Uranium Market

Uranium Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709629 | Last Updated : December 12, 2025 |

Format : ![]()

![]()

![]()

![]()

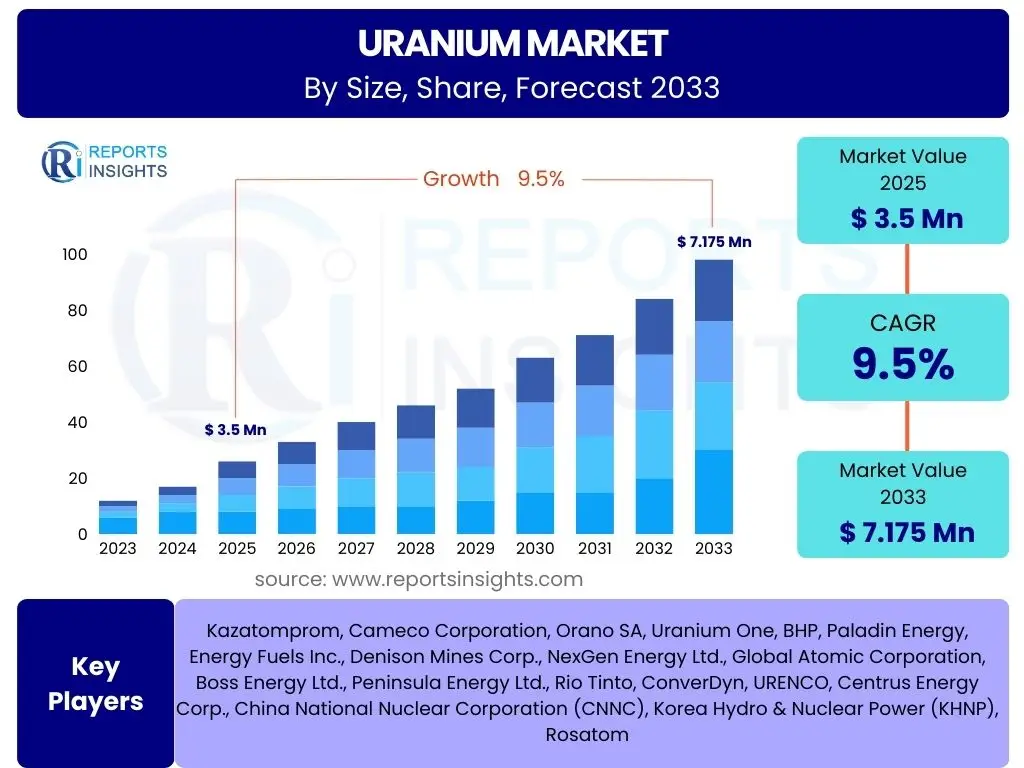

Uranium Market Size

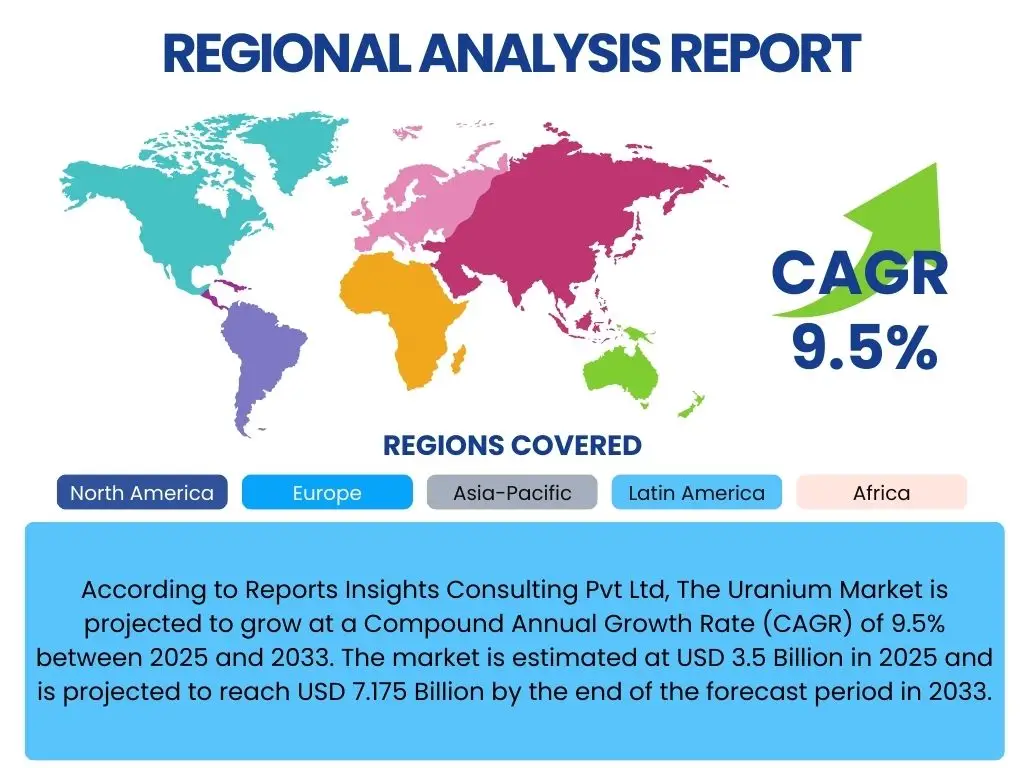

According to Reports Insights Consulting Pvt Ltd, The Uranium Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.5% between 2025 and 2033. The market is estimated at USD 3.5 Billion in 2025 and is projected to reach USD 7.175 Billion by the end of the forecast period in 2033.

Key Uranium Market Trends & Insights

The global uranium market is currently experiencing a significant resurgence, driven by a confluence of factors including increasing energy security concerns, a renewed global commitment to decarbonization, and advancements in nuclear reactor technology. Nations worldwide are re-evaluating nuclear power as a stable, low-carbon baseload energy source, moving away from a previous era of skepticism and phase-outs. This shift is primarily fueled by the imperative to reduce reliance on fossil fuels and achieve ambitious net-zero emission targets, positioning nuclear energy as a critical component of future energy mixes.

A notable trend is the growing interest and investment in Small Modular Reactors (SMRs) and advanced reactor designs. These innovative technologies offer numerous advantages, such as smaller footprints, reduced construction times, lower capital costs, and enhanced safety features, making nuclear power a more attractive and deployable option for a wider range of applications and locations. Furthermore, geopolitical developments and supply chain vulnerabilities have heightened awareness of the strategic importance of a secure and diverse uranium supply, leading to increased focus on domestic mining and diversified procurement strategies among consumer nations.

- Resurgence of nuclear power as a cornerstone for energy security and decarbonization goals.

- Accelerated development and deployment of Small Modular Reactors (SMRs) and advanced nuclear technologies.

- Heightened focus on securing diverse and stable uranium supply chains amidst geopolitical tensions.

- Increased government support and policy initiatives promoting nuclear energy expansion globally.

- Growing investor confidence and capital allocation towards uranium mining and nuclear infrastructure projects.

AI Impact Analysis on Uranium

The integration of Artificial intelligence (AI) is poised to significantly transform various facets of the uranium industry, from exploration and mining to processing, nuclear power plant operations, and safety protocols. Users frequently inquire about how AI can enhance efficiency, reduce costs, and mitigate risks within this highly specialized sector. AI-powered analytics can process vast geological datasets, including seismic, radiometric, and geochemical information, to identify potential uranium deposits with greater precision and speed than traditional methods. This leads to more efficient exploration campaigns, optimizing drilling targets and reducing the overall cost and environmental footprint of prospecting activities.

Furthermore, AI applications extend to the operational efficiency and safety of nuclear power generation. Predictive maintenance algorithms, trained on sensor data from reactor components, can anticipate equipment failures, enabling proactive interventions that minimize downtime and enhance plant safety. AI also plays a crucial role in optimizing the uranium fuel cycle, from monitoring enrichment processes to managing spent fuel. Concerns often revolve around the security of AI systems in critical infrastructure and the need for robust validation, but the overwhelming consensus points towards AI as a key enabler for a safer, more efficient, and more sustainable nuclear energy future.

- Optimized exploration and mining operations through advanced data analytics and predictive modeling for higher success rates and reduced costs.

- Enhanced efficiency and safety in nuclear power plants via AI-driven predictive maintenance, anomaly detection, and operational optimization.

- Improved supply chain management and logistics for uranium concentrate and nuclear fuel, ensuring reliability and reducing lead times.

- Accelerated research and development of new reactor designs, fuel formulations, and waste management solutions through AI-powered simulations and material science.

- Reinforced cybersecurity and physical security measures at nuclear facilities by leveraging AI for threat detection and response.

Key Takeaways Uranium Market Size & Forecast

The uranium market is experiencing robust growth, primarily driven by a global shift towards cleaner energy sources and the strategic imperative of energy independence. User inquiries often highlight the long-term viability and investment potential of uranium, given the anticipated increase in nuclear power capacity worldwide. The projected market expansion to USD 7.175 Billion by 2033, at a CAGR of 9.5%, underscores a strong and sustained demand outlook, reflecting confidence in nuclear energy's role in future power grids. This growth is not merely incremental but represents a fundamental re-evaluation of nuclear power's benefits, especially in the context of climate change and geopolitical instability.

A significant portion of this growth will be catalyzed by the widespread adoption of Small Modular Reactors (SMRs), which are set to democratize nuclear energy deployment and open new markets. The market forecast also signals a period of substantial investment across the entire nuclear fuel cycle, from increased mining activity to advancements in enrichment and fuel fabrication. While challenges related to regulatory hurdles and public perception persist, the overarching narrative is one of renewed optimism and strategic importance for uranium as a critical energy commodity.

- Strong and sustained market growth expected, reaching USD 7.175 Billion by 2033.

- Nuclear renaissance and decarbonization efforts are the primary growth accelerators.

- Small Modular Reactors (SMRs) are a pivotal technology driving future uranium demand.

- Heightened global focus on energy security strengthens uranium's strategic importance.

- Significant investment opportunities across the entire nuclear fuel cycle value chain.

Uranium Market Drivers Analysis

The uranium market is fundamentally driven by the global imperative to achieve decarbonization targets and enhance energy security. As nations commit to net-zero emissions, nuclear power offers a reliable, low-carbon baseload electricity source that can complement intermittent renewables. This renewed political and economic support for nuclear energy is translating into new reactor construction projects and the extension of operational lifespans for existing plants, directly increasing demand for uranium fuel. Moreover, the escalating geopolitical tensions and supply chain vulnerabilities have underscored the strategic necessity for diversified and stable energy sources, further cementing nuclear power's role in national energy policies.

A critical driver for future demand is the rapid advancement and deployment of Small Modular Reactors (SMRs) and other advanced nuclear technologies. SMRs promise to overcome many of the traditional barriers to nuclear power deployment, such as high upfront capital costs, long construction timelines, and large land requirements. Their modular design allows for factory fabrication and phased deployment, making nuclear power more flexible and accessible for various applications, including industrial heat, desalination, and remote power generation. This technological evolution is expanding the potential market for nuclear energy and, consequently, for uranium fuel, positioning it as a key element in the transition to a sustainable global energy system.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Global push for decarbonization and net-zero emissions targets. | +1.8% | Global, particularly Europe, North America, Asia Pacific | Long-term (2025-2033) |

| Increasing demand for nuclear energy as a reliable baseload power source. | +1.5% | Asia Pacific (China, India), North America (US), Europe (France, UK) | Mid to Long-term (2025-2033) |

| Development and deployment of Small Modular Reactors (SMRs) and advanced nuclear technologies. | +1.2% | North America, Europe, Asia Pacific (Canada, US, UK, South Korea) | Mid to Long-term (2027-2033) |

| Heightened energy security concerns and reduced reliance on fossil fuels. | +1.0% | Europe (Germany, Poland), Asia Pacific (Japan, South Korea) | Short to Mid-term (2025-2030) |

| Extension of operational lifespans for existing nuclear power plants. | +0.7% | North America, Europe | Short to Mid-term (2025-2030) |

Uranium Market Restraints Analysis

Despite the positive outlook, the uranium market faces several significant restraints that could temper its growth trajectory. High upfront capital costs and the notoriously long construction times associated with traditional large-scale nuclear power plants remain a considerable barrier to entry and expansion. These financial and temporal commitments deter potential investors and government agencies, particularly in regions where alternative energy projects might offer quicker returns or lower initial outlays. The complexity of nuclear projects also introduces significant project management challenges and risks of cost overruns, further complicating investment decisions.

Public perception and safety concerns, often stemming from historical nuclear accidents such as Chernobyl and Fukushima, continue to act as a potent restraint. These events have fostered a degree of public apprehension and skepticism towards nuclear energy, leading to strong anti-nuclear movements in some regions and stringent regulatory frameworks globally. While significant advancements in reactor safety have been made, overcoming entrenched public fears and navigating complex, often politically charged, regulatory and licensing processes pose ongoing challenges to market expansion. Moreover, the availability and perceived competitiveness of alternative energy sources, including increasingly cost-effective renewables and natural gas, can sometimes divert investment away from nuclear projects, particularly in markets with less emphasis on baseload reliability or carbon neutrality.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High upfront capital costs and long construction timelines for new nuclear power plants. | -1.5% | Global, particularly developing economies | Long-term (2025-2033) |

| Public perception and safety concerns following historical nuclear incidents. | -1.2% | Europe (Germany), North America (US) | Mid to Long-term (2025-2033) |

| Stringent regulatory frameworks, licensing processes, and political opposition. | -1.0% | Global, particularly Western countries | Long-term (2025-2033) |

| Availability and competitiveness of alternative energy sources (renewables, natural gas). | -0.8% | Global, particularly markets with abundant natural gas or high renewable integration | Short to Mid-term (2025-2030) |

| Challenges in radioactive waste management and disposal. | -0.7% | Global | Long-term (2025-2033) |

Uranium Market Opportunities Analysis

The uranium market is ripe with opportunities, particularly stemming from the global energy transition and technological innovation. One significant opportunity lies in the continuous development of advanced mining techniques and processing technologies. Innovations such as in-situ recovery (ISR) offer more environmentally friendly and cost-effective methods for extracting uranium, expanding the range of economically viable deposits. Further advancements in processing efficiency and reducing the environmental footprint of mining operations can enhance the overall sustainability and public acceptance of uranium extraction, making it more attractive for investment and reducing operational costs for producers.

Another substantial opportunity emerges from the expanding geographical reach of nuclear power. Emerging economies, particularly in Asia, Africa, and the Middle East, are increasingly exploring nuclear energy to meet their rapidly growing electricity demands, urbanize, and industrialize. These regions present new markets for reactor deployment and, consequently, for uranium fuel. Moreover, research and development into advanced fuel cycle technologies, including fuel reprocessing and the use of alternative fuel types, could optimize uranium utilization, reduce waste volumes, and enhance the long-term sustainability of nuclear power, thereby creating new value streams within the uranium market. The drive for energy independence in many countries also opens doors for new domestic uranium production or strategic international partnerships.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of new mining techniques (e.g., ISR) and processing technologies to enhance efficiency and reduce costs. | +1.0% | Global, particularly North America, Australia, Kazakhstan | Mid to Long-term (2026-2033) |

| Expansion into new geographic markets, particularly emerging economies with growing energy demands. | +0.9% | Asia Pacific (China, India), Africa, Middle East, Southeast Asia | Long-term (2028-2033) |

| Increased investment in nuclear research and development for next-generation reactors and fuel cycles. | +0.8% | North America, Europe, Asia Pacific | Mid to Long-term (2027-2033) |

| Potential for reprocessing of spent nuclear fuel and advancements in fuel recycling technologies. | +0.7% | Europe (France), Asia Pacific (Japan, China) | Long-term (2030-2033) |

| Leveraging nuclear power for non-electricity applications (e.g., industrial heat, hydrogen production, desalination). | +0.6% | Global | Long-term (2029-2033) |

Uranium Market Challenges Impact Analysis

The uranium market, while promising, is not without its significant challenges that could impede its growth and stability. Geopolitical instability and the concentration of uranium production in a few key countries pose substantial supply chain risks. Disruptions in major producing regions, or political tensions affecting transportation routes, can lead to price volatility and uncertainty in supply, impacting the operational stability of nuclear power plants globally. This dependency on specific regions for a critical resource necessitates robust strategic planning and diversification efforts by consumer nations to mitigate potential shocks.

Another persistent challenge is the long-term management and safe disposal of radioactive waste. This issue not only carries significant technical and financial burdens but also remains a major point of public and political contention, often hindering the social license for new nuclear projects. Finding universally accepted and scientifically sound solutions for waste disposal is crucial for the sustainable growth of the nuclear industry. Furthermore, the nuclear sector faces a challenge in ensuring a sufficient skilled workforce for the complex tasks of reactor construction, operation, and maintenance, as well as for specialized mining and fuel cycle activities. An aging workforce and a historical decline in nuclear engineering enrollments in some regions necessitate concerted efforts in education and training to prevent future labor shortages.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Geopolitical instability and supply chain disruptions affecting uranium prices and availability. | -1.8% | Global, particularly Europe and Asia (reliance on Kazakhstan, Niger) | Short to Mid-term (2025-2028) |

| Long-term management and permanent disposal of radioactive waste. | -1.2% | Global, particularly countries with extensive nuclear programs | Long-term (2025-2033) |

| Ensuring a sufficient skilled workforce for nuclear power plant construction and operation. | -0.9% | North America, Europe, Asia Pacific | Mid to Long-term (2026-2033) |

| High capital intensity and prolonged lead times for new uranium mining projects. | -0.7% | Global | Long-term (2025-2033) |

| Potential for uranium price volatility impacting investment decisions and market stability. | -0.6% | Global | Short to Mid-term (2025-2028) |

Uranium Market - Updated Report Scope

This report provides an in-depth analysis of the global uranium market, covering its size, growth trends, key drivers, restraints, opportunities, and challenges across various segments and geographic regions. It aims to offer comprehensive market intelligence for stakeholders involved in the nuclear energy sector, mining, and investment communities. The study focuses on understanding the evolving landscape of uranium supply and demand, the impact of technological advancements such as Small Modular Reactors (SMRs), and the influence of global energy policies and geopolitical factors. The analysis also incorporates the potential effects of Artificial Intelligence (AI) on operational efficiencies and future developments within the industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 3.5 Billion |

| Market Forecast in 2033 | USD 7.175 Billion |

| Growth Rate | 9.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Kazatomprom, Cameco Corporation, Orano SA, Uranium One, BHP, Paladin Energy, Energy Fuels Inc., Denison Mines Corp., NexGen Energy Ltd., Global Atomic Corporation, Boss Energy Ltd., Peninsula Energy Ltd., Rio Tinto, ConverDyn, URENCO, Centrus Energy Corp., China National Nuclear Corporation (CNNC), Korea Hydro & Nuclear Power (KHNP), Rosatom |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The uranium market is comprehensively segmented to provide a granular understanding of its dynamics across different product types, end-use applications, and reactor technologies. This detailed segmentation allows for a precise assessment of demand drivers and growth opportunities within specific niches of the nuclear fuel cycle. By analyzing these segments, stakeholders can identify key areas for investment, technological innovation, and strategic market positioning, tailoring their approaches to cater to distinct market requirements and regulatory environments.

Understanding these segmentations is critical for market participants, as it reveals the varying demand profiles and growth trajectories for different forms of uranium and its diverse applications beyond traditional power generation. The segmentation by reactor type, for instance, highlights the influence of evolving nuclear technologies, such as the rise of SMRs, on future fuel requirements and design specifications. This analytical framework offers a holistic view of the market structure and aids in forecasting future trends and competitive landscapes across the entire value chain.

- By Type:

- Natural Uranium

- Enriched Uranium

- Depleted Uranium

- By Application:

- Nuclear Fuel (for electricity generation)

- Medical Isotopes

- Counterweights (in aircraft, industrial applications)

- Ammunition (depleted uranium)

- Research and Development

- By Reactor Type:

- Pressurized Water Reactors (PWR)

- Boiling Water Reactors (BWR)

- Candu Reactors (Pressurized Heavy Water Reactors)

- Advanced Gas-Cooled Reactors (AGR)

- Fast Breeder Reactors (FBR)

- Small Modular Reactors (SMR)

- Other Advanced Reactors

Regional Highlights

- North America: This region is witnessing a significant nuclear renaissance, particularly in the United States and Canada. The US is actively pursuing reactor life extensions, new large-scale plant construction, and substantial investment in Small Modular Reactors (SMRs). Canada remains a pivotal global uranium producer and is also advancing SMR technology, solidifying its role in the future nuclear landscape. Energy security and decarbonization goals are driving increased governmental and private sector support.

- Europe: The European continent is undergoing a strategic shift, with several nations reconsidering or reversing nuclear phase-outs (e.g., Sweden, Belgium) and initiating new build programs (e.g., UK, France, Poland) to reduce reliance on imported fossil fuels and meet ambitious climate targets. France continues its strong commitment to nuclear power, while Eastern European countries are exploring nuclear energy for diversification.

- Asia Pacific (APAC): APAC represents the largest and fastest-growing market for nuclear energy, primarily driven by China and India's massive expansion plans. Both countries have extensive pipelines for new reactor construction to meet surging electricity demand and mitigate air pollution. South Korea and Japan are also restarting existing reactors and exploring new technologies, contributing significantly to regional uranium demand.

- Latin America: Several Latin American countries, including Argentina, Brazil, and Mexico, have established nuclear power programs and are exploring opportunities for expansion or modernization. While smaller in scale compared to other regions, the potential for growth is linked to energy independence and economic development.

- Middle East and Africa (MEA): This region is emerging as a significant new frontier for nuclear power, with countries like the UAE already operating plants and Saudi Arabia, Egypt, and Turkey actively pursuing or planning nuclear energy programs. The strategic importance of uranium for energy and water security (desalination) is a key driver. Africa, particularly Niger, also remains a critical source of uranium supply, facing both production opportunities and geopolitical challenges.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Uranium Market.- Kazatomprom

- Cameco Corporation

- Orano SA

- Uranium One

- BHP

- Paladin Energy

- Energy Fuels Inc.

- Denison Mines Corp.

- NexGen Energy Ltd.

- Global Atomic Corporation

- Boss Energy Ltd.

- Peninsula Energy Ltd.

- Rio Tinto

- ConverDyn

- URENCO

- Centrus Energy Corp.

- China National Nuclear Corporation (CNNC)

- Korea Hydro & Nuclear Power (KHNP)

- Rosatom

- TVA (Tennessee Valley Authority)

Frequently Asked Questions

What factors are driving the current demand for uranium?

Current uranium demand is primarily driven by the global push for decarbonization, increased focus on energy security, and the growing recognition of nuclear power as a reliable, low-carbon baseload energy source, supported by the development of Small Modular Reactors (SMRs).

How do Small Modular Reactors (SMRs) impact the uranium market?

SMRs are anticipated to significantly boost uranium demand by making nuclear power more accessible and deployable. Their smaller size, lower capital costs, and faster construction times enable wider adoption across diverse applications and regions, expanding the global nuclear fleet.

What are the main challenges facing the uranium supply chain?

Key challenges include geopolitical instability impacting major producing regions, long lead times for new mining projects, and the concentration of production, which can lead to supply disruptions and price volatility. Ensuring a diversified and secure supply is a continuous challenge.

Which regions are showing the most significant growth in nuclear energy?

The Asia Pacific region, particularly China and India, is demonstrating the most significant growth in nuclear energy capacity. Europe and North America are also experiencing a nuclear renaissance, with commitments to new builds, life extensions, and SMR deployment.

Is uranium a sustainable energy source?

Uranium-fueled nuclear power is considered a sustainable energy source due to its near-zero greenhouse gas emissions during operation and its ability to provide reliable baseload power. While concerns exist regarding waste management, advancements in fuel cycles and reactor technologies are continually improving its environmental profile and resource utilization efficiency.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted