VCSEL Laser Market

VCSEL Laser Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_710047 | Last Updated : December 29, 2025 |

Format : ![]()

![]()

![]()

![]()

VCSEL Laser Market Size

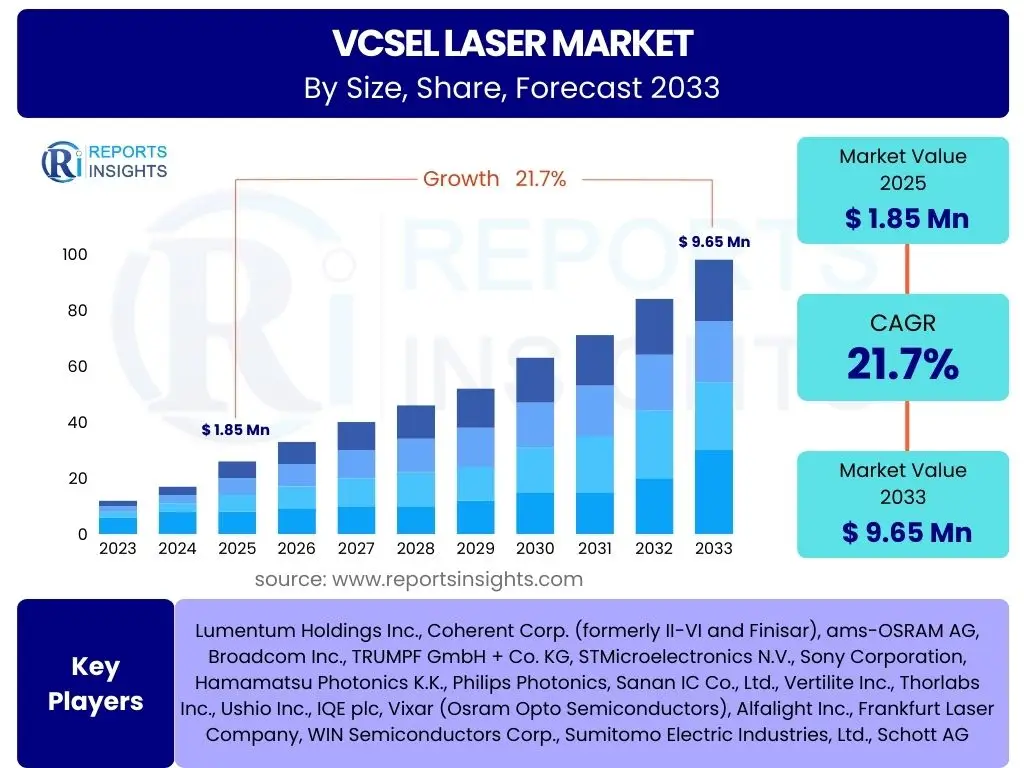

According to Reports Insights Consulting Pvt Ltd, The VCSEL Laser Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.7% between 2025 and 2033. The market is estimated at USD 1.85 Billion in 2025 and is projected to reach USD 9.65 Billion by the end of the forecast period in 2033.

Key VCSEL Laser Market Trends & Insights

The VCSEL (Vertical Cavity Surface Emitting Laser) market is undergoing significant transformation, driven by advancements in miniaturization, power efficiency, and multi-junction designs. Users frequently inquire about the trajectory of VCSEL technology, pointing to its increasing integration into sophisticated 3D sensing systems for consumer electronics and automotive applications. The demand for higher data rates in optical communication and hyperscale data centers is also a pivotal trend, propelling innovation in VCSEL arrays and advanced modulation techniques. Furthermore, there is a growing interest in the expansion of VCSELs beyond traditional applications, exploring new frontiers in medical diagnostics, industrial heating, and emerging quantum technologies, indicating a diversification of its end-use landscape and a strong emphasis on customizable solutions.

The industry is observing a shift towards enhanced spectral efficiency and temperature stability, critical for reliable performance in demanding environments such as autonomous vehicles and augmented reality devices. This focus on performance optimization, coupled with a drive towards cost-effective manufacturing processes, underpins much of the ongoing research and development. The integration of VCSELs with other photonic components on a single chip, often referred to as photonic integrated circuits (PICs), represents another key trend, promising further reductions in size, power consumption, and overall system complexity, which will open doors to even broader adoption.

- Proliferation of 3D Sensing in Consumer Electronics: Facial recognition, gesture control, and augmented reality (AR) applications.

- Rapid Expansion in Data Communication: High-speed optical transceivers for data centers and enterprise networks.

- Increasing Adoption in Automotive LiDAR: Enhanced safety features for advanced driver-assistance systems (ADAS) and autonomous vehicles.

- Emergence of Multi-Junction VCSELs: Improved power efficiency and higher output for demanding applications.

- Miniaturization and Integration: Development of smaller, more integrated VCSEL modules for compact devices.

- New Medical and Industrial Applications: Use in blood glucose monitoring, industrial heating, and precise material processing.

- Advancements in Wavelength Diversity: Exploration of new wavelengths for diverse sensing and communication needs.

AI Impact Analysis on VCSEL Laser

Artificial intelligence is profoundly influencing the VCSEL laser market by acting as both a driver and an enabler for advanced applications. User inquiries often highlight AI's role in boosting demand for high-speed, low-latency data transmission, which VCSELs are uniquely positioned to provide in data centers and intra-device communication. AI's reliance on massive datasets and intensive computational processes necessitates infrastructure that can handle rapid data flow, directly stimulating the need for high-performance optical interconnects, where VCSELs are a preferred choice. Furthermore, AI algorithms are instrumental in optimizing the design, manufacturing, and quality control of VCSELs themselves, leading to more efficient and reliable devices.

Beyond data infrastructure, AI-powered applications, particularly in autonomous systems and advanced robotics, are driving the demand for sophisticated 3D sensing capabilities. VCSELs, with their compact size, excellent beam quality, and rapid modulation, are foundational components for depth perception and environmental mapping in these AI-driven systems. Users are keenly interested in how AI's continuous evolution, from machine learning in consumer devices to deep learning in industrial automation, will further expand the application scope and performance requirements for VCSEL technology, pushing innovation towards higher power, greater precision, and novel integration strategies for AI at the edge.

- Accelerated Demand for High-Speed Data Centers: AI workloads require faster data transfer, increasing VCSEL use in optical transceivers.

- Enhanced 3D Sensing in AI-Driven Devices: VCSELs enable depth sensing for facial recognition, gesture control, and robotic vision.

- Automotive Perception for Autonomous Vehicles: AI-powered ADAS and LiDAR systems rely on VCSELs for environmental mapping.

- Optimized VCSEL Design and Manufacturing: AI algorithms used for material science, process control, and performance prediction.

- Edge AI Computing Requirements: VCSELs support low-latency communication in distributed AI architectures.

- Advanced Medical Imaging and Diagnostics: AI-assisted medical devices leveraging VCSELs for non-invasive sensing.

Key Takeaways VCSEL Laser Market Size & Forecast

The VCSEL laser market is poised for robust and sustained growth, driven primarily by its integral role in high-growth technology sectors. A key takeaway for users is the market's strong correlation with the proliferation of 3D sensing applications in consumer electronics and the accelerating expansion of hyperscale data centers. The forecast indicates that while existing applications will continue to mature, significant future growth will stem from emerging opportunities in automotive LiDAR, advanced industrial sensing, and potentially novel medical diagnostic tools, underscoring the technology's versatile and foundational nature. This diversification reduces reliance on any single application, offering a resilient growth trajectory.

Furthermore, the market's expansion is not merely quantitative but also qualitative, with continuous innovation in VCSEL design and manufacturing processes leading to higher performance, greater efficiency, and reduced costs. Stakeholders should note the increasing importance of strategic partnerships and vertical integration to secure supply chains and capitalize on application-specific customization. The competitive landscape is intensifying, necessitating agile responses to technological shifts and market demands, with successful players focusing on both volume production for consumer markets and high-performance solutions for specialized industrial and automotive segments.

- Strong Growth Trajectory: Sustained high CAGR driven by fundamental technological shifts across multiple industries.

- Diversified Application Portfolio: Reliance on a broad range of applications from consumer to industrial and automotive.

- Technological Innovation as a Core Driver: Continuous advancements in efficiency, power, and spectral range.

- Strategic Importance of 3D Sensing: Remains a primary growth engine, especially in consumer and automotive sectors.

- Critical for Data Infrastructure: Essential component for next-generation high-speed optical communication.

- Intensifying Competition: Market characterized by both established players and emerging innovators.

- Regional Growth Pockets: Asia Pacific and North America are expected to lead in adoption and manufacturing.

VCSEL Laser Market Drivers Analysis

The exponential demand for advanced 3D sensing capabilities in various sectors represents a primary driver for the VCSEL laser market. Consumer electronics, particularly smartphones, have widely adopted VCSELs for facial recognition, augmented reality (AR) applications, and gesture sensing. This widespread integration has familiarized consumers with the technology and continues to push manufacturers to innovate in terms of size, power efficiency, and cost-effectiveness, creating a virtuous cycle of demand and supply. The precision and compact nature of VCSELs make them ideal for these high-volume, performance-critical applications, establishing them as an indispensable component.

Another significant driver is the relentless growth of data communication, particularly within hyperscale data centers and cloud computing infrastructure. As data traffic continues to surge globally, driven by AI, IoT, and streaming services, the need for high-speed, energy-efficient optical interconnects becomes paramount. VCSELs offer superior performance for short-reach optical links (up to 500 meters) compared to edge-emitting lasers (EELs), providing lower power consumption, higher bandwidth density, and easier integration with silicon photonics. Their ability to operate at high modulation frequencies and form dense arrays makes them the preferred choice for intra-data center communication, fueling substantial demand.

Furthermore, the burgeoning automotive industry is increasingly integrating VCSELs for advanced driver-assistance systems (ADAS) and autonomous driving. LiDAR systems, crucial for environmental mapping and obstacle detection, are adopting VCSEL arrays for their robustness, temperature stability, and ability to emit high-power pulses. As the automotive industry moves towards higher levels of autonomy, the demand for reliable and precise sensing solutions, heavily reliant on VCSEL technology, is set to escalate dramatically. The convergence of these powerful trends positions VCSELs at the forefront of several transformative technological shifts.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Adoption of 3D Sensing in Consumer Electronics | +4.5% | North America, Asia Pacific (China, South Korea) | Short to Mid-term (2025-2030) |

| Growing Demand for High-Speed Data Communication in Data Centers | +3.8% | Global (USA, Europe, China) | Mid to Long-term (2025-2033) |

| Expansion of Automotive LiDAR and ADAS Systems | +3.2% | Europe (Germany), North America, Asia Pacific (Japan) | Mid to Long-term (2026-2033) |

| Emergence of New Applications in Medical and Industrial Sectors | +2.0% | Global, especially developed economies | Long-term (2028-2033) |

VCSEL Laser Market Restraints Analysis

Despite the robust growth, the VCSEL laser market faces several restraints that could temper its expansion. One significant challenge is the relatively higher manufacturing cost for certain specialized VCSELs, particularly those requiring advanced packaging or custom wavelengths, compared to conventional edge-emitting lasers (EELs) for some applications. While high-volume production for consumer electronics has driven down costs for standard VCSELs, niche applications still contend with economies of scale challenges. This cost sensitivity can deter adoption in price-sensitive markets or for applications where performance advantages do not sufficiently outweigh the initial investment.

Another restraint pertains to the power output limitations of single VCSEL emitters. While VCSEL arrays can achieve high optical power, individual emitters typically have lower power output compared to EELs. This can be a limitation for applications requiring very high beam intensity or longer-range sensing without complex array configurations. Thermal management also presents a constraint, as high-power VCSEL arrays generate significant heat, which can degrade performance and reduce device lifetime if not effectively dissipated. Designing efficient cooling solutions for compact VCSEL modules adds complexity and cost, particularly in space-constrained applications like portable devices or automotive sensors.

Furthermore, the competitive landscape includes established alternative technologies. For instance, in long-haul optical communication, EELs (especially Distributed Feedback lasers, DFB) remain dominant due to their higher output power and narrower spectral linewidth. While VCSELs excel in short-reach applications, their suitability for distances beyond 500 meters decreases, limiting their addressable market in certain segments. Additionally, supply chain vulnerabilities, particularly for critical raw materials and specialized manufacturing equipment, can pose risks to production consistency and cost stability, especially in a dynamic global geopolitical environment. These factors collectively require strategic mitigation efforts from market participants.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs for Niche Applications | -1.5% | Global, particularly emerging markets | Short to Mid-term (2025-2029) |

| Limited Power Output of Single Emitters and Thermal Management | -1.2% | Global, especially high-power applications | Mid-term (2026-2031) |

| Competition from Alternative Laser Technologies (e.g., EELs) | -0.9% | Global, specific to long-haul communication | Mid to Long-term (2025-2033) |

| Supply Chain Vulnerabilities and Geopolitical Risks | -0.7% | Global, particularly regions dependent on specific suppliers | Short to Mid-term (2025-2030) |

VCSEL Laser Market Opportunities Analysis

The VCSEL laser market is rich with opportunities stemming from the ongoing evolution of several high-tech industries. One significant avenue lies in the expansion of augmented reality (AR) and virtual reality (VR) devices. These immersive technologies require highly compact, efficient, and precise 3D sensing capabilities for hand tracking, eye tracking, and environmental mapping. VCSELs, with their small footprint and fast modulation speeds, are perfectly suited to meet these stringent requirements, paving the way for advanced human-computer interaction and more realistic virtual experiences. As AR/VR moves from niche to mainstream, the demand for integrated VCSEL solutions will surge.

Another substantial opportunity is found in the next generation of industrial automation and robotics. The need for precise real-time object detection, quality control, and human-machine collaboration in smart factories is driving the adoption of sophisticated vision systems. VCSELs offer superior performance for structured light applications, time-of-flight (ToF) sensors, and industrial LiDAR, enabling robots to navigate complex environments and perform intricate tasks with greater accuracy and safety. The industry's move towards Industry 4.0 and autonomous manufacturing processes will increasingly rely on these advanced sensing solutions.

Furthermore, the emergence of quantum computing and advanced medical diagnostics presents long-term, high-value opportunities. In quantum computing, VCSELs could play a role in trapping ions or cooling atoms, requiring highly stable and precise laser sources. In healthcare, their compact size and specific wavelengths are being explored for non-invasive blood glucose monitoring, dermatological treatments, and advanced imaging techniques. These frontier applications, while currently in early stages of adoption, represent areas where VCSELs could provide unique advantages and unlock entirely new market segments, demonstrating the technology's potential for transformational impact beyond its current dominant applications.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration into Augmented Reality (AR) and Virtual Reality (VR) Devices | +3.0% | North America, Europe, Asia Pacific | Mid to Long-term (2027-2033) |

| Expansion in Industrial Automation and Robotics | +2.5% | Europe (Germany), Asia Pacific (Japan, China), North America | Mid to Long-term (2026-2032) |

| Development of New Medical and Healthcare Applications | +1.8% | Global, particularly developed healthcare markets | Long-term (2029-2033) |

| Adoption in Quantum Computing and Advanced Scientific Research | +1.0% | Global research hubs | Long-term (2030-2033) |

VCSEL Laser Market Challenges Impact Analysis

The VCSEL laser market faces several inherent challenges that require innovative solutions and strategic planning. One prominent challenge is the complexity of integrating VCSELs into diverse systems, particularly when moving beyond standardized consumer electronics applications. Each new application often demands custom optical designs, drive electronics, and thermal management solutions, increasing development time and cost. The need for specialized packaging to meet varying environmental requirements, such as those in automotive or industrial settings, adds further layers of complexity, posing a significant hurdle for rapid market expansion and widespread adoption.

Another critical challenge lies in ensuring consistent high-power output and long-term reliability across various operating conditions, especially for emerging applications like automotive LiDAR. VCSEL performance can be sensitive to temperature fluctuations, and ensuring stable operation over a wide temperature range and extended lifetimes in harsh environments is technically demanding. Achieving uniform emission across large VCSEL arrays without significant power drop-off or thermal crosstalk also presents an engineering challenge. These reliability and performance consistency issues can hinder adoption in mission-critical applications where failure rates must be exceptionally low.

Furthermore, the market faces challenges related to standardization and the availability of a skilled workforce. The rapid pace of VCSEL technology development means that industry-wide standards for interfaces, packaging, and testing methodologies are still evolving, leading to fragmentation and potentially slowing down interoperability and mass production. Concurrently, there is a growing demand for engineers and technicians with expertise in optoelectronics, semiconductor manufacturing, and advanced photonics, leading to a talent gap that could limit innovation and manufacturing capacity. Addressing these integration, reliability, and human capital challenges will be crucial for the sustained growth and maturity of the VCSEL market.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Complex Integration and Customization for Diverse Applications | -1.0% | Global, particularly niche markets | Short to Mid-term (2025-2029) |

| Ensuring High Reliability and Performance Consistency in Harsh Environments | -0.8% | Automotive, Industrial, and Military sectors | Mid-term (2026-2031) |

| Lack of Industry Standardization and Interoperability | -0.6% | Global | Mid to Long-term (2027-2033) |

| Talent Shortage in Optoelectronics and Photonics Engineering | -0.5% | North America, Europe, parts of Asia Pacific | Short to Long-term (2025-2033) |

VCSEL Laser Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global VCSEL Laser market, covering historical data from 2019 to 2023, with a detailed forecast extending from 2025 to 2033. The scope includes an assessment of market size, growth drivers, restraints, opportunities, and challenges, segmented across various types, wavelengths, applications, and end-user industries. It offers strategic insights into regional dynamics and competitive landscape, enabling stakeholders to make informed decisions and capitalize on emerging trends. The report also integrates an impact analysis of AI and highlights key takeaways from market size and forecast data.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.85 Billion |

| Market Forecast in 2033 | USD 9.65 Billion |

| Growth Rate | 21.7% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Lumentum Holdings Inc., Coherent Corp. (formerly II-VI and Finisar), ams-OSRAM AG, Broadcom Inc., TRUMPF GmbH + Co. KG, STMicroelectronics N.V., Sony Corporation, Hamamatsu Photonics K.K., Philips Photonics, Sanan IC Co., Ltd., Vertilite Inc., Thorlabs Inc., Ushio Inc., IQE plc, Vixar (Osram Opto Semiconductors), Alfalight Inc., Frankfurt Laser Company, WIN Semiconductors Corp., Sumitomo Electric Industries, Ltd., Schott AG |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The segmentation of the VCSEL laser market provides a granular view of its diverse applications and technological variations, which is crucial for understanding specific market dynamics and growth pockets. This detailed breakdown allows for a more precise analysis of demand drivers, competitive strategies, and regional opportunities. By categorizing the market based on VCSEL type, wavelength, primary application, and end-user industry, stakeholders can identify high-growth segments and tailor their product development and marketing efforts accordingly. The versatility of VCSEL technology across these segments underscores its importance as a foundational component in the modern technological landscape.

- By Type

- Multimode VCSELs: Primarily used for short-reach data communication and certain 3D sensing applications.

- Single-mode VCSELs: Preferred for high-precision sensing, longer-reach communication, and advanced instrumentation.

- By Wavelength

- 850 nm: Dominant in data communication and consumer 3D sensing.

- 940 nm: Widely adopted for proximity sensing and some automotive applications due to reduced sunlight interference.

- 1310 nm: Emerging for longer-reach optical links and specific industrial uses.

- 1550 nm: Explored for automotive LiDAR and medical applications, offering better eye safety.

- Others: Custom wavelengths for specialized scientific or industrial applications.

- By Application

- Data Communication: Fiber optic transceivers for data centers, enterprise networks.

- 3D Sensing: Facial recognition, gesture control, augmented reality in consumer electronics.

- Industrial Heating: Precision heating and drying processes.

- Medical: Blood glucose monitoring, dermatological treatments, advanced imaging.

- Automotive: LiDAR, in-cabin sensing, ADAS.

- Consumer Electronics: Proximity sensing, autofocus, TrueDepth cameras.

- Others: Military, aerospace, scientific research.

- By End-User

- IT & Telecom: Data centers, telecommunication networks, cloud infrastructure.

- Automotive: Car manufacturers, automotive component suppliers.

- Industrial: Manufacturing, automation, robotics.

- Healthcare: Medical device manufacturers, diagnostic equipment.

- Consumer Goods: Smartphone manufacturers, wearable devices, gaming.

Regional Highlights

- North America: Expected to hold a significant market share due to the strong presence of major technology companies, high R&D investments, and early adoption of advanced technologies in data centers, consumer electronics, and autonomous vehicles. The United States is a key contributor, leading in innovation and application development.

- Europe: Demonstrates substantial growth, particularly in the automotive and industrial sectors. Germany, with its robust automotive manufacturing base and focus on Industry 4.0, is a prominent market. Increasing investment in optical communication infrastructure also fuels demand.

- Asia Pacific (APAC): Projected to be the fastest-growing region, driven by the massive consumer electronics manufacturing base in China, South Korea, and Japan. Rapid expansion of data centers, growing automotive industry, and government initiatives promoting advanced technologies contribute significantly to market expansion. China leads in both production and consumption.

- Latin America: Represents an emerging market with gradual adoption of VCSEL technology, primarily in consumer electronics and expanding data center infrastructure. Growth is anticipated as digital transformation accelerates across the region.

- Middle East and Africa (MEA): Shows nascent growth, with increasing investments in smart city projects and digital infrastructure. Adoption of VCSELs is expected to rise with enhanced connectivity and industrial diversification efforts, though from a smaller base.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the VCSEL Laser Market.- Lumentum Holdings Inc.

- Coherent Corp. (formerly II-VI and Finisar)

- ams-OSRAM AG

- Broadcom Inc.

- TRUMPF GmbH + Co. KG

- STMicroelectronics N.V.

- Sony Corporation

- Hamamatsu Photonics K.K.

- Philips Photonics

- Sanan IC Co., Ltd.

- Vertilite Inc.

- Thorlabs Inc.

- Ushio Inc.

- IQE plc

- Vixar (Osram Opto Semiconductors)

- Alfalight Inc.

- Frankfurt Laser Company

- WIN Semiconductors Corp.

- Sumitomo Electric Industries, Ltd.

- Schott AG

Frequently Asked Questions

Analyze common user questions about the VCSEL Laser market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a VCSEL laser?

A VCSEL (Vertical Cavity Surface Emitting Laser) is a type of semiconductor laser diode that emits light perpendicularly from the wafer surface, unlike edge-emitting lasers which emit from the edge. This design allows for easier integration into arrays, high efficiency, and compact size.

What are the primary applications of VCSELs?

VCSELs are predominantly used in 3D sensing for consumer electronics (facial recognition, gesture control), high-speed data communication in data centers, and emerging automotive LiDAR for autonomous vehicles. They also find applications in medical devices and industrial sensing.

How do VCSELs differ from Edge-Emitting Lasers (EELs)?

VCSELs emit light vertically from the wafer surface, allowing for easy testing at the wafer level, array integration, and typically lower power consumption for short-reach applications. EELs emit light from the chip's edge, often offering higher output power and suitability for longer-reach, high-power communication.

What is the growth forecast for the VCSEL Laser Market?

The VCSEL Laser Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 21.7% between 2025 and 2033, reaching an estimated USD 9.65 Billion by 2033, driven by increasing demand from 3D sensing and data communication sectors.

What are the key technological advancements expected in VCSELs?

Key advancements include the development of multi-junction VCSELs for higher power and efficiency, wider wavelength ranges for diverse applications, enhanced temperature stability, and improved integration with silicon photonics for compact, high-performance modules, particularly for AR/VR and advanced automotive systems.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted