Vacuum Valve Market

Vacuum Valve Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708948 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

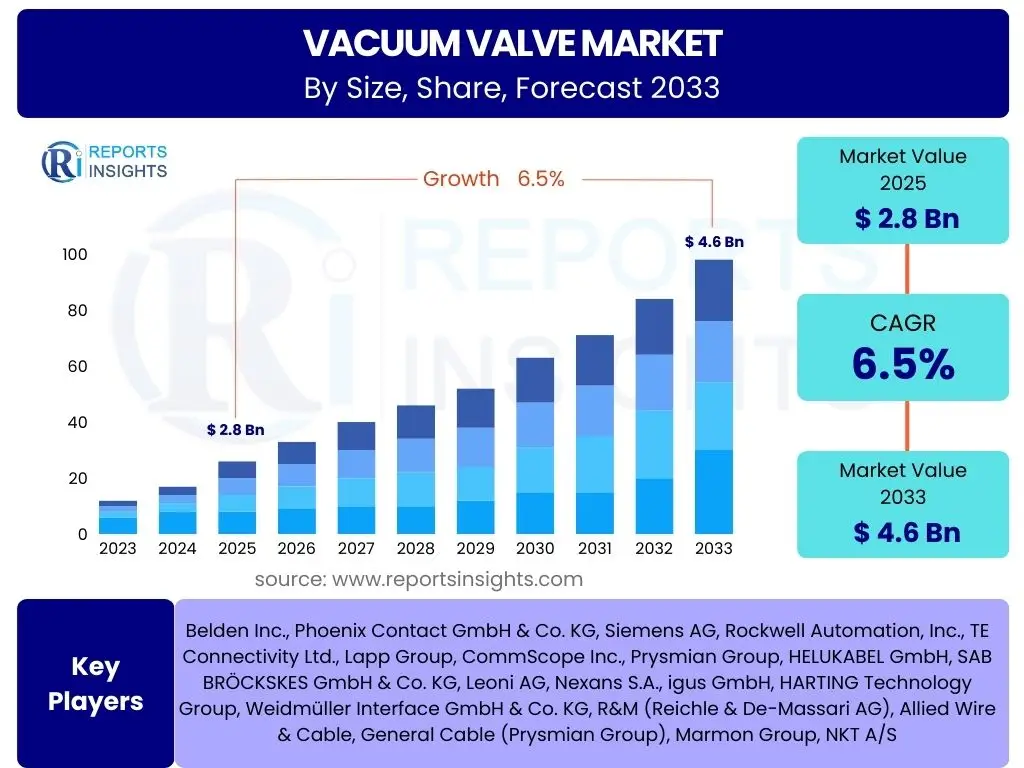

Vacuum Valve Market Size

According to Reports Insights Consulting Pvt Ltd, The Vacuum Valve Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 2.8 Billion in 2025 and is projected to reach USD 4.6 Billion by the end of the forecast period in 2033. This growth is primarily driven by expanding applications in high-tech industries requiring precise vacuum control and the continuous demand for advanced manufacturing processes.

The consistent expansion of the semiconductor industry, coupled with increasing investments in research and development across various scientific fields, underpins this robust growth. Furthermore, the rising adoption of vacuum technologies in emerging markets and the push for greater automation and efficiency in industrial processes globally are significant factors contributing to the market's upward trajectory. Despite potential economic fluctuations, the fundamental need for controlled vacuum environments in critical applications ensures sustained market momentum.

Key Vacuum Valve Market Trends & Insights

Users frequently inquire about the latest innovations, technological advancements, and evolving industry shifts that are shaping the vacuum valve market. Analysis reveals a strong interest in how these trends impact performance, efficiency, and application versatility. Key themes include the integration of smart technologies, advancements in material science for enhanced durability, and the increasing demand for specialized valves tailored to specific industrial processes, particularly within the semiconductor and pharmaceutical sectors. There is also a growing emphasis on energy efficiency and compact designs to meet modern industrial requirements.

Furthermore, inquiries often touch upon the globalization of manufacturing, the push for more sustainable operational practices, and the impact of geopolitical factors on supply chains. The market is observing a pivot towards more sophisticated control mechanisms and real-time monitoring capabilities, driven by the broader Industry 4.0 movement. This includes a focus on predictive maintenance and longer operational lifespans, minimizing downtime and reducing overall operational costs for end-users. These trends collectively underscore a market moving towards greater intelligence, efficiency, and specialization.

- Integration of smart features and IoT for remote monitoring and predictive maintenance.

- Development of advanced materials for enhanced corrosion resistance and extreme temperature operation.

- Miniaturization of vacuum valves to support compact system designs in various applications.

- Increasing demand for ultra-high vacuum (UHV) and extreme ultra-high vacuum (XUHV) capabilities.

- Emphasis on energy-efficient designs and sustainable manufacturing practices.

- Growing adoption of modular designs for easier maintenance and customization.

- Expansion of specialized valve solutions for niche applications like cryogenics and additive manufacturing.

AI Impact Analysis on Vacuum Valve

Common user questions regarding AI's impact on the vacuum valve sector center on how artificial intelligence can optimize valve design, enhance manufacturing processes, improve operational efficiency through predictive analytics, and enable more sophisticated control systems. Users are keen to understand if AI can lead to more reliable valves, reduce maintenance costs, and provide real-time performance insights. The general expectation is that AI will introduce a new paradigm of smart, autonomous, and highly efficient vacuum valve systems capable of self-diagnosis and adaptive control.

Beyond operational improvements, there are expectations that AI will play a crucial role in accelerating material discovery for valve components and in simulating complex vacuum environments to optimize valve placement and type selection. Concerns often revolve around data security, the complexity of integrating AI into existing infrastructure, and the need for a skilled workforce capable of managing these advanced systems. Despite these challenges, the consensus is that AI will be a transformative force, leading to next-generation vacuum valve solutions that are more intelligent, robust, and cost-effective over their lifecycle.

- AI-driven predictive maintenance for vacuum valves, minimizing downtime and optimizing service schedules.

- Enhanced design and simulation capabilities using AI to optimize valve geometries for flow and sealing performance.

- Automated quality control and inspection in manufacturing processes, reducing defects and improving consistency.

- Real-time performance monitoring and anomaly detection, allowing for proactive intervention.

- Intelligent control systems that adapt valve operation based on dynamic process parameters and environmental conditions.

- Supply chain optimization through AI, ensuring efficient procurement and delivery of valve components.

- Potential for AI to personalize valve functionality based on specific application requirements.

Key Takeaways Vacuum Valve Market Size & Forecast

User inquiries about key takeaways from the vacuum valve market size and forecast consistently point to a desire for concise, actionable insights regarding market trajectory, growth catalysts, and future investment areas. The core interest lies in understanding the principal factors driving the market's expansion, identifying segments poised for significant growth, and recognizing potential challenges or opportunities that could alter the forecast. Users seek a clear distillation of complex market data into readily understandable strategic implications.

The insights derived indicate that the market is on a robust growth path, primarily propelled by the semiconductor industry's insatiable demand for advanced process control and the continuous innovation in scientific research and industrial applications. While emerging economies present significant opportunities, the persistent need for high-performance and reliable vacuum solutions across established industries ensures stable demand. Understanding these dynamics is crucial for stakeholders aiming to capitalize on the market's long-term potential and navigate its evolving landscape effectively.

- The Vacuum Valve Market is set for consistent growth, driven largely by the semiconductor and advanced manufacturing sectors.

- Technological innovation, particularly in smart and ultra-high vacuum valves, will be a primary growth enabler.

- Asia Pacific is expected to remain a dominant and rapidly growing region due to manufacturing expansion.

- Investments in R&D and specialized applications will open new revenue streams and market niches.

- Supply chain resilience and material advancements are crucial for sustained market expansion.

Vacuum Valve Market Drivers Analysis

The vacuum valve market is experiencing significant tailwinds from several key factors that are bolstering demand across various industries. Foremost among these is the escalating growth of the semiconductor manufacturing industry, which heavily relies on precise vacuum control for deposition, etching, and other critical processes. Additionally, the increasing global investment in research and development, particularly in fields like nanotechnology, material science, and high-energy physics, necessitates sophisticated vacuum systems, thereby driving the demand for advanced vacuum valves. The expansion of the food and beverage processing sector and the pharmaceutical industry, both requiring sterile and controlled environments, further contributes to this growth by increasing the need for hygienic and reliable vacuum solutions.

Furthermore, the ongoing trend of industrial automation and the integration of Industry 4.0 technologies are pushing for more intelligent and automated vacuum valve systems capable of seamless integration into complex manufacturing lines. This shift towards smart factories emphasizes efficiency, precision, and remote control, making advanced vacuum valves indispensable. The development of new and advanced materials for valve construction, offering enhanced durability, corrosion resistance, and performance in extreme conditions, also acts as a significant driver by expanding the applicability and lifespan of these critical components. These intertwined drivers collectively foster a robust and expanding market environment for vacuum valves.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Surging Demand from Semiconductor Manufacturing | +2.1% | Asia Pacific (China, Taiwan, South Korea, Japan), North America, Europe | Long-term (2025-2033) |

| Increasing Investments in Research & Development | +1.7% | North America, Europe, Asia Pacific (Global) | Long-term (2025-2033) |

| Growth in Food & Beverage and Pharmaceutical Industries | +1.3% | Global, particularly emerging economies | Mid-to-Long-term (2027-2033) |

| Advancements in Industrial Automation and Industry 4.0 | +1.1% | North America, Europe, Asia Pacific | Mid-term (2026-2031) |

| Development of Advanced Materials for Valve Construction | +0.8% | Global, particularly R&D hubs | Long-term (2028-2033) |

Vacuum Valve Market Restraints Analysis

Despite the positive growth trajectory, the vacuum valve market faces several significant restraints that could temper its expansion. One primary challenge is the high initial investment cost associated with advanced vacuum valve systems, especially for ultra-high vacuum applications or those requiring specialized materials. This cost can be prohibitive for smaller enterprises or for industries operating on tight budgetary constraints, potentially limiting adoption rates. Furthermore, the market is subject to stringent regulatory standards and certifications, particularly in sectors like pharmaceuticals, aerospace, and nuclear, which adds to manufacturing complexity and compliance costs, thereby impacting market accessibility and innovation cycles.

Another notable restraint is the vulnerability of the global supply chain, which can be disrupted by geopolitical events, trade disputes, or pandemics, leading to material shortages and increased lead times for critical components. This instability directly affects production schedules and delivery, creating uncertainty for both manufacturers and end-users. Additionally, the demand for highly skilled labor for the installation, operation, and maintenance of complex vacuum systems poses a significant challenge. A shortage of such expertise can slow down the adoption of advanced vacuum technologies and increase operational costs, acting as a decelerating force on market growth. These factors collectively require strategic mitigation efforts from market participants to sustain growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment and Equipment Costs | -1.2% | Global, particularly developing economies | Long-term (2025-2033) |

| Stringent Regulatory Standards and Certifications | -0.9% | Europe, North America, Japan | Long-term (2025-2033) |

| Supply Chain Vulnerabilities and Geopolitical Risks | -0.8% | Global interconnected economies | Mid-term (2025-2029) |

| Shortage of Skilled Labor for Installation & Maintenance | -0.7% | Global, particularly highly industrialized regions | Long-term (2025-2033) |

Vacuum Valve Market Opportunities Analysis

The vacuum valve market presents substantial opportunities driven by evolving technological landscapes and expanding industrial needs. The emergence of new applications in industries such as additive manufacturing (3D printing), space simulation, and cryogenics creates novel demand for specialized vacuum valves capable of operating under extreme conditions and with high precision. These developing sectors require custom-engineered solutions that push the boundaries of current valve technology, opening avenues for innovation and market penetration. Furthermore, the increasing focus on energy efficiency and environmental sustainability across global industries provides an opportunity for manufacturers to develop and market greener vacuum valve solutions that consume less power and have a reduced environmental footprint, appealing to environmentally conscious enterprises and regulations.

Another significant opportunity lies in the burgeoning market for Internet of Things (IoT) integration and smart factory initiatives. The demand for vacuum valves equipped with advanced sensors, connectivity, and real-time data analytics capabilities is growing, enabling predictive maintenance, remote diagnostics, and optimized operational performance. This trend allows manufacturers to offer value-added services and move towards more sophisticated product offerings. Additionally, the rapid industrialization and technological advancements in emerging economies, particularly in Asia Pacific and Latin America, present vast untapped markets for vacuum valve manufacturers. As these regions continue to invest in high-tech manufacturing and research infrastructure, the demand for reliable and efficient vacuum solutions is expected to surge, creating lucrative growth opportunities.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emergence of New Applications (e.g., Additive Manufacturing, Space Simulation) | +1.5% | Global, particularly North America, Europe, Asia Pacific | Long-term (2026-2033) |

| Growing Demand for IoT Integration and Smart Factory Solutions | +1.2% | North America, Europe, Asia Pacific (highly industrialized regions) | Mid-to-Long-term (2027-2033) |

| Focus on Energy Efficiency and Sustainable Vacuum Solutions | +0.9% | Global, especially Europe and North America | Mid-term (2025-2030) |

| Expansion into Untapped Markets in Emerging Economies | +1.0% | Asia Pacific (Southeast Asia), Latin America, MEA | Long-term (2028-2033) |

Vacuum Valve Market Challenges Impact Analysis

The vacuum valve market faces several inherent challenges that require strategic navigation to ensure sustained growth. Intense market competition from both established global players and emerging regional manufacturers is a significant hurdle. This competitive landscape often leads to price pressures, reduced profit margins, and the need for continuous innovation to differentiate products, making it difficult for some companies to maintain market share or achieve desired growth rates. Additionally, the rapid pace of technological obsolescence in the high-tech industries that utilize vacuum valves means that products can quickly become outdated, necessitating constant investment in research and development to keep pace with evolving demands and maintain relevance.

Another critical challenge stems from the cyclical nature of key end-use industries, particularly the semiconductor and display manufacturing sectors. Economic downturns or oversupply in these industries can lead to significant reductions in capital expenditure, directly impacting the demand for new vacuum valve installations and upgrades. Furthermore, geopolitical instability, including trade wars, regional conflicts, and protectionist policies, can disrupt international supply chains, increase tariffs, and create uncertainty in market access, complicating global sales and distribution strategies. These challenges demand agility, resilience, and a forward-looking approach from market participants to mitigate risks and capitalize on opportunities effectively.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Intense Market Competition and Price Pressures | -1.0% | Global | Long-term (2025-2033) |

| Rapid Technological Obsolescence in End-Use Industries | -0.8% | Global, particularly semiconductor and electronics hubs | Long-term (2025-2033) |

| Cyclical Nature of Key End-Use Industries (e.g., Semiconductor) | -0.7% | Global (impacts major manufacturing regions) | Short-to-Mid-term (2025-2027) |

| Geopolitical Instability and Trade Barriers | -0.6% | Global, particularly regions with trade disputes | Mid-term (2025-2030) |

Vacuum Valve Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the global vacuum valve market, providing critical insights into its current size, historical performance, and future growth projections. The scope encompasses detailed segmentation analysis by valve type, operation, application, and end-use industry, along with a thorough regional breakdown to highlight key market dynamics across different geographies. The report further investigates key market trends, drivers, restraints, opportunities, and challenges, offering a holistic view for strategic decision-making. It aims to equip stakeholders with granular data and expert analysis essential for understanding market evolution and competitive landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.8 Billion |

| Market Forecast in 2033 | USD 4.6 Billion |

| Growth Rate | 6.5% |

| Number of Pages | 267 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | VAT Group, Pfeiffer Vacuum, Leybold GmbH, Kurt J. Lesker Company, SMC Corporation, MKS Instruments, Festo AG & Co. KG, Varian Medical Systems, GNB Corporation, Fujikin Inc., HVA LLC, Agilent Technologies, CKD Corporation, Nor-Cal Products Inc., Kitz Corporation, Emerson Electric Co., Parker Hannifin Corporation, Swagelok Company, Hitachi Ltd., WEIR Group PLC |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The vacuum valve market is meticulously segmented to provide a detailed understanding of its diverse landscape and specific growth avenues. This segmentation spans across various dimensions, including valve type, operational mechanism, specific application, and the myriad of end-use industries that rely on these critical components. Each segment offers unique insights into demand patterns, technological preferences, and regional adoption rates, allowing for a nuanced market assessment. Analyzing these distinct categories helps in identifying high-growth areas and tailoring strategic approaches to meet the specialized needs of different market verticals.

Understanding the interplay between these segments is crucial for market participants. For instance, the demand for gate valves and angle valves is particularly strong in semiconductor manufacturing due to their excellent sealing properties and high conductance, while diaphragm valves find extensive use in pharmaceutical and food processing for their hygienic design. Similarly, the shift towards automated processes is boosting the pneumatic and electric operation segments, reflecting the broader trend towards intelligent industrial control. This granular segmentation provides a robust framework for assessing market dynamics, competitive positioning, and future investment opportunities across the entire vacuum valve ecosystem.

- By Type:

- Gate Valves

- Angle Valves

- Ball Valves

- Butterfly Valves

- Diaphragm Valves

- Check Valves

- Solenoid Valves

- Others (e.g., Transfer Valves, Custom Valves)

- By Operation:

- Manual

- Pneumatic

- Electric

- Solenoid

- By Application:

- Isolation

- Flow Control

- Pressure Regulation

- Process Control

- Safety

- By End-Use Industry:

- Semiconductor & Electronics

- Research & Development (R&D)

- Food & Beverage

- Pharmaceutical & Biotechnology

- Chemical & Petrochemical

- Aerospace & Defense

- Packaging

- Others (e.g., Metallurgy, Automotive, Display Manufacturing)

Regional Highlights

- Asia Pacific (APAC): This region is anticipated to be the largest and fastest-growing market, primarily driven by the robust expansion of the semiconductor, electronics, and display manufacturing industries in countries like China, Taiwan, South Korea, and Japan. Significant government investments in R&D and industrial infrastructure further propel demand.

- North America: A mature market characterized by high adoption of advanced vacuum technologies in aerospace, defense, R&D, and pharmaceutical sectors. The United States accounts for a substantial share, with a focus on innovation and high-performance solutions.

- Europe: This region exhibits stable growth fueled by stringent regulatory environments in the pharmaceutical and food & beverage industries, coupled with strong manufacturing bases in Germany, the UK, and France. Emphasis on energy efficiency and sustainable practices drives demand for advanced valves.

- Latin America: An emerging market with growing industrialization and increasing investments in manufacturing and research facilities, particularly in Brazil and Mexico. While smaller in scale, it offers considerable long-term growth potential.

- Middle East & Africa (MEA): This region is characterized by rising investments in chemical, petrochemical, and scientific research infrastructure, particularly in the UAE and Saudi Arabia. Market growth is gradually accelerating as industrial diversification continues.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Vacuum Valve Market.- VAT Group

- Pfeiffer Vacuum

- Leybold GmbH

- Kurt J. Lesker Company

- SMC Corporation

- MKS Instruments

- Festo AG & Co. KG

- Varian Medical Systems

- GNB Corporation

- Fujikin Inc.

- HVA LLC

- Agilent Technologies

- CKD Corporation

- Nor-Cal Products Inc.

- Kitz Corporation

- Emerson Electric Co.

- Parker Hannifin Corporation

- Swagelok Company

- Hitachi Ltd.

- WEIR Group PLC

Frequently Asked Questions

What is a vacuum valve and what is its primary function?

A vacuum valve is a mechanical device designed to regulate, isolate, or control the flow of gases in a vacuum system, creating and maintaining specific vacuum levels. Its primary function is to seal off or open vacuum chambers, lines, or components to atmospheric pressure or other vacuum regions, enabling precise control over vacuum processes.

Which industries are the primary consumers of vacuum valves?

The semiconductor and electronics manufacturing industries are the largest consumers, utilizing vacuum valves for critical processes like deposition, etching, and ion implantation. Other significant industries include research and development (e.g., high-energy physics, material science), pharmaceutical and biotechnology, food and beverage processing, chemical and petrochemical, and aerospace.

What are the main types of vacuum valves available in the market?

Common types include gate valves for high conductance and isolation, angle valves for compact design and flow control, ball valves, butterfly valves for large diameters, diaphragm valves for hygienic applications, check valves for backflow prevention, and solenoid valves for automated control. Each type serves specific operational and application requirements.

How is technological advancement impacting the vacuum valve market?

Technological advancements are leading to smarter, more efficient, and specialized vacuum valves. This includes the integration of IoT for remote monitoring and predictive maintenance, development of advanced materials for extreme conditions, miniaturization for compact systems, and enhanced designs for ultra-high vacuum (UHV) capabilities, all driven by Industry 4.0 trends.

What is the forecast for the vacuum valve market's growth?

The vacuum valve market is projected for robust growth, with a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033, reaching an estimated USD 4.6 Billion by 2033. This growth is primarily fueled by the expanding semiconductor industry, increasing R&D investments, and rising demand for automation and precise vacuum control across various high-tech sectors globally.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted