Thick Film Substrate Market

Thick Film Substrate Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_707968 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

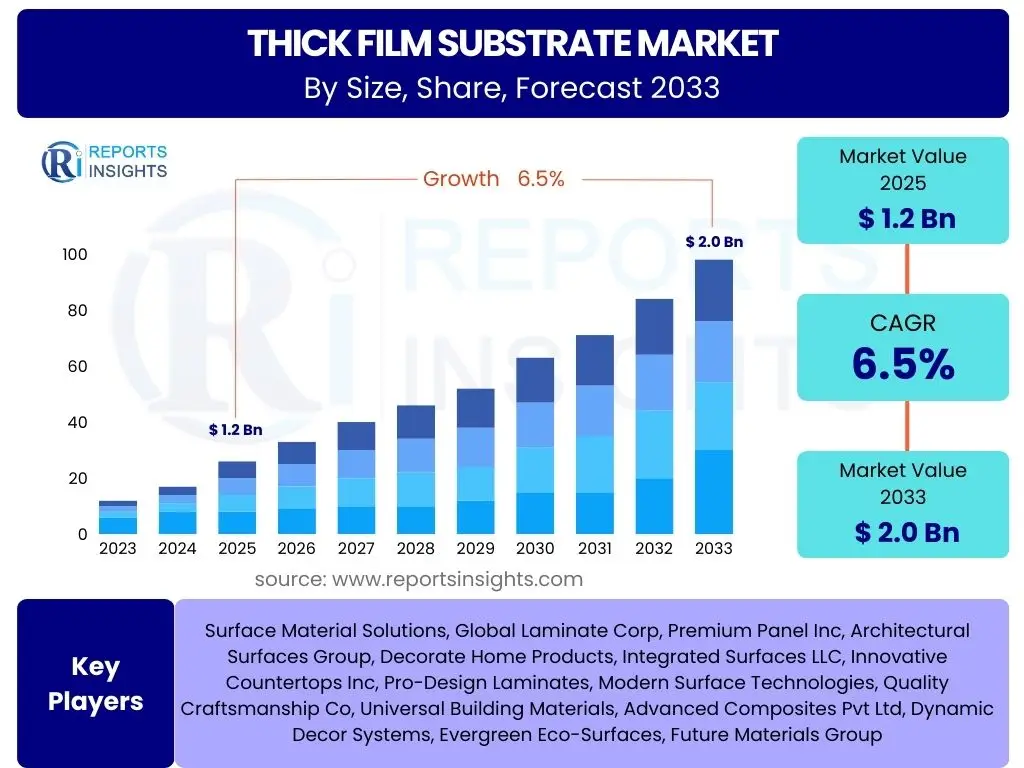

Thick Film Substrate Market Size

According to Reports Insights Consulting Pvt Ltd, The Thick Film Substrate Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.5% between 2025 and 2033. The market is estimated at USD 1.2 Billion in 2025 and is projected to reach USD 2.0 Billion by the end of the forecast period in 2033.

Key Thick Film Substrate Market Trends & Insights

The Thick Film Substrate market is currently experiencing significant evolution driven by several technological advancements and shifts in end-user demands. A prominent trend involves the increasing need for miniaturization in electronic components, particularly in sectors such as consumer electronics, automotive, and medical devices. This miniaturization requires substrates that can support higher circuit densities and offer superior performance in compact form factors, pushing manufacturers towards advanced ceramic materials and refined printing techniques.

Another critical trend is the escalating demand for enhanced thermal management capabilities. As electronic devices become more powerful and operate at higher frequencies, heat dissipation becomes a major challenge. Thick film substrates with high thermal conductivity, such as aluminum nitride, are gaining traction to effectively manage heat, improve device reliability, and extend operational lifespans. This is particularly crucial in power electronics, LED lighting, and automotive applications where extreme temperatures are common.

Furthermore, the integration of thick film technology into emerging applications like IoT (Internet of Things) devices, 5G infrastructure, and electric vehicles (EVs) is shaping market dynamics. The robustness, reliability, and cost-effectiveness of thick film substrates make them ideal for these demanding environments. There is also a growing focus on environmentally friendly manufacturing processes and materials, influencing material selection and production methodologies across the industry.

- Miniaturization and high circuit density integration

- Enhanced thermal management requirements for high-power applications

- Increasing adoption in automotive electronics and electric vehicles (EVs)

- Growth in IoT, wearable devices, and medical applications

- Development of advanced materials for high-frequency and 5G communication

AI Impact Analysis on Thick Film Substrate

Artificial Intelligence (AI) is poised to exert a transformative impact on the Thick Film Substrate market, primarily by optimizing design processes, enhancing manufacturing efficiency, and enabling the development of next-generation applications. Users frequently inquire about how AI can streamline the complex design of thick film circuits, which often involves intricate patterns and material considerations. AI-driven simulation tools and generative design algorithms can significantly reduce development cycles, allowing engineers to explore a vast array of design parameters and predict performance outcomes with greater accuracy, leading to more robust and efficient substrates.

In manufacturing, AI and machine learning algorithms are revolutionizing quality control and process automation. There is considerable interest in how AI can monitor production lines in real-time, identify anomalies, and predict potential equipment failures, thereby reducing waste and improving yield rates. Predictive maintenance, powered by AI, can anticipate issues with printing equipment or firing furnaces, ensuring consistent quality and minimizing downtime. This operational efficiency is crucial for meeting the stringent quality requirements of high-reliability applications, such as those in the automotive or aerospace industries.

Beyond manufacturing, AI is also influencing the demand for thick film substrates themselves. The proliferation of AI-enabled devices, from smart sensors to advanced robotics, necessitates reliable and high-performance electronic components. Thick film substrates are well-suited for these applications due to their robustness and ability to integrate various functionalities. Users are keen to understand how these substrates will evolve to support the unique power and thermal management needs of compact AI processing units, driving innovation in material science and packaging technologies within the thick film industry.

- Optimization of substrate design and material selection through AI-driven simulation

- Enhanced manufacturing process control and quality assurance via machine learning

- Predictive maintenance for production equipment, reducing downtime and waste

- Facilitation of complex circuit integration and performance prediction

- Creation of specialized substrates for AI-enabled and high-performance computing devices

Key Takeaways Thick Film Substrate Market Size & Forecast

The Thick Film Substrate market is poised for steady and robust growth, underpinned by its integral role in modern electronic systems across diverse industries. A key takeaway from the market size and forecast analysis is the consistent demand for reliable and high-performance substrates that can withstand harsh operating conditions. The market's resilience is notable, as it continues to adapt to evolving technological landscapes and increasingly stringent performance requirements, particularly in sectors demanding enhanced power handling and thermal dissipation capabilities.

Another significant insight reveals that while traditional applications continue to provide a stable foundation, the primary accelerators for market expansion are emerging and high-growth sectors. The automotive industry, driven by the electrification of vehicles and the proliferation of advanced driver-assistance systems (ADAS), represents a substantial growth engine. Similarly, the ongoing expansion of the Internet of Things (IoT) and the need for robust connectivity solutions are creating new opportunities for thick film technology in compact, reliable sensor and communication modules.

Furthermore, the forecast underscores the importance of continuous innovation in materials science and manufacturing processes. To maintain competitive advantage and capture future market share, companies must invest in developing next-generation materials with improved thermal, electrical, and mechanical properties. Customization and the ability to offer tailored solutions for specific high-performance applications will be crucial differentiators, allowing market participants to capitalize on niche but high-value segments.

- The market is projected for consistent growth, reaching USD 2.0 Billion by 2033.

- Automotive, medical, and IoT sectors are major growth catalysts.

- Thermal management and miniaturization remain critical design priorities.

- Innovation in advanced materials and customization are essential for market competitiveness.

- Robustness and reliability are key attributes driving adoption in demanding applications.

Thick Film Substrate Market Drivers Analysis

The Thick Film Substrate market is primarily driven by the escalating demand for miniaturized and high-performance electronic components across various industries. The continuous push for smaller, lighter, and more powerful devices necessitates substrates that can accommodate increased circuit density while maintaining reliability. This trend is particularly evident in consumer electronics, where space is at a premium, and in medical devices, which require compact and dependable solutions for implantable or portable applications. The ability of thick film technology to create complex circuits on a small footprint makes it an ideal choice for meeting these evolving requirements.

Another significant driver is the rapid expansion of the automotive electronics sector, especially with the global shift towards electric vehicles (EVs) and autonomous driving systems. These advanced automotive applications demand components that are highly durable, resistant to extreme temperatures, and capable of managing high power loads. Thick film substrates, with their excellent thermal conductivity and mechanical robustness, are increasingly integrated into power modules, sensors, and control units within modern vehicles, ensuring reliable operation under harsh conditions. The growing complexity of automotive systems directly translates into higher demand for sophisticated substrate solutions.

Furthermore, the growth of the Internet of Things (IoT) and the widespread deployment of 5G infrastructure contribute substantially to market expansion. IoT devices, ranging from smart home sensors to industrial monitoring systems, require cost-effective, durable, and reliable electronic foundations. Thick film substrates provide the necessary platform for these devices, enabling robust connectivity and long-term operation. Similarly, 5G technology demands high-frequency performance and advanced thermal management in its infrastructure components, areas where thick film technology offers distinct advantages over alternative solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Electronics Miniaturization and High-Density Packaging | +1.5% | Global | Short to Mid-term |

| Increasing Demand for Automotive Electronics and EVs | +1.2% | Asia Pacific, Europe | Mid to Long-term |

| Growth in IoT, Wearable Devices, and Smart Sensors | +1.0% | North America, Europe | Mid-term |

| Advancements in Medical Devices and Healthcare Technology | +0.8% | North America, Europe | Long-term |

| Rising Applications in High Power and High-Frequency Electronics | +1.0% | Global | Mid-term |

Thick Film Substrate Market Restraints Analysis

Despite the robust growth prospects, the Thick Film Substrate market faces several notable restraints that could temper its expansion. One primary concern is the relatively higher manufacturing cost associated with advanced thick film substrates, particularly those utilizing exotic materials or complex multi-layer designs. The precision required for screen printing, the cost of specialized pastes and inks, and the energy-intensive firing processes can make these substrates more expensive compared to traditional PCB-based solutions or some thin-film alternatives. This cost factor can be a significant barrier for price-sensitive applications, particularly in high-volume consumer electronics segments.

Another substantial restraint comes from the intense competition posed by alternative technologies. Low Temperature Co-fired Ceramic (LTCC), High Temperature Co-fired Ceramic (HTCC), and various types of Printed Circuit Boards (PCBs), including flexible PCBs and HDI (High-Density Interconnect) PCBs, offer competing solutions for different application niches. While thick film excels in certain areas like power handling and thermal management, other technologies might offer advantages in terms of cost, integration density, or flexibility, thereby limiting the thick film market's reach in specific segments. Continuous innovation in these competing fields necessitates constant R&D investment from thick film manufacturers to maintain relevance.

Furthermore, the complexity of fabrication processes for advanced thick film substrates can act as a restraint. Achieving consistent, high-quality thick film circuits requires precise control over numerous variables, including paste rheology, screen printing parameters, drying, and firing profiles. The learning curve for new manufacturing facilities can be steep, and variations in production can lead to lower yields, impacting profitability. Additionally, sourcing specific raw materials, particularly specialty ceramics and precious metal pastes, can be subject to supply chain volatilities and environmental regulations, adding another layer of complexity and potential cost increases.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Higher Manufacturing Costs for Specialized Substrates | -1.0% | Global | Mid-term |

| Intense Competition from Alternative Packaging Technologies | -0.8% | Asia Pacific, North America | Short to Mid-term |

| Complexity of Fabrication and Process Control | -0.7% | Global | Mid-term |

| Supply Chain Vulnerabilities and Material Sourcing Challenges | -0.5% | Global | Short to Mid-term |

| Environmental Regulations and Disposal Concerns | -0.4% | Europe | Long-term |

Thick Film Substrate Market Opportunities Analysis

The Thick Film Substrate market is presented with numerous opportunities for growth, primarily driven by the ongoing advancements in material science and expansion into novel application areas. The development of new ceramic materials with enhanced thermal conductivity, improved dielectric properties, and lower sintering temperatures offers significant potential. These innovations can lead to substrates that are more efficient, cost-effective to produce, and capable of meeting even more demanding performance specifications, opening doors to new high-value applications that were previously inaccessible to thick film technology. Investing in R&D for next-generation material compositions is a key strategic imperative for market players.

Another significant opportunity lies in the burgeoning renewable energy sector, particularly in power conversion modules for solar inverters, wind turbine controls, and energy storage systems. These applications require robust, high-power electronic modules that can operate reliably in harsh environmental conditions. Thick film ceramic substrates, known for their excellent thermal management and high-temperature stability, are ideally suited for these demanding power electronics, offering superior performance compared to traditional organic PCBs. As global investment in green energy solutions continues to accelerate, the demand for such reliable power modules will only intensify.

Furthermore, the continuous need for customization and specialty applications presents a lucrative avenue for market participants. Many high-performance industries, such as aerospace and defense, advanced medical diagnostics, and industrial automation, require bespoke substrate solutions tailored to unique operational parameters. Companies capable of offering highly customized designs, including multi-layer substrates with integrated passive components or specific thermal profiles, can capture significant market share in these niche, high-margin segments. Emerging markets in Asia Pacific and Latin America also represent substantial opportunities, as industrialization and technological adoption drive demand for a wide range of electronic components, including thick film substrates.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development of Novel Ceramic Materials and Composites | +1.2% | Global | Long-term |

| Expansion in Renewable Energy and Power Electronics Sector | +1.0% | Europe, Asia Pacific | Mid to Long-term |

| Growing Demand for Customization and Specialty Applications | +0.9% | North America, Europe | Mid-term |

| Emerging Markets and Industrialization in Developing Regions | +0.8% | Asia Pacific, Latin America | Long-term |

| Integration with Advanced Packaging Technologies and System-in-Package (SiP) | +1.0% | Global | Mid-term |

Thick Film Substrate Market Challenges Impact Analysis

The Thick Film Substrate market faces several significant challenges that could impede its growth trajectory and profitability. One prominent challenge is the risk of technological obsolescence. With rapid advancements in materials science and manufacturing techniques for competing technologies like LTCC and advanced PCBs, thick film manufacturers must continuously innovate to remain competitive. The emergence of new packaging paradigms and semiconductor integration methods could potentially displace traditional thick film applications if the technology does not evolve to meet new performance benchmarks in areas like ultra-miniaturization or extremely high-frequency operations. Keeping pace with these rapid technological shifts requires substantial and ongoing investment in research and development.

Another critical challenge involves the inherent complexities and environmental considerations associated with the materials and processes used in thick film manufacturing. Many thick film pastes contain precious metals (e.g., gold, silver, palladium) and other specialized chemicals, leading to high raw material costs and potential environmental concerns regarding waste disposal and recycling. Furthermore, the energy-intensive firing processes contribute to the carbon footprint, prompting increasing scrutiny from regulators and environmentally conscious consumers. Navigating these material and environmental complexities while maintaining cost-effectiveness and performance standards represents a significant hurdle for industry players.

Supply chain disruptions pose a persistent challenge, particularly in a globalized market. The specialized nature of raw materials, including high-purity ceramic powders, specific metal alloys, and functional pastes, means that supply chains can be vulnerable to geopolitical events, trade disputes, and natural disasters. Any disruption in the availability or pricing of these critical components can directly impact production schedules and profitability. Additionally, the need for a highly skilled workforce, from material scientists to process engineers, is becoming increasingly challenging to meet. A shortage of talent capable of handling the intricate processes and continuous innovation required in thick film technology could limit the industry's growth potential, particularly in regions with aging workforces or less developed technical education systems.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Risk of Technological Obsolescence from Competing Technologies | -1.0% | Global | Long-term |

| High Raw Material Costs and Environmental Regulations | -0.8% | Global, Europe | Mid-term |

| Complex Manufacturing Processes and Yield Management | -0.7% | Global | Mid-term |

| Supply Chain Volatility and Geopolitical Risks | -0.6% | Asia Pacific, Global | Short to Mid-term |

| Shortage of Skilled Labor and Technical Expertise | -0.5% | North America, Europe | Long-term |

Thick Film Substrate Market - Updated Report Scope

This comprehensive report provides an in-depth analysis of the global Thick Film Substrate Market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. The scope encompasses a thorough examination of market drivers, restraints, opportunities, and challenges, coupled with an impact analysis to forecast market evolution. Key market metrics such as size, growth rate, and future projections are meticulously assessed to offer a strategic outlook for stakeholders.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.2 Billion |

| Market Forecast in 2033 | USD 2.0 Billion |

| Growth Rate | 6.5% CAGR |

| Number of Pages | 245 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | CeramTec Corporation, Kyocera Corporation, Maruwa Co., Ltd., Denka Company Limited, NGK Spark Plug Co., Ltd., CoorsTek Inc., Dymatix Corporation, Heraeus Electronics, Murata Manufacturing Co., Ltd., TDK Corporation, Fuji Ceramic Corporation, Vishay Intertechnology, Inc., Laird Thermal Systems, EM Microelectronic, Littelfuse, Inc., Semiconductor Components Industries, LLC, Rogers Corporation, Ametek Inc., Mitsubishi Materials Corporation, Stellar Industries |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The Thick Film Substrate market is comprehensively segmented by material type, application, and end-use industry, providing a granular view of its diverse landscape and growth opportunities. This segmentation allows for a detailed understanding of the specific market dynamics within each category, highlighting the prevalent materials and the sectors driving demand for thick film technology. Each segment reflects unique performance requirements, cost considerations, and technological preferences, shaping the competitive strategies of market participants.

The material segment is crucial as it dictates the physical, electrical, and thermal properties of the substrate, directly impacting its suitability for various applications. Alumina (Al2O3) remains a foundational material due to its excellent electrical insulation and mechanical strength, while Aluminum Nitride (AlN) is gaining significant traction for its superior thermal conductivity, especially in power electronics. Beryllium Oxide (BeO) is used in niche, high-performance applications where extreme thermal dissipation is critical, despite its toxicity concerns. Other materials like Silicon Nitride (Si3N4) and Zirconia (ZrO2) offer specialized properties for specific high-stress or biomedical applications.

Application-wise, the market is highly diversified, ranging from traditional Hybrid Integrated Circuits (HICs) and power modules to advanced sensors, LED lighting, and critical automotive electronics. The increasing complexity of modern electronic systems necessitates robust and reliable substrates that can withstand harsh operating environments. The end-use industry segmentation further clarifies the demand landscape, with the automotive sector, consumer electronics, medical devices, and industrial equipment representing significant segments. Each industry has unique demands concerning reliability, cost, and performance, which in turn drives the selection and development of specific thick film substrate solutions.

- By Material:

- Alumina (Al2O3)

- Aluminum Nitride (AlN)

- Beryllium Oxide (BeO)

- Silicon Nitride (Si3N4)

- Zirconia (ZrO2)

- Others (Sapphire, Glass)

- By Application:

- Hybrid Integrated Circuits (HICs)

- Power Modules

- Sensors

- LED Lighting

- Automotive Electronics

- Medical Devices

- Consumer Electronics

- Industrial Equipment

- Telecommunications

- Others

- By End-Use Industry:

- Automotive

- Consumer Electronics

- Medical

- Industrial

- Telecommunications

- Aerospace & Defense

- Energy

- Others

Regional Highlights

- North America: This region is characterized by early adoption of advanced technologies, strong R&D capabilities, and a significant presence in the medical devices and aerospace & defense industries. Demand is driven by high-performance computing, specialized sensors, and advanced automotive applications.

- Europe: Europe maintains a robust market for thick film substrates, primarily fueled by its prominent automotive manufacturing base, industrial automation sector, and strong emphasis on renewable energy. Stringent quality standards and a focus on high-reliability applications also contribute to demand.

- Asia Pacific (APAC): The APAC region stands as the largest and fastest-growing market due to its expansive manufacturing capabilities in consumer electronics, automotive components, and telecommunications. Countries like China, Japan, South Korea, and Taiwan are major production hubs and significant consumers of thick film substrates, driven by rapid industrialization and technological adoption.

- Latin America: This region represents an emerging market with increasing industrialization and growing investments in automotive and consumer electronics manufacturing. While smaller than other regions, it offers considerable growth potential as economic development progresses.

- Middle East and Africa (MEA): The MEA market is developing, with demand primarily stemming from infrastructure development projects, telecommunications expansion, and niche industrial applications. Growth is expected to be gradual, influenced by economic diversification efforts and technological investments.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Thick Film Substrate Market.- CeramTec Corporation

- Kyocera Corporation

- Maruwa Co., Ltd.

- Denka Company Limited

- NGK Spark Plug Co., Ltd.

- CoorsTek Inc.

- Dymatix Corporation

- Heraeus Electronics

- Murata Manufacturing Co., Ltd.

- TDK Corporation

- Fuji Ceramic Corporation

- Vishay Intertechnology, Inc.

- Laird Thermal Systems

- EM Microelectronic

- Littelfuse, Inc.

- Semiconductor Components Industries, LLC

- Rogers Corporation

- Ametek Inc.

- Mitsubishi Materials Corporation

- Stellar Industries

Frequently Asked Questions

Analyze common user questions about the Thick Film Substrate market and generate a concise list of summarized FAQs reflecting key topics and concerns.What are Thick Film Substrates?

Thick film substrates are ceramic-based electronic components featuring conductive, resistive, and dielectric layers applied through screen printing and firing processes. They provide a robust and thermally stable platform for hybrid integrated circuits and power modules, offering superior performance in harsh environments compared to traditional PCBs.

What are the primary applications of Thick Film Substrates?

Primary applications include hybrid integrated circuits (HICs), power modules for electric vehicles, LED lighting, various sensors, medical devices, automotive electronics, and telecommunication infrastructure. They are crucial in areas requiring high reliability, excellent thermal management, and operation in demanding conditions.

What factors drive the growth of the Thick Film Substrate market?

Key growth drivers include the increasing demand for miniaturized electronics, the rapid expansion of automotive electronics (especially EVs), the proliferation of IoT and wearable devices, and the need for advanced thermal management solutions in high-power and high-frequency applications.

Which materials are commonly used in Thick Film Substrates?

Common materials for thick film substrates include Alumina (Al2O3) for its electrical insulation and strength, Aluminum Nitride (AlN) for high thermal conductivity, and Beryllium Oxide (BeO) for extreme thermal performance. Other specialized materials like Silicon Nitride (Si3N4) and Zirconia (ZrO2) are used for specific applications.

What challenges does the Thick Film Substrate market face?

The market faces challenges such as higher manufacturing costs for advanced substrates, intense competition from alternative technologies (like LTCC and advanced PCBs), complexities in fabrication processes, and potential supply chain vulnerabilities for specialized raw materials.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted