Thermoforming Plastic Packing Market

Thermoforming Plastic Packing Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_709203 | Last Updated : September 15, 2025 |

Format : ![]()

![]()

![]()

![]()

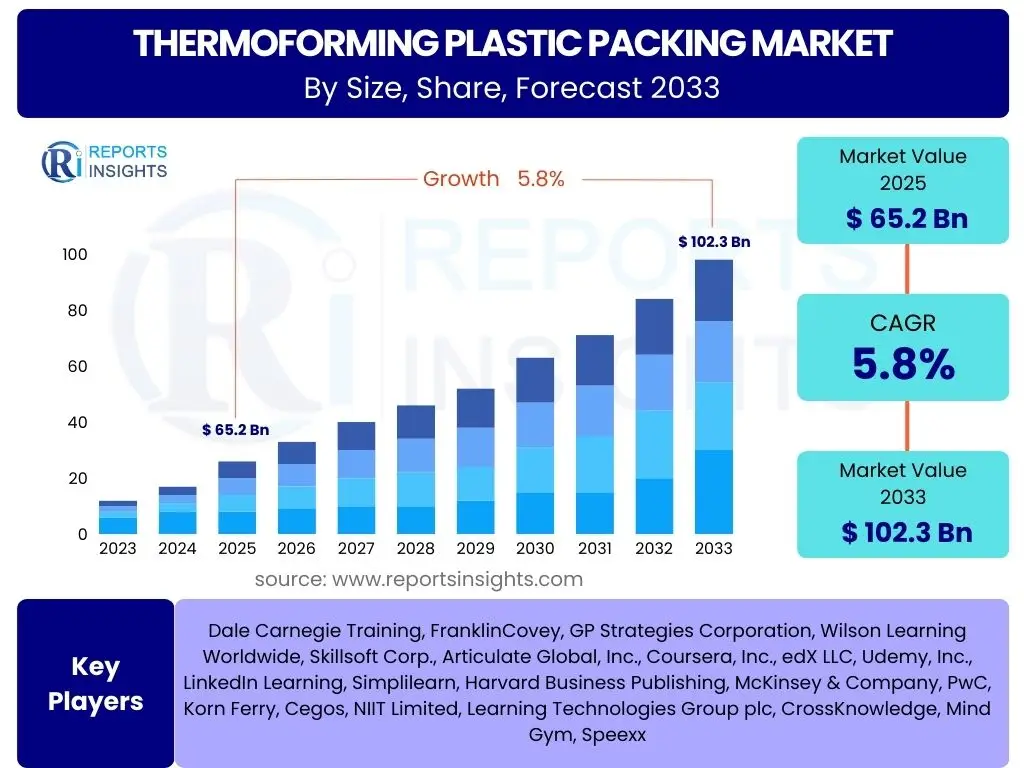

Thermoforming Plastic Packing Market Size

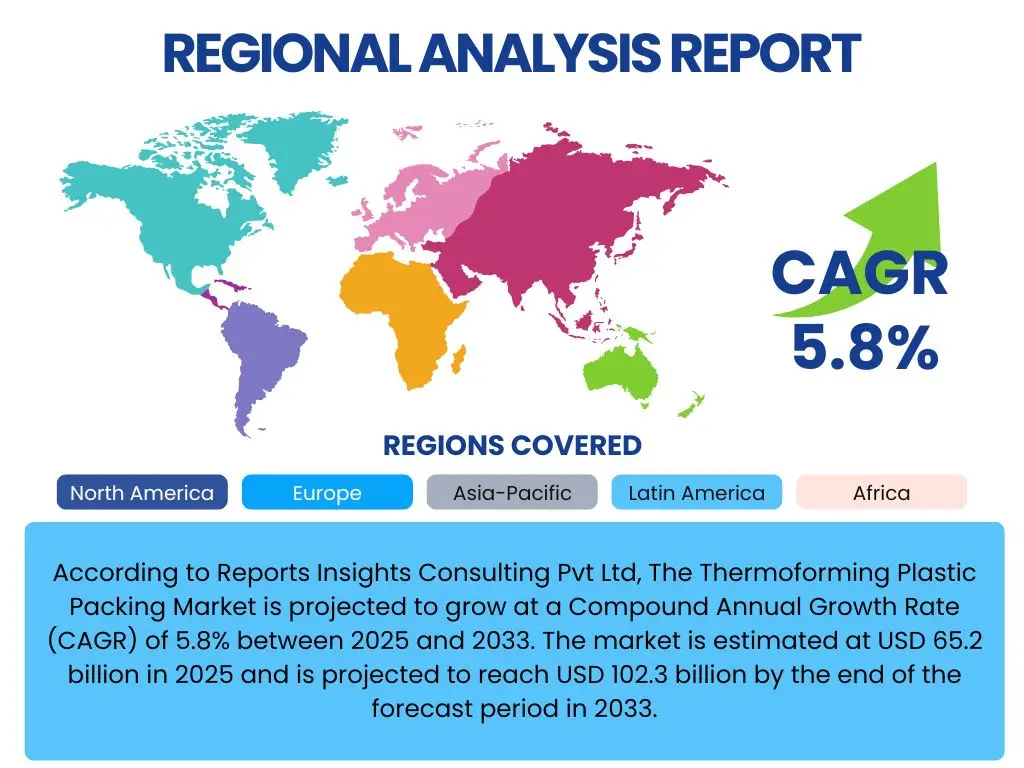

According to Reports Insights Consulting Pvt Ltd, The Thermoforming Plastic Packing Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033. The market is estimated at USD 65.2 billion in 2025 and is projected to reach USD 102.3 billion by the end of the forecast period in 2033.

Key Thermoforming Plastic Packing Market Trends & Insights

User inquiries frequently highlight the shift towards sustainable packaging solutions, the increasing demand for convenience foods, and the technological advancements in thermoforming processes. Consumers and industries are actively seeking packaging options that minimize environmental impact, such as those made from recycled content or biodegradable materials. This trend significantly influences material selection and processing innovations within the thermoforming sector, driving research into bio-based plastics and enhanced recyclability.

Furthermore, the rapid expansion of e-commerce and the growing preference for ready-to-eat and ready-to-cook meal options are bolstering the demand for efficient and protective thermoformed packaging. Packaging design is evolving to meet diverse product requirements, offering extended shelf life, improved visual appeal, and ease of use. Automation and smart manufacturing principles are also gaining traction, enhancing production efficiency, reducing waste, and enabling greater customization capabilities in thermoforming operations.

- Increased adoption of sustainable and recycled content materials (PCR, bio-plastics).

- Growing demand for convenience and on-the-go food packaging.

- Advancements in high-barrier thermoformed packaging for extended shelf life.

- Rise of customized and aesthetically appealing packaging designs.

- Integration of automation and smart manufacturing in production processes.

- Shift towards lightweight packaging to reduce transportation costs and carbon footprint.

AI Impact Analysis on Thermoforming Plastic Packing

Common user questions regarding AI's influence on thermoforming plastic packaging center around its potential to optimize production, enhance quality control, and drive innovation in design. Stakeholders are particularly interested in how AI can streamline complex manufacturing processes, predict equipment maintenance needs, and reduce material waste. The integration of AI algorithms into thermoforming machinery can lead to predictive analytics for operational efficiency, ensuring minimal downtime and maximizing throughput.

Moreover, AI is expected to revolutionize packaging design and material science within the thermoforming sector. AI-powered generative design tools can rapidly explore numerous design iterations, optimizing for material usage, structural integrity, and aesthetic appeal, thereby accelerating product development cycles. In quality control, AI vision systems can detect defects with unprecedented accuracy and speed, far surpassing human capabilities, leading to higher product quality and reduced recall risks. The ability of AI to analyze vast datasets on consumer preferences and market trends also offers opportunities for creating highly targeted and effective packaging solutions.

- Optimization of production parameters and machine performance through predictive analytics.

- Enhanced quality control with AI-powered vision systems for defect detection.

- Accelerated design and prototyping using AI-driven generative design.

- Improved supply chain management and inventory forecasting.

- Reduction in material waste and energy consumption through process optimization.

- Development of smart packaging solutions with integrated sensors and data analysis.

Key Takeaways Thermoforming Plastic Packing Market Size & Forecast

Analysis of common inquiries regarding the thermoforming plastic packaging market size and forecast reveals a strong interest in understanding the underlying growth drivers, particularly those related to evolving consumer lifestyles and regulatory pressures. Users frequently seek insights into how shifts towards convenience foods, personal care products, and pharmaceutical packaging are fueling market expansion. The long-term projections indicate a robust growth trajectory, primarily due to the versatility and cost-effectiveness of thermoformed plastics, which continue to make them a preferred choice across various end-use industries.

Furthermore, the market's future is heavily influenced by advancements in material science, focusing on creating more sustainable and high-performance plastic formulations. While the demand for conventional plastics remains significant, the increasing emphasis on circular economy principles and stringent environmental regulations is pushing manufacturers towards bio-based, recycled, and recyclable alternatives. This dual focus on performance and sustainability will shape investment strategies and product development, ensuring continued innovation and market resilience throughout the forecast period.

- Market growth primarily driven by demand from food & beverage, healthcare, and consumer goods sectors.

- Increasing adoption of sustainable materials (recycled content, bio-based polymers) influencing future market dynamics.

- Technological advancements in thermoforming machinery enhancing production efficiency and product quality.

- E-commerce expansion significantly contributing to demand for protective and lightweight packaging.

- Asia Pacific anticipated to be the fastest-growing region due to industrialization and urbanization.

- Cost-effectiveness and design flexibility remain core competitive advantages of thermoformed packaging.

Thermoforming Plastic Packing Market Drivers Analysis

The global thermoforming plastic packaging market is significantly propelled by the burgeoning demand for packaging solutions in the food and beverage industry. With global populations urbanizing and consumer lifestyles becoming increasingly fast-paced, there is an escalating preference for convenience foods, ready-to-eat meals, and portion-controlled packaging. Thermoformed plastics offer excellent barrier properties, extended shelf life, and aesthetic appeal, making them ideal for a wide range of food products, from fresh produce to dairy and baked goods. This continuous demand from a vital consumer sector forms a fundamental growth catalyst.

Another critical driver is the expanding application of thermoformed packaging in the healthcare and pharmaceutical sectors. The need for sterile, secure, and tamper-evident packaging for medical devices, pharmaceuticals, and personal care products is paramount. Thermoformed blisters, trays, and clamshells provide protection, transparency for product visibility, and cost-efficient solutions that meet stringent regulatory requirements. The aging global population and advancements in medical technologies further amplify this demand, ensuring a steady uptake of thermoforming solutions.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Growing demand from Food & Beverage sector | +1.5% | Global, particularly Asia Pacific & Europe | Short to Mid-Term |

| Increased adoption in Healthcare & Pharmaceutical industries | +1.2% | North America, Europe, China | Mid to Long-Term |

| Rise of e-commerce and need for protective packaging | +0.8% | Global | Short to Mid-Term |

| Technological advancements in thermoforming machinery | +0.5% | Developed regions (North America, Europe) | Mid to Long-Term |

Thermoforming Plastic Packing Market Restraints Analysis

The thermoforming plastic packaging market faces significant headwinds from increasing environmental concerns and stringent regulatory frameworks concerning plastic waste. Public awareness about plastic pollution, particularly single-use plastics, has led to a push for bans and restrictions on certain plastic packaging formats. Governments worldwide are implementing policies that promote recycling, reduce plastic consumption, and encourage the use of alternative materials, thereby increasing pressure on the thermoforming industry to innovate or face market contraction in specific segments. This regulatory environment necessitates substantial investments in research and development for sustainable alternatives.

Another notable restraint is the volatile pricing of raw materials, primarily plastic resins such as PET, PP, PS, and PVC. The cost of these feedstocks is intrinsically linked to crude oil prices and the dynamics of the petrochemical industry, which can fluctuate significantly due to geopolitical events, supply chain disruptions, or changes in production capacity. Such price instability directly impacts manufacturing costs for thermoforming companies, leading to challenges in maintaining profit margins and stable pricing for end-users, ultimately slowing market growth and investment in new capacity.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent environmental regulations & plastic waste concerns | -1.0% | Europe, North America, emerging economies | Short to Long-Term |

| Volatile raw material prices (plastic resins) | -0.7% | Global | Short to Mid-Term |

| Competition from alternative packaging materials (paper, glass, metal) | -0.4% | Global | Mid-Term |

| High initial investment costs for advanced machinery | -0.3% | Developing regions | Short-Term |

Thermoforming Plastic Packing Market Opportunities Analysis

The increasing emphasis on sustainability presents a significant opportunity for the thermoforming plastic packaging market, driving innovation in recycled and bio-based materials. As consumer and regulatory pressures mount, there is a growing demand for packaging solutions that incorporate Post-Consumer Recycled (PCR) content or are derived from renewable resources like PLA and PHA. Companies that invest in developing and manufacturing such sustainable thermoformed products can differentiate themselves, gain market share, and align with global environmental objectives. This shift opens new avenues for material suppliers, converters, and brand owners seeking eco-friendly alternatives without compromising performance.

Moreover, the continuous advancement in thermoforming technology, particularly in automation and high-speed production, offers substantial growth opportunities. Modern thermoforming machines are becoming more efficient, capable of handling a wider range of materials, and producing complex geometries with greater precision and speed. Innovations such as in-mold labeling, enhanced barrier technologies, and multi-layer thermoforming allow manufacturers to offer superior packaging solutions that meet the evolving needs of various industries. This technological evolution not only improves cost-effectiveness but also enables the creation of highly customized and functional packaging tailored for specific product requirements.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Development and adoption of sustainable & recycled materials | +1.3% | Global, particularly Europe & North America | Mid to Long-Term |

| Technological advancements in machinery & processes | +0.9% | Developed & rapidly industrializing regions | Mid-Term |

| Expansion into emerging markets (Asia Pacific, Latin America) | +0.7% | Asia Pacific, Latin America, Middle East | Long-Term |

| Increasing demand for customized and functional packaging | +0.6% | Global | Short to Mid-Term |

Thermoforming Plastic Packing Market Challenges Impact Analysis

One of the primary challenges for the thermoforming plastic packaging market is overcoming the negative public perception and regulatory scrutiny surrounding plastic use. Despite the functional benefits and cost-effectiveness of plastic packaging, widespread concerns about plastic pollution and its environmental impact lead to significant pressure from consumers, NGOs, and governments. This often translates into unfavorable policy decisions, such as bans on certain plastic items or mandates for high recycled content, which can disrupt existing supply chains and necessitate costly retooling or material substitutions for manufacturers.

Another considerable challenge is managing the complex and often capital-intensive transition towards a circular economy for plastic packaging. Achieving true circularity requires not only the development of recyclable materials but also the establishment of robust collection, sorting, and recycling infrastructure, which is currently inadequate in many regions. The high costs associated with designing for recyclability, investing in advanced recycling technologies, and ensuring consistent quality of recycled content pose significant hurdles. Furthermore, scaling up the production of bio-based or compostable plastics to meet market demand while maintaining cost competitiveness and performance parity with traditional plastics remains a complex technical and economic endeavor.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Negative perception & regulatory pressures against plastics | -0.9% | Global, particularly Europe | Short to Long-Term |

| High cost and complexity of establishing circular economy infrastructure | -0.6% | Developed & rapidly developing regions | Mid to Long-Term |

| Availability and quality concerns of recycled plastic content | -0.5% | Global | Short to Mid-Term |

| Intense competition and price sensitivity in mature markets | -0.4% | North America, Europe | Short-Term |

Thermoforming Plastic Packing Market - Updated Report Scope

This comprehensive market insights report meticulously examines the thermoforming plastic packaging sector, providing an in-depth analysis of its current landscape and future growth trajectories. The scope encompasses detailed market sizing, forecasting, trend analysis, and an evaluation of key drivers, restraints, opportunities, and challenges influencing the industry. Special emphasis is placed on material types, end-use applications, and regional market dynamics to offer a holistic view of the market's evolving structure and competitive environment.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 65.2 billion |

| Market Forecast in 2033 | USD 102.3 billion |

| Growth Rate | 5.8% |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | Amcor PLC, Sonoco Products Company, Pactiv Evergreen Inc., WestRock Company, DS Smith Plc, Huhtamäki Oyj, Berry Global Group Inc., Sealed Air Corporation, Winpak Ltd., Tekni-Plex Inc., Genpak LLC, Sabert Corporation, Dart Container Corporation, Silgan Holdings Inc., RPC Group (now Berry Global Group), Placon Corporation, Fabri-Kal Corporation, Greiner Packaging International GmbH, Faerch A/S, CM Packaging B.V. |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The thermoforming plastic packaging market is extensively segmented by material, product type, and application, reflecting the diverse requirements of end-use industries. Material segmentation includes widely used plastics like PET, PP, PS, and PVC, each offering distinct properties such as clarity, rigidity, and barrier performance, making them suitable for specific packaging needs. The emergence of bioplastics like PLA and PHA represents a growing segment driven by sustainability initiatives, although their adoption rate is still influenced by cost and performance considerations compared to conventional plastics.

Product type segmentation covers common thermoformed items such as clamshells, blister packs, trays, cups, and containers, which cater to a broad spectrum of products from retail goods to foodservice. Application-wise, the food and beverage industry remains the largest consumer, leveraging thermoformed packaging for its ability to protect, preserve, and present perishable goods. The healthcare sector is another critical application area, where thermoformed solutions provide sterile and secure packaging for medical devices and pharmaceuticals, emphasizing safety and compliance.

- By Material: Polyethylene Terephthalate (PET), Polypropylene (PP), Polystyrene (PS), Polyvinyl Chloride (PVC), High-Impact Polystyrene (HIPS), Bioplastics (PLA, PHA), Others.

- By Product Type: Clamshells, Blister Packs, Trays, Cups & Containers, Lids & Domes, Others.

- By Application: Food & Beverages (Meat, Poultry, & Seafood; Dairy & Desserts; Bakery & Confectionery; Fruits & Vegetables; Ready-to-Eat Meals; Others), Healthcare & Pharmaceuticals (Medical Devices; Pharmaceuticals; Personal Care Products), Consumer Goods (Electronics; Cosmetics; Toys; Hardware), Industrial Packaging, Others.

Regional Highlights

- North America: A mature market characterized by high consumer awareness regarding sustainability and a robust healthcare industry. Demand is driven by convenience food trends and strict regulations for medical packaging. Significant focus on recycled content and advanced barrier solutions.

- Europe: Leading the charge in sustainable packaging, with stringent environmental policies and a strong push towards circular economy models. High adoption of recycled plastics and bioplastics. Innovation in lightweight and resealable thermoformed designs is prominent.

- Asia Pacific (APAC): The fastest-growing region, fueled by rapid industrialization, urbanization, and increasing disposable incomes. Burgeoning food & beverage and consumer goods sectors contribute significantly to demand. China and India are key growth markets, experiencing a surge in organized retail and e-commerce.

- Latin America: Exhibiting steady growth, primarily driven by expanding food processing industries and increasing demand for packaged consumer goods. Brazil and Mexico are pivotal markets, with a growing focus on cost-effective and practical packaging solutions.

- Middle East & Africa (MEA): Emerging market with increasing investments in manufacturing and logistics infrastructure. Growing demand for packaged food and personal care products, alongside a rising awareness of modern retail formats, are key growth factors.

Top Key Players

The market research report includes a detailed profile of leading stakeholders in the Thermoforming Plastic Packing Market.- Amcor PLC

- Sonoco Products Company

- Pactiv Evergreen Inc.

- WestRock Company

- DS Smith Plc

- Huhtamäki Oyj

- Berry Global Group Inc.

- Sealed Air Corporation

- Winpak Ltd.

- Tekni-Plex Inc.

- Genpak LLC

- Sabert Corporation

- Dart Container Corporation

- Silgan Holdings Inc.

- Placon Corporation

- Fabri-Kal Corporation

- Greiner Packaging International GmbH

- Faerch A/S

- CM Packaging B.V.

- InterFlex Group Inc.

Frequently Asked Questions

What is thermoforming plastic packaging?

Thermoforming plastic packaging involves heating a plastic sheet to a pliable temperature, molding it into a specific shape using a mold, and then trimming the finished product. This process is highly versatile for creating various packaging solutions like trays, clamshells, and blister packs for multiple industries.

Which materials are commonly used in thermoforming plastic packaging?

Common materials include Polyethylene Terephthalate (PET), Polypropylene (PP), Polystyrene (PS), Polyvinyl Chloride (PVC), and High-Impact Polystyrene (HIPS). Increasingly, bioplastics like PLA and PHA, and recycled content (PCR), are also being utilized due to sustainability efforts.

What are the primary applications of thermoforming plastic packaging?

The primary applications are in the food and beverage industry for items such as meat trays, dairy cups, and fresh produce containers, as well as in healthcare for medical device packaging and pharmaceuticals, and for consumer goods like electronics and cosmetics.

How do environmental regulations impact the thermoforming plastic packaging market?

Environmental regulations significantly impact the market by driving demand for sustainable materials, increasing the adoption of recycled content, and fostering innovation in design for recyclability. These regulations also impose restrictions on single-use plastics, encouraging alternatives.

What is the projected growth rate of the thermoforming plastic packaging market?

The thermoforming plastic packaging market is projected to grow at a Compound Annual Growth Rate (CAGR) of 5.8% between 2025 and 2033, driven by sustained demand from end-use industries and ongoing advancements in material science and processing technologies.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted