Video Gaming Hardware Market

Video Gaming Hardware Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701427 | Last Updated : July 29, 2025 |

Format : ![]()

![]()

![]()

![]()

Video Gaming Hardware Market Size

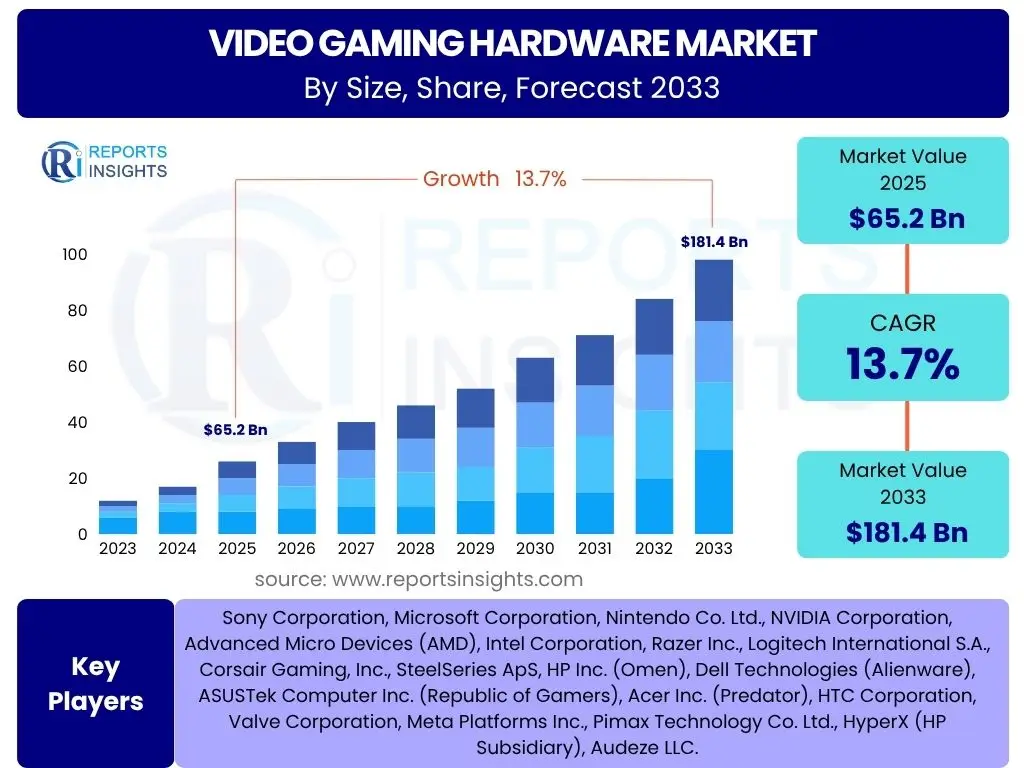

According to Reports Insights Consulting Pvt Ltd, The Video Gaming Hardware Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 13.7% between 2025 and 2033. The market is estimated at USD 65.2 billion in 2025 and is projected to reach USD 181.4 billion by the end of the forecast period in 2033.

Key Video Gaming Hardware Market Trends & Insights

The video gaming hardware market is currently undergoing significant transformation, driven by a convergence of technological advancements and evolving consumer preferences. Key trends indicate a strong shift towards more immersive and high-fidelity experiences, demanding more powerful and specialized hardware. Users are increasingly concerned with performance metrics such as refresh rates, resolution, and loading times, pushing manufacturers to innovate in processor, graphics card, and storage technologies. The proliferation of diverse gaming platforms, from traditional consoles and high-end PCs to emerging cloud gaming services and portable devices, also highlights a trend towards versatile and accessible hardware solutions. Furthermore, customization and personalization options are gaining traction, as gamers seek unique setups that reflect their individual styles and optimize their play experiences. The integration of advanced haptic feedback, sophisticated audio solutions, and virtual reality capabilities is reshaping how players interact with games, moving beyond conventional inputs to more sensory-rich engagements.

Another prominent trend is the increasing focus on sustainability and energy efficiency in hardware design and manufacturing. As the environmental impact of electronic waste and energy consumption becomes a global concern, consumers and regulators alike are encouraging the adoption of greener technologies and more responsible production cycles. This includes developing components that consume less power while maintaining high performance, utilizing recycled materials, and designing hardware for easier repairability and upgrades. The rise of competitive gaming, commonly known as esports, continues to profoundly influence hardware development, necessitating ultra-low latency peripherals, robust networking capabilities, and highly durable components built for intense, prolonged use. This demand from the professional gaming circuit filters down to mainstream consumers, elevating overall hardware standards across the market. Moreover, the expanding accessibility of gaming, particularly in emerging economies and through mobile platforms, is driving demand for more affordable yet capable hardware solutions, fostering innovation in entry-level and mid-range segments.

- Hyper-realistic graphics and high refresh rate demands drive GPU/CPU innovation.

- Increased adoption of Virtual Reality (VR) and Augmented Reality (AR) headsets.

- Growth in portable and handheld gaming devices.

- Rise of cloud gaming influence on peripheral and streaming hardware.

- Emphasis on customization, modularity, and aesthetic design.

- Sustainability initiatives in hardware manufacturing and energy efficiency.

- Esports popularity driving demand for high-performance and low-latency peripherals.

- Integration of advanced haptic feedback and immersive audio technologies.

AI Impact Analysis on Video Gaming Hardware

The impact of Artificial intelligence (AI) on the video gaming hardware market is profound and multifaceted, addressing key user interests related to performance, realism, and personalized experiences. Gamers are keenly interested in how AI can enhance visual fidelity without compromising frame rates, leading to significant advancements in AI-powered upscaling technologies like NVIDIA's DLSS and AMD's FSR. These technologies leverage machine learning to reconstruct high-resolution images from lower-resolution inputs, effectively boosting performance on existing hardware and making high-fidelity gaming more accessible. Beyond rendering, users are also curious about AI's role in optimizing hardware utilization, from dynamic power management to intelligent cooling systems that adapt to gaming loads. This optimization can extend hardware lifespan and improve overall efficiency, directly addressing concerns about hardware longevity and performance consistency.

Furthermore, AI is increasingly being integrated into the gaming experience itself, influencing hardware requirements. This includes AI for smarter non-player characters (NPCs) that adapt to player actions, procedural content generation that creates dynamic game worlds, and personalized recommendation engines that suggest games or in-game content tailored to individual player preferences. Such AI-driven game mechanics may necessitate specialized AI accelerators or more powerful general-purpose processing units within gaming hardware to handle the computational load efficiently. The potential for AI to create more immersive and responsive game environments is a significant draw, pushing the boundaries of what gaming hardware needs to achieve. Concerns also revolve around the future-proofing of hardware to support increasingly complex AI models, influencing consumer purchasing decisions towards hardware with robust AI capabilities. As AI models become more sophisticated, the demand for dedicated AI cores or accelerated processing units within gaming GPUs and CPUs is expected to intensify, shaping the next generation of gaming hardware design.

- AI-Powered Upscaling: Enhances visual fidelity and performance, requiring specialized hardware acceleration (Tensor Cores, XMX Engines).

- Intelligent Hardware Optimization: AI manages power efficiency, cooling, and resource allocation dynamically.

- Advanced Game AI: Enables more realistic NPCs and dynamic game worlds, potentially requiring more processing power.

- Personalized Gaming Experiences: AI algorithms for content recommendation and adaptive gameplay.

- Hardware Design & Manufacturing: AI optimizes chip layouts and production processes for efficiency.

- Edge AI Processing: Growing need for local AI processing capabilities in consoles and PCs for immediate responsiveness.

Key Takeaways Video Gaming Hardware Market Size & Forecast

The Video Gaming Hardware market is poised for robust growth, driven by an insatiable demand for immersive and high-performance gaming experiences, as well as the continuous evolution of core technologies. A significant takeaway from the market forecast is the strong compound annual growth rate projected through 2033, indicating sustained expansion across various hardware segments. This growth is underpinned by the increasing global gaming population, the ongoing console cycle, and the rising popularity of competitive esports, which collectively necessitate continuous upgrades and innovation in gaming devices. The market's substantial valuation by 2033 underscores its pivotal role in the broader entertainment and technology sectors, demonstrating its resilience and capacity for innovation amidst economic shifts.

Another crucial insight is the dynamic interplay between software advancements and hardware development; as games become more graphically intensive and feature-rich, they inherently drive the demand for more powerful and specialized hardware. This symbiotic relationship ensures a continuous cycle of innovation and consumer adoption. The forecast also highlights the growing importance of emerging markets, where increasing disposable incomes and internet penetration are opening new avenues for hardware sales, complementing the mature markets where replacement cycles and premium product sales remain strong. Ultimately, the market is characterized by a strong consumer appetite for cutting-edge technology, a competitive landscape fostering rapid innovation, and a long-term trajectory indicating substantial investment and expansion opportunities for manufacturers and related industries.

- Significant Growth Trajectory: Market to nearly triple in value by 2033, reflecting strong global demand.

- Technology-Driven Expansion: Advancements in graphics, processing, and display technologies are primary growth catalysts.

- Diverse Segment Contribution: Growth driven by consoles, high-end PCs, and expanding peripheral markets.

- Esports & Immersive Experiences: Key drivers for premium and specialized hardware adoption.

- Emerging Market Potential: Asia Pacific and Latin America show significant untapped growth opportunities.

- AI Integration Critical: AI's role in performance enhancement and game development will increasingly shape hardware design.

Video Gaming Hardware Market Drivers Analysis

The Video Gaming Hardware market is propelled by a confluence of robust drivers, primarily centered around rapid technological advancements and the expanding global appeal of gaming as a mainstream entertainment form. Innovations in semiconductor technology, particularly in graphics processing units (GPUs) and central processing units (CPUs), are consistently pushing the boundaries of what gaming hardware can achieve, enabling higher resolutions, faster refresh rates, and more realistic visual effects. This perpetual cycle of technological progress creates a strong incentive for consumers to upgrade their existing hardware or invest in new systems, ensuring a continuous demand flow. Additionally, the proliferation of high-speed internet infrastructure globally facilitates online multiplayer gaming and the adoption of digital distribution platforms, which in turn fuels the demand for capable hardware to support these experiences.

Beyond technology, the burgeoning esports industry plays a critical role in driving hardware sales, as professional and aspiring competitive gamers require top-tier, low-latency equipment to gain a competitive edge. This demand trickles down to casual gamers who aspire to emulate professional setups. The increasing disposable income in developing regions, coupled with a growing youth demographic actively engaged in gaming, further expands the consumer base. The diversification of gaming platforms, including dedicated consoles, high-end gaming PCs, and the emergence of cloud gaming services, caters to a wider array of preferences and budgets, ensuring broad market penetration. Moreover, the integration of gaming into cultural phenomena, media, and social interactions reinforces its status as a primary entertainment choice, sustaining and escalating hardware consumption.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technological Advancements in GPUs & CPUs | +1.8% | Global (North America, APAC, Europe) | Long-term (2025-2033) |

| Growing Popularity of Esports & Competitive Gaming | +1.5% | APAC (China, South Korea), North America, Europe | Mid-term (2026-2030) |

| Increasing Disposable Income & Urbanization in Emerging Markets | +1.2% | APAC (India, Southeast Asia), Latin America, MEA | Long-term (2025-2033) |

| Expansion of Gaming User Base & Digital Distribution | +1.0% | Global | Short to Mid-term (2025-2028) |

Video Gaming Hardware Market Restraints Analysis

Despite its robust growth, the Video Gaming Hardware market faces several significant restraints that could temper its expansion. One primary concern is the high cost associated with premium gaming hardware, particularly high-end PCs, next-generation consoles, and advanced peripherals like VR headsets. These substantial upfront investments can deter price-sensitive consumers or those with limited disposable income, especially in emerging markets where gaming is still gaining traction. The rapid pace of technological obsolescence further exacerbates this issue; new hardware iterations are released frequently, often making previous generations less desirable within a short timeframe. This rapid depreciation can lead to consumer hesitation in making significant purchases, as they anticipate newer, more powerful, or more feature-rich models being released shortly after their acquisition.

Another critical restraint involves global supply chain disruptions, as experienced during recent semiconductor shortages. The complex manufacturing processes and reliance on specialized components from a limited number of suppliers make the industry vulnerable to production bottlenecks, logistical challenges, and geopolitical tensions. Such disruptions can lead to inflated prices, extended waiting periods for consumers, and missed sales opportunities for manufacturers. Furthermore, intense competition from alternative entertainment options, including mobile gaming, streaming services, and other leisure activities, presents a continuous challenge. While mobile gaming can be a gateway for new players, it also offers a low-cost entry point that may prevent some users from migrating to dedicated hardware platforms. Balancing performance with energy consumption and addressing environmental concerns related to electronic waste also pose ongoing challenges that can influence consumer perception and regulatory scrutiny, potentially impacting market growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Cost of Premium Hardware | -0.8% | Global (Impacts Emerging Markets More) | Long-term (2025-2033) |

| Rapid Technological Obsolescence & Frequent Upgrades | -0.6% | North America, Europe, APAC (Mature Markets) | Mid-term (2026-2030) |

| Global Supply Chain Vulnerabilities & Component Shortages | -0.7% | Global | Short to Mid-term (2025-2027) |

| Competition from Mobile Gaming & Alternative Entertainment | -0.5% | Global | Long-term (2025-2033) |

Video Gaming Hardware Market Opportunities Analysis

The Video Gaming Hardware market presents significant opportunities for innovation and expansion, particularly driven by emerging technological frontiers and untapped consumer segments. The continued development of Virtual Reality (VR) and Augmented Reality (AR) technologies offers a substantial growth avenue, as these immersive platforms require specialized and powerful hardware for optimal performance. As VR/AR adoption broadens beyond niche markets into mainstream entertainment and even enterprise applications, the demand for dedicated headsets, controllers, and high-performance computing components will surge, opening new revenue streams for hardware manufacturers. Furthermore, the evolution of cloud gaming services presents a paradoxical but promising opportunity; while it reduces the need for high-end local processing, it simultaneously fuels demand for low-latency peripherals, robust networking hardware, and specialized streaming devices optimized for cloud environments, allowing for a broader reach of gaming experiences.

Another major opportunity lies in the expansion into developing and underserved markets, where increasing internet penetration and rising middle-class populations are creating a vast new consumer base. Regions such as Southeast Asia, India, Latin America, and parts of Africa are witnessing a surge in gaming interest, often starting with mobile but gradually transitioning to more dedicated hardware as disposable income rises. This demographic shift necessitates the development of more affordable yet capable hardware solutions and tailored distribution strategies. Moreover, the growing focus on sustainability and eco-friendly practices in manufacturing and product design represents an opportunity for brands to differentiate themselves and appeal to environmentally conscious consumers. Innovations in modular and upgradeable hardware, allowing for longer product lifespans and reduced electronic waste, also align with consumer desires for value and sustainability, creating a positive market narrative and fostering brand loyalty.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion of VR/AR Gaming Ecosystem | +1.3% | Global (North America, Europe, APAC) | Long-term (2027-2033) |

| Growth in Emerging Markets (LatAm, SEA, India, MEA) | +1.1% | Latin America, Southeast Asia, India, MEA | Long-term (2025-2033) |

| Cloud Gaming Optimization & Peripheral Demand | +0.9% | Global (with strong internet infrastructure) | Mid-term (2026-2030) |

| Development of Sustainable & Modular Hardware | +0.7% | Europe, North America, Japan | Long-term (2028-2033) |

Video Gaming Hardware Market Challenges Impact Analysis

The Video Gaming Hardware market faces several persistent challenges that demand strategic responses from industry players. One significant challenge is the ongoing issue of component shortages and price volatility, particularly for critical semiconductors and raw materials. Geopolitical tensions, natural disasters, and unexpected spikes in demand can disrupt global supply chains, leading to manufacturing delays, increased production costs, and ultimately, higher retail prices for consumers. This instability makes forecasting and inventory management exceptionally difficult for hardware manufacturers, impacting profitability and market stability. Another formidable challenge is the intense competition within the market, not only among established hardware manufacturers but also from alternative entertainment forms and the burgeoning mobile gaming sector. This fierce competition necessitates continuous innovation and substantial investment in research and development to maintain a competitive edge, placing considerable pressure on profit margins and market share.

Moreover, concerns regarding e-waste and the environmental impact of hardware production and disposal represent a growing challenge. As global environmental regulations become stricter and consumer awareness about sustainability increases, manufacturers are under pressure to adopt more eco-friendly production processes, utilize recycled materials, and design products for extended lifespans or easier recycling. This shift requires significant investment in new technologies and adherence to complex compliance standards. The rapid pace of technological advancements, while a driver, also poses a challenge in terms of ensuring backward compatibility for older games and peripherals, as well as managing the high research and development costs associated with staying at the forefront of innovation. Furthermore, issues such as intellectual property infringement, counterfeiting, and ensuring robust cybersecurity for networked gaming devices continue to present ongoing hurdles for the industry, demanding proactive measures and collaborative efforts.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Component Shortages & Supply Chain Volatility | -0.9% | Global | Short to Mid-term (2025-2027) |

| Intense Competition & Price Pressure | -0.7% | Global | Long-term (2025-2033) |

| Environmental Concerns & E-Waste Management | -0.6% | Europe, North America, Japan (Highly Regulated Regions) | Long-term (2028-2033) |

| Ensuring Backward Compatibility & Future-proofing | -0.5% | Global | Mid-term (2026-2030) |

Video Gaming Hardware Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Video Gaming Hardware market, encompassing historical data, current market dynamics, and future projections. It delves into the multifaceted aspects of the market, including its size, growth drivers, restraints, opportunities, and challenges. The scope covers various hardware types, components, and end-user applications across key geographical regions, offering a holistic view for stakeholders to make informed strategic decisions. The report also highlights the significant impact of emerging technologies like AI and VR/AR on market evolution, alongside critical trends shaping consumer demand and technological innovation.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 65.2 billion |

| Market Forecast in 2033 | USD 181.4 billion |

| Growth Rate | 13.7% CAGR |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Sony Corporation, Microsoft Corporation, Nintendo Co. Ltd., NVIDIA Corporation, Advanced Micro Devices (AMD), Intel Corporation, Razer Inc., Logitech International S.A., Corsair Gaming, Inc., SteelSeries ApS, HP Inc. (Omen), Dell Technologies (Alienware), ASUSTek Computer Inc. (Republic of Gamers), Acer Inc. (Predator), HTC Corporation, Valve Corporation, Meta Platforms Inc., Pimax Technology Co. Ltd., HyperX (HP Subsidiary), Audeze LLC. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Video Gaming Hardware market is meticulously segmented to provide a granular understanding of its diverse components and consumer base, enabling targeted strategic planning. These segmentations allow for a detailed analysis of market dynamics across different hardware types, underlying components, end-user applications, and distribution channels. Understanding these segments is crucial for identifying specific growth pockets, tailoring product development, and optimizing market entry strategies for various regions and consumer demographics. The inherent versatility of gaming hardware, ranging from dedicated consoles to modular PC components and specialized peripherals, necessitates this comprehensive breakdown to capture the market's full scope and potential.

Each segment exhibits unique growth drivers and competitive landscapes. For instance, the console segment is largely driven by cyclical releases and exclusive game titles, while the PC hardware segment is characterized by continuous technological upgrades and a robust modding community. Peripherals, on the other hand, benefit from both casual and professional gaming demands for enhanced immersion and competitive advantage. The application-based segmentation further differentiates between personal consumer use and commercial applications like esports arenas, each with distinct requirements for durability, performance, and scale. Finally, the distribution channel analysis highlights the evolving preferences between online retail convenience and the tactile experience offered by offline stores, influencing sales strategies and market reach across the globe.

- By Type: Covers Gaming Consoles (e.g., PlayStation, Xbox, Nintendo Switch), Handheld Consoles, Gaming PCs (Desktops & Laptops), Peripherals (Controllers, VR/AR Headsets, Keyboards, Mice, Monitors, Headsets), and Arcade Machines.

- By Component: Focuses on the internal hardware, including Processors (CPUs, GPUs), Memory (RAM, SSDs), Motherboards, Power Supply Units, and Cooling Systems, highlighting the underlying technology driving performance.

- By Application/End-Use: Distinguishes between Personal/Individual Gaming (consumer market) and Commercial Gaming (esports centers, gaming cafes, arcades, and other entertainment venues).

- By Distribution Channel: Analyzes sales pathways, including Online Retail (e-commerce platforms, brand direct sales) and Offline Retail (specialty electronics stores, hypermarkets, and supermarkets).

Regional Highlights

- North America: A mature market characterized by high disposable incomes, strong adoption of high-end gaming PCs and consoles, and a thriving esports scene. The region leads in terms of early adoption of new technologies like VR and premium peripherals. Significant presence of key industry players and strong digital infrastructure supports sustained growth and high average revenue per user (ARPU).

- Europe: Diverse market with strong presence of both console and PC gaming. Western European countries exhibit high penetration rates for advanced gaming hardware, driven by a strong gaming culture and competitive esports. Eastern Europe is an emerging market with increasing internet penetration and rising disposable incomes fueling demand for both new and refurbished hardware.

- Asia Pacific (APAC): The largest and fastest-growing regional market, primarily driven by countries like China, Japan, South Korea, and India. China and South Korea are global hubs for esports and PC gaming, driving immense demand for high-performance hardware. India and Southeast Asian countries represent significant growth opportunities due to their large youth populations, increasing smartphone penetration, and rising interest in gaming, leading to demand for affordable and mid-range hardware. Japan remains a powerhouse for console and handheld gaming innovation.

- Latin America: An emerging market experiencing rapid growth due to improving internet infrastructure, increasing urbanization, and a burgeoning middle class. Console gaming is particularly popular, but PC gaming is also gaining traction, especially in countries like Brazil and Mexico. The region offers significant potential for market expansion for hardware manufacturers.

- Middle East and Africa (MEA): A nascent but rapidly growing market, particularly in the GCC countries (Saudi Arabia, UAE) due to high youth populations, government investments in digital infrastructure, and increasing disposable incomes. Console gaming dominates, but PC gaming and esports are gaining momentum. Africa presents long-term growth opportunities as internet access and economic development improve.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Video Gaming Hardware Market.- Sony Corporation

- Microsoft Corporation

- Nintendo Co. Ltd.

- NVIDIA Corporation

- Advanced Micro Devices (AMD)

- Intel Corporation

- Razer Inc.

- Logitech International S.A.

- Corsair Gaming, Inc.

- SteelSeries ApS

- HP Inc. (Omen)

- Dell Technologies (Alienware)

- ASUSTek Computer Inc. (Republic of Gamers)

- Acer Inc. (Predator)

- HTC Corporation

- Valve Corporation

- Meta Platforms Inc.

- Pimax Technology Co. Ltd.

- HyperX (HP Subsidiary)

- Audeze LLC

Frequently Asked Questions

Analyze common user questions about the Video Gaming Hardware market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the projected growth rate of the Video Gaming Hardware Market?

The Video Gaming Hardware Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 13.7% from 2025 to 2033, reaching an estimated value of USD 181.4 billion by the end of the forecast period.

What are the primary drivers of the Video Gaming Hardware Market?

Key drivers include continuous technological advancements in GPUs and CPUs, the increasing global popularity of esports and competitive gaming, rising disposable incomes in emerging markets, and the expanding global gaming user base facilitated by digital distribution platforms.

How does AI impact the Video Gaming Hardware Market?

AI significantly impacts the market through technologies like AI-powered upscaling (e.g., DLSS, FSR) for enhanced visual performance, intelligent hardware optimization for efficiency, and advanced in-game AI that demands more powerful processing, influencing future hardware design.

Which regions are expected to show significant growth in the Video Gaming Hardware Market?

Asia Pacific (APAC), particularly China, South Korea, India, and Southeast Asia, is expected to exhibit the fastest growth. Latin America and parts of the Middle East and Africa also present substantial emerging market opportunities due to increasing internet penetration and rising gaming interest.

What are the main challenges faced by the Video Gaming Hardware Market?

Major challenges include persistent component shortages and supply chain volatility, intense market competition leading to price pressure, growing environmental concerns related to e-waste, and the ongoing need to balance performance with energy efficiency while ensuring backward compatibility.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted