Tractor Market

Tractor Market Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707138 | Last Updated : September 08, 2025 |

Format : ![]()

![]()

![]()

![]()

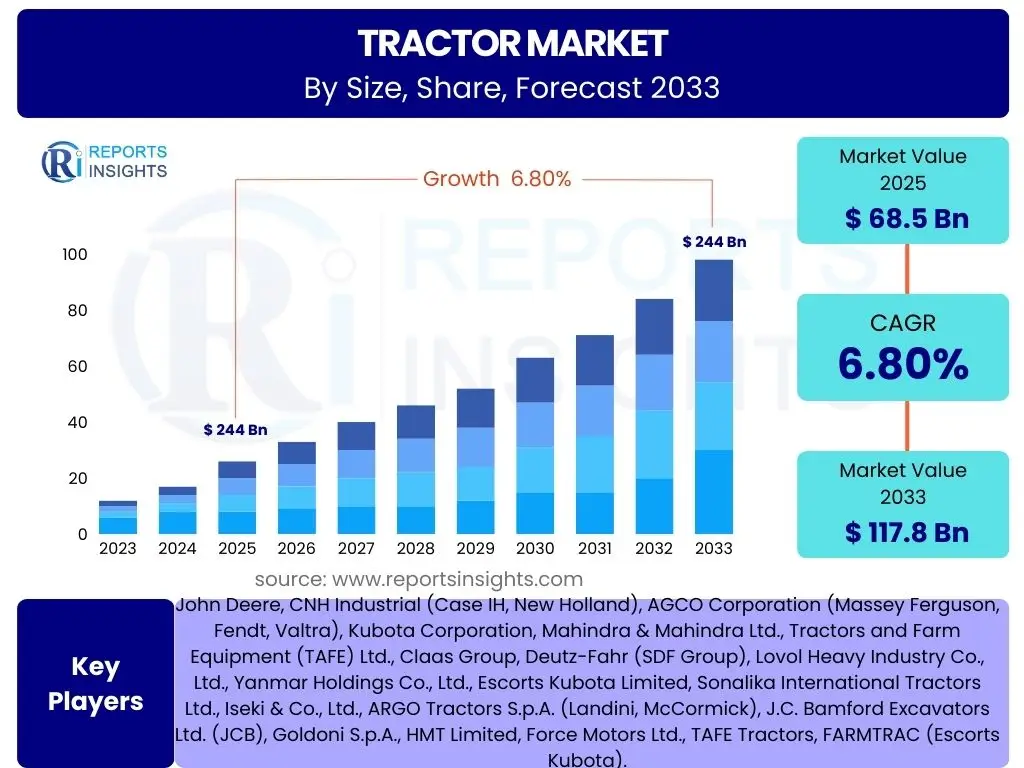

Tractor Market Size

According to Reports Insights Consulting Pvt Ltd, The Tractor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 68.5 billion in 2025 and is projected to reach USD 117.8 billion by the end of the forecast period in 2033.

The global tractor market's expansion is fundamentally driven by the escalating demand for food production worldwide, necessitating enhanced agricultural mechanization. As the global population continues to grow, so does the pressure on agricultural sectors to increase yield and efficiency, which directly translates into higher demand for advanced farming equipment, including tractors. This growth is further supported by government initiatives in various countries aimed at modernizing agriculture, offering subsidies, and promoting farm mechanization, particularly in developing economies where traditional farming methods are being rapidly replaced.

Technological advancements play a crucial role in shaping the market's trajectory, with the introduction of smart tractors, autonomous capabilities, and precision farming technologies driving higher adoption rates. These innovations not only improve operational efficiency and reduce labor costs but also contribute to sustainable farming practices, aligning with global environmental objectives. The shift towards larger and more powerful tractors, capable of handling diverse farming tasks, also contributes significantly to the overall market value, reflecting a trend towards increased productivity and economies of scale for agricultural enterprises.

Key Tractor Market Trends & Insights

The tractor market is undergoing significant transformation, driven by a confluence of technological advancements, evolving agricultural practices, and growing environmental concerns. Key user questions frequently revolve around the adoption of smart farming technologies, the shift towards electric or alternative fuel tractors, the role of automation, and the increasing prevalence of rental and digital service models. Farmers and industry stakeholders are keen to understand how these trends will influence operational efficiency, sustainability, and long-term profitability. The insights suggest a clear trajectory towards more connected, intelligent, and eco-friendly agricultural machinery, redefining traditional farming paradigms.

One prominent trend is the widespread integration of precision agriculture technologies, enabling farmers to optimize resource utilization through GPS-guided steering, variable rate application, and yield monitoring systems. This not only enhances productivity but also minimizes waste and environmental impact. Furthermore, there is a notable increase in the development and adoption of electric and hybrid tractors, driven by stringent emission regulations and a desire for lower operating costs and reduced carbon footprints. These electric models, while still nascent, are gaining traction, particularly in smaller-scale farming and specialized applications.

Another crucial insight points to the growing interest in autonomous and semi-autonomous tractors, which promise to address labor shortages and further improve efficiency. Although full autonomy is still some years away for widespread adoption, advanced driver-assistance systems and automated functions are becoming standard features. Beyond technology, business model innovations such as tractor rental and leasing services are gaining popularity, especially among small and medium-sized farmers who cannot afford outright purchase. Digital platforms for farm management, predictive maintenance, and data analytics are also becoming integral, connecting the entire agricultural ecosystem and providing valuable insights for farmers.

- Adoption of Precision Agriculture Technologies (GPS, Telematics, Sensors)

- Development and Commercialization of Electric and Hybrid Tractors

- Increased Focus on Automation and Autonomous Tractor Features

- Growth of Tractor Rental and Leasing Services

- Integration of Digital Platforms for Farm Management and Data Analytics

- Rising Demand for High-Horsepower and Multi-Functional Tractors

- Emphasis on Ergonomics, Comfort, and Safety Features

AI Impact Analysis on Tractor

Artificial Intelligence (AI) is rapidly transforming the tractor industry, addressing common user questions regarding how advanced technologies can enhance agricultural productivity, reduce labor dependency, and promote sustainable practices. Users are particularly interested in AI's role in enabling autonomous operations, optimizing resource management, and facilitating predictive maintenance. The analysis reveals that AI-driven solutions are moving beyond traditional mechanization to create truly intelligent farming systems, offering unprecedented levels of efficiency and environmental stewardship.

AI's influence is most significant in the realm of autonomous tractors, where algorithms enable self-driving capabilities, path planning, and obstacle detection, thereby reducing the need for continuous human oversight and allowing for 24/7 operation. Furthermore, AI is crucial for precision agriculture, interpreting vast datasets from sensors, drones, and satellite imagery to provide real-time insights for variable rate application of fertilizers and pesticides, optimized irrigation, and targeted harvesting. This data-driven approach ensures resources are used only where and when needed, minimizing waste and maximizing yield.

Beyond field operations, AI also contributes significantly to tractor maintenance and fleet management. Predictive maintenance systems, powered by AI, analyze operational data to forecast potential equipment failures, allowing for proactive servicing and minimizing costly downtime. AI-driven logistics and supply chain optimization for agricultural inputs and outputs further enhance overall farm profitability. While concerns exist regarding initial investment costs and the need for robust digital infrastructure, the long-term benefits of AI in terms of efficiency, sustainability, and increased profitability are compelling, positioning it as a pivotal force in the future of tractor technology.

- Enabling Autonomous Operation and Navigation

- Optimizing Resource Application (e.g., fertilizers, water) through Precision Farming

- Facilitating Predictive Maintenance and Diagnostics for Tractors

- Enhancing Crop Monitoring and Yield Prediction

- Improving Data Analysis for Farm Management Decisions

- Automating Tasks and Reducing Labor Dependence

- Developing Smart Implements and Attachments

Key Takeaways Tractor Market Size & Forecast

Key user questions regarding the tractor market size and forecast often center on identifying the primary growth drivers, the impact of technological advancements, and the regions poised for significant expansion. The market's projected growth indicates a strong trajectory driven by the imperative for increased food production globally and the ongoing mechanization of agriculture in emerging economies. The forecast underscores the critical role of innovation, particularly in smart and sustainable farming solutions, in shaping future demand and market dynamics.

A significant takeaway is the pivotal role of government support and subsidies in stimulating market demand, especially in Asia Pacific and Africa, where agricultural development is a top priority. Moreover, the increasing adoption of precision agriculture technologies and the nascent but growing demand for electric and autonomous tractors are identified as key catalysts for value growth. While unit sales may fluctuate, the value per unit is expected to rise due to higher technological content and advanced features, signaling a premium placed on efficiency and sustainability.

The market is expected to remain competitive, with established players focusing on R&D for advanced solutions and regional expansion. The forecast highlights opportunities for new entrants in specialized segments, such as electric powertrains or AI-driven farm management solutions. Despite potential challenges such as fluctuating raw material costs and climate variability, the fundamental need for efficient food production ensures a sustained demand for tractors, making it a resilient and attractive market for investment and innovation.

- Significant market growth driven by global food demand and agricultural mechanization.

- Technological advancements, including precision farming and automation, are crucial growth enablers.

- Asia Pacific and emerging economies are forecast to be major growth hubs due to government support.

- Increasing average tractor price due to higher technology integration and advanced features.

- Market resilience despite economic headwinds due to essential nature of agriculture.

Tractor Market Drivers Analysis

The global tractor market is propelled by a multitude of factors, each contributing significantly to its expansion. One of the foremost drivers is the burgeoning global population, which necessitates a continuous increase in food production. This demographic trend directly translates into a higher demand for efficient agricultural machinery to maximize crop yields and optimize farming operations. Coupled with this, the persistent shortage of agricultural labor in many regions globally further underscores the need for mechanization, driving farmers to invest in tractors to perform tasks more efficiently and with less manual intervention.

Government initiatives and policies aimed at modernizing agriculture also play a pivotal role. Many nations offer subsidies, incentives, and easy credit facilities to farmers for purchasing advanced farm equipment, including tractors. These supportive measures are designed to boost agricultural productivity, enhance food security, and improve farmers' livelihoods, thereby accelerating tractor adoption. Furthermore, the growing trend of precision agriculture, smart farming, and digitalization in the agricultural sector encourages the uptake of technologically advanced tractors equipped with GPS, telematics, and data analytics capabilities, enhancing efficiency and sustainability.

The increasing economic prosperity of farmers in developing countries, alongside a rise in the average farm size in some regions, also contributes to market growth. As farmers' incomes improve, they are more inclined to invest in capital-intensive machinery to reduce operational costs, increase farm output, and achieve economies of scale. Additionally, the expansion of commercial farming and contract farming practices, particularly in emerging markets, creates a consistent demand for a diverse range of tractors to meet specific agricultural requirements and operational demands efficiently.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Population & Food Demand | +1.5% | Global, particularly Asia Pacific & Africa | Long-term (2025-2033) |

| Agricultural Mechanization & Labor Shortage | +1.2% | North America, Europe, Asia Pacific | Medium-term (2025-2029) |

| Government Support & Subsidies for Farming | +1.0% | India, China, Brazil, ASEAN, EU | Medium-term (2025-2029) |

| Technological Advancements & Precision Farming Adoption | +0.8% | North America, Europe, Oceania | Long-term (2025-2033) |

| Rise in Commercial & Contract Farming | +0.7% | Latin America, Southeast Asia, Eastern Europe | Medium-term (2026-2030) |

Tractor Market Restraints Analysis

Despite robust growth prospects, the tractor market faces several significant restraints that could impede its expansion. One primary concern is the high initial capital investment required for purchasing tractors, especially advanced models equipped with modern technology. This cost barrier can be prohibitive for small and marginal farmers, particularly in developing economies where access to credit and financial resources may be limited. The high cost of maintenance and spare parts further adds to the operational expenditure, making it challenging for farmers with limited budgets to sustain tractor ownership.

Another major restraint is the fragmentation of landholdings in many parts of the world, particularly in Asia. Small, scattered land parcels make the efficient use of large, modern tractors impractical and uneconomical. This structural issue limits the adoption of high-horsepower tractors and favors smaller, less efficient models or the continued reliance on manual labor or animal power. Climate change and unpredictable weather patterns also pose a significant challenge, as extreme weather events like droughts or floods can severely impact agricultural output and, consequently, reduce farmers' purchasing power for new machinery.

Furthermore, stringent emission regulations and environmental standards, particularly in developed regions like Europe and North America, can increase the manufacturing cost of tractors, translating into higher prices for end-users. While these regulations are necessary for environmental protection, they add complexity to design and production, potentially slowing down market growth. The availability of skilled labor to operate and maintain advanced tractors is also a growing concern, especially as agricultural education and training infrastructure may not keep pace with technological advancements in some regions.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Initial Investment & Maintenance Costs | -0.9% | Global, particularly developing economies | Long-term (2025-2033) |

| Land Fragmentation & Small Farm Sizes | -0.8% | Asia Pacific, parts of Africa & Latin America | Long-term (2025-2033) |

| Stringent Emission Regulations | -0.6% | Europe, North America | Medium-term (2025-2029) |

| Climate Change & Weather Volatility | -0.5% | Global, especially vulnerable agricultural regions | Long-term (2025-2033) |

| Shortage of Skilled Operators & Technicians | -0.4% | Global, more pronounced in emerging markets | Medium-term (2026-2030) |

Tractor Market Opportunities Analysis

The tractor market is ripe with opportunities, particularly those stemming from technological advancements and evolving agricultural needs. One significant area of opportunity lies in the burgeoning adoption of precision agriculture technologies. As farmers increasingly seek to optimize resource use, reduce waste, and enhance crop yields, the demand for tractors integrated with advanced GPS, sensors, and data analytics capabilities is expected to surge. This presents a lucrative avenue for manufacturers to innovate and offer smart farming solutions that provide superior efficiency and environmental benefits.

Emerging markets, especially in Asia Pacific and Africa, represent another substantial growth opportunity. These regions are witnessing a rapid push towards agricultural mechanization, driven by government support, rising population, and a shift from subsistence farming to commercial agriculture. The vast unfulfilled demand for modern farm equipment in these areas provides a fertile ground for market penetration for both established players and new entrants, particularly for cost-effective and robust tractor models suited to diverse farming conditions.

Furthermore, the development of electric and alternative fuel tractors offers a unique opportunity to address environmental concerns and achieve lower operational costs. As global awareness about climate change intensifies and fuel prices remain volatile, there is a growing demand for sustainable agricultural machinery. Companies investing in research and development for electric, hybrid, and hydrogen-powered tractors stand to gain a competitive edge. Additionally, the expansion of tractor rental and leasing services, coupled with the rising trend of contract farming, provides new business models that broaden market access, particularly for small and medium-sized farmers who prefer not to incur the high capital cost of outright purchase.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growth in Precision Agriculture & Smart Farming | +1.3% | North America, Europe, Oceania | Long-term (2025-2033) |

| Untapped Potential in Emerging Markets | +1.1% | Asia Pacific, Africa, Latin America | Long-term (2025-2033) |

| Development of Electric & Alternative Fuel Tractors | +0.9% | Europe, North America, Japan | Medium-term (2027-2033) |

| Expansion of Rental & Leasing Services | +0.7% | Global, particularly India, China, Brazil | Medium-term (2025-2029) |

| Increasing Focus on Customized & Specialized Tractors | +0.6% | Global, especially niche agriculture | Medium-term (2026-2030) |

Tractor Market Challenges Impact Analysis

The tractor market, while robust, faces several significant challenges that could temper its growth trajectory. One pervasive challenge is the volatility of raw material prices, including steel, rubber, and various metals. Fluctuations in these prices directly impact manufacturing costs, which manufacturers often pass on to consumers, potentially leading to higher tractor prices and decreased affordability for farmers. This can strain profit margins for manufacturers and reduce demand, especially in price-sensitive markets.

Another critical challenge stems from the increasing complexity of supply chains and the potential for disruptions. Global events such as pandemics, geopolitical tensions, and trade disputes can severely impact the timely availability of components and raw materials, leading to production delays and increased logistical costs. This unpredictability makes inventory management and production planning difficult for tractor manufacturers, affecting their ability to meet market demand consistently and efficiently.

Furthermore, intense market competition among both global giants and regional players poses a significant challenge. Companies are constantly innovating and offering new features at competitive prices, which can lead to price wars and reduced profitability for all participants. Maintaining a competitive edge requires continuous investment in research and development, effective marketing, and a strong distribution network. Finally, farmer indebtedness and financial instability, particularly in regions prone to agricultural distress caused by adverse weather or market price collapses, can severely limit the purchasing power of farmers, directly impacting tractor sales and market growth.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Volatile Raw Material Prices | -0.7% | Global | Short to Medium-term (2025-2028) |

| Supply Chain Disruptions | -0.6% | Global | Short to Medium-term (2025-2028) |

| Intense Market Competition | -0.5% | Global | Long-term (2025-2033) |

| Farmer Indebtedness & Financial Instability | -0.4% | India, Sub-Saharan Africa, parts of Latin America | Long-term (2025-2033) |

| Changing Climate & Extreme Weather Events | -0.3% | Global, specific agricultural zones | Long-term (2025-2033) |

Tractor Market - Updated Report Scope

This comprehensive report offers an in-depth analysis of the global Tractor Market, providing detailed insights into its size, growth trends, drivers, restraints, opportunities, and challenges across various segments and key regions. It examines the market landscape from historical data to future projections, incorporating the impact of technological advancements such as AI and precision farming, alongside evolving market dynamics. The scope covers a thorough examination of market attributes, competitive landscape, and strategic recommendations for stakeholders aiming to navigate this dynamic industry.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 68.5 billion |

| Market Forecast in 2033 | USD 117.8 billion |

| Growth Rate | 6.8% CAGR |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | John Deere, CNH Industrial (Case IH, New Holland), AGCO Corporation (Massey Ferguson, Fendt, Valtra), Kubota Corporation, Mahindra & Mahindra Ltd., Tractors and Farm Equipment (TAFE) Ltd., Claas Group, Deutz-Fahr (SDF Group), Lovol Heavy Industry Co., Ltd., Yanmar Holdings Co., Ltd., Escorts Kubota Limited, Sonalika International Tractors Ltd., Iseki & Co., Ltd., ARGO Tractors S.p.A. (Landini, McCormick), J.C. Bamford Excavators Ltd. (JCB), Goldoni S.p.A., HMT Limited, Force Motors Ltd., TAFE Tractors, FARMTRAC (Escorts Kubota). |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The global tractor market is comprehensively segmented to provide a granular view of its diverse components and dynamics. This segmentation helps in understanding the varying demands and adoption patterns across different farmer needs, operational requirements, technological preferences, and end-use applications. Analyzing these segments individually offers insights into specific market niches and their growth potential, allowing for targeted strategic planning and product development by manufacturers and stakeholders.

The segmentation by horsepower reflects the varying needs of farmers, from small-scale operations requiring low-horsepower tractors to large commercial farms demanding high-horsepower machines for extensive cultivation. Drive type segmentation differentiates between 2-wheel drive, suitable for lighter tasks and dry conditions, and 4-wheel drive, preferred for heavy-duty applications and challenging terrains. Application-based segmentation highlights the versatility of tractors beyond traditional agriculture, extending to construction and industrial uses, showcasing their multi-functional utility.

Technological segmentation, encompassing traditional, smart/precision farming, and autonomous categories, demonstrates the ongoing evolution of tractor capabilities and the market's shift towards advanced, data-driven solutions. Finally, end-use segmentation reveals how different customer groups, including individual farmers, rental services, and government bodies, contribute to overall market demand. Each segment offers distinct opportunities and challenges, influencing market strategies for product design, distribution, and pricing across regional and global contexts.

- By Horsepower:

- Below 40 HP

- 40-100 HP

- Above 100 HP

- By Drive Type:

- 2-Wheel Drive (2WD)

- 4-Wheel Drive (4WD)

- By Application:

- Agriculture

- Construction

- Industrial

- Others

- By Technology:

- Traditional

- Smart/Precision Farming

- Autonomous

- By End Use:

- Individual Farmers

- Rental Services

- Government & Commercial

- Others

Regional Highlights

- Asia Pacific: This region is the largest and fastest-growing market for tractors, primarily driven by large agrarian economies like India and China. Government support for agricultural mechanization, increasing population, rising farmer incomes, and the fragmentation of landholdings favoring smaller tractors contribute significantly to market growth. Countries like India are major production hubs and consumers of tractors, particularly in the lower to mid-horsepower segments.

- North America: Characterized by large farm sizes and a high adoption rate of advanced farming technologies, North America is a mature but technologically forward market. The demand here is largely for high-horsepower, technologically advanced tractors equipped with precision agriculture, automation, and telematics systems. The region leads in the adoption of smart farming solutions and is a key market for autonomous and electric tractor innovations.

- Europe: The European tractor market is driven by stringent emission regulations, a strong focus on sustainability, and the adoption of high-tech, fuel-efficient, and precision farming tractors. There's a growing preference for specialty tractors (e.g., vineyard, orchard) and a rising trend in electric and alternative fuel models. Western Europe represents a technologically advanced market, while Eastern Europe presents growth opportunities through agricultural modernization.

- Latin America: This region exhibits significant growth potential due to increasing agricultural land utilization, government investments in modern farming, and rising demand for commercial agriculture. Countries like Brazil and Argentina are key markets, showing a growing appetite for medium to high-horsepower tractors as farming operations scale up and mechanization efforts intensify.

- Middle East and Africa (MEA): The MEA region is poised for substantial growth in tractor adoption, propelled by food security concerns, government initiatives to boost agricultural output, and the expansion of irrigated land. While still nascent in terms of mechanization compared to other regions, the market offers considerable opportunities for basic and mid-range tractors. Challenges like climate variability and financing remain, but the fundamental need for agricultural development drives demand.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Tractor Market.- John Deere

- CNH Industrial

- AGCO Corporation

- Kubota Corporation

- Mahindra & Mahindra Ltd.

- Tractors and Farm Equipment (TAFE) Ltd.

- Claas Group

- Deutz-Fahr (SDF Group)

- Lovol Heavy Industry Co., Ltd.

- Yanmar Holdings Co., Ltd.

- Escorts Kubota Limited

- Sonalika International Tractors Ltd.

- Iseki & Co., Ltd.

- ARGO Tractors S.p.A.

- J.C. Bamford Excavators Ltd. (JCB)

- New Holland Agriculture

- Fendt

- Valtra

- Kioti

- Shandong Lovol Heavy Industry Co., Ltd.

Frequently Asked Questions

What is the current market size and projected growth for the Tractor Market?

The global Tractor Market is estimated at USD 68.5 billion in 2025 and is projected to reach USD 117.8 billion by 2033, growing at a Compound Annual Growth Rate (CAGR) of 6.8%.

What are the key trends shaping the Tractor Market?

Key trends include the increasing adoption of precision agriculture technologies, the development of electric and hybrid tractors, advancements in automation and autonomous features, growth in tractor rental and leasing services, and the integration of digital platforms for farm management.

How is AI impacting the Tractor industry?

AI is significantly impacting the tractor industry by enabling autonomous operation, optimizing resource application through precision farming, facilitating predictive maintenance, enhancing crop monitoring, and improving data analysis for farm management decisions, leading to increased efficiency and sustainability.

Which regions are expected to drive the most growth in the Tractor Market?

Asia Pacific is expected to be the largest and fastest-growing region due to agricultural mechanization efforts, government support, and rising food demand. Latin America and parts of Africa also show significant growth potential.

Who are the leading manufacturers in the global Tractor Market?

Leading manufacturers in the global Tractor Market include John Deere, CNH Industrial, AGCO Corporation, Kubota Corporation, Mahindra & Mahindra Ltd., and Tractors and Farm Equipment (TAFE) Ltd., among others, who are investing in advanced technologies and expanding their global presence.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted