TV Ad spending Market

TV Ad spending Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707330 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

TV Ad spending Market Size

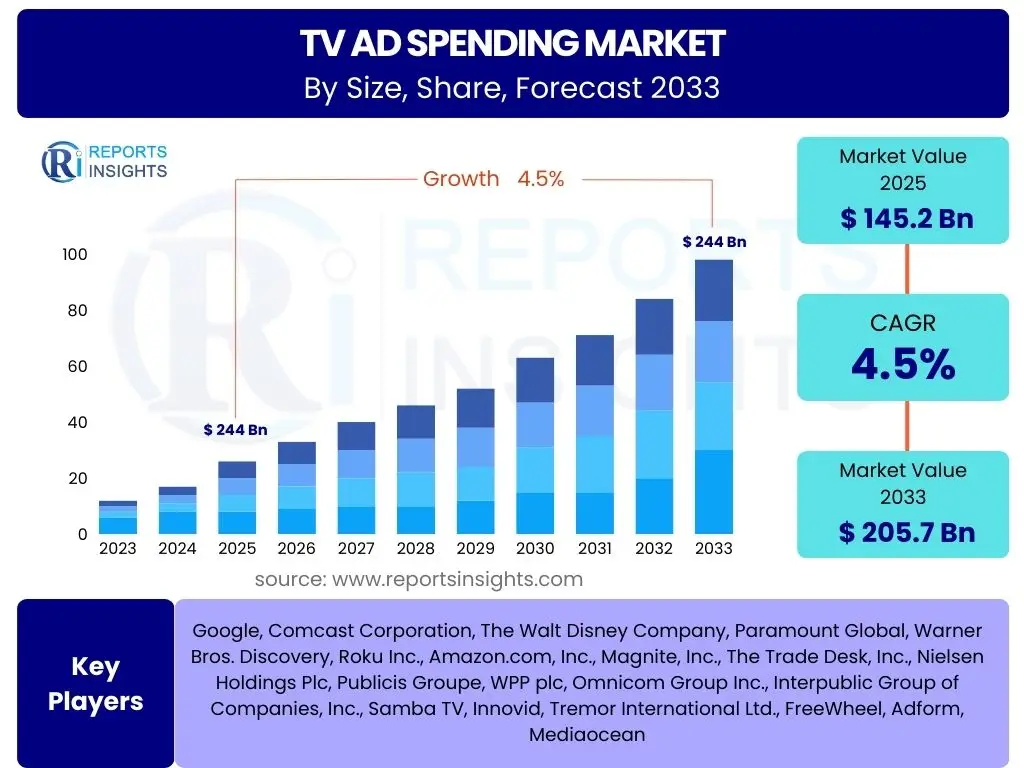

According to Reports Insights Consulting Pvt Ltd, The TV Ad spending Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.5% between 2025 and 2033. The market is estimated at USD 145.2 Billion in 2025 and is projected to reach USD 205.7 Billion by the end of the forecast period in 2033.

Key TV Ad spending Market Trends & Insights

The TV advertising landscape is undergoing a significant transformation, driven by evolving consumer behaviors and technological advancements. Users frequently inquire about the enduring relevance of traditional linear TV, the rise of Connected TV (CTV), and how advertisers are adapting to fragmented audiences. A key insight is the shift from broad, demographic-based targeting to more precise, data-driven approaches, mirroring trends seen in digital advertising. This evolution emphasizes the convergence of traditional broadcast reach with digital-like personalization and measurement capabilities.

Another area of user interest concerns the integration of TV with other media channels. Advertisers are increasingly looking for holistic, cross-platform strategies that maximize reach and engagement while providing unified attribution. The emergence of programmatic TV and addressable advertising is central to these discussions, offering greater efficiency and targeting precision than ever before in the TV medium. This allows for more dynamic campaign adjustments and optimization, moving away from static media buys to more flexible, performance-oriented models.

Furthermore, there is a growing emphasis on creative optimization and the quality of ad experiences. As consumers face an abundance of content and advertising, the effectiveness of TV ads relies not just on placement but also on compelling narratives and relevant messaging. The industry is responding by exploring new ad formats, interactive elements, and content integrations that enhance viewer engagement rather than disrupt it. These trends collectively underscore a strategic pivot towards smarter, more integrated, and viewer-centric TV advertising.

- Convergence of linear TV and Connected TV (CTV) for unified campaigns.

- Increased adoption of programmatic TV advertising for automated buying and selling.

- Growth of addressable TV advertising, enabling household-level targeting.

- Greater emphasis on data-driven audience segmentation and personalized ad delivery.

- Development of advanced measurement and attribution models for TV campaigns.

- Shift towards outcomes-based media buying and performance marketing on TV.

- Integration of interactive ad formats and shoppable TV experiences.

AI Impact Analysis on TV Ad spending

Common user questions related to the impact of AI on TV Ad spending revolve around its ability to enhance targeting, automate processes, and improve campaign performance. Users are keen to understand how artificial intelligence can make TV advertising more efficient and effective, particularly in an increasingly complex media ecosystem. The key themes include AI's role in audience segmentation, predictive analytics for media planning, and the optimization of ad creative for maximum impact. There is an expectation that AI will unlock new levels of precision and responsiveness in TV campaigns, moving beyond traditional demographic buys to highly granular audience engagement.

Concerns often raised include the potential for AI to displace human roles in media buying and planning, as well as the ethical implications of data usage for highly personalized advertising. However, the prevailing sentiment is that AI will augment, rather than replace, human expertise, allowing professionals to focus on strategic insights and creative development while repetitive tasks are automated. The technology is anticipated to provide deeper insights into viewer behavior, enabling advertisers to identify optimal ad placements, times, and content environments with unprecedented accuracy.

Ultimately, users expect AI to drive significant advancements in return on investment (ROI) for TV ad spending. This includes improved ad relevancy, reduced wastage, and the ability to dynamically adjust campaigns based on real-time performance data. The transformative potential of AI extends to areas like fraud detection in programmatic TV, automated content tagging for contextual targeting, and even the generation of tailored ad creatives. These capabilities are poised to reshape the competitive landscape, making TV advertising more agile, accountable, and aligned with modern marketing objectives.

- Enhanced audience targeting through granular data analysis and predictive modeling.

- Automated media planning and buying, optimizing ad placement across platforms.

- Dynamic creative optimization (DCO) for personalized ad content delivery.

- Real-time campaign performance tracking and automated adjustments.

- Improved attribution modeling to better link TV ad exposure to consumer actions.

- Contextual ad placement using AI to analyze content and viewer engagement.

- Fraud detection and brand safety assurance in programmatic TV environments.

- Personalized ad delivery based on household-level viewing habits and preferences.

Key Takeaways TV Ad spending Market Size & Forecast

Analyzing common user questions about key takeaways from the TV Ad spending market size and forecast reveals a persistent curiosity about the resilience and future relevance of television as an advertising medium. Users seek clear indications of where the growth will originate and which segments will drive market expansion. A primary insight is that while linear TV faces competition from digital platforms, its foundational strength in delivering mass reach and building brand awareness remains unparalleled for many advertisers, particularly in categories that benefit from broad exposure.

Another crucial takeaway is the increasing convergence of traditional TV with digital streaming and Connected TV (CTV). The market forecast indicates that much of the projected growth will be fueled by innovations within the broader TV ecosystem, including programmatic buying, addressable advertising, and advanced measurement capabilities that offer digital-like precision. This convergence allows advertisers to leverage the impact of TV while gaining the targeting and attribution benefits previously exclusive to digital channels, optimizing overall media spend.

The forecast also highlights the importance of data integration and cross-platform strategies. Advertisers are increasingly demanding holistic views of their campaigns, requiring sophisticated tools to measure effectiveness across linear, on-demand, and digital TV platforms. The ability to unify data, optimize delivery, and measure true ROI across these diverse environments will be critical for stakeholders in the TV ad spending market. The market's growth trajectory signifies its adaptability and the continued value proposition TV offers in a data-driven advertising landscape.

- The TV ad market demonstrates resilience, driven by innovation in targeting and measurement.

- Growth is primarily fueled by the expansion of Connected TV (CTV) and addressable advertising.

- Convergence of linear and digital TV advertising is paramount for future market expansion.

- Data-driven strategies and advanced analytics are becoming central to TV ad buying.

- TV continues to be a critical channel for mass reach and brand building, complementing digital efforts.

TV Ad spending Market Drivers Analysis

The TV Ad spending Market is significantly influenced by several key drivers that contribute to its sustained growth and evolution. A primary driver is the enduring power of television for mass reach and brand building. Despite the fragmentation of audiences across various digital platforms, traditional linear TV remains highly effective for reaching large, diverse audiences simultaneously, especially during major live events such as sports championships, news broadcasts, and cultural phenomena. This broad reach is invaluable for brands seeking to establish widespread awareness and reinforce their presence in the public consciousness, making TV an indispensable component of many advertising strategies.

Furthermore, the rapid advancements in advertising technology, particularly in areas like Connected TV (CTV) and addressable advertising, are revolutionizing the TV ad landscape. These technologies enable advertisers to target specific households or demographic segments with personalized ads, moving beyond the traditional one-to-many broadcast model. The ability to deliver more relevant advertisements, combined with enhanced measurement capabilities that provide deeper insights into campaign performance, drives increased investment from advertisers looking for more efficient and accountable spending. This technological evolution effectively bridges the gap between the broad impact of linear TV and the precision of digital advertising, creating new value propositions.

The increasing availability and consumption of premium video content across various platforms also serve as a significant driver. Viewers continue to gravitate towards high-quality, professionally produced content, whether through linear channels or streaming services. Advertisers recognize that associating their brands with engaging and reputable content enhances brand perception and effectively captures audience attention. Additionally, the strategic use of television in political advertising, particularly in democratic countries with frequent election cycles, provides a consistent and substantial boost to ad spending. These factors collectively underscore the dynamic and adaptable nature of the TV ad spending market.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Enduring Power of Mass Reach & Brand Building | +1.2% | Global, particularly North America, Europe | Long-term (2025-2033) |

| Advancements in Connected TV (CTV) & Addressable Advertising | +1.5% | Global, strong in developed markets | Medium to Long-term (2025-2033) |

| Increased Consumption of Premium Video Content | +0.8% | Global, expanding in APAC | Medium-term (2025-2030) |

| Growth in Programmatic TV Advertising | +1.0% | North America, Europe | Medium-term (2025-2030) |

| Political Advertising & Major Live Events | +0.5% | Specific countries (USA, India, major sporting nations) | Short-term (Event-specific peaks) |

TV Ad spending Market Restraints Analysis

Despite its inherent strengths, the TV Ad spending Market faces several significant restraints that could impede its growth trajectory. One of the most prominent challenges is the ongoing shift in audience viewership from traditional linear television to digital and streaming platforms. Consumers, particularly younger demographics, are increasingly opting for on-demand content through Subscription Video On Demand (SVOD) and Advertising-based Video On Demand (AVOD) services, which often offer limited or no commercial breaks. This fragmentation of audience attention reduces the pool of readily available viewers for linear TV advertisements, making it harder for advertisers to achieve the same reach and frequency as in the past.

Another critical restraint is the relatively higher cost and complexity associated with traditional TV advertising compared to digital alternatives. While TV offers unparalleled reach, the barrier to entry for smaller businesses can be prohibitive due to high production costs and media buying expenses. Furthermore, the lack of granular targeting and real-time optimization capabilities in traditional linear TV contrasts sharply with the precision and flexibility offered by digital ad platforms. This often leads to concerns about ad wastage and inefficient spending, compelling some advertisers to reallocate budgets to more digitally-centric channels where return on investment can be more directly measured and optimized.

Moreover, the rise of ad-blocking technologies and the increasing popularity of ad-free subscription models for content consumption further limit the potential exposure of TV advertisements. Viewers are becoming more adept at avoiding commercials, whether through DVR skipping or by choosing premium, ad-free viewing experiences. This trend forces advertisers to seek more integrated and less intrusive ad formats, which can be challenging to implement at scale across the diverse TV ecosystem. Additionally, difficulties in cross-platform measurement and attribution create a fragmented view of campaign performance, making it hard for advertisers to justify TV spend against other measurable channels, posing a significant hurdle for continued investment.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Shift of Audience to Digital & Streaming Platforms | -1.5% | Global, particularly North America, Europe | Long-term (2025-2033) |

| High Cost and Complexity of Traditional TV Advertising | -0.8% | Global, affecting SMEs | Long-term (2025-2033) |

| Ad-blocking & Rise of Ad-Free Subscription Models | -1.0% | Developed markets | Medium-term (2025-2030) |

| Fragmented Measurement & Attribution Challenges | -0.7% | Global, especially cross-platform campaigns | Medium-term (2025-2030) |

| Limited Granular Targeting in Linear TV | -0.6% | Global | Long-term (2025-2033) |

TV Ad spending Market Opportunities Analysis

Despite the challenges, the TV Ad spending Market presents numerous opportunities for growth and innovation, largely driven by technological advancements and evolving viewer behaviors. A significant opportunity lies in the continued integration of linear television with Connected TV (CTV) and Over-The-Top (OTT) platforms. This convergence allows advertisers to execute holistic campaigns that leverage the broad reach of traditional broadcast alongside the precise targeting and measurement capabilities of digital streaming. By offering a seamless experience across multiple screens, advertisers can maximize their impact and optimize frequency, capturing audiences wherever they consume video content and providing a more unified view of campaign performance.

Furthermore, the expansion of addressable TV and programmatic TV advertising represents a transformative opportunity. Addressable TV enables advertisers to deliver different ads to different households watching the same program, based on demographic, behavioral, or geographic data. Programmatic TV automates the buying and selling of ad inventory, bringing efficiency, real-time optimization, and data-driven decision-making to the TV landscape. These technologies empower advertisers to reduce ad waste, enhance personalization, and achieve greater return on investment, thereby attracting new ad spend that might have previously gone to purely digital channels. The ability to buy and optimize TV campaigns with digital-like agility makes the medium more appealing to performance-oriented marketers.

Another substantial opportunity is the development of advanced data analytics and unified measurement solutions. As more viewer data becomes available from smart TVs, set-top boxes, and streaming platforms, the ability to analyze this data to derive actionable insights for targeting, creative optimization, and attribution is paramount. Solutions that can provide a single source of truth for cross-platform campaign performance will unlock new levels of accountability and demonstrate the true value of TV advertising. Additionally, the exploration of innovative ad formats, such as interactive ads, shoppable TV experiences, and dynamic product placements, offers new avenues for engagement and monetization, transforming passive viewing into active participation and creating direct paths to conversion for advertisers.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Convergence of Linear TV, CTV, & OTT Platforms | +1.8% | Global, high in developed markets | Long-term (2025-2033) |

| Expansion of Addressable TV Advertising | +1.5% | North America, Europe, increasing in APAC | Medium to Long-term (2025-2033) |

| Growth in Programmatic TV Adoption | +1.3% | Global, strong in North America | Medium-term (2025-2030) |

| Advancements in Data Analytics & Unified Measurement | +1.0% | Global | Medium to Long-term (2025-2033) |

| Development of New & Interactive Ad Formats | +0.7% | Global | Short to Medium-term (2025-2028) |

TV Ad spending Market Challenges Impact Analysis

The TV Ad spending Market faces several critical challenges that demand strategic responses from industry participants. A primary challenge is adapting to the rapidly changing media consumption habits of audiences, particularly the younger demographics. The proliferation of streaming services, social media, and short-form video content means that viewer attention is more fragmented than ever before. This fragmentation complicates media planning and buying, making it harder for advertisers to achieve consistent reach and frequency across diverse platforms and consumption patterns. Effectively reaching and engaging these multifaceted audiences requires continuous innovation in content, distribution, and advertising models.

Another significant hurdle is the lack of standardized, cross-platform measurement and attribution. Advertisers often struggle to get a unified view of their campaign performance across linear TV, Connected TV (CTV), and other digital video channels. This siloed measurement makes it difficult to compare the effectiveness of TV spend against other media investments and to optimize budget allocation for maximum return. Developing robust, industry-wide standards for cross-platform measurement and attribution is crucial for demonstrating the comprehensive value of TV advertising and attracting sustained investment, enabling more informed decision-making for marketing departments.

Furthermore, the intensifying competition from digital-native advertising platforms, which offer highly sophisticated targeting, real-time optimization, and granular analytics, presents a formidable challenge. These platforms often boast lower entry barriers and a clear path to conversion, appealing to a wide range of advertisers, particularly those focused on direct response. To remain competitive, the TV ad ecosystem must continue to innovate by integrating similar capabilities, such as advanced programmatic tools and data-driven personalization, while leveraging its unique strengths in brand building and emotional connection. Balancing the traditional appeal of TV with the demands for digital-level performance and accountability is key to navigating this competitive landscape effectively.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Adapting to Fragmented Audience Consumption Habits | -1.2% | Global | Long-term (2025-2033) |

| Lack of Standardized Cross-Platform Measurement | -1.0% | Global, especially for integrated campaigns | Medium to Long-term (2025-2033) |

| Intense Competition from Digital Ad Platforms | -0.9% | Global, particularly in direct response categories | Long-term (2025-2033) |

| Ensuring Brand Safety & Ad Fraud Prevention in CTV | -0.5% | Global, emerging concern | Short to Medium-term (2025-2028) |

| Evolving Data Privacy Regulations | -0.4% | Europe (GDPR), North America (CCPA, CPRA) | Ongoing |

TV Ad spending Market - Updated Report Scope

This comprehensive market research report delves into the intricate dynamics of the global TV Ad spending Market, offering a detailed analysis of its current state, historical performance, and future growth prospects. The scope encompasses a thorough examination of market size and forecast, key trends, and the profound impact of artificial intelligence on advertising strategies. It provides in-depth insights into the primary market drivers, restraints, opportunities, and challenges that shape the industry landscape, offering a holistic understanding for stakeholders. The report aims to equip businesses with actionable intelligence to navigate the evolving complexities of TV advertising and capitalize on emerging opportunities across various segments and regions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 145.2 Billion |

| Market Forecast in 2033 | USD 205.7 Billion |

| Growth Rate | 4.5% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Google, Comcast Corporation, The Walt Disney Company, Paramount Global, Warner Bros. Discovery, Roku Inc., Amazon.com, Inc., Magnite, Inc., The Trade Desk, Inc., Nielsen Holdings Plc, Publicis Groupe, WPP plc, Omnicom Group Inc., Interpublic Group of Companies, Inc., Samba TV, Innovid, Tremor International Ltd., FreeWheel, Adform, Mediaocean |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The TV Ad spending Market is extensively segmented to provide a granular understanding of its diverse components and drivers. This segmentation allows for a detailed analysis of spending patterns, technological adoption, and strategic preferences across various dimensions of the advertising ecosystem. By breaking down the market into distinct categories, this analysis reveals the nuances of how different ad types, industry verticals, platforms, campaign objectives, and audience demographics contribute to the overall market landscape, offering actionable insights for advertisers and media companies alike.

Understanding these segments is crucial for stakeholders to tailor their strategies, identify niche opportunities, and optimize their media investments. For instance, while linear TV continues to dominate certain ad types and industry verticals, the rapid expansion of Connected TV (CTV) and programmatic solutions is reshaping platform-based spending. Similarly, the shift from broad brand awareness campaigns to more targeted direct response initiatives highlights evolving advertiser demands. This comprehensive segmentation provides a roadmap for navigating the complexities of the TV ad market and for identifying key areas of growth and innovation in the coming years.

- By Ad Type:

- Spot Ads

- Sponsorships

- Product Placements

- Infomercials

- Public Service Announcements (PSAs)

- By Industry Vertical:

- Automotive

- Consumer Packaged Goods (CPG)

- Retail & E-commerce

- Financial Services

- Healthcare & Pharmaceuticals

- Telecommunications

- Media & Entertainment

- Travel & Tourism

- Technology

- Others

- By Platform:

- Linear TV

- Connected TV (CTV)

- Addressable TV

- Programmatic TV

- By Campaign Objective:

- Brand Awareness

- Direct Response

- Lead Generation

- Product Launch

- By Audience Demographic:

- General Public

- Specific Age Groups (e.g., Millennials, Gen Z)

- Income Brackets

- Lifestyle Segments

Regional Highlights

The global TV Ad spending Market exhibits distinct regional dynamics, influenced by varying levels of economic development, technological adoption, regulatory frameworks, and cultural consumption habits. North America, particularly the United States, represents a dominant force in the market, characterized by its mature advertising ecosystem, high penetration of Connected TV (CTV), and rapid adoption of programmatic and addressable advertising technologies. This region continues to drive innovation in measurement and targeting, often setting trends that influence other global markets. The competitive landscape and significant advertising budgets in the U.S. contribute substantially to overall market value.

Europe presents a complex but significant market, with diverse country-specific regulations and advertising practices. While Western European countries show high adoption of advanced TV advertising solutions, Eastern Europe is gradually catching up, driven by increasing internet penetration and modernization of broadcast infrastructure. The region is witnessing a steady shift towards converged TV strategies, where traditional broadcasters are integrating more digital-like capabilities. Asia Pacific (APAC) is projected to be one of the fastest-growing regions, fueled by a burgeoning middle class, increasing disposable incomes, and the widespread adoption of smart TVs and digital video consumption, especially in populous countries like China and India. The region offers immense untapped potential for advertisers seeking to reach vast, emerging audiences.

Latin America and the Middle East & Africa (MEA) are also experiencing growth in TV ad spending, albeit at different paces. Latin America benefits from a strong tradition of linear TV viewership, now increasingly augmented by CTV solutions. Countries like Brazil and Mexico are key markets within this region. In MEA, the growth is often linked to economic development, infrastructure improvements, and the increasing availability of diverse content. While these regions may present unique challenges related to market maturity and regulatory environments, they also offer significant opportunities for advertisers looking to expand their global reach and connect with diverse cultural segments through the enduring power of television.

- North America: Dominates the market with high CTV penetration, advanced programmatic capabilities, and significant advertising budgets. The United States leads in innovation for addressable TV and cross-platform measurement.

- Europe: A mature market with diverse national regulations, witnessing a strong push towards converged TV and data-driven advertising solutions. Western Europe remains a key contributor, with Eastern Europe showing increasing potential.

- Asia Pacific (APAC): Fastest-growing region, driven by large populations, rising disposable incomes, and increasing smart TV adoption. Countries like China, India, and Japan are pivotal markets.

- Latin America: Exhibits steady growth, propelled by traditional TV viewership and gradual adoption of CTV. Brazil and Mexico are key markets within the region.

- Middle East & Africa (MEA): Emerging market with growth tied to economic development and improving digital infrastructure. Opportunities are expanding as internet and smart TV penetration increases.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the TV Ad spending Market.- Comcast Corporation

- The Walt Disney Company

- Paramount Global

- Warner Bros. Discovery

- Roku Inc.

- Amazon.com, Inc.

- Magnite, Inc.

- The Trade Desk, Inc.

- Nielsen Holdings Plc

- Publicis Groupe

- WPP plc

- Omnicom Group Inc.

- Interpublic Group of Companies, Inc.

- Samba TV

- Innovid

- Tremor International Ltd.

- FreeWheel

- Adform

- Mediaocean

Frequently Asked Questions

Analyze common user questions about the TV Ad spending market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is the current outlook for the TV Ad spending market?

The TV Ad spending market is projected for moderate growth between 2025 and 2033, despite competition from digital platforms. This growth is largely driven by the evolution of TV advertising to include more targeted, measurable, and programmatic solutions, especially through Connected TV (CTV) and addressable advertising. While linear TV remains significant for mass reach, the overall market is adapting to new consumption habits by integrating digital capabilities, indicating a resilient and transforming future.

The market is increasingly focused on data-driven strategies and cross-platform integration to maximize ad effectiveness and demonstrate clear return on investment. This includes advancements in attribution modeling and the development of new ad formats that enhance viewer engagement. The outlook suggests that TV advertising will continue to be a crucial component of marketing strategies, particularly as it evolves to offer greater precision and accountability, appealing to a broader range of advertisers.

How is Connected TV (CTV) impacting TV Ad spending?

Connected TV (CTV) is profoundly impacting TV Ad spending by merging the traditional reach of television with the targeting and measurement capabilities of digital advertising. It allows advertisers to deliver personalized ads to specific households, shifting from a broad broadcast model to a more precise one-to-one or one-to-many approach. This enables more efficient ad spend by reducing waste and increasing relevancy for viewers, leading to higher engagement and better campaign performance.

The rise of CTV also facilitates programmatic TV buying, automating the ad transaction process and allowing for real-time optimization based on performance data. This offers advertisers greater flexibility and agility in their campaigns, similar to digital channels. As consumer viewership continues to shift towards streaming, CTV is becoming an increasingly vital component of the overall TV ad spending landscape, driving innovation and attracting new investments into the television medium.

Is traditional linear TV advertising still effective in the digital age?

Yes, traditional linear TV advertising remains effective in the digital age, particularly for achieving mass reach and building widespread brand awareness. Despite audience fragmentation, major live events, news, and popular programming on linear TV still attract large, simultaneous viewerships, making it an unparalleled medium for broad campaigns. Its ability to create emotional connections and establish brand authority across diverse demographics is a foundational strength.

However, its effectiveness is increasingly enhanced when integrated with digital strategies. Many advertisers now employ converged TV strategies that combine linear TV's extensive reach with the precise targeting and measurement capabilities of Connected TV (CTV) and other digital platforms. This hybrid approach allows brands to maximize their impact by reaching audiences across all screens while also leveraging data to optimize overall campaign performance, ensuring that linear TV continues to play a vital role in comprehensive media plans.

What are the primary challenges for advertisers in the TV Ad spending market?

The primary challenges for advertisers in the TV Ad spending market include adapting to fragmented audience consumption habits, the lack of standardized cross-platform measurement, and intense competition from digital-native advertising platforms. As viewers migrate across linear TV, CTV, and various streaming services, reaching a consistent audience becomes more complex. This fragmentation complicates media planning and necessitates innovative approaches to capture attention.

Moreover, the absence of a unified measurement system across these diverse platforms makes it difficult for advertisers to gain a holistic view of their campaign performance and accurately attribute ROI. This often leads to fragmented data and challenges in justifying TV spend compared to highly measurable digital channels. The strong competitive offerings from digital platforms, which provide granular targeting and real-time optimization, also pressure TV advertisers to continually evolve their strategies and demonstrate competitive value.

How is AI transforming the TV Ad spending market?

Artificial intelligence (AI) is transforming the TV Ad spending market by introducing unprecedented levels of efficiency, precision, and personalization. AI-driven solutions enable enhanced audience targeting through advanced data analytics and predictive modeling, allowing advertisers to identify and reach specific demographic and behavioral segments with greater accuracy. This moves beyond traditional broad demographic targeting to highly granular, household-level ad delivery, optimizing relevance and reducing ad waste.

Furthermore, AI facilitates automated media planning and buying processes, streamlining ad operations and optimizing ad placement across linear and Connected TV platforms in real time. It also powers dynamic creative optimization (DCO), where ad content can be personalized and adapted based on individual viewer preferences and real-time performance data. AI's capabilities extend to improved attribution modeling, linking TV ad exposure to actual consumer actions, and enhancing fraud detection, ultimately leading to more accountable and effective TV advertising campaigns.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted