Truck Fender Market

Truck Fender Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708453 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

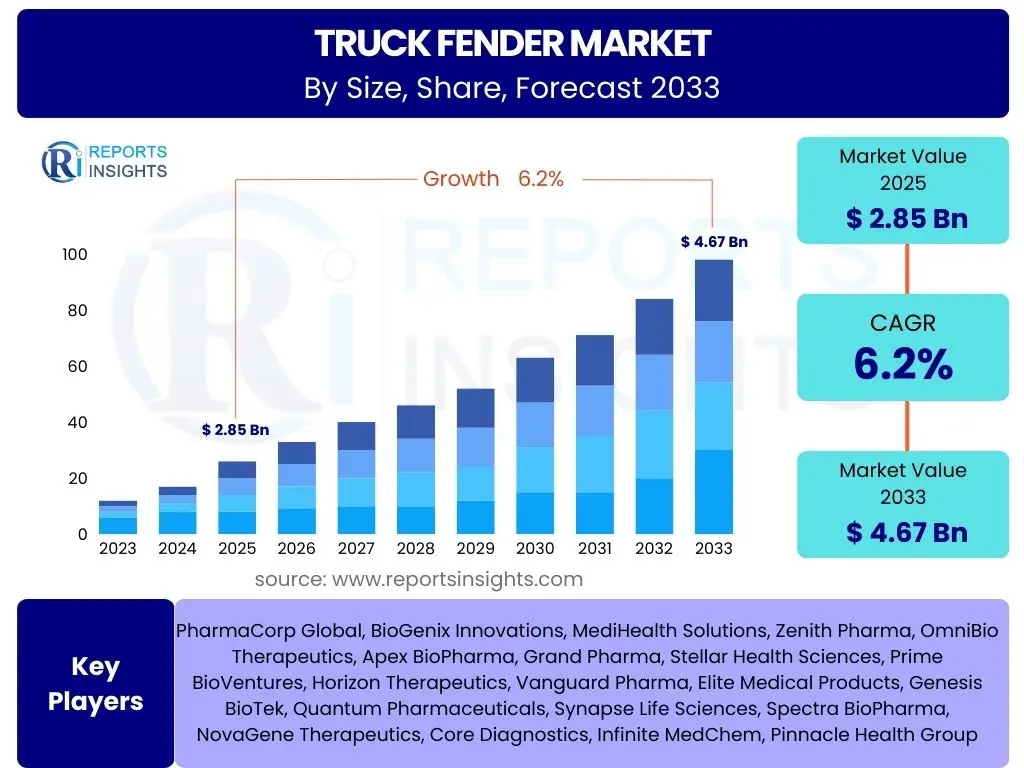

Truck Fender Market Size

According to Reports Insights Consulting Pvt Ltd, The Truck Fender Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.2% between 2025 and 2033. The market is estimated at USD 2.85 Billion in 2025 and is projected to reach USD 4.67 Billion by the end of the forecast period in 2033.

Key Truck Fender Market Trends & Insights

The truck fender market is currently experiencing significant evolution driven by several key factors including the demand for enhanced vehicle aesthetics, improved aerodynamic efficiency, and the integration of advanced materials. Users frequently inquire about the latest innovations in fender design, the impact of electrification on material choices, and the growing emphasis on sustainability within manufacturing processes. There is a clear shift towards lightweight yet durable solutions, often incorporating composite materials, to meet fuel efficiency targets and reduce overall vehicle weight. Furthermore, customization and modular designs are gaining traction, allowing for easier maintenance and personalization.

Another prominent trend involves the increasing adoption of smart manufacturing processes, leveraging automation and data analytics to optimize production and ensure consistent quality. The aftermarket segment also plays a crucial role, with a continuous demand for replacement parts and upgrades that adhere to evolving safety standards and aesthetic preferences. Regulatory pressures regarding vehicle safety, emissions, and pedestrian protection further shape product development, pushing manufacturers towards more robust and compliant fender solutions. The global expansion of logistics and e-commerce has also directly contributed to the growth in commercial vehicle fleets, consequently boosting the demand for truck fenders.

- Growing adoption of lightweight and composite materials for enhanced fuel efficiency.

- Increasing demand for aerodynamic fender designs to reduce drag.

- Emphasis on modular and customizable fender solutions for easier maintenance.

- Integration of advanced manufacturing techniques, including automation and 3D printing.

- Rising focus on sustainable and recycled materials in fender production.

- Evolution of designs to accommodate electric and autonomous truck architectures.

- Stringent safety regulations driving demand for robust and protective fender systems.

AI Impact Analysis on Truck Fender

Artificial Intelligence (AI) is set to profoundly influence the truck fender market, from design and manufacturing to supply chain and maintenance. User inquiries often revolve around how AI can optimize material selection, improve production efficiency, and enable predictive maintenance for fenders. AI-powered generative design tools are revolutionizing the conceptualization phase, allowing engineers to rapidly explore thousands of design iterations that optimize for weight, strength, and aerodynamics, far beyond what traditional methods can achieve. This capability is critical for developing innovative fender designs that meet stringent performance requirements and aesthetic demands while reducing material waste.

In manufacturing, AI is enhancing process automation, predictive quality control, and robotic assembly, leading to higher precision, reduced defects, and faster production cycles. Machine learning algorithms can analyze production data to identify potential issues before they occur, minimizing downtime and optimizing resource utilization. Furthermore, AI contributes to supply chain resilience by forecasting demand more accurately, optimizing inventory levels, and streamlining logistics for raw materials and finished products. While direct AI integration into fenders themselves is less common, the overarching impact of AI on the trucking industry, especially in autonomous vehicle development, will drive demand for specialized, AI-informed fender designs that can integrate with sensor arrays and advanced safety systems.

- AI-driven generative design optimizing fender weight, strength, and aerodynamics.

- Enhanced manufacturing efficiency through AI-powered automation and robotics.

- Predictive maintenance for production machinery and potentially for fender integrity monitoring.

- Improved supply chain management and demand forecasting for fender components.

- AI-enabled quality control and defect detection in the manufacturing process.

- Development of specialized fender designs to accommodate sensors for autonomous trucks.

Key Takeaways Truck Fender Market Size & Forecast

The truck fender market is poised for steady growth, driven primarily by the expansion of global commercial vehicle fleets, continuous advancements in material science, and the increasing stringency of safety and environmental regulations. Users frequently seek to understand the primary growth catalysts, the segments expected to exhibit the strongest performance, and the overarching factors influencing the market's long-term trajectory. A significant takeaway is the ongoing transition towards lightweight, durable, and sustainable materials, which is crucial for achieving better fuel economy and reducing the environmental footprint of heavy-duty vehicles. This shift not only addresses regulatory mandates but also responds to consumer demand for more efficient and eco-friendly transport solutions.

Moreover, the aftermarket segment continues to be a robust revenue stream, underscoring the importance of product longevity and the availability of replacement parts. The forecast indicates sustained investment in research and development aimed at innovative designs and manufacturing processes, including the adoption of smart technologies and AI. Regional dynamics, particularly in emerging economies with rapidly expanding logistics sectors, will play a critical role in shaping market demand. Overall, the market is characterized by a drive for efficiency, durability, and compliance, presenting both opportunities and challenges for stakeholders.

- Robust market growth fueled by expanding commercial vehicle fleets and logistics.

- Shift towards lightweight, sustainable, and high-performance materials.

- Strong influence of stringent safety and environmental regulations on product development.

- Significant contribution from the aftermarket segment to overall market revenue.

- Technological innovation, including AI and advanced manufacturing, as a key growth enabler.

- Emerging economies represent substantial growth opportunities due to infrastructure development.

- Continuous focus on improving aerodynamics and vehicle aesthetics.

Truck Fender Market Drivers Analysis

The truck fender market is significantly propelled by several concurrent factors that collectively contribute to its expansion and evolution. A primary driver is the consistent increase in global commercial vehicle production, directly linked to the booming e-commerce sector, industrial growth, and expanding logistics networks worldwide. As more goods are transported across regions, the demand for trucks, and consequently their components like fenders, naturally rises. This sustained demand from both Original Equipment Manufacturers (OEMs) and the aftermarket segment creates a stable growth environment. Furthermore, the evolving landscape of vehicle design and technology, including the advent of electric and autonomous trucks, necessitates new and specialized fender solutions, driving innovation and market uptake.

Another crucial driver is the increasingly stringent regulatory framework concerning vehicle safety, emissions, and crashworthiness across various global regions. Governments and regulatory bodies are imposing stricter standards that mandate the use of durable, impact-resistant, and pedestrian-friendly fender designs. This regulatory push compels manufacturers to innovate and upgrade their product offerings, ensuring compliance and enhancing safety. Additionally, advancements in material science, particularly in composites and high-strength plastics, allow for the development of lighter yet more robust fenders, which directly contribute to fuel efficiency and vehicle performance, appealing to fleet operators looking to minimize operational costs.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Commercial Vehicle Production & Sales | +2.1% | Global, particularly Asia Pacific & North America | Long-term (2025-2033) |

| Stringent Vehicle Safety & Emissions Regulations | +1.8% | Europe, North America, China | Medium-term (2025-2029) |

| Growth in E-commerce & Logistics Sector | +1.5% | Global, especially developing economies | Long-term (2025-2033) |

| Advancements in Material Science (Lightweight & Durable) | +1.3% | Global | Long-term (2025-2033) |

Truck Fender Market Restraints Analysis

Despite the positive growth trajectory, the truck fender market faces several significant restraints that could impede its expansion. One major challenge is the volatility of raw material prices, particularly for steel, aluminum, and various polymers and composites. Fluctuations in commodity markets can directly impact production costs, leading to increased pricing pressures on manufacturers and potentially higher retail costs for end-users. This unpredictability makes long-term planning and cost management complex, potentially affecting profit margins and market competitiveness. Economic downturns or slowdowns in key industrial sectors, such as construction or freight, can also directly reduce demand for new commercial vehicles, consequently affecting the market for truck fenders.

Another restraint involves the increasingly stringent environmental regulations regarding manufacturing processes and material disposal. While promoting sustainability, these regulations often necessitate costly investments in new production technologies, waste management systems, and compliance measures. This can increase operational overheads for manufacturers, especially smaller and medium-sized enterprises. Furthermore, the long replacement cycles of commercial vehicles, particularly heavy-duty trucks, can limit the demand for new OEM fenders, shifting a significant portion of the market to the aftermarket, which operates on different pricing and distribution dynamics. Intense competition among existing players, coupled with the potential for new entrants, also leads to price wars and compressed profit margins, especially in mature markets.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Raw Material Price Volatility | -1.5% | Global | Medium-term (2025-2029) |

| High Manufacturing & R&D Costs for Advanced Materials | -1.2% | Global | Long-term (2025-2033) |

| Economic Slowdowns Affecting Commercial Vehicle Sales | -1.0% | Europe, North America | Short-term (2025-2027) |

| Stringent Environmental & Disposal Regulations | -0.8% | Europe, North America, China | Long-term (2025-2033) |

Truck Fender Market Opportunities Analysis

The truck fender market presents several compelling opportunities for growth and innovation, driven by evolving vehicle technologies and market demands. A significant opportunity lies in the burgeoning electric truck segment. As the automotive industry shifts towards electrification, there is a growing need for specialized fender designs that accommodate battery packs, charging ports, and unique aerodynamic requirements of electric vehicles. Manufacturers who invest in developing lightweight, high-strength, and perhaps even integrated smart fenders for electric trucks stand to gain a competitive advantage in this rapidly expanding niche. Furthermore, the increasing focus on vehicle customization and personalization, particularly in the aftermarket, opens doors for diverse product offerings, including aesthetic enhancements, specialized coatings, and performance-oriented fender solutions.

Another key opportunity resides in the continuous development and adoption of advanced materials, such as lightweight composites, recycled plastics, and bio-based materials. These materials not only help meet stringent environmental regulations and fuel efficiency targets but also offer superior durability and impact resistance. Companies that can innovate in material science and incorporate these sustainable options into their production processes will appeal to environmentally conscious consumers and fleet operators. Additionally, the expansion into untapped or underserved emerging markets, particularly in Asia Pacific and Latin America, where infrastructure development and commercial vehicle fleet growth are accelerating, represents a significant avenue for market penetration and revenue generation. Strategic partnerships with OEMs for co-development of next-generation fender systems also offer robust growth prospects.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth of Electric & Autonomous Truck Segments | +2.0% | Global, particularly North America, Europe, China | Long-term (2025-2033) |

| Development & Adoption of Sustainable Lightweight Materials | +1.7% | Global | Long-term (2025-2033) |

| Expansion into Emerging Markets | +1.4% | Asia Pacific, Latin America, MEA | Medium-term (2025-2029) |

| Increasing Demand for Aftermarket Customization & Upgrades | +1.1% | North America, Europe | Long-term (2025-2033) |

Truck Fender Market Challenges Impact Analysis

The truck fender market faces several intricate challenges that demand strategic solutions from manufacturers and suppliers. One significant hurdle is adapting to the rapid pace of technological advancements in the broader automotive industry, particularly the transition towards electric, autonomous, and connected vehicles. These new vehicle architectures often require completely redesigned fender systems that can integrate sensors, improve aerodynamics, and accommodate unique structural elements, posing complex R&D and manufacturing challenges. The substantial capital investment required for retooling production lines and developing new material processing capabilities can be a barrier, especially for smaller market participants. Furthermore, maintaining product quality and ensuring compliance with a myriad of international safety and environmental standards, which are constantly evolving, adds another layer of complexity to product development and market entry.

Another critical challenge stems from intense market competition, leading to price erosion and pressure on profit margins. The presence of numerous established players and the emergence of lower-cost manufacturers, particularly in Asia, create a highly competitive landscape where differentiation becomes difficult. This often forces companies to innovate continuously or risk losing market share. Additionally, disruptions in the global supply chain, such as those caused by geopolitical events, natural disasters, or pandemics, can severely impact the availability of raw materials and components, leading to production delays and increased costs. Counterfeit products, which mimic genuine parts but often lack quality and safety standards, also pose a threat, eroding brand trust and legitimate sales. Addressing these challenges requires a combination of technological innovation, robust supply chain management, and strategic market positioning.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Rapid Technological Shifts in Vehicle Design (EV, AV) | -1.8% | Global | Long-term (2025-2033) |

| Intense Market Competition & Price Pressure | -1.5% | Global, particularly Asia Pacific | Medium-term (2025-2029) |

| Supply Chain Disruptions & Raw Material Availability | -1.3% | Global | Short-term (2025-2027) |

| Compliance with Evolving Global Safety & Environmental Standards | -1.0% | Europe, North America | Long-term (2025-2033) |

Truck Fender Market - Updated Report Scope

This report offers a comprehensive analysis of the Truck Fender Market, providing in-depth insights into market size, growth drivers, restraints, opportunities, and challenges across various segments and regions. It includes a detailed forecast from 2025 to 2033, building upon historical data from 2019 to 2023, to present a holistic view of the market's trajectory. The scope encompasses detailed segmentation analysis by material, vehicle type, sales channel, and end-use, providing granular understanding of market dynamics. Furthermore, the report identifies key market trends, analyzes the impact of emerging technologies like AI, and profiles leading market participants to offer a strategic competitive landscape.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 2.85 Billion |

| Market Forecast in 2033 | USD 4.67 Billion |

| Growth Rate | 6.2% |

| Number of Pages | 257 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Automotive Components Inc., Global Fender Solutions, TruckGuard Manufacturing, DuraFender Systems, FleetShield Parts, ProGuard Automotive, Custom Truck Accessories, RoadMaster Fenders, HeavyDuty Gear Inc., TrukKustom Parts, Elite Truck Components, Prime Auto Fenders, Apex Vehicle Solutions, Summit Truck Parts, RhinoFender Co., TransPro Components, Universal Truck Parts, Precision Fabrication Group, Modern Mobility Solutions, Advanced Composites Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The truck fender market is intricately segmented across various dimensions, providing a granular view of its diverse dynamics and demand patterns. These segmentations are critical for understanding market behavior, identifying high-growth areas, and tailoring strategies for specific product types or end-user applications. The primary segmentation categories include material type, vehicle type, sales channel, and end-use, each revealing unique trends and competitive landscapes. Analyzing these segments helps stakeholders pinpoint where demand is strongest and where innovation is most impactful, guiding investment and product development decisions.

For instance, the segmentation by material highlights the shift towards lighter and more durable composites and plastics from traditional metals, driven by fuel efficiency and regulatory pressures. Vehicle type segmentation, on the other hand, distinguishes between the needs of light-duty versus heavy-duty trucks, with specialized requirements for each. The sales channel split between OEM and aftermarket is crucial for understanding distribution strategies and profit margins. Finally, end-use segmentation underscores how different industries, from logistics to construction, have varying demands for fender characteristics such as robustness, weather resistance, and aesthetic appeal. This comprehensive segmentation analysis provides a foundational understanding of the market's structure and operational intricacies.

- By Material: This segment categorizes fenders based on the primary material used in their construction, reflecting trends in durability, weight, and cost.

- Steel Fenders

- Aluminum Fenders

- Fiberglass Fenders

- Plastic/Polymer Fenders (e.g., Polypropylene, ABS)

- Composite Fenders

- By Vehicle Type: Differentiates fenders based on the size and application of the truck, influencing design and material requirements.

- Light-Duty Trucks

- Medium-Duty Trucks

- Heavy-Duty Trucks

- Electric Trucks

- Specialty Trucks (e.g., Vocational, Off-Road)

- By Sales Channel: Distinguishes between direct sales to vehicle manufacturers and sales to the replacement parts market.

- Original Equipment Manufacturer (OEM)

- Aftermarket

- By End-Use: Examines fender demand from various industries utilizing trucks, showcasing specific needs and volumes.

- Logistics & Transportation

- Construction

- Mining

- Agriculture

- Waste Management

- Other Industrial Applications (e.g., Emergency Services, Utility Fleets)

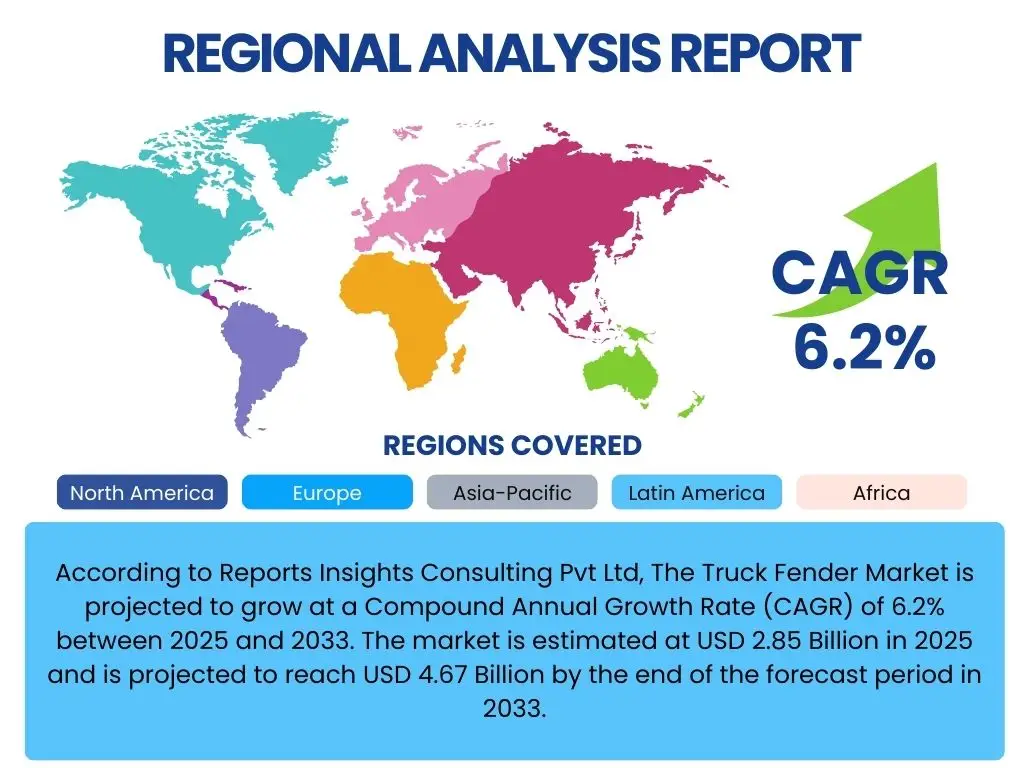

Regional Highlights

The global truck fender market exhibits distinct regional dynamics driven by varying levels of economic development, commercial vehicle production, regulatory frameworks, and infrastructure investments. North America and Europe, as mature markets, are characterized by a strong emphasis on advanced materials, aerodynamic designs, and compliance with stringent safety and environmental regulations. These regions also show a significant aftermarket presence and a growing interest in electric truck components. Innovation in these regions often focuses on high-performance, lightweight solutions that contribute to fuel efficiency and reduced emissions. The demand for heavy-duty truck fenders is consistently high due to extensive freight and logistics operations.

Asia Pacific is projected to be the fastest-growing region, primarily fueled by rapid industrialization, urbanization, and the expansion of the e-commerce sector in countries like China and India. This leads to a substantial increase in commercial vehicle fleets, driving both OEM and aftermarket demand. While cost-effectiveness remains a key factor, there is a growing shift towards better quality and more durable fenders in response to improving infrastructure and increasing regulatory oversight. Latin America and the Middle East & Africa (MEA) represent emerging markets with considerable growth potential, spurred by infrastructure development projects, increasing trade activities, and a rising need for efficient transportation solutions. These regions often prioritize robust and cost-effective fender options suitable for diverse terrains and operating conditions. Each region presents unique opportunities and challenges for market participants to tailor their strategies.

- North America: Dominant market share due to high commercial vehicle sales, advanced logistics networks, and strong aftermarket demand. Emphasis on durable, aerodynamic, and lightweight solutions.

- Europe: Driven by strict environmental and safety regulations, fostering innovation in sustainable materials and advanced designs for fuel efficiency. Growing adoption of electric trucks.

- Asia Pacific (APAC): Fastest-growing region, propelled by booming e-commerce, rapid industrialization, and increasing commercial vehicle production in countries like China and India. Focus on both cost-effective and quality products.

- Latin America: Emerging market with increasing demand due to infrastructure development and expanding trade. Emphasis on robust and durable fenders for challenging road conditions.

- Middle East & Africa (MEA): Growth driven by investments in logistics, construction, and mining sectors. Demand for heavy-duty and resilient fender solutions, often for harsh operating environments.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Truck Fender Market.- Automotive Components Inc.

- Global Fender Solutions

- TruckGuard Manufacturing

- DuraFender Systems

- FleetShield Parts

- ProGuard Automotive

- Custom Truck Accessories

- RoadMaster Fenders

- HeavyDuty Gear Inc.

- TrukKustom Parts

- Elite Truck Components

- Prime Auto Fenders

- Apex Vehicle Solutions

- Summit Truck Parts

- RhinoFender Co.

- TransPro Components

- Universal Truck Parts

- Precision Fabrication Group

- Modern Mobility Solutions

- Advanced Composites Ltd.

Frequently Asked Questions

What is a truck fender and its primary function?

A truck fender is a body part positioned over a wheel, serving primarily to prevent mud, sand, rocks, and other debris from being thrown into the air by the rotating tire, thus protecting the vehicle body, passengers, and other vehicles or pedestrians. It also contributes to the vehicle's aesthetic appeal and aerodynamic efficiency.

What materials are commonly used in manufacturing truck fenders?

Truck fenders are commonly manufactured from materials such as steel, aluminum, fiberglass, various plastics (e.g., polypropylene, ABS), and advanced composites. The choice of material depends on factors like vehicle type, desired durability, weight reduction goals, cost-effectiveness, and specific regulatory requirements.

How do regulations impact the design and production of truck fenders?

Regulations significantly impact truck fender design and production by imposing stringent standards for vehicle safety, crashworthiness, pedestrian protection, and sometimes even material use and recycling. These regulations drive innovation towards more durable, impact-absorbing, and environmentally compliant fender solutions.

What are the key differences between OEM and aftermarket truck fenders?

OEM (Original Equipment Manufacturer) truck fenders are parts supplied directly by the vehicle manufacturer or their approved suppliers, designed to exact specifications. Aftermarket fenders are produced by third-party manufacturers, often offering a wider range of designs, materials, and price points for replacement or customization, though quality can vary.

What emerging trends are shaping the future of the truck fender market?

Emerging trends include a strong focus on lightweight and sustainable materials for improved fuel efficiency and reduced environmental impact, the integration of aerodynamic designs, and the development of specialized fenders for electric and autonomous trucks. Customization options and advanced manufacturing techniques like 3D printing are also gaining prominence.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted