Thin Film Capacitor Market

Thin Film Capacitor Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_702237 | Last Updated : July 31, 2025 |

Format : ![]()

![]()

![]()

![]()

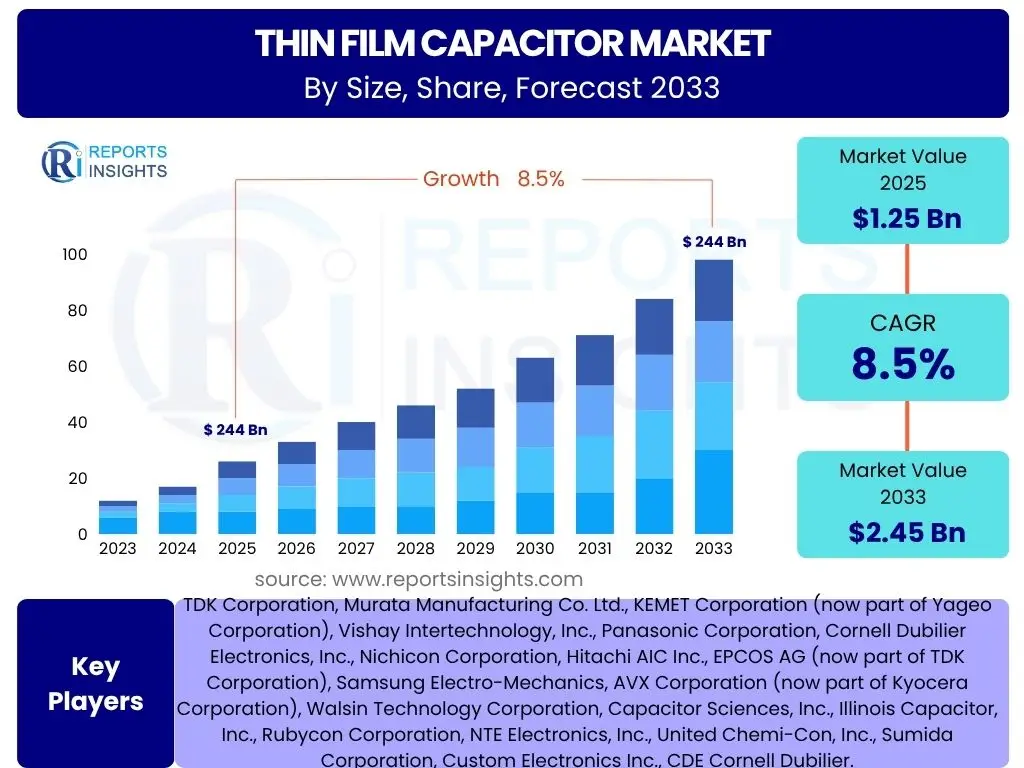

Thin Film Capacitor Market Size

According to Reports Insights Consulting Pvt Ltd, The Thin Film Capacitor Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 8.5% between 2025 and 2033. The market is estimated at USD 1.25 billion in 2025 and is projected to reach USD 2.45 billion by the end of the forecast period in 2033.

Key Thin Film Capacitor Market Trends & Insights

The Thin Film Capacitor market is currently experiencing significant shifts driven by advancements in material science and evolving application demands. Users frequently inquire about the latest technological advancements, the impact of miniaturization, and the increasing adoption across various high-growth industries. Key trends highlight a move towards higher energy density, improved temperature stability, and enhanced performance in high-frequency environments, directly addressing the needs of modern electronics. Furthermore, the push for sustainable manufacturing processes and the development of eco-friendly materials are becoming increasingly prominent in market discussions, reflecting a broader industry commitment to environmental responsibility.

Market insights suggest a strong correlation between the rise of compact, high-performance electronic devices and the demand for advanced thin film capacitors. The integration of these capacitors into power electronics, communication systems, and medical implants underscores their critical role in enabling next-generation technologies. There is also a notable trend towards customization and specialized solutions, as standard off-the-shelf components may not always meet the stringent requirements of emerging applications. This focus on bespoke designs is fostering innovation and collaboration between manufacturers and end-users, driving further market expansion.

Anticipated trends indicate continued growth in the automotive sector, particularly with the proliferation of electric vehicles (EVs) and advanced driver-assistance systems (ADAS), which require robust and reliable passive components. Similarly, the expansion of 5G infrastructure and the Internet of Things (IoT) ecosystem will further fuel demand for high-frequency, low-loss capacitors. The market is also witnessing a trend towards multi-layer thin film capacitors that offer higher capacitance values within smaller form factors, catering to the ongoing miniaturization of electronic devices and the increasing complexity of integrated circuits.

- Miniaturization and compact device integration

- Increased demand from electric vehicles (EVs) and hybrid electric vehicles (HEVs)

- Growth in high-frequency applications (5G, IoT)

- Advancements in material science for improved performance

- Rising adoption in renewable energy systems

AI Impact Analysis on Thin Film Capacitor

Common user questions regarding AI's impact on the Thin Film Capacitor market often revolve around its potential to revolutionize design, manufacturing, and quality control processes. There is significant interest in how artificial intelligence can optimize material selection, predict performance characteristics, and accelerate the development cycle for new capacitor technologies. Users also frequently ask about AI's role in enhancing manufacturing efficiency, reducing defects, and implementing predictive maintenance protocols within production facilities. The general expectation is that AI will streamline operations and lead to more advanced, reliable, and cost-effective thin film capacitors.

AI’s influence extends to various stages of the thin film capacitor lifecycle. In research and development, machine learning algorithms can analyze vast datasets of material properties and performance simulations to identify optimal compositions and structures for specific applications, significantly reducing the time and cost associated with traditional trial-and-error methods. This accelerates the discovery of novel materials with superior dielectric properties or enhanced thermal stability, pushing the boundaries of capacitor performance. Furthermore, AI-driven simulations can predict the behavior of capacitors under various operational stresses, leading to more robust designs and extended product lifespans.

Within manufacturing, AI-powered systems are being deployed for real-time process monitoring, anomaly detection, and automated quality inspection. Computer vision systems combined with AI can identify microscopic defects on thin film layers with unprecedented accuracy, minimizing waste and improving overall product yield. Predictive analytics can anticipate equipment failures, enabling proactive maintenance and reducing downtime. The integration of AI into manufacturing lines promises a new era of smart factories for thin film capacitors, characterized by higher precision, greater efficiency, and superior product consistency, ultimately impacting market supply and quality standards.

- Optimized material design and selection through machine learning

- Enhanced manufacturing process control and efficiency

- Predictive maintenance for production equipment

- Automated quality inspection and defect detection

- Accelerated R&D cycles for new capacitor formulations

Key Takeaways Thin Film Capacitor Market Size & Forecast

Common user questions regarding key takeaways from the Thin Film Capacitor market size and forecast typically center on identifying the primary growth drivers, understanding the market's long-term sustainability, and pinpointing critical investment areas. Users seek concise summaries of what truly matters for market participants and observers. The dominant takeaway is the robust and sustained growth projected for the market, underpinned by relentless technological innovation and the pervasive integration of electronics across all industries. This growth is not merely incremental but represents a fundamental shift towards higher performance and miniaturization requirements that thin film capacitors are uniquely positioned to address.

Another crucial insight is the direct correlation between macro-level technological advancements, such as the electrification of transportation and the expansion of digital infrastructure, and the specific demand for thin film capacitors. These components are not just passive elements but active enablers of energy efficiency, signal integrity, and system reliability in these burgeoning fields. The market forecast underscores a period of significant investment in research and development, as manufacturers strive to meet increasingly stringent performance specifications and cost pressures. This competitive landscape will likely drive further innovation, leading to more advanced and versatile products.

The market's resilience is also a significant takeaway, demonstrating its ability to adapt to economic fluctuations and supply chain challenges through diversification of applications and a focus on critical, high-value segments. Emerging economies are expected to play a pivotal role in future growth, as their industrialization and digital transformation efforts create new demand centers. For stakeholders, the message is clear: the thin film capacitor market offers substantial long-term growth opportunities, but success will depend on strategic investments in R&D, manufacturing capabilities, and market diversification, coupled with an agile response to evolving technological landscapes and sustainability imperatives.

- Robust growth driven by advanced electronics and emerging technologies.

- Critical role in electric vehicles, 5G, IoT, and renewable energy.

- Continued innovation in materials and manufacturing processes is essential.

- Miniaturization and high-performance requirements are primary market forces.

- Significant investment opportunities across various end-use industries.

Thin Film Capacitor Market Drivers Analysis

The thin film capacitor market is propelled by a confluence of technological advancements and increasing demands from high-growth industries. A primary driver is the pervasive trend of miniaturization in electronic devices, which necessitates components that offer high capacitance density within incredibly small form factors. Thin film capacitors, with their inherent ability to be fabricated into compact, high-performance layers, are ideally suited to meet these evolving design requirements, enabling sleeker, more powerful portable electronics, medical devices, and integrated circuits. This miniaturization extends beyond consumer electronics to industrial and automotive applications, where space and weight savings are critical.

Another significant driver is the rapid expansion of the electric vehicle (EV) and hybrid electric vehicle (HEV) sectors. These vehicles require highly efficient and reliable power electronics for battery management systems, inverters, and onboard chargers. Thin film capacitors offer superior performance in high-temperature and high-frequency environments, making them indispensable for ensuring the efficiency, safety, and longevity of EV power trains. As global commitments to decarbonization intensify and EV adoption rates accelerate, the demand for these specialized capacitors in the automotive industry is set to soar, presenting a lucrative growth avenue.

Furthermore, the global rollout of 5G networks and the proliferation of Internet of Things (IoT) devices are substantially boosting the demand for thin film capacitors. Both 5G infrastructure and IoT endpoints rely on high-frequency communication and require passive components with excellent high-frequency response, low loss, and stable performance. Thin film capacitors excel in these areas, ensuring signal integrity and power delivery efficiency in advanced communication modules, sensors, and data processing units. The continuous expansion of these digital ecosystems acts as a strong, sustained driver for market growth, reinforcing the critical role of these components.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Miniaturization of Electronic Devices | +2.1% | Global, particularly APAC (China, Korea, Japan), North America, Europe | 2025-2033 |

| Growth in Electric Vehicles & Automotive Electronics | +1.8% | Europe, North America, APAC (China, Japan) | 2025-2033 |

| Expansion of 5G & IoT Infrastructure | +1.5% | Global, particularly North America, APAC (China, India), Europe | 2025-2033 |

| Increasing Demand from Renewable Energy Systems | +1.2% | Europe, North America, APAC (China, India) | 2026-2033 |

| Advancements in Medical Devices & Implants | +0.8% | North America, Europe | 2025-2033 |

Thin Film Capacitor Market Restraints Analysis

Despite the robust growth prospects, the thin film capacitor market faces several notable restraints that could temper its expansion. One significant challenge is the relatively high manufacturing cost associated with thin film deposition techniques compared to traditional capacitor fabrication methods. The need for specialized equipment, cleanroom environments, and precise control over material deposition processes makes the production of thin film capacitors inherently more expensive. This cost factor can limit their adoption in price-sensitive applications or in markets where cost-effectiveness is prioritized over superior performance, thus constraining broader market penetration.

Another key restraint is the complexity of the fabrication process. Producing high-quality thin film capacitors requires intricate multi-layer deposition, precise patterning, and sophisticated material handling, which demand a high level of technical expertise and strict quality control. Any deviations in the manufacturing process can lead to defects, lower yields, and increased production costs. This complexity can also act as a barrier to entry for new manufacturers, concentrating market power among a few technologically advanced players and potentially slowing down overall innovation by limiting competitive pressures.

Furthermore, the market's reliance on specific, sometimes scarce, raw materials can pose a restraint. While thin film capacitors generally use common materials like silicon dioxide, aluminum oxide, or various polymers, the purity and specific forms required for thin film deposition can lead to supply chain vulnerabilities. Geopolitical factors, trade restrictions, or sudden spikes in demand for these materials can disrupt production and increase costs, impacting market stability and growth. The ongoing search for alternative, more readily available, and cost-effective materials is a continuous effort to mitigate this restraint, but it remains a persistent challenge for the industry.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Manufacturing Costs | -1.5% | Global | 2025-2033 |

| Complex Fabrication Processes & Yield Challenges | -1.2% | Global | 2025-2033 |

| Competition from Alternative Capacitor Technologies | -0.9% | Global | 2025-2030 |

| Supply Chain Vulnerabilities for Key Materials | -0.7% | Global, particularly APAC | 2025-2033 |

Thin Film Capacitor Market Opportunities Analysis

The thin film capacitor market is poised to capitalize on several significant opportunities driven by emerging technologies and evolving industry needs. One key opportunity lies in the burgeoning field of advanced power electronics, particularly for high-power density applications in industrial machinery, grid infrastructure, and specialized military equipment. As these systems demand higher efficiency, reduced form factors, and improved thermal management, thin film capacitors with their superior power handling capabilities and stability at elevated temperatures become increasingly attractive, opening new avenues for market expansion beyond traditional consumer electronics.

Another substantial opportunity resides in the integration of thin film capacitors into advanced packaging solutions and System-in-Package (SiP) architectures. As electronic devices become more compact and functionally dense, the ability to embed passive components directly within integrated circuits or package substrates offers significant performance benefits, including reduced parasitic inductance and improved signal integrity. This trend towards heterogeneous integration presents a lucrative niche for thin film capacitor manufacturers capable of developing ultra-thin, highly reliable components compatible with advanced packaging techniques, fostering closer collaboration with semiconductor companies.

Furthermore, the increasing global focus on renewable energy sources, such as solar and wind power, creates immense opportunities for thin film capacitors. These energy systems require robust and efficient power conversion electronics, including inverters and converters, which operate under demanding conditions. Thin film capacitors are critical for filtering, energy storage, and power factor correction in these applications, contributing to the overall efficiency and stability of renewable energy grids. As countries worldwide invest heavily in green energy infrastructure, the demand for specialized, high-performance thin film capacitors is expected to rise significantly, offering a long-term growth trajectory for the market.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Integration into Advanced Packaging (SiP, SoP) | +1.7% | Global, particularly APAC, North America | 2026-2033 |

| Growing Adoption in High-Power Industrial Electronics | +1.4% | North America, Europe, APAC | 2025-2033 |

| Expansion in Medical & Biomedical Devices | +1.1% | North America, Europe | 2025-2033 |

| Emergence of Flexible & Wearable Electronics | +0.9% | Global | 2027-2033 |

Thin Film Capacitor Market Challenges Impact Analysis

The thin film capacitor market faces several significant challenges that necessitate strategic responses from manufacturers. One primary challenge is the continuous pressure to enhance performance parameters, such as capacitance density, breakdown voltage, and equivalent series resistance (ESR), while simultaneously reducing physical size. Meeting these evolving and often conflicting demands requires substantial investment in research and development, particularly in novel materials and advanced deposition techniques. The technical complexity involved in pushing these limits can slow down product development cycles and increase R&D costs, posing a barrier to rapid innovation.

Another critical challenge is intense market competition, not only among thin film capacitor manufacturers but also from alternative capacitor technologies. Ceramic capacitors, electrolytic capacitors, and even supercapacitors continually evolve, offering compelling alternatives for various applications. Thin film capacitor manufacturers must consistently differentiate their products through superior performance in specific niches, cost-effectiveness for high-volume applications, or unique integration capabilities. This competitive landscape puts pressure on pricing and profit margins, demanding operational efficiency and strategic market positioning to maintain viability and growth.

Furthermore, navigating complex and evolving regulatory landscapes, especially concerning environmental standards and material restrictions, presents an ongoing challenge. Compliance with directives such as RoHS (Restriction of Hazardous Substances) and REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) requires manufacturers to meticulously track their supply chains and ensure all materials meet stringent environmental and safety criteria. Adherence to these regulations adds layers of complexity to manufacturing processes and can necessitate costly reformulations or sourcing changes, impacting global supply chains and product availability. Staying ahead of these regulatory changes is crucial for uninterrupted market access and consumer trust.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Achieving Higher Performance in Smaller Footprints | -1.0% | Global | 2025-2033 |

| Intense Competition & Price Pressure | -0.8% | Global | 2025-2033 |

| Complexities of Multi-Layer Fabrication | -0.7% | Global | 2025-2030 |

| Compliance with Environmental Regulations | -0.5% | Europe, North America, APAC | 2025-2033 |

Thin Film Capacitor Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Thin Film Capacitor Market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. The scope encompasses a thorough examination of market size and growth forecasts, key drivers, restraints, opportunities, and challenges influencing the industry. It also includes a robust analysis of AI's impact on manufacturing and design processes, alongside a competitive profiling of major market players. The report aims to equip stakeholders with actionable intelligence for strategic decision-making and market penetration.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.25 Billion |

| Market Forecast in 2033 | USD 2.45 Billion |

| Growth Rate | 8.5% |

| Number of Pages | 250 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | TDK Corporation, Murata Manufacturing Co. Ltd., KEMET Corporation (now part of Yageo Corporation), Vishay Intertechnology, Inc., Panasonic Corporation, Cornell Dubilier Electronics, Inc., Nichicon Corporation, Hitachi AIC Inc., EPCOS AG (now part of TDK Corporation), Samsung Electro-Mechanics, AVX Corporation (now part of Kyocera Corporation), Walsin Technology Corporation, Capacitor Sciences, Inc., Illinois Capacitor, Inc., Rubycon Corporation, NTE Electronics, Inc., United Chemi-Con, Inc., Sumida Corporation, Custom Electronics Inc., CDE Cornell Dubilier. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Thin Film Capacitor market is extensively segmented to provide a granular view of its diverse applications and underlying technologies. This comprehensive segmentation allows for a precise understanding of market dynamics across different product types, end-use industries, and material compositions. Each segment exhibits unique growth drivers and market potential, influenced by specific technological requirements and regional demand patterns. Analyzing these segments individually offers insights into niche opportunities and areas of intense competition within the broader market landscape, enabling targeted strategic planning for market participants.

- By Type

- Metalized Film Capacitors

- Polypropylene Film Capacitors

- Polyester Film Capacitors

- Polyethylene Naphthalate (PEN) Film Capacitors

- Polysulfone Film Capacitors

- Others (Polycarbonate, Polystyrene)

- By Application

- Automotive Electronics

- Consumer Electronics

- Industrial Electronics

- Power & Energy Systems

- Medical Devices

- Telecommunications

- Aerospace & Defense

- Others (Lighting, Home Appliances)

- By End-Use Industry

- Automotive

- Consumer Electronics

- Industrial

- Power Generation & Distribution

- Healthcare

- Telecommunications & IT

- Aerospace & Defense

- By Material

- Polypropylene (PP)

- Polyester (PET)

- Polycarbonate (PC)

- Polysulfone (PSU)

- Polyethylene Naphthalate (PEN)

- Ceramic

- Others

- By Voltage Type

- Low Voltage

- Medium Voltage

- High Voltage

Regional Highlights

- Asia Pacific (APAC): The Asia Pacific region is anticipated to dominate the thin film capacitor market, driven by the strong presence of consumer electronics manufacturing hubs, rapid industrialization, and significant investments in electric vehicle production in countries like China, Japan, South Korea, and India. The region also leads in 5G infrastructure deployment and renewable energy projects, fueling the demand for high-performance capacitors. Government initiatives supporting local manufacturing and technological innovation further bolster market growth.

- North America: North America represents a mature yet dynamically growing market for thin film capacitors, characterized by substantial R&D investments in advanced aerospace and defense technologies, medical devices, and high-end automotive electronics. The region's focus on technological innovation, early adoption of emerging technologies like AI and IoT, and a robust telecommunications infrastructure contribute significantly to market expansion. The presence of key market players and a strong demand for reliable, high-performance components sustain its market share.

- Europe: Europe is a key region in the thin film capacitor market, largely due to its advanced automotive industry, particularly in electric and hybrid vehicles, and its strong commitment to renewable energy initiatives. Countries like Germany, France, and the UK are at the forefront of adopting sustainable energy solutions and smart grid technologies, which heavily rely on efficient power electronics. Additionally, the region's robust industrial automation sector and stringent quality standards drive the demand for high-reliability thin film capacitors.

- Latin America: The Latin American market for thin film capacitors is experiencing steady growth, primarily influenced by increasing investments in infrastructure development, expanding consumer electronics markets, and the gradual adoption of electric vehicles. While smaller compared to other regions, industrialization efforts and a growing middle class are creating new opportunities, particularly in Brazil and Mexico, for various electronic components, including thin film capacitors.

- Middle East & Africa (MEA): The MEA region is an emerging market for thin film capacitors, with growth primarily stemming from investments in telecommunications infrastructure, energy projects, and selective industrial advancements. The expansion of smart city initiatives and renewable energy deployments in certain Gulf Cooperation Council (GCC) countries is creating a nascent demand for high-performance capacitors. However, the market's overall growth is contingent on further industrial diversification and technological adoption across the region.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Thin Film Capacitor Market.- TDK Corporation

- Murata Manufacturing Co. Ltd.

- KEMET Corporation (now part of Yageo Corporation)

- Vishay Intertechnology, Inc.

- Panasonic Corporation

- Cornell Dubilier Electronics, Inc.

- Nichicon Corporation

- Hitachi AIC Inc.

- EPCOS AG (now part of TDK Corporation)

- Samsung Electro-Mechanics

- AVX Corporation (now part of Kyocera Corporation)

- Walsin Technology Corporation

- Capacitor Sciences, Inc.

- Illinois Capacitor, Inc.

- Rubycon Corporation

- NTE Electronics, Inc.

- United Chemi-Con, Inc.

- Sumida Corporation

- Custom Electronics Inc.

- CDE Cornell Dubilier

Frequently Asked Questions

Analyze common user questions about the Thin Film Capacitor market and generate a concise list of summarized FAQs reflecting key topics and concerns.What is a thin film capacitor?

A thin film capacitor is an electronic component that stores electrical energy, fabricated by depositing very thin layers of dielectric and conductive materials onto a substrate. Its compact size, high performance, and reliability make it ideal for miniaturized and high-frequency electronic circuits.

What are the primary applications of thin film capacitors?

Thin film capacitors are primarily used in applications requiring high reliability, stability, and compactness, including automotive electronics (EVs, ADAS), consumer devices (smartphones, wearables), medical implants, industrial power electronics, and high-frequency telecommunication systems like 5G infrastructure.

How does the thin film capacitor market differ from other capacitor markets?

The thin film capacitor market stands out due to its emphasis on ultra-small form factors, superior high-frequency performance, excellent temperature stability, and high precision. Unlike bulkier ceramic or electrolytic capacitors, thin film types are optimized for integration into compact, advanced electronic assemblies and high-power applications.

What factors are driving the growth of the thin film capacitor market?

Key growth drivers include the increasing demand for miniaturized electronic devices, the rapid expansion of electric vehicles, the global rollout of 5G networks and IoT devices, and growing adoption in renewable energy systems, all of which require high-performance, compact, and reliable energy storage solutions.

What challenges does the thin film capacitor market face?

Major challenges include the high manufacturing costs associated with precise deposition techniques, the technical complexities of achieving higher performance in smaller footprints, intense competition from alternative capacitor technologies, and the need to comply with evolving environmental regulations regarding materials and processes.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted