Pin Fin Heat Sink for IGBT Market

Pin Fin Heat Sink for IGBT Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_701659 | Last Updated : July 30, 2025 |

Format : ![]()

![]()

![]()

![]()

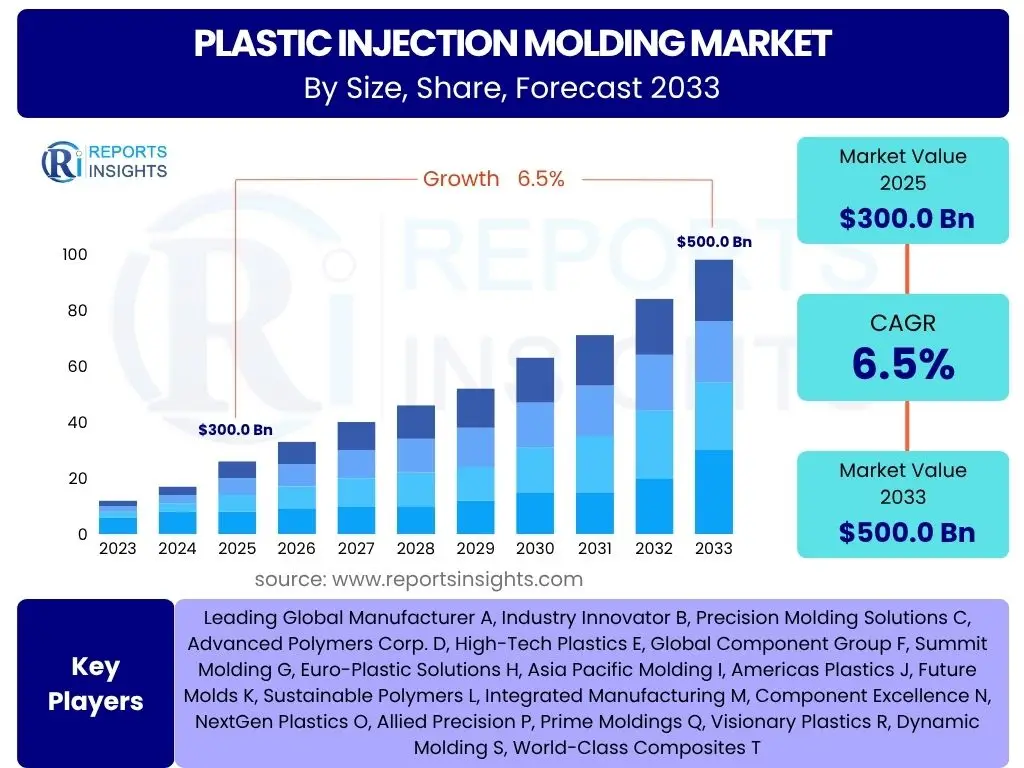

Pin Fin Heat Sink for IGBT Market Size

According to Reports Insights Consulting Pvt Ltd, The Pin Fin Heat Sink for IGBT Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 9.8% between 2025 and 2033. The market is estimated at USD 345.5 Million in 2025 and is projected to reach USD 726.8 Million by the end of the forecast period in 2033.

Key Pin Fin Heat Sink for IGBT Market Trends & Insights

Common user questions about trends and insights in the Pin Fin Heat Sink for IGBT market frequently revolve around how evolving power electronics demands influence heat sink design, the impact of new materials, and the drive towards enhanced thermal efficiency. Users are particularly interested in trends facilitating miniaturization, improved reliability, and sustainability. The market is witnessing a strong push towards advanced manufacturing techniques and the integration of sophisticated thermal management strategies to cope with increasing power densities and strict environmental regulations. This includes a focus on solutions that offer higher heat dissipation in compact forms while maintaining cost-effectiveness and long-term durability, especially for high-power applications like electric vehicles and renewable energy systems.

Furthermore, there is a growing inquiry into the adoption of specialized pin fin geometries and surface enhancements designed to optimize airflow and maximize heat transfer coefficients. The industry is also exploring hybrid cooling solutions that combine pin fin designs with other thermal technologies to achieve superior performance. Another significant area of interest is the supply chain resilience and the availability of raw materials, given the global nature of electronic manufacturing. The market is adapting to these trends by investing in research and development to produce next-generation pin fin heat sinks that are not only more efficient but also scalable and adaptable to diverse application requirements.

- Increasing adoption of high-power density IGBT modules necessitating advanced thermal solutions.

- Rising demand for compact and lightweight heat sinks, particularly in electric vehicles and portable power systems.

- Growing integration of advanced materials such such as aluminum alloys, copper, and composite materials for improved thermal conductivity.

- Emergence of additive manufacturing (3D printing) for complex and customized pin fin geometries.

- Emphasis on energy efficiency and sustainability driving the demand for optimized thermal management solutions.

- Development of smart thermal solutions with integrated sensors for real-time monitoring and adaptive cooling.

AI Impact Analysis on Pin Fin Heat Sink for IGBT

Common user questions related to the impact of AI on Pin Fin Heat Sink for IGBT modules often center on how artificial intelligence can revolutionize design processes, optimize performance, and enhance manufacturing efficiency. Users are keen to understand if AI can predict thermal behavior more accurately, leading to superior heat sink designs, and whether it can contribute to cost reduction through optimized material usage or production flows. There is also significant interest in AI's role in predictive maintenance for thermal systems in critical applications, ensuring long-term reliability and preventing failures.

The key themes emerging from user inquiries include AI-driven generative design capabilities, allowing for the exploration of highly complex and efficient pin fin geometries that traditional methods might overlook. Concerns often relate to the computational resources required and the integration of AI tools within existing engineering workflows. Expectations are high that AI will lead to faster design iterations, enable predictive analytics for thermal performance under varying loads, and facilitate intelligent control of cooling systems, thereby pushing the boundaries of thermal management for IGBTs. This advanced analytical capability is anticipated to yield heat sinks that are not only more effective but also tailored precisely to the unique thermal profiles of specific IGBT applications.

- AI-driven generative design for optimizing pin fin geometries, leading to higher thermal efficiency and material savings.

- Predictive analytics for thermal performance simulation, enabling more accurate design validation and reduced prototyping cycles.

- Machine learning algorithms enhancing manufacturing process control, reducing defects, and improving production throughput for heat sinks.

- AI-powered smart thermal management systems for real-time monitoring and adaptive cooling of IGBT modules, increasing system longevity.

- Optimization of material selection and allocation through AI, leading to cost efficiencies and improved sustainability.

Key Takeaways Pin Fin Heat Sink for IGBT Market Size & Forecast

Common user questions about key takeaways from the Pin Fin Heat Sink for IGBT market size and forecast reveal a strong interest in understanding the core growth drivers, the longevity of market expansion, and the primary applications fueling demand. Users are particularly keen to identify the most promising segments and the underlying technological shifts that will sustain market momentum over the forecast period. There is also an emphasis on recognizing the critical factors that could either accelerate or impede market growth, alongside insights into regional dynamics.

The market is poised for robust expansion, primarily propelled by the burgeoning electric vehicle sector, the global shift towards renewable energy sources, and the increasing power requirements of industrial and telecommunication infrastructure. The forecast indicates a sustained demand for high-performance, compact, and efficient thermal management solutions for IGBTs. Key insights highlight the imperative for innovation in materials and manufacturing processes to meet these evolving needs, emphasizing that companies prioritizing research and development in advanced cooling technologies will likely capture significant market share. The market's resilience is also tied to its ability to adapt to new power semiconductor technologies and increasingly stringent energy efficiency regulations.

- The Pin Fin Heat Sink for IGBT market is expected to demonstrate significant growth, driven by electrification across various industries.

- Automotive (especially EVs) and renewable energy sectors are the primary demand generators for high-performance IGBT thermal solutions.

- Technological advancements in heat sink design and materials are crucial for meeting increasing power density and efficiency requirements.

- Market expansion is strongly influenced by global initiatives promoting energy efficiency and decarbonization.

- Customization and application-specific thermal solutions will be key differentiators for market players.

Pin Fin Heat Sink for IGBT Market Drivers Analysis

The Pin Fin Heat Sink for IGBT market is propelled by several robust drivers, fundamentally linked to the global push for higher power efficiency, miniaturization, and the increasing adoption of power electronics across diverse sectors. The continuous advancement of IGBT technology, which allows for higher power handling in smaller footprints, inherently necessitates more effective thermal management solutions to prevent overheating and ensure optimal performance and longevity. This core requirement forms the bedrock of market growth.

Key industries such as automotive, renewable energy, and industrial automation are rapidly integrating high-power IGBT modules, thereby amplifying the demand for specialized heat sinks. Electric vehicles, for instance, rely heavily on IGBTs for power conversion in inverters, chargers, and motor drives, where efficient heat dissipation directly impacts vehicle performance, range, and battery life. Similarly, the proliferation of solar inverters and wind turbine systems globally mandates robust thermal solutions for their IGBTs to ensure reliable and efficient energy conversion. These sectoral demands, coupled with continuous innovation in material science and manufacturing processes for heat sinks, collectively create a strong positive impetus for the market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Surge in Electric Vehicle (EV) Production | +2.5% | North America, Europe, Asia Pacific (China, Japan, South Korea) | Short to Mid-term (2025-2030) |

| Growth of Renewable Energy Installations (Solar & Wind) | +2.0% | Asia Pacific (China, India), Europe, North America | Mid to Long-term (2027-2033) |

| Increasing Demand for High-Power Density Electronics | +1.8% | Global, particularly developed regions with advanced manufacturing | Short to Mid-term (2025-2030) |

| Advancements in Industrial Automation & Motor Drives | +1.5% | Europe, North America, Asia Pacific | Mid-term (2026-2031) |

| Expansion of Data Centers and 5G Infrastructure | +1.2% | North America, Asia Pacific, Europe | Short to Mid-term (2025-2029) |

Pin Fin Heat Sink for IGBT Market Restraints Analysis

Despite the strong growth drivers, the Pin Fin Heat Sink for IGBT market faces several restraints that could impede its full potential. One significant challenge revolves around the inherent trade-offs between cost, performance, and size. Designing a highly efficient pin fin heat sink often involves complex geometries and advanced materials, which can significantly drive up manufacturing costs. This cost sensitivity becomes particularly pronounced in high-volume applications where maintaining competitive pricing is paramount, potentially leading manufacturers to opt for less efficient but more affordable thermal solutions.

Another restraint stems from the increasing complexity of thermal management requirements. As IGBTs become more powerful and compact, the thermal design process becomes more intricate, demanding specialized expertise and advanced simulation tools. This can extend design cycles and increase development costs. Furthermore, competition from alternative cooling technologies, such as liquid cooling or vapor chambers, especially in very high-power density applications where air cooling may not be sufficient, poses a competitive threat. Supply chain vulnerabilities for critical raw materials, such as copper and aluminum, and fluctuations in their prices, also represent an ongoing concern for market stability and production planning. These factors collectively necessitate strategic mitigation efforts from market participants to sustain growth.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs of Advanced Heat Sinks | -1.5% | Global, particularly emerging economies | Short to Mid-term (2025-2030) |

| Complexity in Design and Optimization | -1.0% | Global, affecting smaller manufacturers | Mid-term (2026-2031) |

| Competition from Alternative Cooling Technologies | -0.8% | Global, especially in high-power applications | Mid to Long-term (2027-2033) |

| Supply Chain Volatility and Raw Material Price Fluctuations | -0.7% | Global, impacting all manufacturers | Short-term (2025-2027) |

Pin Fin Heat Sink for IGBT Market Opportunities Analysis

The Pin Fin Heat Sink for IGBT market is ripe with opportunities driven by several emerging technological shifts and expanding application landscapes. A significant opportunity lies in the rapid development and adoption of wide-bandgap (WBG) semiconductors like Silicon Carbide (SiC) and Gallium Nitride (GaN). While these materials offer superior power efficiency and operate at higher temperatures, they still require effective thermal management, often demanding more compact and specialized heat sinks to manage localized hot spots efficiently. This transition presents a chance for manufacturers to innovate and develop advanced pin fin designs tailored to the unique thermal properties of WBG devices.

Another key opportunity is the increasing customization required for diverse applications. As industries like aerospace, defense, and specialized medical equipment integrate high-power IGBTs, there is a growing need for bespoke thermal solutions that fit specific form factors and operating environments. This allows for higher-value product offerings and strengthens manufacturer-client relationships. Furthermore, advancements in additive manufacturing (3D printing) open new avenues for producing highly complex and optimized pin fin geometries that were previously unachievable with traditional manufacturing methods. This technology enables rapid prototyping and the creation of highly efficient, lightweight structures, presenting a significant competitive advantage for early adopters and innovators in the market. Expanding into untapped geographical markets and integrating smart thermal management features also present compelling growth prospects.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration with Wide Bandgap (SiC, GaN) Semiconductors | +2.2% | Global, particularly in high-growth power electronics segments | Mid to Long-term (2027-2033) |

| Advancements in Additive Manufacturing (3D Printing) | +1.7% | Developed economies with strong R&D infrastructure | Mid-term (2026-2031) |

| Emerging Applications in Aerospace, Defense, and Medical | +1.4% | North America, Europe, select APAC countries | Long-term (2028-2033) |

| Development of Hybrid Cooling Solutions | +1.0% | Global, for demanding thermal environments | Mid-term (2026-2030) |

| Focus on Customization and Application-Specific Designs | +0.9% | Global, catering to diverse industrial needs | Short to Mid-term (2025-2029) |

Pin Fin Heat Sink for IGBT Market Challenges Impact Analysis

The Pin Fin Heat Sink for IGBT market faces a distinct set of challenges that require proactive strategies from manufacturers and suppliers. A significant challenge is striking the optimal balance between cost-effectiveness and high thermal performance. Customers in various industries, from automotive to consumer electronics, demand increasingly efficient thermal solutions but often at competitive price points. This pressure forces manufacturers to innovate in design and material selection without significantly escalating production costs, which can be a complex engineering and economic problem, especially for high-volume applications.

Another critical challenge involves the rapid pace of technological evolution in power electronics. IGBT modules are continually improving in power density and efficiency, leading to higher heat fluxes within smaller packages. This necessitates constant research and development in heat sink design and materials to keep pace with these evolving thermal demands. Ensuring long-term reliability and managing thermal stress under extreme operating conditions, particularly in harsh environments like electric vehicle powertrains or renewable energy inverters, also poses a significant hurdle. Furthermore, intellectual property protection in a highly competitive market, coupled with the need for global standardization, adds layers of complexity. Overcoming these challenges will be crucial for sustainable growth and market leadership.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Balancing Cost-Effectiveness with High Performance | -1.2% | Global, impacting all market segments | Short to Mid-term (2025-2030) |

| Rapid Technological Advancements in IGBTs | -1.0% | Global, affecting R&D investments | Short to Mid-term (2025-2029) |

| Ensuring Long-term Reliability in Harsh Environments | -0.9% | Global, particularly in critical applications | Mid-term (2026-2031) |

| Supply Chain Disruptions for Key Materials | -0.6% | Global, with regional variations | Short-term (2025-2027) |

Pin Fin Heat Sink for IGBT Market - Updated Report Scope

This market insights report on Pin Fin Heat Sink for IGBT provides a comprehensive analysis of the current market landscape and future growth trajectories. It delves into the market size, historical trends from 2019 to 2023, and forecasts for the period 2025 to 2033. The report offers an in-depth examination of key market drivers, restraints, opportunities, and challenges that shape the industry, along with their quantified impact on the Compound Annual Growth Rate. It also includes an analysis of the AI impact on design and manufacturing processes. The scope covers detailed segmentation by material, manufacturing process, application, and end-use industry, providing granular insights into market dynamics across different regions and key countries. Furthermore, it profiles leading market players, offering a strategic overview for stakeholders to make informed business decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 345.5 Million |

| Market Forecast in 2033 | USD 726.8 Million |

| Growth Rate | 9.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Aavid Thermalloy, Advanced Thermal Solutions (ATS), Boyd Corporation, TE Connectivity, Celsia Inc., Alpha Novatech, DAU, Ohmite Manufacturing, Thermoson Inc., Wakefield-Vette, Dynatron Corporation, Fuji Electric, Nidec Corporation, Laird Thermal Systems, Delta Electronics, Sumitomo Electric Industries, Mecc.Al S.p.A., Enertron Inc., Foxconn Technology Group, San Ace (Sanyo Denki) |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Pin Fin Heat Sink for IGBT market is comprehensively segmented to provide a detailed understanding of its various facets and their individual contributions to market dynamics. This segmentation allows for a granular analysis of product types, manufacturing methods, and end-use applications, highlighting specific growth areas and technological preferences across different sectors. By categorizing the market based on material, manufacturing process, application, and end-use industry, the report offers insights into how specific industry trends and technological advancements influence demand and adoption patterns within each segment, enabling stakeholders to identify lucrative opportunities and tailor their strategies accordingly.

The material segment is crucial as it dictates thermal performance, weight, and cost, with aluminum and copper being primary choices alongside emerging composites and ceramics. Manufacturing processes highlight the evolution from traditional methods like extrusion to advanced techniques such as additive manufacturing, which enables complex geometries for improved heat dissipation. The application segment reveals the key demand drivers, from the rapidly expanding electric vehicle market to the stable growth in industrial drives and renewable energy systems. Lastly, the end-use industry segmentation provides a macro-level view of where these solutions are most critically applied, helping to understand broader market shifts and investment priorities.

- By Material: Aluminum, Copper, Ceramic, Graphite, Composite Materials, Others

- By Manufacturing Process: Extrusion, Forging, Casting, Stamping, Skiving, Additive Manufacturing (3D Printing), CNC Machining

- By Application: Electric Vehicles (EVs), Hybrid Electric Vehicles (HEVs), Renewable Energy Systems (Solar Inverters, Wind Turbines), Industrial Motor Drives & Controls, Uninterruptible Power Supplies (UPS), Power Converters, Telecommunication Base Stations, Consumer Electronics (High-Power Appliances), Medical Equipment, Data Centers & IT Infrastructure, Rail & Transportation

- By End-Use Industry: Automotive, Energy & Power, Industrial, Telecommunications, IT & Data Centers, Consumer Electronics, Medical, Aerospace & Defense

Regional Highlights

- North America: This region demonstrates robust growth, primarily driven by significant investments in electric vehicle infrastructure, the expansion of data centers, and advanced industrial automation. The presence of key technology developers and the emphasis on energy efficiency contribute to the adoption of high-performance pin fin heat sinks. Regulations and a strong research and development ecosystem foster innovation in thermal management.

- Europe: Europe is a key market, characterized by its strong automotive industry, particularly in premium electric and hybrid vehicles, and a leading position in renewable energy installations. Stringent environmental regulations and a focus on industrial efficiency drive the demand for advanced and highly efficient thermal solutions for IGBTs in power conversion applications.

- Asia Pacific (APAC): APAC represents the largest and fastest-growing market, largely due to its vast manufacturing base for electronics, electric vehicles, and renewable energy equipment. Countries like China, Japan, South Korea, and India are experiencing rapid industrialization and urbanization, leading to high demand for power electronics across consumer electronics, industrial drives, and telecommunications, thus boosting the Pin Fin Heat Sink for IGBT market.

- Latin America: The market in Latin America is projected for steady growth, influenced by increasing industrialization, infrastructure development, and growing adoption of renewable energy projects. While currently smaller, the region presents emerging opportunities as manufacturing capabilities expand and demand for modern power electronics increases.

- Middle East and Africa (MEA): The MEA region is expected to show gradual growth, propelled by government initiatives towards diversifying economies, investing in renewable energy, and modernizing industrial sectors. Projects related to smart cities and telecommunications infrastructure also contribute to the demand for efficient thermal management solutions for IGBTs.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Pin Fin Heat Sink for IGBT Market.- Aavid Thermalloy

- Advanced Thermal Solutions (ATS)

- Boyd Corporation

- TE Connectivity

- Celsia Inc.

- Alpha Novatech

- DAU

- Ohmite Manufacturing

- Thermoson Inc.

- Wakefield-Vette

- Dynatron Corporation

- Fuji Electric

- Nidec Corporation

- Laird Thermal Systems

- Delta Electronics

- Sumitomo Electric Industries

- Mecc.Al S.p.A.

- Enertron Inc.

- Foxconn Technology Group

- San Ace (Sanyo Denki)

Frequently Asked Questions

Analyze common user questions about the Pin Fin Heat Sink for IGBT market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are Pin Fin Heat Sinks for IGBTs?

Pin fin heat sinks are thermal management devices featuring an array of cylindrical, elliptical, or conical pins extending from a base plate. They are specifically designed to dissipate heat from Insulated Gate Bipolar Transistors (IGBTs), which are high-power semiconductor devices, by maximizing surface area for efficient convection cooling, crucial for maintaining optimal operating temperatures and ensuring reliability.

What industries primarily drive the demand for Pin Fin Heat Sinks for IGBTs?

The primary industries driving demand include automotive (especially electric vehicles for inverters and chargers), renewable energy (solar inverters, wind turbines), industrial automation (motor drives, power supplies), and telecommunications (base stations). These sectors rely heavily on high-power IGBTs, necessitating robust thermal management.

What materials are commonly used in manufacturing Pin Fin Heat Sinks for IGBTs?

Common materials include aluminum alloys (due to their light weight and good thermal conductivity), copper (for superior thermal performance in demanding applications), and increasingly, composite materials or ceramics for specialized needs. The choice depends on performance requirements, cost, and weight considerations.

How does additive manufacturing (3D printing) impact the Pin Fin Heat Sink market?

Additive manufacturing enables the creation of highly complex and optimized pin fin geometries that are difficult or impossible to achieve with traditional methods. This allows for improved thermal efficiency, custom designs for specific applications, reduced material waste, and rapid prototyping, significantly enhancing design flexibility and performance.

What are the key challenges in the Pin Fin Heat Sink for IGBT market?

Key challenges include balancing high thermal performance with cost-effectiveness, keeping pace with the rapid advancements in IGBT power density, ensuring long-term reliability under harsh operating conditions, and navigating supply chain complexities for raw materials. Intense competition and the need for continuous innovation also pose significant hurdles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted