, textiles, and packaging in countries such as China and India.

What are the key challenges facing the Vinyl Acetate Monomer market?

Key challenges facing the VAM market include the volatility of raw material prices (ethylene and acetic acid), stringent environmental regulations impacting production processes, global supply chain disruptions, and intense competition leading to pricing pressures from major manufacturers.

Are there sustainable alternatives or advancements in VAM production?

Yes, significant advancements are being made in developing sustainable alternatives, including bio-based Vinyl Acetate Monomer (Bio-VAM) derived from renewable resources. There is also an increasing focus on optimizing production processes to reduce energy consumption and environmental footprint, aligning with global sustainability goals.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted