Tight Gas Market

Tight Gas Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_678127 | Last Updated : July 18, 2025 |

Format : ![]()

![]()

![]()

![]()

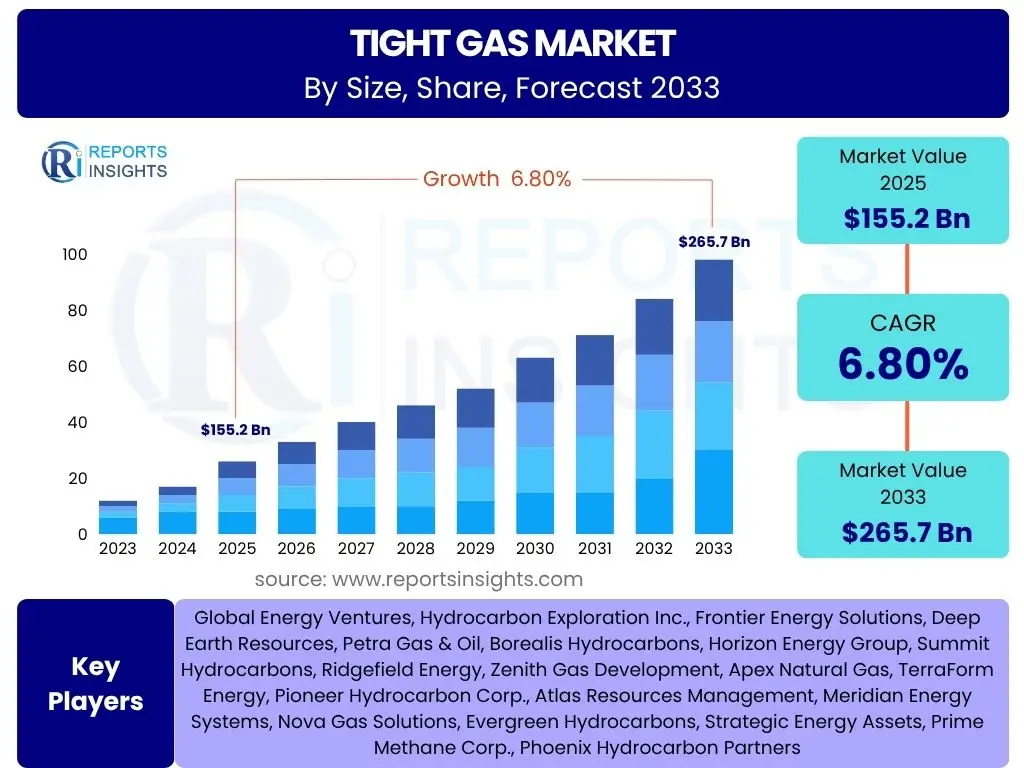

Tight Gas Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033, valued at USD 78.5 billion in 2025 and is projected to grow to USD 115.3 billion by 2033 the end of the forecast period.

Key Tight Gas Market Trends & Insights

The global tight gas market is undergoing a significant transformation, driven by a confluence of technological advancements, evolving energy demands, and shifting geopolitical landscapes. Innovations in drilling and extraction techniques are continuously unlocking new reserves, making previously uneconomical resources viable. Simultaneously, the growing global population and industrial expansion are fueling a sustained demand for cleaner energy sources, positioning natural gas, including tight gas, as a critical component of the future energy mix. Environmental regulations and the global push towards decarbonization are also influencing market dynamics, encouraging the adoption of cleaner production methods and integrated energy solutions.

The market is characterized by increasing investment in infrastructure development to support enhanced production and distribution. Regional disparities in regulatory frameworks and geological endowments play a crucial role in shaping investment decisions and market penetration. Furthermore, the integration of advanced data analytics and artificial intelligence is becoming increasingly vital for optimizing operational efficiencies and enhancing exploration success rates, signifying a lean towards more technologically sophisticated extraction processes. This blend of technological prowess, market demand, and strategic investments defines the current trajectory of the tight gas sector.

The tight gas market is witnessing several prominent trends that are reshaping its landscape. These trends encompass technological innovation, shifts in global energy consumption patterns, and a heightened focus on environmental sustainability, all contributing to the sector's dynamic evolution. Operators are increasingly adopting advanced digital tools and automation to improve efficiency and reduce operational costs, making tight gas extraction more competitive. Furthermore, geopolitical developments continue to influence supply chains and investment flows, highlighting the strategic importance of energy security in national policies.

- Advanced drilling and hydraulic fracturing technologies enhancing recovery rates.

- Increasing global energy demand, particularly from industrial and power generation sectors.

- Focus on natural gas as a bridge fuel in the energy transition.

- Growing investments in exploration and production in unconventional plays.

- Digitalization and automation of field operations for improved efficiency.

- Shifting geopolitical dynamics impacting supply and demand chains.

- Enhanced environmental regulations promoting cleaner extraction methods.

AI Impact Analysis on Tight Gas

Artificial Intelligence (AI) is rapidly transforming the tight gas industry, offering unprecedented opportunities to optimize operations, enhance decision-making, and improve safety across the entire value chain. From the initial stages of geological exploration to the final production and distribution, AI algorithms are being deployed to analyze vast datasets, identify patterns, and predict outcomes with remarkable accuracy. This integration of AI is leading to a paradigm shift in how tight gas resources are discovered, developed, and managed, marking a significant leap forward in operational intelligence.

The application of AI extends to various critical areas within the tight gas sector, including seismic data interpretation, reservoir modeling, and drilling optimization. AI-powered predictive maintenance programs are minimizing downtime by anticipating equipment failures, while autonomous drilling systems are improving efficiency and reducing human error. Furthermore, AI is crucial in optimizing well placement, managing fluid injection for hydraulic fracturing, and monitoring environmental impacts, contributing to more sustainable and cost-effective operations. The ability of AI to process complex, multi-dimensional data sets allows for more informed strategic planning and real-time operational adjustments, making tight gas extraction more precise and profitable.

AI's influence is particularly evident in improving the economic viability and environmental footprint of tight gas extraction. Machine learning models can predict reservoir behavior more accurately, leading to higher recovery rates and reduced waste. In logistics and supply chain management, AI optimizes transportation routes and inventory, further cutting costs and emissions. The predictive capabilities of AI also aid in risk assessment, helping companies navigate volatile market conditions and regulatory changes more effectively. This technological integration is not merely an incremental improvement but a fundamental reshaping of industry practices towards a more intelligent, efficient, and sustainable future.

- Optimizing seismic data interpretation for more accurate geological mapping.

- Predictive analytics for enhanced reservoir performance and production forecasting.

- AI-driven automated drilling systems improving efficiency and precision.

- Predictive maintenance reducing equipment downtime and operational costs.

- Real-time monitoring and anomaly detection for enhanced safety and environmental compliance.

- Machine learning models for optimizing hydraulic fracturing fluid composition and injection.

- Enhanced supply chain logistics and energy trading through AI-driven insights.

Key Takeaways Tight Gas Market Size & Forecast

- The global tight gas market is projected to reach USD 115.3 billion by 2033.

- The market is expected to grow at a CAGR of 4.8% from 2025 to 2033.

- North America currently dominates the market due to extensive shale gas reserves and advanced technology.

- Asia Pacific is anticipated to exhibit the highest growth rate driven by increasing energy demand.

- Key growth drivers include technological advancements in extraction and rising global energy consumption.

- Environmental regulations and public opposition pose significant restraints to market expansion.

- Opportunities exist in the development of cleaner extraction technologies and integrated energy solutions.

- Challenges include significant capital intensity and the need for large volumes of water for fracturing.

Tight Gas Market Drivers Impact Analysis

The tight gas market is significantly influenced by a range of powerful drivers that collectively propel its growth and expansion. These drivers are primarily rooted in the increasing global demand for energy, advancements in extraction technologies, and the strategic importance of natural gas in the global energy transition. As industrialization and urbanization continue globally, particularly in emerging economies, the demand for reliable and relatively cleaner energy sources like tight gas escalates. This fundamental demand underpins much of the investment and development in the sector, ensuring a consistent need for its output.

Technological innovation plays a pivotal role, continuously improving the efficiency and economic viability of tight gas extraction. Breakthroughs in horizontal drilling and multi-stage hydraulic fracturing have unlocked vast reserves that were previously inaccessible or uneconomical. Ongoing research and development efforts are focused on further reducing costs, minimizing environmental impacts, and enhancing recovery rates, making tight gas an increasingly competitive energy option. These technological advancements not only expand the potential supply but also make extraction processes more appealing to operators and investors.

Furthermore, the role of natural gas as a cleaner alternative to coal and oil in power generation and industrial applications supports the tight gas market's growth. As nations strive to reduce carbon emissions and transition to a lower-carbon economy, natural gas is often favored as a "bridge fuel." Government policies and energy security concerns in various regions also contribute to the push for domestic energy production, leading to increased exploration and production of unconventional gas resources like tight gas. These combined factors create a robust environment for sustained market development.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Energy Demand | +1.5% | Global, particularly Asia Pacific, North America | Short to Long-term |

| Advancements in Drilling & Fracturing Technologies | +1.2% | North America, Europe, China | Medium to Long-term |

| Natural Gas as a Transition Fuel | +1.0% | Global, especially Europe, Asia Pacific | Medium-term |

| Geopolitical Focus on Energy Security | +0.8% | Europe, North America, Middle East | Short to Medium-term |

| Favorable Government Policies & Incentives | +0.5% | North America, Argentina, China | Medium-term |

Tight Gas Market Restraints Impact Analysis

Despite its significant growth potential, the tight gas market faces several notable restraints that can impede its expansion and adoption. Environmental concerns constitute a primary barrier, particularly regarding the high water consumption involved in hydraulic fracturing and the potential for groundwater contamination. Public perception and opposition to these environmental risks often lead to stricter regulatory oversight and permit delays, increasing the operational complexities and costs for operators. The debate around methane emissions from natural gas operations also adds to the environmental scrutiny, challenging the perception of tight gas as a cleaner energy source.

Regulatory hurdles and evolving policy frameworks represent another significant restraint. Governments worldwide are increasingly scrutinizing unconventional drilling practices, leading to moratoriums, stricter environmental compliance requirements, and increased taxation. These unpredictable policy shifts can create uncertainty for investors and operators, discouraging long-term capital commitments. The complex and often fragmented regulatory landscape across different jurisdictions means that companies must navigate a diverse set of rules, which can be time-consuming and expensive, thereby slowing down project development and market entry.

Furthermore, the capital-intensive nature of tight gas exploration and production, coupled with the volatility of natural gas prices, poses substantial financial risks. Developing tight gas fields requires significant upfront investment in specialized equipment, infrastructure, and drilling operations. Fluctuations in global natural gas prices can severely impact profitability and return on investment, making it challenging for companies to secure funding or justify new projects during periods of low prices. The competition from rapidly expanding renewable energy sources also acts as a long-term restraint, as green energy alternatives become increasingly cost-competitive and preferred for sustainable development goals.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Environmental Concerns & Regulations (Water Usage, Methane Emissions) | -1.3% | Global, particularly Europe, North America | Long-term |

| Public Opposition & Social License to Operate | -0.9% | North America, Europe, Australia | Medium to Long-term |

| Volatile Natural Gas Prices | -0.8% | Global | Short to Medium-term |

| High Capital Intensity & Exploration Costs | -0.7% | Global | Long-term |

| Competition from Renewable Energy Sources | -0.5% | Global | Long-term |

Tight Gas Market Opportunities Impact Analysis

The tight gas market is ripe with opportunities that can significantly accelerate its growth trajectory and enhance its long-term viability. One of the most promising avenues lies in the continuous advancement and deployment of innovative extraction technologies. Research into more efficient and environmentally friendly fracturing fluids, alternative stimulation techniques, and digitalized field operations holds the potential to unlock more reserves at lower costs and with reduced ecological footprints. Such technological leaps can expand the geographical scope of viable tight gas plays and improve overall economic returns, making new projects more attractive for investment and development.

The increasing global demand for energy, particularly in emerging economies, presents a substantial market expansion opportunity. As countries like China and India continue their industrial development and urbanization, their energy needs are escalating rapidly. Tight gas, with its relatively abundant reserves and cleaner burning properties compared to coal, can play a crucial role in meeting this demand, especially in regions seeking to diversify their energy mix and improve air quality. Strategic partnerships and investments in these high-growth regions can unlock significant market potential and establish new supply chains.

Furthermore, the integration of tight gas with carbon capture, utilization, and storage (CCUS) technologies offers a compelling opportunity to align natural gas production with global climate goals. By capturing and storing CO2 emissions from tight gas processing and power generation, the industry can significantly reduce its carbon footprint, enhancing its environmental credentials and securing its role in a low-carbon future. The development of integrated energy solutions, where tight gas complements renewable energy sources as a reliable baseload power, also represents a strategic opportunity to provide energy security while progressing towards sustainability objectives. These synergistic opportunities position tight gas as a crucial component of a balanced and sustainable energy portfolio.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Technological Innovation for Enhanced Recovery & Reduced Environmental Impact | +1.4% | Global, particularly North America, Europe | Medium to Long-term |

| Growing Energy Demand in Emerging Economies | +1.1% | Asia Pacific (China, India), Latin America | Short to Long-term |

| Integration with Carbon Capture & Storage (CCS) Technologies | +0.9% | North America, Europe, Middle East | Long-term |

| Development of New Unconventional Plays | +0.7% | Argentina, China, Australia | Medium to Long-term |

| Digital Transformation & AI-driven Optimization | +0.6% | Global | Short to Medium-term |

Tight Gas Market Challenges Impact Analysis

The tight gas market, while robust, confronts several significant challenges that require strategic navigation for sustained growth and profitability. One of the foremost challenges is the substantial capital intensity required for exploration, development, and production. Establishing and operating tight gas wells demands significant upfront investment in specialized drilling rigs, fracturing equipment, and pipeline infrastructure, making it a capital-heavy industry. This financial commitment is further exacerbated by the inherent risks associated with unconventional resource extraction, including the uncertainty of reserve estimation and production rates, which can deter potential investors and necessitate robust financial planning.

Environmental and regulatory complexities also present a persistent challenge. The use of hydraulic fracturing, while essential for tight gas extraction, often faces public scrutiny and strict environmental regulations concerning water usage, wastewater disposal, and potential seismic activity. Compliance with diverse and evolving regulatory frameworks across different regions can be costly and time-consuming, leading to project delays and increased operational expenses. Moreover, concerns about methane leakage from wellheads and pipelines contribute to the greenhouse gas emission debate, placing additional pressure on the industry to adopt more rigorous environmental monitoring and mitigation practices.

Furthermore, geopolitical instabilities and volatile energy prices pose significant external challenges. Supply chain disruptions, trade tensions, or political unrest in key energy-producing or consuming regions can directly impact the tight gas market by affecting demand, investment flows, and the availability of essential equipment and services. The inherent volatility of global natural gas prices, driven by supply-demand dynamics and external economic factors, creates revenue uncertainty for operators, making long-term financial forecasting and investment decisions particularly complex. Navigating these multifaceted challenges requires innovative solutions, adaptive strategies, and strong stakeholder engagement to ensure the market's resilience and continued development.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Upfront Capital Investment and Operating Costs | -1.1% | Global | Long-term |

| Water Scarcity and Management for Hydraulic Fracturing | -0.9% | North America, Australia, China | Medium to Long-term |

| Methane Emissions and Climate Change Concerns | -0.8% | Global, particularly Europe, North America | Long-term |

| Geopolitical Instability and Supply Chain Disruptions | -0.7% | Global, particularly Europe, Middle East | Short to Medium-term |

| Depletion Rates of Mature Tight Gas Fields | -0.6% | North America | Long-term |

Tight Gas Market - Updated Report Scope

This comprehensive market research report offers an in-depth analysis of the global tight gas market, providing stakeholders with crucial insights into its current state and future trajectory. It delineates the market size, historical trends, and robust forecasts, encompassing key growth drivers, significant restraints, emerging opportunities, and inherent challenges that define the industry landscape. The report's scope is meticulously designed to provide actionable intelligence, aiding business professionals and decision-makers in navigating the complexities of the tight gas sector and capitalizing on its potential. It delves into detailed segmentation, regional dynamics, and competitive analysis, presenting a holistic view of the market ecosystem.

| Report Attributes | Report Details |

|---|---|

| Report Name | Tight Gas Market |

| Market Size in 2025 | USD 78.5 billion |

| Market Forecast in 2033 | USD 115.3 billion |

| Growth Rate | CAGR of 2025 to 2033 4.8% |

| Number of Pages | 200+ |

| Key Companies Covered | Exxon Mobil, Royal Dutch Shell, Chevron, CNPC, Sinopec Group, Canadian Natural, YPF, Valeura Energy |

| Segments Covered | By Type, By Application, By End-Use Industry, and By Region |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Customization Scope | Avail customised purchase options to meet your exact research needs. Request For Customization |

Segmentation Analysis

The tight gas market is extensively segmented to provide a granular understanding of its diverse components and their respective contributions to overall market dynamics. This segmentation facilitates a detailed analysis of specific product types and their varied applications across different sectors, offering insights into demand patterns and growth areas. Understanding these segments is crucial for strategic planning, allowing businesses to tailor their offerings to specific market needs and identify niche opportunities for development and expansion within the tight gas industry.

Market Product Type Segmentation:-- Processed Tight Gas

- Unprocessed Tight Gas

- Residential

- Commercial

- Industrial Production

- Power Generation

- Others

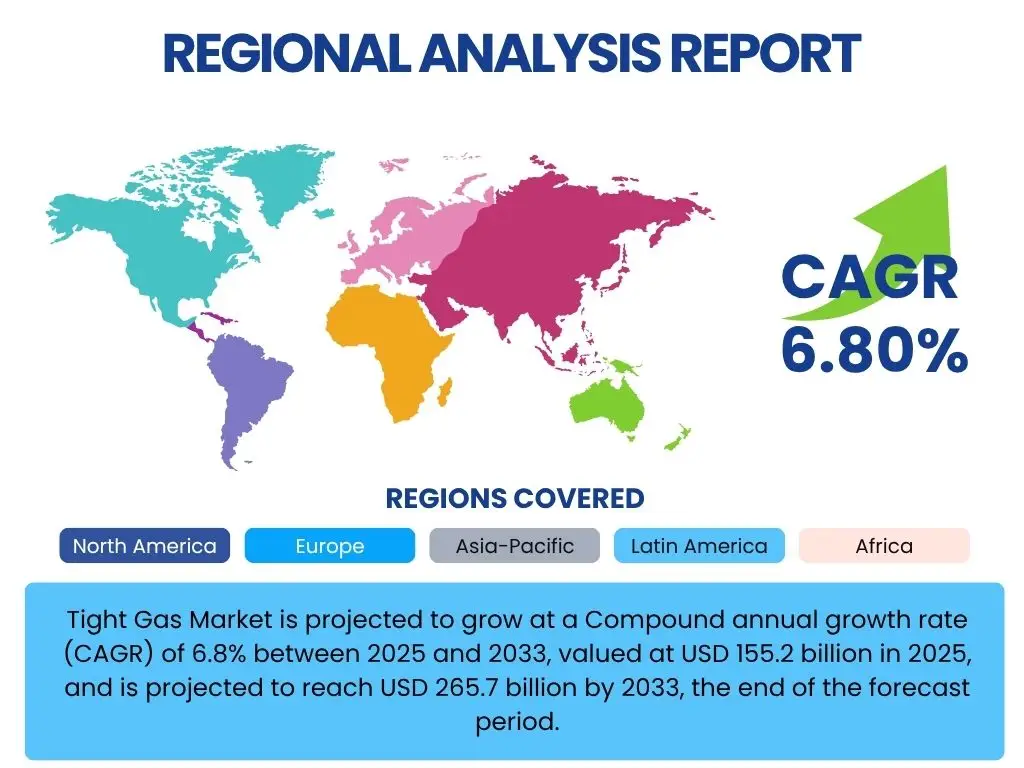

Regional Highlights

The tight gas market exhibits distinct regional dynamics, influenced by geological endowments, technological advancements, regulatory environments, and energy demands across various continents. These regional nuances are critical for understanding global supply-demand balances and identifying key investment hubs. Each region presents a unique set of opportunities and challenges, shaping the overall market trajectory.

- North America: This region stands as the undisputed leader in the tight gas market, primarily driven by the extensive development of shale gas formations in the United States and Canada. Advanced horizontal drilling and hydraulic fracturing technologies have unlocked vast unconventional reserves, making it a global hub for tight gas production. The robust pipeline infrastructure and established regulatory frameworks further support sustained growth.

- Asia Pacific (APAC): Expected to be the fastest-growing region, APAC's tight gas market is propelled by surging energy demand from rapidly industrializing economies like China and India. While still in nascent stages compared to North America, significant investments in exploration and technology transfer are underway, with China actively pursuing its own tight gas reserves to enhance energy security.

- Europe: The European tight gas market faces significant regulatory and public acceptance challenges, leading to slower development. While countries like Poland and the UK possess potential reserves, environmental concerns and strong public opposition have hindered widespread commercial production. Focus remains on energy diversification and importing natural gas.

- Latin America: Argentina leads the tight gas market in Latin America, particularly with the Vaca Muerta formation in Patagonia, which holds substantial unconventional gas resources. Favorable government policies and foreign investments are encouraging exploration and production, positioning the region as a significant emerging player. Other countries are also assessing their tight gas potential.

- Middle East and Africa (MEA): This region holds considerable tight gas potential, though it remains largely underexplored compared to conventional gas. Countries like Saudi Arabia and Algeria are investing in unconventional gas development to meet rising domestic energy demand and free up conventional gas for export. Challenges include water scarcity and the need for specialized technology.

Top Key Players:

The market research report covers the analysis of key stake holders of the Tight Gas Market. Some of the leading players profiled in the report include -:- Exxon Mobil

- Royal Dutch Shell

- Chevron

- CNPC

- Sinopec Group

- Canadian Natural

- YPF

- Valeura Energy

Frequently Asked Questions:

What is tight gas and how is it extracted?

Tight gas is natural gas trapped in low-permeability rock formations, such as sandstone and limestone, that do not allow gas to flow easily. It is primarily extracted using advanced techniques like horizontal drilling and hydraulic fracturing (fracking), which involve drilling a well horizontally into the gas-rich rock and then injecting a high-pressure mixture of water, sand, and chemicals to create fractures, allowing the gas to flow to the surface.

What is the market size forecast for the Tight Gas Market?

The global Tight Gas Market is projected to be valued at approximately USD 78.5 billion in 2025 and is forecasted to grow to USD 115.3 billion by 2033. This growth represents a Compound Annual Growth Rate (CAGR) of 4.8% between 2025 and 2033.

Which regions are leading the Tight Gas Market and why?

North America, particularly the United States and Canada, is the leading region in the Tight Gas Market. This dominance is attributed to vast unconventional gas reserves, early adoption and continuous innovation in hydraulic fracturing and horizontal drilling technologies, and well-established energy infrastructure and regulatory support.

What are the primary drivers for the growth of the Tight Gas Market?

The main drivers for the Tight Gas Market's growth include the increasing global energy demand, especially from industrial and power generation sectors; continuous advancements in drilling and hydraulic fracturing technologies that improve extraction efficiency; and the strategic positioning of natural gas as a bridge fuel in the global energy transition towards lower-carbon emissions.

What are the key challenges facing the Tight Gas Market?

The Tight Gas Market faces several challenges, including significant upfront capital investment and high operating costs, environmental concerns related to water usage and potential methane emissions from hydraulic fracturing, and public opposition to unconventional drilling practices. Additionally, the volatility of natural gas prices and competition from rapidly developing renewable energy sources pose economic hurdles.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted