Thermal Power Plant Market

Thermal Power Plant Market Size, Scope, Growth, Trends and By Segmentation Types, Applications, Regional Analysis and Industry Forecast (2025-2033)

Report ID : RI_700299 | Last Updated : July 23, 2025 |

Format : ![]()

![]()

![]()

![]()

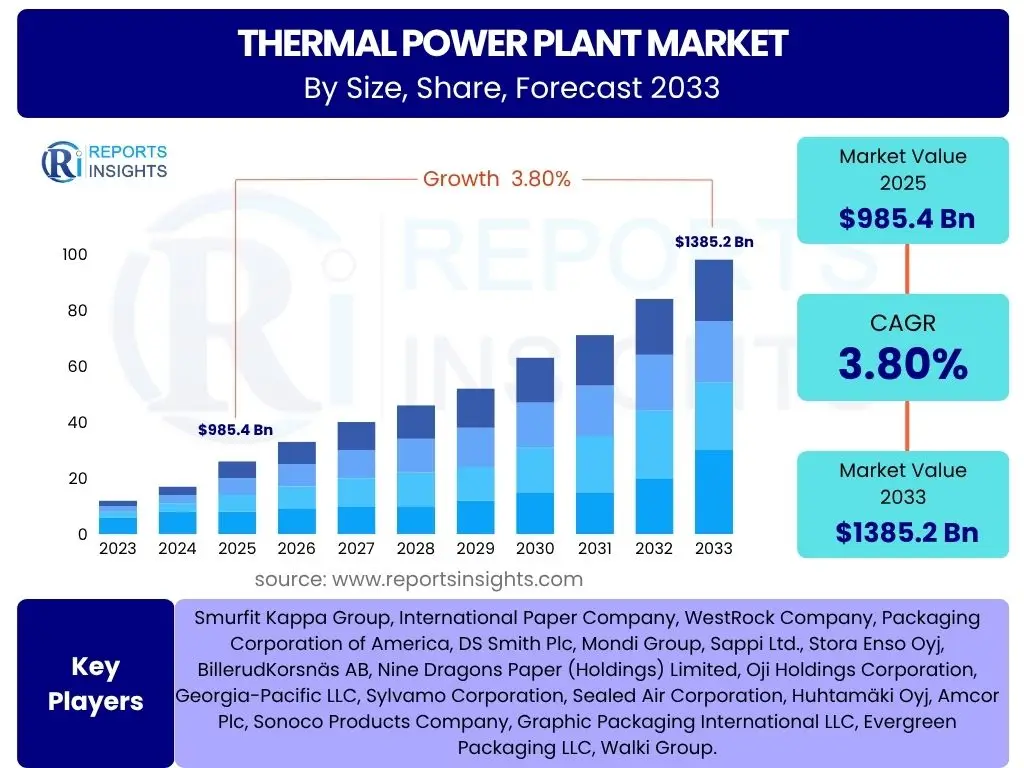

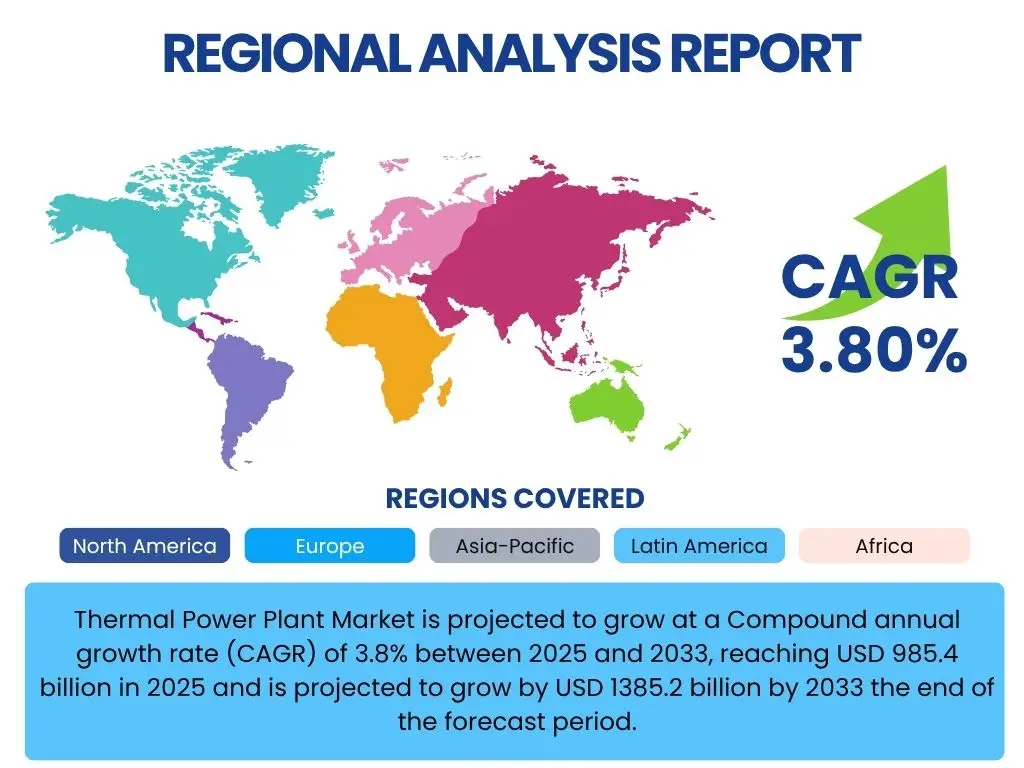

Thermal Power Plant Market is projected to grow at a Compound annual growth rate (CAGR) of 3.8% between 2025 and 2033, reaching USD 985.4 billion in 2025 and is projected to grow by USD 1385.2 billion by 2033 the end of the forecast period.

Key Thermal Power Plant Market Trends & Insights

The global thermal power plant market is currently navigating a complex landscape shaped by evolving energy demands, environmental imperatives, and technological advancements. A significant trend involves the modernization and upgrading of existing thermal power infrastructure to enhance efficiency and reduce emissions, rather than focusing solely on new coal-fired plant constructions. There is a growing emphasis on flexible operation capabilities to support grid stability as renewable energy sources become more prevalent. Furthermore, the development and adoption of carbon capture, utilization, and storage (CCUS) technologies are emerging as crucial strategies to decarbonize thermal power generation, aiming to reconcile energy security with climate goals.

Another prominent trend is the diversification of fuel sources within the thermal power sector, with a gradual shift towards cleaner fossil fuels like natural gas, and an increased interest in biomass and waste-to-energy technologies. Digitalization and automation are also playing a transformative role, enabling predictive maintenance, optimizing plant performance, and improving operational safety. The push for distributed generation and microgrids, while typically associated with renewables, also influences how thermal plants are integrated into smaller, more resilient energy systems. These trends collectively underscore the industry's efforts to adapt to a sustainable energy future while continuing to meet base-load power requirements.

- Increased focus on plant modernization and efficiency upgrades.

- Growing adoption of carbon capture, utilization, and storage (CCUS) technologies.

- Shift towards natural gas and biomass co-firing for reduced emissions.

- Integration of digital solutions for predictive maintenance and operational optimization.

- Enhanced flexibility requirements for thermal plants to support renewable energy intermittency.

- Development of advanced materials for improved turbine performance and longevity.

- Decentralization of power generation with smaller, more localized thermal units.

AI Impact Analysis on Thermal Power Plant

Artificial Intelligence (AI) is rapidly transforming the thermal power plant sector by enhancing operational efficiency, predictive maintenance, and overall plant management. AI algorithms can analyze vast amounts of operational data from sensors and control systems, identifying subtle patterns and anomalies that might indicate impending equipment failure. This capability enables predictive maintenance, shifting from reactive repairs to proactive interventions, thereby minimizing downtime, extending asset lifecycles, and reducing maintenance costs. Furthermore, AI-driven optimization systems can fine-tune combustion processes, boiler efficiency, and steam turbine operations in real-time, leading to significant fuel savings and reduced emissions, contributing directly to a plant's economic and environmental performance.

Beyond operational improvements, AI also plays a crucial role in optimizing energy dispatch and grid integration for thermal power plants. AI-powered forecasting models can predict electricity demand and renewable energy output with higher accuracy, allowing thermal plants to adjust their generation schedules to maintain grid stability and balance supply with demand more effectively. This adaptability is particularly vital in grids with high penetration of intermittent renewable sources. Additionally, AI contributes to enhanced safety by monitoring critical parameters and alerting operators to potential hazards, while also supporting workforce training through simulation and virtual reality environments. The integration of AI tools is thus essential for modern thermal power plants to remain competitive, resilient, and environmentally responsible in a dynamic energy landscape.

- Enhanced predictive maintenance reducing downtime and operational costs.

- Real-time optimization of combustion processes and plant efficiency.

- Improved energy dispatch and grid integration through AI-driven forecasting.

- Automated anomaly detection for early fault identification.

- Optimized fuel consumption and reduced emissions through intelligent control.

- Advanced analytics for performance monitoring and operational insights.

- AI-assisted decision-making for resource allocation and plant management.

Key Takeaways Thermal Power Plant Market Size & Forecast

- Market size projected to reach USD 1385.2 billion by 2033.

- CAGR estimated at 3.8% from 2025 to 2033.

- Significant growth driven by global energy demand and industrialization.

- Modernization and efficiency upgrades are key investment areas.

- Shifting focus towards cleaner fuels and CCUS technologies.

- Asia Pacific remains a dominant region due to expanding infrastructure.

- Market resilience supported by base-load power requirements.

Thermal Power Plant Market Drivers Analysis

The persistent global demand for electricity serves as a fundamental driver for the thermal power plant market. Despite the rapid growth of renewable energy sources, thermal power plants continue to provide critical base-load power and grid stability, especially in developing economies experiencing rapid urbanization and industrialization. Countries like India, China, and various nations in Southeast Asia are still heavily reliant on thermal generation to meet their burgeoning energy needs, necessitating either the expansion of existing capacities or the construction of new, more efficient facilities. This consistent and increasing energy requirement underpins the continued relevance and investment in thermal power infrastructure, ensuring its foundational role in national energy mixes for the foreseeable future.

Another significant driver stems from the advancements in thermal power generation technologies aimed at improving efficiency and reducing environmental impact. Modern thermal plants are designed with supercritical and ultra-supercritical technologies that operate at higher temperatures and pressures, significantly increasing fuel efficiency and reducing greenhouse gas emissions per unit of electricity generated. The ongoing research and development into carbon capture, utilization, and storage (CCUS) technologies also provide a pathway for existing and new thermal plants to meet stringent environmental regulations, thereby extending their operational lifespans and addressing climate change concerns. These technological innovations not only enhance performance but also contribute to the long-term viability and sustainability of thermal power, driving continued investment in these upgraded systems.

| Drivers | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Increasing Global Electricity Demand | +1.2% | Asia Pacific, Latin America, Africa | Long-term (2025-2033) |

| Industrialization and Urbanization in Developing Economies | +0.9% | China, India, Southeast Asia | Medium to Long-term |

| Technological Advancements in Efficiency and Emissions Reduction | +0.7% | Global, particularly developed nations | Continuous |

| Reliability and Base-load Power Generation Needs | +0.6% | All regions, especially grid-constrained areas | Long-term |

| Lower Fuel Costs for Certain Thermal Sources (e.g., Coal in some regions) | +0.4% | Asia Pacific, Eastern Europe | Short to Medium-term |

Thermal Power Plant Market Restraints Analysis

Stringent environmental regulations and growing global concerns over climate change represent a significant restraint on the thermal power plant market. Governments worldwide are implementing stricter emission standards for pollutants like sulfur dioxide, nitrogen oxides, and particulate matter, as well as imposing carbon pricing mechanisms or cap-and-trade systems. These regulations necessitate substantial investments in emission control technologies, such as flue gas desulfurization (FGD) and selective catalytic reduction (SCR) systems, which significantly increase the capital and operational costs of thermal plants. The increasing pressure to reduce greenhouse gas emissions, particularly from coal-fired plants, often leads to delays in project approvals, cancellation of new projects, or even the early retirement of older, less efficient plants, thereby hindering market expansion.

The accelerating cost competitiveness and deployment of renewable energy sources such as solar and wind power pose another substantial restraint. As renewable technologies mature and economies of scale are achieved, their levelized cost of electricity (LCOE) continues to decline, making them increasingly attractive alternatives for new power generation capacity. This shift in investment preference towards renewables, coupled with government incentives and mandates for clean energy, diverts capital away from thermal power projects. Additionally, public and investor sentiment is increasingly favoring green investments, making it challenging for thermal power projects to secure financing, especially for coal-fired power. This competitive pressure from renewables, combined with shifting investment trends, directly impacts the growth trajectory of the thermal power plant market.

| Restraints | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Stringent Environmental Regulations and Emission Standards | -1.5% | North America, Europe, China | Long-term |

| Increasing Competitiveness of Renewable Energy Sources | -1.2% | Global, particularly developed markets | Continuous |

| High Capital Costs and Long Construction Timelines | -0.8% | Global | Medium to Long-term |

| Fluctuations in Fossil Fuel Prices | -0.6% | Global | Short to Medium-term |

Thermal Power Plant Market Opportunities Analysis

The widespread adoption of advanced technologies for efficiency enhancement and emissions reduction presents a significant opportunity for the thermal power plant market. Investments in supercritical and ultra-supercritical combustion technologies, combined cycle gas turbines (CCGT), and integrated gasification combined cycle (IGCC) systems can drastically improve fuel efficiency and lower the carbon footprint of thermal power generation. Beyond core combustion, opportunities lie in optimizing auxiliary systems, implementing advanced control systems (like AI and IoT-based solutions), and integrating waste heat recovery systems. These technological upgrades not only help meet environmental compliance but also enhance operational profitability by reducing fuel consumption and increasing output, allowing existing plants to extend their operational lives and new projects to secure viability.

Another major opportunity arises from the development and commercialization of Carbon Capture, Utilization, and Storage (CCUS) technologies. As global efforts to decarbonize intensify, CCUS offers a pathway for thermal power plants to capture significant portions of their CO2 emissions before they enter the atmosphere. While currently expensive, ongoing research and government incentives are driving down costs and improving the scalability of these technologies. Furthermore, the concept of hydrogen co-firing or 100% hydrogen-fired turbines for natural gas plants presents a transformative opportunity. As green hydrogen production scales up, this could allow gas-fired thermal plants to operate with virtually zero carbon emissions, positioning them as a critical component of a future clean energy system that still requires dispatchable, reliable power. These innovative solutions offer a lifeline for the thermal power sector to align with climate goals.

| Opportunities | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Adoption of Carbon Capture, Utilization, and Storage (CCUS) Technologies | +1.1% | North America, Europe, Asia Pacific | Medium to Long-term |

| Modernization and Retrofitting of Existing Plants | +0.9% | Global, especially developed economies | Continuous |

| Increased Use of Natural Gas and Biomass as Cleaner Fuels | +0.8% | Global, particularly emerging economies | Medium-term |

| Integration of Digitalization and AI for Optimization | +0.7% | Global | Short to Medium-term |

Thermal Power Plant Market Challenges Impact Analysis

One of the primary challenges confronting the thermal power plant market is the increasingly negative public perception and investor reluctance driven by environmental concerns. As climate change becomes a more pressing global issue, coal-fired power plants, in particular, are viewed as major contributors to greenhouse gas emissions and air pollution. This perception often leads to public protests, lobbying efforts against new thermal projects, and increased scrutiny from environmental organizations. Consequently, institutional investors, banks, and financial institutions are increasingly divesting from fossil fuel projects and setting strict environmental, social, and governance (ESG) criteria, making it significantly harder for thermal power plants to secure necessary financing and insurance, particularly for long-term projects, thereby stifling growth and development.

Another significant challenge for thermal power plants is the integration into grids with high penetrations of intermittent renewable energy sources. As solar and wind power capacities expand, the need for flexible, dispatchable power to balance the grid when renewables are not generating becomes paramount. While thermal plants can provide this flexibility, frequent cycling (starting up and shutting down, or ramping output up and down rapidly) due to renewable intermittency can lead to increased wear and tear on equipment, reduced efficiency, and higher operational costs. Adapting existing thermal plants to operate efficiently under these cycling conditions, or designing new plants with enhanced flexibility, requires significant technological upgrades and operational adjustments. This dynamic grid environment poses complex technical and economic challenges that thermal power plant operators must overcome to remain competitive and essential for grid stability.

| Challenges | (~) Impact on CAGR % Forecast | Regional/Country Relevance | Impact Time Period |

|---|---|---|---|

| Negative Public Perception and Investor Reluctance | -1.0% | Global, especially developed nations | Long-term |

| Integration with Intermittent Renewable Energy Sources | -0.9% | Europe, North America, Australia | Continuous |

| Aging Infrastructure and High Maintenance Costs | -0.7% | North America, Europe | Medium-term |

| Cybersecurity Threats to Critical Infrastructure | -0.5% | Global | Continuous |

Thermal Power Plant Market - Updated Report Scope

This comprehensive market research report provides an in-depth analysis of the global thermal power plant market, offering detailed insights into market dynamics, segmentation, regional trends, and competitive landscape. It covers the current market scenario, historical data, and future growth projections, enabling stakeholders to make informed strategic decisions and capitalize on emerging opportunities within the energy sector. The report specifically addresses the impact of technological advancements, environmental policies, and evolving energy demands on market growth.

| Report Attributes | Report Details |

|---|---|

| Base Year | 2024 |

| Historical Year | 2019 to 2023 |

| Forecast Year | 2025 - 2033 |

| Market Size in 2025 | USD 985.4 Billion |

| Market Forecast in 2033 | USD 1385.2 Billion |

| Growth Rate | 3.8% (CAGR from 2025 to 2033) |

| Number of Pages | 247 |

| Key Trends |

|

| Segments Covered |

|

| Key Companies Covered | General Electric, Siemens Energy, Mitsubishi Heavy Industries, Toshiba Energy Systems & Solutions, Doosan Enerbility, Harbin Electric, Dongfang Electric Corporation, Shanghai Electric, Bharat Heavy Electricals Limited, BHEL, IHI Corporation, Babcock & Wilcox Enterprises, Valmet, EDF, Enel, RWE, Adani Power, NTPC Limited, Korea Electric Power Corporation, JERA Co., Inc., Southern Company |

| Regions Covered | North America, Europe, Asia Pacific (APAC), Latin America, Middle East, and Africa (MEA) |

| Speak to Analyst | Avail customised purchase options to meet your exact research needs. Request For Analyst Or Customization |

Segmentation Analysis

The thermal power plant market is comprehensively segmented to provide a granular understanding of its diverse components and drivers. These segments offer insights into various aspects of power generation, including the primary energy sources utilized, the sophistication of technologies employed, the scale of power generation facilities, and the ultimate application of the generated electricity. Understanding these segments is crucial for stakeholders to identify specific growth areas, assess competitive landscapes, and formulate targeted strategies within the evolving energy sector. The segmentation highlights the market's complexity and its adaptation to both traditional and emerging power generation paradigms, considering efficiency, environmental impact, and economic viability across different applications.- By Fuel Type: This segment categorizes thermal power plants based on the primary fuel source used for electricity generation.

- Coal-Fired: Includes plants utilizing pulverized coal, fluidized bed combustion (FBC) for better emissions control, and advanced integrated gasification combined cycle (IGCC) technology.

- Gas-Fired: Comprises plants using natural gas, including highly efficient combined cycle gas turbines (CCGT), simpler open cycle gas turbines, and combined heat and power (CHP) or cogeneration facilities.

- Oil-Fired: Power plants primarily running on various forms of fuel oil.

- Biomass & Waste-to-Energy: Facilities that generate electricity from organic matter or municipal and industrial waste.

- Nuclear Power: Although not "thermal" in the traditional sense, nuclear power plants utilize steam turbines generated by nuclear fission, thus their steam cycle components are considered within this broader market context for relevant equipment and services.

- By Technology: This segment focuses on the specific engineering and operational designs of thermal power plants that impact efficiency and emissions.

- Subcritical: Older generation technology with lower steam parameters.

- Supercritical: Operates at higher pressures and temperatures than subcritical, leading to improved efficiency.

- Ultra-Supercritical: The most advanced conventional coal technology, offering even greater efficiency and lower emissions due to extreme steam conditions.

- Combined Cycle: Integrates gas and steam turbines to maximize efficiency from gas combustion.

- Cogeneration/CHP: Systems producing both electricity and useful heat simultaneously.

- Fluidized Bed Combustion (FBC): Technology designed for burning various fuels efficiently with reduced emissions.

- By Capacity: This segmentation classifies power plants based on their power output, reflecting scale and investment levels.

- Small (Up to 100 MW): Typically serving localized industrial needs or smaller grids.

- Medium (101 MW - 500 MW): Mid-sized plants suitable for regional power supply.

- Large (Above 500 MW): Major utility-scale plants forming the backbone of national grids.

- By End-Use: This segment identifies the primary consumers or applications of the electricity generated by thermal power plants.

- Utilities: Large-scale power generation for public consumption and grid supply.

- Industrial: Power plants dedicated to specific industrial processes (e.g., cement, steel, chemical manufacturing) often for self-consumption or co-generation.

- Commercial: Smaller scale thermal power for commercial establishments.

Regional Highlights

- Asia Pacific (APAC) is projected to remain the dominant region in the thermal power plant market, primarily driven by robust industrialization, rapid urbanization, and the immense growth in electricity demand from countries like China, India, and Indonesia. Despite a global push towards renewables, the sheer scale of energy requirements in these emerging economies necessitates continued reliance on and investment in thermal power, particularly coal-fired, to provide stable base-load electricity. There's also a significant focus on upgrading existing subcritical plants to more efficient supercritical and ultra-supercritical technologies to meet environmental targets while ensuring energy security.

- North America is characterized by a mature thermal power market undergoing significant transformation. The region is witnessing a gradual shift away from coal-fired power towards natural gas, driven by abundant shale gas resources and increasingly stringent environmental regulations. The emphasis here is on modernization of existing natural gas and remaining coal plants for enhanced efficiency, flexibility, and integration with a growing renewable energy grid. Investments are increasingly focused on carbon capture and storage (CCS) technologies and hydrogen co-firing pilots to decarbonize the thermal fleet.

- Europe leads in the decarbonization efforts, with many countries phasing out coal power plants and prioritizing renewable energy. However, thermal power, particularly natural gas plants, remains crucial for grid stability and security of supply, acting as a flexible backup to intermittent renewables. The market trend in Europe involves significant investments in CCUS technologies, hydrogen-ready gas turbines, and advanced digital solutions for optimal plant operation and emissions monitoring, aiming for a cleaner and more responsive thermal fleet.

- Middle East and Africa (MEA) present a mixed but growing landscape. The Middle East, with its vast oil and gas reserves, sees continued investment in gas-fired thermal power plants to meet escalating domestic electricity demand from population growth and industrial expansion. Efficiency improvements and combined cycle technologies are key. In Africa, many nations face significant energy deficits, leading to continued development of thermal power infrastructure, especially coal in certain resource-rich areas and gas in others, to support economic development and electrification initiatives.

- Latin America exhibits a diverse energy mix, with a growing need for reliable power. While hydro and renewables are prominent, thermal power plants, predominantly gas-fired, play a vital role in ensuring grid stability, especially during droughts affecting hydropower. The region sees moderate investment in new gas-fired capacity and efficiency upgrades to existing plants, balancing energy security with a gradual transition towards cleaner sources.

Top Key Players:

The market research report covers the analysis of key stake holders of the Thermal Power Plant Market. Some of the leading players profiled in the report include -:- General Electric

- Siemens Energy

- Mitsubishi Heavy Industries

- Toshiba Energy Systems & Solutions

- Doosan Enerbility

- Harbin Electric

- Dongfang Electric Corporation

- Shanghai Electric

- Bharat Heavy Electricals Limited (BHEL)

- IHI Corporation

- Babcock & Wilcox Enterprises

- Valmet

- EDF

- Enel

- RWE

- Adani Power

- NTPC Limited

- Korea Electric Power Corporation (KEPCO)

- JERA Co., Inc.

- Southern Company

Frequently Asked Questions:

What is the projected growth rate for the Thermal Power Plant Market?

The Thermal Power Plant Market is projected to grow at a Compound Annual Growth Rate (CAGR) of 3.8% between 2025 and 2033. This growth is underpinned by persistent global electricity demand, ongoing industrialization in developing economies, and continuous technological advancements aimed at improving efficiency and reducing environmental impact within the sector. While facing competition from renewables, thermal power plants continue to be essential for providing stable base-load power.

What are the primary drivers of the Thermal Power Plant Market?

Key drivers for the Thermal Power Plant Market include the increasing global electricity demand, particularly from rapidly industrializing and urbanizing economies in Asia Pacific and other emerging regions. The inherent reliability and capability of thermal plants to provide base-load power and grid stability are also crucial drivers. Furthermore, ongoing technological advancements in areas such as supercritical and ultra-supercritical combustion, as well as the development of carbon capture, utilization, and storage (CCUS) technologies, are driving investments aimed at enhancing efficiency and mitigating environmental concerns.

How do environmental regulations impact the Thermal Power Plant Market?

Environmental regulations significantly restrain the Thermal Power Plant Market by imposing stringent emission standards for pollutants and greenhouse gases. These regulations necessitate substantial investments in abatement technologies, increasing operational costs, and often leading to the cancellation of new projects or early retirement of older, less efficient plants. However, these regulations also create opportunities for innovation in cleaner thermal technologies, such as advanced gas turbines, biomass co-firing, and CCUS, pushing the market towards more sustainable practices.

What role does AI play in the future of Thermal Power Plants?

Artificial Intelligence (AI) is set to play a transformative role in the future of Thermal Power Plants by enhancing operational efficiency, predictive maintenance, and overall plant management. AI algorithms can optimize combustion processes, predict equipment failures, and improve real-time control, leading to reduced fuel consumption, lower emissions, and increased uptime. Furthermore, AI-powered forecasting models will enable thermal plants to better integrate with intermittent renewable energy sources, ensuring grid stability and more efficient dispatch of power.

Which region is expected to dominate the Thermal Power Plant Market and why?

The Asia Pacific (APAC) region is expected to dominate the Thermal Power Plant Market throughout the forecast period. This dominance is primarily attributed to the massive and continuously growing electricity demand driven by rapid industrialization, urbanization, and population growth in countries such as China, India, and Southeast Asian nations. Despite significant renewable energy deployment, the sheer scale of energy needs and the requirement for stable base-load power mean that thermal power plants remain a critical component of the energy mix in these economies, leading to ongoing investments in new capacity and efficiency upgrades.

| Single User | : $3680 |

|---|---|

| Multi User | : $5680 |

| Corporate User | : $6400 |

Buy Now

Secure SSL Encrypted