Thermosetting Polyimide Market

Thermosetting Polyimide Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_708320 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

Thermosetting Polyimide Market Size

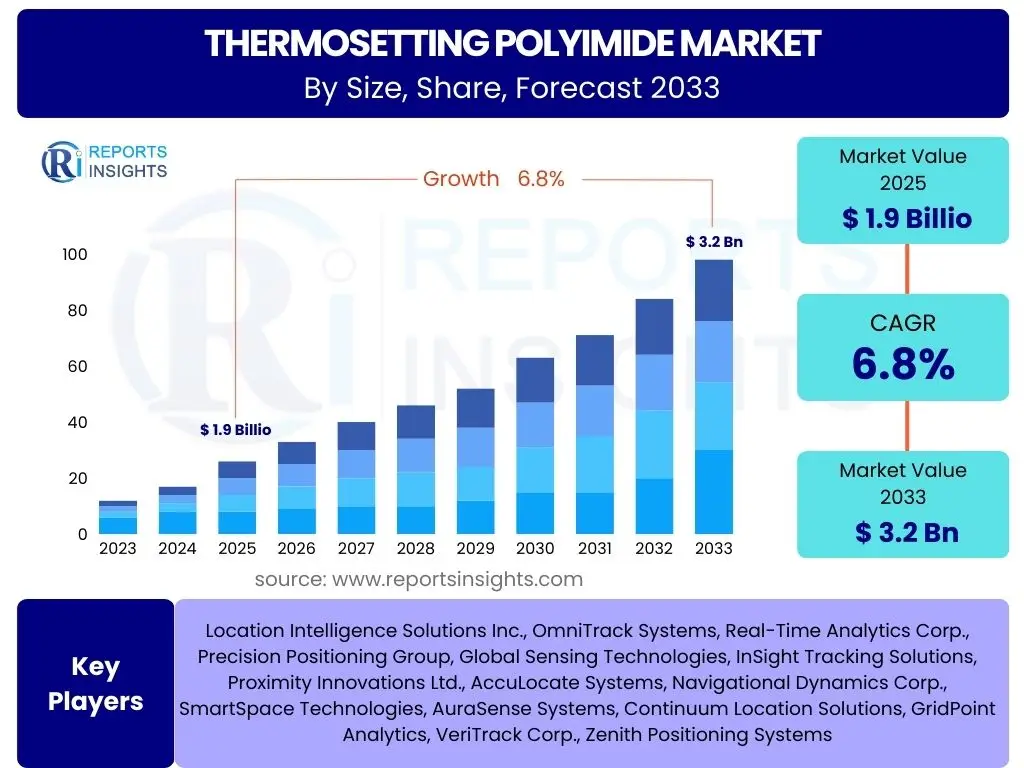

According to Reports Insights Consulting Pvt Ltd, The Thermosetting Polyimide Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033. The market is estimated at USD 1.9 Billion in 2025 and is projected to reach USD 3.2 Billion by the end of the forecast period in 2033.

Key Thermosetting Polyimide Market Trends & Insights

The thermosetting polyimide market is experiencing dynamic shifts driven by advancements in material science and an increasing demand for high-performance polymers across critical industries. A primary trend involves the continuous development of novel polyimide formulations that offer enhanced thermal stability, mechanical strength, and chemical resistance, pushing the boundaries of traditional material capabilities. This innovation is crucial for applications requiring extreme operational conditions, where conventional plastics fail to perform adequately.

Furthermore, the industry is witnessing a significant trend towards the adoption of thermosetting polyimides in lightweighting initiatives, particularly within the aerospace, automotive, and defense sectors. The inherent strength-to-weight ratio of these materials makes them ideal for replacing heavier metallic components, leading to improved fuel efficiency and reduced emissions. This trend is not only environmentally beneficial but also economically advantageous, aligning with global sustainability goals and stringent regulatory frameworks.

Another notable insight points to the growing integration of thermosetting polyimides in advanced manufacturing processes, including additive manufacturing and automated composite fabrication. This integration enables the production of complex geometries with superior precision and reduced waste, opening new avenues for product design and application. The synergy between material innovation and manufacturing technology is poised to accelerate market expansion and diversification.

- Increasing demand from aerospace and defense for high-performance composites.

- Growing adoption in electric vehicles (EVs) and advanced automotive applications for lightweighting and thermal management.

- Technological advancements in manufacturing processes, including additive manufacturing.

- Development of new formulations offering improved processability and cost-effectiveness.

- Rising demand for flexible electronics and miniaturized components.

AI Impact Analysis on Thermosetting Polyimide

Artificial intelligence (AI) is poised to significantly transform the thermosetting polyimide market by enhancing various stages of the product lifecycle, from fundamental research and development to manufacturing and quality control. Users are increasingly curious about how AI can accelerate the discovery of new polyimide chemistries, optimize formulation processes, and predict material properties with greater accuracy. This includes leveraging AI algorithms to screen vast chemical libraries, identify optimal monomer combinations, and simulate molecular structures to achieve desired performance characteristics, thereby dramatically reducing the time and cost associated with traditional experimental methods.

In manufacturing, AI is expected to revolutionize production efficiency and consistency. Stakeholders anticipate AI-powered solutions to monitor and control processing parameters in real-time, such as temperature, pressure, and curing cycles, to minimize defects and ensure uniform product quality. Predictive maintenance facilitated by AI can also optimize equipment uptime, reduce operational costs, and enhance overall plant productivity. The ability of AI to analyze complex sensor data will be critical in achieving higher levels of automation and process optimization within polyimide production facilities.

Beyond R&D and manufacturing, AI’s influence extends to supply chain management and market analysis. Users are interested in how AI can forecast demand more accurately, optimize inventory levels, and identify potential supply chain disruptions proactively, leading to more resilient and efficient operations. Furthermore, AI tools can analyze market trends, competitor strategies, and customer feedback to inform strategic decisions, enabling companies to identify emerging opportunities and tailor their product offerings more effectively to market needs. The integration of AI promises a more agile, data-driven, and innovative thermosetting polyimide industry.

- Accelerated material discovery and optimization through AI-driven simulations and data analysis.

- Enhanced manufacturing process control and efficiency, leading to reduced defects and improved yields.

- Predictive maintenance for production equipment, minimizing downtime and operational costs.

- Optimized supply chain management and demand forecasting for raw materials and finished products.

- Improved quality control and consistency through real-time data monitoring and AI-powered analytics.

Key Takeaways Thermosetting Polyimide Market Size & Forecast

The thermosetting polyimide market is positioned for robust growth over the forecast period, driven by an escalating demand for high-performance materials across multiple industrial sectors. A primary takeaway is the significant expansion projected in core application areas such as aerospace, defense, and electronics, where the unique properties of polyimides—including exceptional thermal stability, mechanical strength, and electrical insulation—are indispensable. This sustained demand underlines the material's critical role in next-generation technologies and challenging operational environments.

Another crucial insight highlights the increasing investment in research and development aimed at improving the processability and cost-effectiveness of thermosetting polyimides. While their superior performance is widely acknowledged, the higher manufacturing costs and complex processing requirements have traditionally limited broader adoption. Innovations leading to more user-friendly formulations and advanced manufacturing techniques are key to unlocking new market segments and accelerating market penetration, particularly in cost-sensitive industries.

Furthermore, the market forecast underscores the pivotal role of regional growth, with the Asia Pacific region expected to emerge as a dominant force due to rapid industrialization, burgeoning electronics manufacturing, and expanding aerospace and automotive industries. North America and Europe will also maintain significant market shares, propelled by ongoing technological advancements and stringent performance requirements. Understanding these regional dynamics is essential for strategic market entry and investment planning.

- Strong growth trajectory driven by high-performance requirements in critical end-use industries.

- Significant market expansion anticipated in aerospace & defense, electronics, and automotive sectors.

- Ongoing innovation in material formulations and processing technologies to enhance cost-efficiency and performance.

- Asia Pacific region identified as a key growth engine due to industrial expansion and manufacturing hubs.

- Continued demand for lightweight and thermally stable solutions as industries seek greater efficiency and durability.

Thermosetting Polyimide Market Drivers Analysis

The thermosetting polyimide market is propelled by a confluence of factors that underscore the material's indispensable role in modern industrial applications. These drivers are rooted in the intrinsic properties of polyimides, coupled with evolving industrial demands for superior performance, efficiency, and sustainability.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Demand from Aerospace & Defense Industries | +1.5% | North America, Europe, Asia Pacific (China, India) | Medium to Long-term (2025-2033) |

| Growing Adoption in Electric Vehicles (EVs) | +1.2% | Asia Pacific (China, South Korea, Japan), Europe, North America | Medium to Long-term (2025-2033) |

| Miniaturization and High Performance in Electronics | +1.0% | Asia Pacific (China, Taiwan, South Korea), North America | Short to Medium-term (2025-2030) |

| Advancements in Composite Manufacturing Technologies | +0.8% | Global, particularly developed regions | Medium to Long-term (2025-2033) |

Increasing Demand from Aerospace & Defense Industries: The aerospace and defense sectors are major consumers of thermosetting polyimides due to their unparalleled performance requirements. These industries require materials that can withstand extreme temperatures, exhibit high mechanical strength, possess excellent resistance to chemicals, and offer superior lightweighting capabilities. Polyimide composites are increasingly replacing heavier metallic components in aircraft structures, engine parts, and missile components, leading to significant fuel efficiency improvements and enhanced operational performance. This trend is further supported by the continuous development of new aircraft programs and the upgrading of existing fleets, particularly in regions like North America and Europe, which are hubs for aerospace manufacturing, and emerging markets in Asia Pacific.

The drive for reduced weight directly translates into lower operating costs and increased payload capacity, making polyimides a material of choice. Furthermore, the rigorous safety and reliability standards in these industries necessitate materials with proven long-term durability and performance under harsh conditions. Thermosetting polyimides meet these stringent criteria, making them indispensable for critical applications where material failure is not an option. Investments in next-generation aircraft and defense systems will continue to fuel this demand, maintaining polyimides as a core component of future innovations.

Growing Adoption in Electric Vehicles (EVs): The burgeoning electric vehicle market presents a substantial growth opportunity for thermosetting polyimides. As EVs become more prevalent, there is an escalating need for materials that can withstand high operating temperatures in battery packs, motor insulation, and power electronics, while also contributing to overall vehicle lightweighting. Thermosetting polyimides offer excellent thermal management properties, electrical insulation, and mechanical integrity, which are crucial for enhancing the safety, efficiency, and longevity of EV components.

The transition to higher voltage systems and faster charging capabilities in EVs further intensifies the demand for advanced insulating materials that can prevent thermal runaway and ensure reliable performance. Polyimide films and coatings are being utilized in battery separators, motor windings, and printed circuit boards, effectively managing heat and providing critical dielectric strength. The global push for electrification in transportation, particularly in leading automotive manufacturing regions such as Asia Pacific (China, South Korea, Japan), Europe, and North America, ensures that the automotive sector will be a significant driver for polyimide market expansion in the coming years.

Miniaturization and High Performance in Electronics: The relentless trend towards miniaturization and increased functionality in the electronics industry is a powerful driver for thermosetting polyimides. As electronic devices become smaller, more powerful, and operate at higher frequencies, the demand for materials with exceptional thermal stability, low dielectric constant, and superior mechanical properties intensifies. Polyimide films, often used in flexible printed circuits (FPCs), chip packaging, and insulating layers, enable the production of compact and high-performance electronic components.

These materials are crucial for next-generation devices, including smartphones, wearables, IoT devices, and advanced computing systems, which require intricate circuitry packed into minimal space. The ability of polyimides to maintain their integrity under high operating temperatures, coupled with their excellent electrical insulation properties, makes them ideal for demanding electronic applications. Major electronics manufacturing hubs in Asia Pacific (China, Taiwan, South Korea) and North America are at the forefront of this technological evolution, driving continuous innovation and adoption of thermosetting polyimides in advanced electronic packaging and interconnects.

Advancements in Composite Manufacturing Technologies: Innovations in composite manufacturing processes are significantly broadening the application scope and enhancing the cost-effectiveness of thermosetting polyimides. Advanced techniques such as automated fiber placement (AFP), automated tape laying (ATL), resin transfer molding (RTM), and additive manufacturing (3D printing) are enabling the production of complex polyimide composite structures with greater precision, reduced waste, and shorter lead times. These manufacturing advancements address some of the traditional challenges associated with processing high-performance thermosets, such as their high viscosity and long cure cycles.

The ability to precisely control fiber orientation and resin impregnation in automated processes leads to superior mechanical properties and consistent part quality, making polyimide composites more attractive for high-volume applications beyond niche markets. Furthermore, the development of additive manufacturing techniques for polyimides opens up new design freedoms, allowing for the creation of intricate, lightweight structures previously impossible to achieve. These technological strides are global in their impact, particularly benefiting developed regions with advanced manufacturing capabilities, and are crucial for unlocking the full potential of thermosetting polyimides in a wider range of industries.

Thermosetting Polyimide Market Restraints Analysis

Despite the strong growth drivers, the thermosetting polyimide market faces several significant restraints that could impede its expansion. These challenges primarily revolve around cost, processability, and competition from alternative materials, which collectively influence market adoption and penetration.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| High Cost of Raw Materials and Manufacturing | -0.9% | Global | Long-term (2025-2033) |

| Complex Processing Requirements | -0.7% | Global, particularly small & medium enterprises | Medium to Long-term (2025-2033) |

| Competition from Alternative High-Performance Polymers | -0.6% | Global | Medium to Long-term (2025-2033) |

High Cost of Raw Materials and Manufacturing: The primary restraint on the thermosetting polyimide market is the inherently high cost associated with its raw materials and complex manufacturing processes. The specialized monomers used in polyimide synthesis are typically more expensive than those for commodity plastics, leading to a higher base material cost. Furthermore, the synthesis and processing of polyimides often require stringent conditions, including high temperatures and pressures, and specialized equipment, contributing to elevated production expenses. This cost factor can be a significant barrier to widespread adoption, especially in applications where performance requirements are high but budget constraints are tight.

The high initial investment for manufacturing facilities capable of producing polyimides also limits the number of players in the market, indirectly affecting competitive pricing. While the performance benefits often justify the cost in critical applications like aerospace and high-end electronics, the relative expense compared to other engineering plastics can deter their use in more cost-sensitive industries. Efforts to develop more economical synthesis routes and improve manufacturing efficiency are ongoing, but the cost remains a fundamental challenge across all regions globally.

Complex Processing Requirements: Thermosetting polyimides are renowned for their outstanding properties, but their processing can be challenging and complex, representing a significant market restraint. Many polyimide resins exhibit high melt viscosity or require specific curing cycles involving elevated temperatures and extended durations. This can lead to difficulties in handling, shaping, and integrating them into composite structures or intricate electronic components. The need for precise control over processing parameters, such as cure temperature profiles, pressure, and vacuum, demands specialized expertise and equipment.

These complexities increase manufacturing lead times and can result in higher scrap rates if not managed meticulously. For smaller and medium-sized enterprises (SMEs), investing in the necessary infrastructure and acquiring the specialized knowledge to process polyimides effectively can be prohibitive. This limits market entry and reduces the overall accessibility of these materials. While advancements in processability are being made through new resin formulations and manufacturing techniques, the inherent processing challenges continue to be a hurdle for broader industrial adoption, impacting the market globally.

Competition from Alternative High-Performance Polymers: The thermosetting polyimide market faces intense competition from a range of alternative high-performance polymers, both thermosetting and thermoplastic. Materials such as PEEK (Polyetheretherketone), PEI (Polyetherimide), PPS (Polyphenylene Sulfide), and advanced epoxies offer similar, albeit sometimes slightly inferior, properties at potentially lower costs or with easier processability. For applications where the absolute highest thermal or mechanical performance is not critical, these alternatives can provide a more economically viable solution.

Thermoplastics, in particular, offer advantages in terms of recyclability, ease of processing (e.g., injection molding), and shorter cycle times, which can be attractive for high-volume manufacturing. While polyimides often surpass these alternatives in extreme performance envelopes, the continuous improvement in properties and processing of competing materials narrows the performance gap, making the decision-making process more complex for end-users. This competitive landscape forces polyimide manufacturers to continually innovate and demonstrate superior value propositions to maintain and expand market share across all regions.

Thermosetting Polyimide Market Opportunities Analysis

The thermosetting polyimide market is replete with opportunities driven by technological advancements, emerging applications, and a growing demand for durable, high-performance materials. These opportunities are strategically positioned to expand the market's reach beyond its traditional strongholds.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Emerging Applications in 5G Technology and Data Centers | +1.1% | Asia Pacific, North America, Europe | Short to Medium-term (2025-2030) |

| Growth in Additive Manufacturing (3D Printing) | +0.9% | Global, particularly developed economies | Medium to Long-term (2025-2033) |

| Development of Lower-Cost, Easier-to-Process Formulations | +0.8% | Global | Medium to Long-term (2025-2033) |

| Demand from Renewable Energy and Energy Storage | +0.7% | Europe, North America, Asia Pacific (China, India) | Medium to Long-term (2025-2033) |

Emerging Applications in 5G Technology and Data Centers: The global rollout of 5G networks and the exponential growth of data centers are creating significant new opportunities for thermosetting polyimides. These technologies demand materials that can handle higher data rates, operate at higher frequencies, and dissipate heat effectively without compromising signal integrity or structural stability. Polyimide films and coatings are ideal for these applications due to their low dielectric constant, low dielectric loss, and excellent thermal management properties, which are critical for high-speed signal transmission and reliable operation of power-intensive equipment.

In 5G infrastructure, polyimides are crucial for antenna substrates, flexible circuit boards in base stations, and high-frequency connectors, where their stability under varying environmental conditions is paramount. Similarly, within data centers, they are utilized in server components, power supply units, and advanced packaging to ensure long-term reliability and performance. Regions leading in digital infrastructure development, such as Asia Pacific, North America, and Europe, are at the forefront of this opportunity, driving the demand for advanced polyimide solutions for next-generation communication and computing technologies.

Growth in Additive Manufacturing (3D Printing): The rapid expansion of additive manufacturing (3D printing) technologies presents a transformative opportunity for thermosetting polyimides. While traditional polyimides are challenging to process with 3D printing due to their high processing temperatures and viscosity, ongoing research is yielding new polyimide-based resins specifically designed for various additive manufacturing techniques, including stereolithography (SLA), fused deposition modeling (FDM), and selective laser sintering (SLS). This enables the creation of complex, high-performance components with intricate geometries that are impossible or too costly to produce with conventional methods.

The ability to 3D print polyimide parts opens new design freedoms for engineers, allowing for customized components with optimized weight, strength, and thermal properties for niche applications in aerospace, medical, and specialized industrial sectors. As 3D printing technology matures and material science advances, the adoption of polyimide-based filaments and resins for additive manufacturing is expected to accelerate globally, particularly in developed economies that are leading the charge in advanced manufacturing research and implementation. This trend will not only expand market volume but also diversify the application landscape for thermosetting polyimides.

Development of Lower-Cost, Easier-to-Process Formulations: A significant opportunity lies in the continuous development of novel thermosetting polyimide formulations that offer improved processability and reduced manufacturing costs. Addressing the traditional barriers of high cost and complex processing will unlock new market segments and accelerate broader adoption across various industries. Researchers are focusing on synthesizing polyimides with lower melt viscosities, shorter cure times, and compatibility with more conventional processing techniques, such as injection molding or vacuum infusion processes.

Innovations in precursor materials, catalyst systems, and polymer architecture are crucial for achieving these goals without sacrificing the exceptional performance characteristics inherent to polyimides. Furthermore, the exploration of bio-based or recycled content in polyimide synthesis could contribute to cost reduction and enhance sustainability credentials, appealing to a wider range of environmentally conscious industries. Successful development and commercialization of such user-friendly and cost-effective formulations will significantly expand the addressable market for thermosetting polyimides globally, allowing them to compete more effectively with other high-performance materials in volume applications.

Demand from Renewable Energy and Energy Storage: The global transition towards renewable energy sources and the increasing focus on advanced energy storage systems represent a burgeoning opportunity for thermosetting polyimides. In renewable energy applications, such as wind turbines and solar panels, polyimides are valued for their durability, resistance to harsh environmental conditions, and lightweight properties. They are used in structural components, electrical insulation, and protective coatings to enhance the efficiency and longevity of these systems. For instance, in wind turbine blades, polyimide composites can offer superior fatigue resistance and lighter weight, contributing to increased energy capture.

In the rapidly evolving field of energy storage, particularly in advanced battery technologies (beyond just EVs), polyimides are crucial for high-performance separators, encapsulants, and thermal management components. Their thermal stability and electrical insulation properties are essential for ensuring the safety and efficiency of battery cells and modules, which operate under demanding conditions. As investments in renewable energy infrastructure and energy storage solutions surge across Europe, North America, and Asia Pacific (especially China and India), the demand for high-performance materials like thermosetting polyimides is expected to grow substantially, contributing to market expansion and diversification.

Thermosetting Polyimide Market Challenges Impact Analysis

While the thermosetting polyimide market presents significant opportunities, it also faces notable challenges that could constrain its growth. These challenges range from regulatory hurdles and sustainability pressures to supply chain complexities and the need for specialized skills.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Environmental and Sustainability Concerns | -0.5% | Europe, North America, parts of Asia Pacific | Long-term (2025-2033) |

| Supply Chain Volatility and Raw Material Availability | -0.4% | Global | Short to Medium-term (2025-2030) |

| Talent Gap and Need for Specialized Expertise | -0.3% | Global | Long-term (2025-2033) |

Environmental and Sustainability Concerns: The thermosetting polyimide market faces increasing scrutiny regarding its environmental impact and sustainability profile, particularly in regions with stringent environmental regulations like Europe and North America. The synthesis of polyimides often involves the use of certain chemicals, some of which may raise environmental concerns during manufacturing or disposal. Furthermore, as thermosets, polyimides are typically not melt-processable once cured, making recycling challenging compared to thermoplastics. This presents a long-term challenge as industries and consumers increasingly prioritize eco-friendly materials and circular economy principles.

Growing pressure from regulatory bodies, NGOs, and end-users for more sustainable material solutions necessitates the development of greener polyimide formulations, including those derived from bio-based feedstocks or with improved recyclability or biodegradability. While the performance benefits of polyimides often outweigh these concerns in critical applications, addressing the sustainability challenge is crucial for broader market acceptance and long-term growth. Companies operating in regions like Europe and certain parts of Asia Pacific are particularly affected by these evolving environmental expectations and regulatory frameworks, pushing for innovation in sustainable polyimide chemistry.

Supply Chain Volatility and Raw Material Availability: The thermosetting polyimide industry is susceptible to supply chain volatility and challenges related to the availability of key raw materials. The specialized monomers and precursors required for polyimide synthesis are often sourced from a limited number of suppliers, making the supply chain vulnerable to disruptions from geopolitical events, natural disasters, trade policies, or unforeseen production issues. Such disruptions can lead to significant price fluctuations, extended lead times, and, in severe cases, material shortages, directly impacting production schedules and profitability for polyimide manufacturers and their customers.

Global economic uncertainties and geopolitical tensions have amplified these vulnerabilities in recent years, demonstrating the need for more resilient and diversified supply chain strategies. Companies are increasingly looking to regionalize supply chains or develop alternative sourcing options to mitigate risks. However, the inherent complexity and specialized nature of these raw materials make such transitions challenging and time-consuming. This challenge is global in its scope, affecting manufacturers and end-users across all major markets and demanding strategic planning for supply chain resilience in the short to medium term.

Talent Gap and Need for Specialized Expertise: The highly specialized nature of thermosetting polyimide chemistry, processing, and application creates a significant talent gap within the industry, posing a long-term challenge to growth and innovation. Developing, manufacturing, and applying polyimides effectively requires deep expertise in polymer science, chemical engineering, materials engineering, and advanced composite fabrication. There is a growing shortage of skilled professionals with the necessary knowledge and experience to drive research, optimize production processes, and provide technical support for complex applications.

This talent deficit can hinder innovation, slow down new product development, and make it difficult for companies to scale operations or enter new markets. Universities and vocational training programs often struggle to keep pace with the rapidly evolving technical demands of advanced materials industries. Addressing this challenge requires sustained investment in education, industry-academia collaboration, and robust training programs to cultivate a new generation of scientists and engineers proficient in polyimide technology. This challenge is global, affecting the advanced materials sector across all regions and potentially impacting the long-term growth trajectory of the thermosetting polyimide market.

Thermosetting Polyimide Market - Updated Report Scope

This report provides an in-depth analysis of the global thermosetting polyimide market, offering comprehensive insights into market dynamics, segmentation, regional trends, and competitive landscape. It covers the period from 2019 to 2033, with a detailed forecast from 2025 to 2033, enabling stakeholders to make informed strategic decisions.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 1.9 Billion |

| Market Forecast in 2033 | USD 3.2 Billion |

| Growth Rate | 6.8% |

| Number of Pages | 265 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | DuPont, Solvay, Ube Industries, Kaneka Corporation, Taimide Technology Inc., Mitsubishi Gas Chemical Company, SABIC, Evonik Industries AG, DIC Corporation, Toray Industries, Saint-Gobain S.A., Changzhou Sunchem, Suzhou ODEC, Lonza, Axon' Cable, Shenzhen Wote Advanced Materials, Miyoshi Oil & Fat Co., Ltd., Hongda Chemical, Asahi Kasei Corporation, Sumitomo Bakelite Co., Ltd. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The thermosetting polyimide market is extensively segmented to provide a granular understanding of its diverse applications and end-use industries. This segmentation highlights the various forms in which polyimides are utilized and the specific types that cater to distinct performance requirements, offering a clear view of market dynamics across different categories.

- By Type: This segment primarily includes Bismaleimide (BMI) and other advanced thermosetting polyimide types. BMI polyimides are known for their excellent thermal stability, mechanical properties, and solvent resistance, making them crucial for high-performance composites and electrical applications. The 'Others' category encompasses various modified polyimides and novel formulations that offer enhanced processability or tailored properties for niche applications, such as thermoplastic-modified thermosets designed to combine the benefits of both polymer classes.

- By Form: Thermosetting polyimides are available in multiple forms to suit diverse manufacturing processes and end-use requirements. Key forms include Resin (used for molding, casting, and impregnating), Prepregs (fiber reinforcements pre-impregnated with resin), Films (thin sheets for insulation and flexible circuits), Coatings (protective layers for various substrates), Adhesives (for high-temperature bonding), and Composites (finished parts combining polyimide matrix with reinforcements). Each form is critical for specific applications, ranging from electronic components to structural aerospace parts.

- By Application: The applications segment delineates the primary uses of thermosetting polyimides across industries. It includes Composites (e.g., in aerospace, automotive), Adhesives & Sealants (high-temperature bonding), Films & Coatings (electrical insulation, protective layers), Electronic Components (flexible PCBs, chip packaging, insulators), and Others (e.g., specialized insulators, friction parts, structural components). The broad range of applications underscores the versatility and indispensable nature of polyimides in demanding environments.

- By End-Use Industry: This segmentation focuses on the key sectors driving demand for thermosetting polyimides. Major end-use industries include Aerospace & Defense (lightweighting, thermal resistance), Electronics & Electrical (insulation, high-frequency circuits), Automotive (EV components, lightweighting), Medical (sterilizable components, implants), Industrial (high-temperature parts, seals), and Others (e.g., energy, telecommunications, machinery). The specific needs and performance criteria of each industry dictate the type and form of polyimide employed.

- By Region: The market is geographically segmented into North America, Europe, Asia Pacific (APAC), Latin America, and Middle East, and Africa (MEA). This regional analysis provides insights into market size, growth trends, and regulatory landscapes unique to each geographic area, reflecting varying levels of industrial development and technological adoption.

Regional Highlights

- North America: North America represents a mature yet robust market for thermosetting polyimides, primarily driven by its strong aerospace and defense industries, coupled with significant investments in advanced electronics and R&D. The demand for high-performance composites in aircraft manufacturing, including both commercial and military platforms, remains a cornerstone of the market. Furthermore, the region's focus on technological innovation in 5G infrastructure, advanced computing, and electric vehicle development continually fuels the need for polyimides in specialized applications requiring exceptional thermal stability and electrical properties.

- Europe: Europe is a key market for thermosetting polyimides, characterized by its advanced automotive sector, thriving aerospace industry, and a strong emphasis on sustainability and energy efficiency. The region's automotive industry, particularly its focus on electric vehicles and lightweighting, is a significant driver for polyimide adoption in battery components, motor insulation, and structural parts. Similarly, European aerospace giants maintain a steady demand for high-performance composites for both commercial aircraft and space applications, where polyimides offer crucial advantages in weight reduction and thermal endurance.

Moreover, Europe's commitment to renewable energy initiatives and advanced manufacturing, including additive manufacturing, creates additional opportunities for polyimides. The region's stringent environmental regulations also foster innovation in greener polyimide chemistries and more sustainable production processes. Countries like Germany, France, and the UK, with their strong industrial bases and research capabilities, are at the forefront of polyimide consumption and development in the European market.

- Asia Pacific (APAC): The Asia Pacific region is projected to be the fastest-growing and largest market for thermosetting polyimides, fueled by rapid industrialization, burgeoning electronics manufacturing, and expanding aerospace and automotive industries, particularly in countries like China, Japan, South Korea, and India. The region's dominance in global electronics production, including flexible displays, semiconductors, and mobile devices, drives immense demand for polyimide films and coatings due to their electrical insulation and thermal stability properties. The rapid adoption of 5G technology across APAC further amplifies this demand.

Furthermore, significant investments in infrastructure development, local aerospace programs, and a booming automotive industry, especially in the EV segment, contribute substantially to market expansion. As manufacturing capabilities continue to advance and disposable incomes rise, leading to increased consumption of electronic goods and vehicles, the demand for high-performance materials like thermosetting polyimides will experience sustained growth. The competitive manufacturing landscape in APAC also encourages innovation in cost-effective polyimide solutions.

The presence of leading material science companies and a strong innovation ecosystem contributes to the development and adoption of new polyimide formulations and processing technologies. Stringent performance and safety regulations in key industries also drive the preference for proven, high-reliability materials like thermosetting polyimides. While growth rates might be lower than emerging economies, the consistent demand from high-value applications ensures North America's continued significance in the global market.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Thermosetting Polyimide Market.- DuPont

- Solvay

- Ube Industries

- Kaneka Corporation

- Taimide Technology Inc.

- Mitsubishi Gas Chemical Company

- SABIC

- Evonik Industries AG

- DIC Corporation

- Toray Industries

- Saint-Gobain S.A.

- Changzhou Sunchem

- Suzhou ODEC

- Lonza

- Axon' Cable

- Shenzhen Wote Advanced Materials

- Miyoshi Oil & Fat Co., Ltd.

- Hongda Chemical

- Asahi Kasei Corporation

- Sumitomo Bakelite Co., Ltd.

Frequently Asked Questions

What are the primary applications of thermosetting polyimides?

Thermosetting polyimides are primarily used in high-performance applications across aerospace and defense (composites, structural parts), electronics (flexible printed circuits, chip packaging, insulation), automotive (EV components, lightweighting), and industrial sectors (high-temperature adhesives, coatings, seals) due to their exceptional thermal, mechanical, and electrical properties.

How is the thermosetting polyimide market expected to grow by 2033?

The thermosetting polyimide market is projected to grow at a Compound Annual Growth Rate (CAGR) of 6.8% between 2025 and 2033, reaching an estimated USD 3.2 Billion by 2033, up from USD 1.9 Billion in 2025, driven by demand for high-performance materials in critical industries.

What key factors are driving the growth of the thermosetting polyimide market?

Key growth drivers include increasing demand from the aerospace and defense industries for lightweight, high-temperature materials, the growing adoption of polyimides in electric vehicles for thermal management and insulation, and the miniaturization trends in the electronics sector requiring high-performance films and coatings.

What are the main challenges faced by the thermosetting polyimide market?

Major challenges include the high cost of raw materials and complex manufacturing processes, significant competition from alternative high-performance polymers, and increasing environmental and sustainability concerns regarding synthesis and recyclability, which can limit broader market adoption.

Which region is expected to dominate the thermosetting polyimide market?

The Asia Pacific (APAC) region is anticipated to dominate the thermosetting polyimide market, driven by its robust electronics manufacturing base, rapid industrialization, burgeoning automotive (especially EV) sector, and growing aerospace investments in countries like China, Japan, and South Korea.