Vehicle Augmented Reality Market

Vehicle Augmented Reality Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_706955 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

Vehicle Augmented Reality Market Size

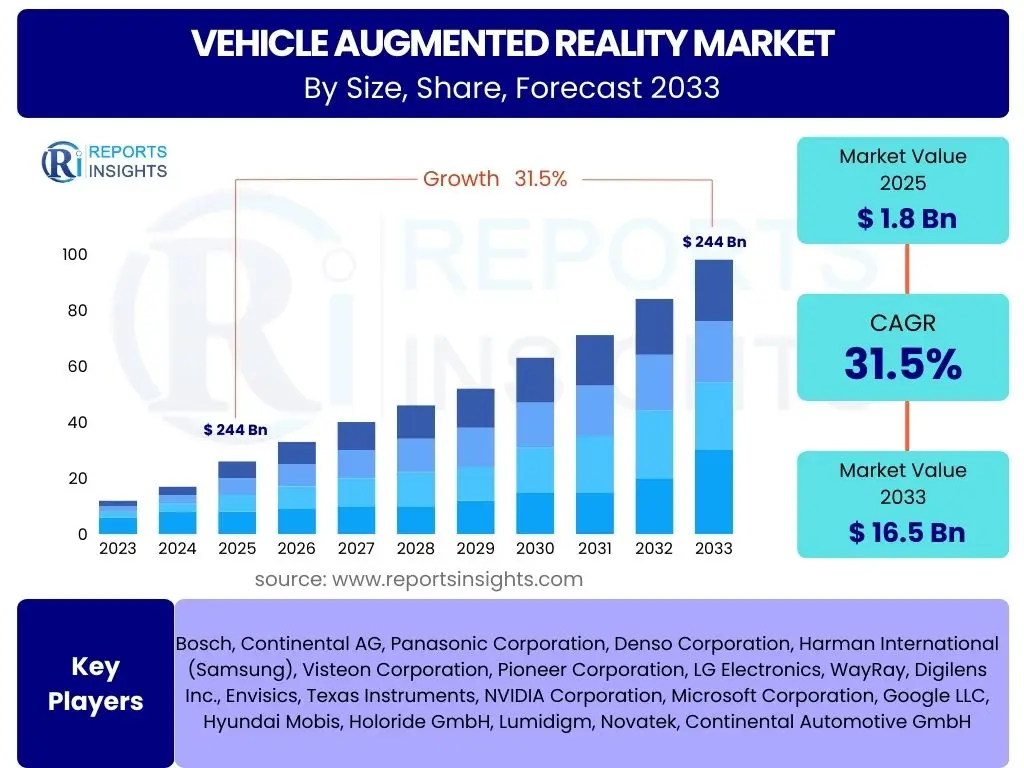

According to Reports Insights Consulting Pvt Ltd, The Vehicle Augmented Reality Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 31.5% between 2025 and 2033. The market is estimated at USD 1.8 billion in 2025 and is projected to reach USD 16.5 billion by the end of the forecast period in 2033.

Key Vehicle Augmented Reality Market Trends & Insights

The Vehicle Augmented Reality (VAR) market is undergoing significant transformation, driven by advancements in display technologies, sensor fusion, and sophisticated software algorithms. Consumer demand for enhanced in-car experiences, coupled with stringent safety regulations, is accelerating the adoption of AR systems in vehicles. These systems are moving beyond basic head-up displays (HUDs) to integrate complex real-time information onto the driver's field of vision, offering intuitive navigation, advanced driver-assistance system (ADAS) overlays, and immersive infotainment.

A notable trend is the integration of VAR with connected car ecosystems, enabling vehicles to communicate with infrastructure and other vehicles to provide more precise and context-aware AR overlays. This includes real-time traffic updates, pedestrian warnings, and parking assistance augmented directly onto the windshield or dedicated AR displays. Furthermore, the push towards autonomous vehicles is fostering the development of AR systems that can enhance human-machine interface (HMI), providing passengers with situational awareness even when the vehicle is driving itself, thereby increasing trust and comfort.

Another emerging insight is the increasing emphasis on personalization and customization of AR interfaces. Manufacturers are exploring ways to allow drivers to tailor the information displayed, its format, and its prominence, catering to individual preferences and reducing cognitive load. The convergence of 5G connectivity, cloud computing, and advanced graphics processing units (GPUs) is paving the way for more sophisticated and high-fidelity AR experiences, blurring the lines between the digital and physical driving environments.

- Advanced HUDs with wider field of view and higher resolution.

- Integration with ADAS for enhanced safety features and intuitive warnings.

- Development of personalized and customizable AR interfaces.

- Convergence with connected car technologies and 5G networks.

- Focus on passenger-centric AR experiences in autonomous vehicles.

- Real-time object recognition and semantic segmentation for improved contextual data.

AI Impact Analysis on Vehicle Augmented Reality

Artificial Intelligence (AI) serves as a foundational technology for the next generation of Vehicle Augmented Reality systems, addressing critical challenges related to real-time data processing, contextual understanding, and user interaction. AI algorithms are crucial for analyzing vast streams of sensor data from cameras, radar, lidar, and GPS, enabling AR systems to accurately detect, classify, and track objects in the vehicle's environment. This capability is essential for generating precise and relevant AR overlays for navigation, collision warnings, and pedestrian detection, enhancing both safety and situational awareness for drivers.

Beyond perception, AI plays a pivotal role in optimizing the information displayed through AR interfaces. Machine learning models can predict driver intent, anticipate potential hazards, and personalize the content presented based on driving conditions, driver behavior, and preferences. For instance, AI can prioritize critical safety alerts over general navigation cues during high-stress driving situations, or dynamically adjust the transparency and placement of AR elements to avoid visual clutter. This intelligent filtering and presentation of data are vital for ensuring that AR systems augment, rather than distract, the driver.

Furthermore, AI-powered natural language processing and computer vision are enabling more intuitive human-machine interaction within VAR. Drivers can use voice commands or even gaze tracking to interact with AR elements, asking for information about points of interest or controlling vehicle functions. AI also facilitates the continuous learning and improvement of AR systems, allowing them to adapt to diverse driving environments and user needs over time, leading to more robust and reliable augmented experiences. The symbiotic relationship between AI and VAR is central to the future evolution of intelligent and highly interactive in-car environments.

- Enhanced real-time object detection and tracking for accurate overlays.

- Contextual understanding and predictive analytics for relevant information display.

- Personalization of AR content based on driver behavior and preferences.

- Improved sensor fusion for comprehensive environmental mapping.

- Facilitation of intuitive human-machine interaction through voice and gaze.

- Adaptive learning capabilities for continuous system improvement.

Key Takeaways Vehicle Augmented Reality Market Size & Forecast

The Vehicle Augmented Reality market is poised for substantial growth over the next decade, driven by its transformative potential to redefine the driving experience. The significant projected CAGR underscores a robust and expanding demand for solutions that enhance safety, improve navigation, and enrich in-car entertainment. Key stakeholders, including automotive manufacturers, technology providers, and content developers, are actively investing in research and development to bring more advanced and integrated AR capabilities to mainstream vehicles, moving beyond luxury segment offerings.

The market's expansion is not merely about incremental improvements but rather a fundamental shift towards more intelligent and context-aware vehicle interfaces. The integration of advanced sensors, AI processing, and high-resolution displays will enable AR systems to provide highly intuitive and actionable information to drivers and passengers. This trend is further supported by evolving regulatory landscapes that encourage the adoption of technologies enhancing road safety, positioning AR as a critical component of future automotive ecosystems.

Looking ahead, the market's trajectory indicates a strong potential for new business models, including subscription-based services for AR content and feature upgrades. The increasing sophistication of AR hardware and software will lead to greater penetration across various vehicle segments, from premium to mid-range. The collaborative efforts between automotive OEMs and AR technology specialists will be crucial in overcoming technical complexities and ensuring a seamless, high-performance user experience, cementing AR's role as a cornerstone of smart mobility.

- Substantial market growth projected with a high CAGR, indicating strong demand.

- VAR's critical role in enhancing vehicle safety, navigation, and infotainment.

- Increasing investment and collaboration among automotive and tech companies.

- Shift towards intelligent, context-aware, and personalized in-car interfaces.

- Potential for new business models, including AR content subscriptions.

- Expected wider adoption across diverse vehicle segments.

Vehicle Augmented Reality Market Drivers Analysis

The increasing emphasis on road safety and the rapid advancements in ADAS technologies are primary drivers for the Vehicle Augmented Reality market. AR systems, by superimposing critical information such as lane departure warnings, collision alerts, and navigation instructions directly onto the driver's field of view, significantly reduce reaction times and enhance situational awareness. This integration helps mitigate risks associated with traditional dashboard displays that require drivers to divert their gaze from the road, thereby contributing to a safer driving experience and meeting evolving safety regulations.

Consumer demand for enhanced in-car experiences also plays a crucial role in driving market growth. Modern vehicle owners seek more intuitive, engaging, and personalized interactions with their vehicles. VAR systems offer an immersive way to consume infotainment, visualize navigation, and access vehicle diagnostics without significant distraction. The perceived value addition, particularly in premium and luxury vehicle segments, where advanced technology features are a key differentiator, is pushing automotive manufacturers to integrate sophisticated AR solutions.

Furthermore, the ongoing digitalization of the automotive industry and the proliferation of connected vehicle ecosystems provide a fertile ground for AR adoption. As vehicles become more connected, generating vast amounts of data from internal and external sensors, AR can serve as an effective interface to present this complex information in an easily digestible and actionable format. This confluence of safety mandates, consumer expectations, and technological integration collectively propels the expansion of the Vehicle Augmented Reality market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Focus on Road Safety & ADAS Integration | +8.2% | North America, Europe, Asia Pacific | Short-term to Mid-term |

| Growing Consumer Demand for Enhanced In-car Experience | +6.5% | Global, particularly developed economies | Mid-term |

| Advancements in Display Technologies & Connectivity (5G) | +7.8% | Global | Short-term to Long-term |

| Rising Adoption of Autonomous and Semi-Autonomous Vehicles | +5.9% | North America, Europe, China | Mid-term to Long-term |

Vehicle Augmented Reality Market Restraints Analysis

One significant restraint on the Vehicle Augmented Reality market is the high initial cost associated with developing and integrating advanced AR hardware and software components. The sophisticated display technologies, high-precision sensors, and powerful processing units required for seamless and accurate AR overlays represent a substantial investment for automotive manufacturers. This elevated cost often translates into a higher final price for consumers, limiting the widespread adoption of VAR systems primarily to premium and luxury vehicle segments, thus hindering market penetration into the mass market.

Another considerable challenge pertains to the technical complexities and integration challenges involved in fitting AR systems into diverse vehicle architectures. Ensuring precise calibration, real-time synchronization with vehicle dynamics, and seamless integration with existing in-car electronic systems requires extensive engineering effort. Issues such as latency, image distortion, and accurate projection onto curved windshields present significant hurdles. Furthermore, ensuring the reliability and durability of AR components in varying environmental conditions (e.g., extreme temperatures, vibrations) adds to the development complexity and cost.

Potential for driver distraction also remains a key concern and a significant restraint. While AR aims to enhance safety, poorly designed or overly complex AR interfaces could inadvertently increase cognitive load and visual distraction for drivers, particularly in critical driving situations. Regulatory bodies and consumers alike are vigilant about technologies that might compromise road safety. Addressing this perception and ensuring that AR systems genuinely augment the driving experience without creating new hazards requires careful design, extensive testing, and adherence to evolving safety standards, adding a layer of caution to market expansion.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Development and Integration Costs | -4.5% | Global | Short-term to Mid-term |

| Technical Complexities and Performance Challenges (Latency, Accuracy) | -3.8% | Global | Short-term to Mid-term |

| Potential for Driver Distraction and Regulatory Scrutiny | -2.1% | North America, Europe | Short-term to Mid-term |

| Limited Standardization and Interoperability | -1.7% | Global | Mid-term |

Vehicle Augmented Reality Market Opportunities Analysis

The expansion into the mass-market segment presents a significant opportunity for the Vehicle Augmented Reality market. Currently, VAR is predominantly found in high-end vehicles due to cost constraints. However, as production volumes increase, manufacturing processes become more efficient, and display technologies become more affordable, there is a substantial opportunity to integrate basic to mid-range AR features into mid-tier and entry-level vehicles. This democratized access will dramatically expand the potential customer base and drive economies of scale, leading to further price reductions and wider adoption.

Another key opportunity lies in the development of specialized AR applications beyond traditional navigation and safety. This includes immersive infotainment for passengers, personalized maintenance alerts, real-time diagnostic overlays, and even gamified driving experiences. With the advent of highly autonomous vehicles, AR can transform the passenger cabin into a dynamic interactive space, offering entertainment, productivity tools, and even virtual tours of the surrounding environment, thereby creating entirely new revenue streams and value propositions for vehicle owners.

Furthermore, the aftermarket segment offers a robust growth opportunity. While factory-installed AR systems are gaining traction, there is a burgeoning market for retrofit AR solutions, particularly for older vehicles or those lacking advanced features. Companies specializing in aftermarket HUDs and AR-enabled dash cams can cater to a wider audience seeking to upgrade their existing vehicles with enhanced safety and convenience features without purchasing a new car. This segment can leverage lower-cost solutions and flexible installation options to capture a significant portion of the market not served by OEM integrations.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Expansion into Mass-Market and Mid-Tier Vehicle Segments | +7.0% | Global, particularly Asia Pacific | Mid-term to Long-term |

| Development of Advanced and Diversified AR Applications (e.g., Infotainment) | +6.2% | Global | Mid-term to Long-term |

| Growth of Aftermarket AR Solutions and Retrofit Installations | +4.9% | Global | Short-term to Mid-term |

| Strategic Partnerships between OEMs and Tech Innovators | +3.5% | North America, Europe, Asia Pacific | Short-term to Long-term |

Vehicle Augmented Reality Market Challenges Impact Analysis

A significant challenge impacting the Vehicle Augmented Reality market is the need for highly precise and reliable data synchronization in real-time. For AR overlays to be effective and safe, they must accurately correspond with the physical environment as perceived by the driver, with minimal latency. Any lag or misalignment between the digital projection and the real world can lead to disorientation, cognitive overload, or even safety hazards. Achieving this level of precision requires sophisticated sensor fusion, powerful edge computing, and robust communication protocols, which are technically complex and expensive to implement consistently across varied driving conditions.

The issue of human factors and user acceptance also presents a considerable challenge. While AR offers compelling benefits, there is a learning curve for drivers to adapt to augmented displays, and individual preferences for information density and presentation vary widely. Over-saturation of information or poorly designed interfaces can lead to visual clutter and cognitive distraction, counteracting the intended safety benefits. Ensuring that AR systems are intuitive, non-intrusive, and genuinely enhance the driving experience without overwhelming the driver is crucial for widespread acceptance and requires extensive user interface/user experience (UI/UX) research and iterative design.

Lastly, regulatory and standardization complexities pose a substantial hurdle. As VAR technology evolves, governments and industry bodies are working to establish guidelines for display content, brightness, placement, and safety features to prevent distraction and ensure interoperability. The absence of comprehensive, globally harmonized standards can slow down development, increase compliance costs for manufacturers, and create market fragmentation. Addressing these regulatory uncertainties and working towards universal best practices will be essential for the seamless integration and scaling of Vehicle Augmented Reality solutions across different regions and vehicle types.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Real-time Data Accuracy and Latency Management | -3.0% | Global | Short-term to Mid-term |

| Human Factors and User Acceptance (Distraction, Cognitive Load) | -2.5% | Global | Short-term to Mid-term |

| Regulatory Frameworks and Standardization | -2.0% | North America, Europe, Asia Pacific | Mid-term |

| High Power Consumption of AR Systems | -1.5% | Global | Short-term |

Vehicle Augmented Reality Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the Vehicle Augmented Reality market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. It aims to equip stakeholders with a thorough understanding of the current market scenario and future growth opportunities, leveraging a robust methodology for accurate forecasting and trend identification.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.8 Billion |

| Market Forecast in 2033 | USD 16.5 Billion |

| Growth Rate | 31.5% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Bosch, Continental AG, Panasonic Corporation, Denso Corporation, Harman International (Samsung), Visteon Corporation, Pioneer Corporation, LG Electronics, WayRay, Digilens Inc., Envisics, Texas Instruments, NVIDIA Corporation, Microsoft Corporation, Google LLC, Hyundai Mobis, Holoride GmbH, Lumidigm, Novatek, Continental Automotive GmbH |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Vehicle Augmented Reality market is comprehensively segmented to provide a granular understanding of its various facets and growth trajectories across different product offerings, technological implementations, and end-use applications. This segmentation allows for a detailed analysis of market penetration, adoption rates, and revenue generation opportunities within each specific category. Understanding these segments is crucial for stakeholders to identify niche markets, tailor product development, and formulate targeted marketing strategies.

The segmentation by component differentiates between the tangible hardware elements necessary for AR projection and data processing, and the sophisticated software that powers the AR experience. Display type segmentation further breaks down the market by the method of AR presentation, with Head-up Displays currently dominating but advanced AR displays gaining traction. Application-based segmentation highlights the diverse functionalities of VAR, from critical safety features to passenger entertainment, indicating varied adoption drivers for each use case.

Furthermore, the market is categorized by vehicle type, recognizing the different needs and integration possibilities across passenger and commercial vehicles, as well as distinct sub-segments within passenger vehicles like luxury versus economy cars. The segmentation by level of autonomous driving acknowledges the evolving role of AR in vehicles with varying degrees of autonomy, from driver-centric systems in semi-autonomous vehicles to passenger-centric experiences in fully autonomous ones. This multi-dimensional approach to segmentation offers a holistic view of the market’s intricate structure and potential for expansion.

- By Component: Hardware (Projectors/Combiners, Sensors, Processing Units, Software), Software (AR Platforms, Application Software)

- By Display Type: Head-up Displays (HUD) (Windshield-based, Combiner-based), AR Displays (Transparent Displays, Head-mounted Displays for testing/development)

- By Application: Navigation, Advanced Driver Assistance Systems (ADAS), Infotainment, Vehicle Telematics, Parking Assistance, Predictive Maintenance

- By Vehicle Type: Passenger Vehicles (Luxury, Mid-Range, Economy), Commercial Vehicles

- By Level of Autonomous Driving: Semi-Autonomous Vehicles, Fully Autonomous Vehicles

- By Offering: Hardware, Software, Services

Regional Highlights

- North America: Expected to hold a significant market share due to the strong presence of major automotive OEMs and technology companies, high consumer disposable income, and increasing adoption of advanced vehicle technologies. Early adoption of ADAS and autonomous driving features further propels the market.

- Europe: Anticipated to be a key market for Vehicle Augmented Reality, driven by stringent safety regulations, a strong luxury automotive sector, and significant investments in smart mobility initiatives. Germany, France, and the UK are leading countries in this region.

- Asia Pacific (APAC): Projected to exhibit the highest growth rate, primarily due to the rapid expansion of the automotive manufacturing sector in countries like China, Japan, South Korea, and India. Increasing demand for connected cars, rising consumer awareness, and government initiatives supporting technological adoption contribute to this growth.

- Latin America: Emerging market with growing potential, characterized by increasing vehicle sales and a gradual shift towards modern in-car technologies. Brazil and Mexico are key contributors to market growth in this region.

- Middle East and Africa (MEA): Expected to show steady growth, influenced by rising disposable incomes, urbanization, and government initiatives aimed at modernizing transportation infrastructure. Adoption of luxury and technologically advanced vehicles in countries like UAE and Saudi Arabia drives demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Vehicle Augmented Reality Market.- Bosch

- Continental AG

- Panasonic Corporation

- Denso Corporation

- Harman International (Samsung)

- Visteon Corporation

- Pioneer Corporation

- LG Electronics

- WayRay

- Digilens Inc.

- Envisics

- Texas Instruments

- NVIDIA Corporation

- Microsoft Corporation

- Google LLC

- Hyundai Mobis

- Holoride GmbH

- Lumidigm

- Novatek

- Continental Automotive GmbH

Frequently Asked Questions

What is Vehicle Augmented Reality (VAR)?

Vehicle Augmented Reality (VAR) is a technology that overlays digital information, such as navigation directions, speed, and safety alerts, onto the driver's real-world view of the road, typically via a windshield or a dedicated transparent display, to enhance driving safety, awareness, and convenience.

How large is the Vehicle Augmented Reality market expected to be by 2033?

The Vehicle Augmented Reality market is projected to reach approximately USD 16.5 billion by the end of 2033, growing at a significant Compound Annual Growth Rate (CAGR) from its 2025 valuation.

What are the primary drivers of the Vehicle Augmented Reality market?

Key drivers include the increasing focus on road safety and integration with Advanced Driver-Assistance Systems (ADAS), growing consumer demand for enhanced in-car experiences, and continuous advancements in display technologies and connectivity like 5G.

What are the main challenges for the Vehicle Augmented Reality market?

Major challenges encompass the high initial development and integration costs, technical complexities related to real-time data accuracy and latency, potential for driver distraction, and the evolving landscape of regulatory frameworks and standardization.

Which regions are leading the adoption of Vehicle Augmented Reality?

North America and Europe currently lead in market share due to technological maturity and consumer demand, while the Asia Pacific region, particularly China and Japan, is expected to exhibit the highest growth rate due to rapid automotive sector expansion and increasing technological adoption.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted